The Giant Debt-for-Equity Swap

I wrote this article in December 2019. Much has changed but with bond yields heading lower on the back of more QE, it still seems surprisingly valid.

The Giant Debt-for-Equity Swap

I wrote this article in December 2019. Much has changed but with bond yields heading lower on the back of more QE, it still seems surprisingly valid.

![]()

Macro Letter – No 128 – 17-04-2020

A Rose by Any Other Name – Corona Bonds and the Future of the Eurozone

On April 9th the Eurogroup of Finance Ministers eventually agreed upon a three-pronged package to avert some of the economic impact of the Covid-19 pandemic. For financial markets this was a relief, had the Eurogroup broken up, for the second time in a week, without a deal markets would have reacted badly. The three-pronged package included health expenditure funding from the European Stability Mechanism (ESM), loans for businesses from the European Investment Bank (EIB) and further funding from the European Commission’s unemployment fund. The total package is a modest Euro 540bln, the political ramifications are much less so.

What was not agreed, despite the unprecedented circumstances surrounding the pandemic, was a collective pooling of Eurozone (EZ) resources in the form of ‘Eurobonds,’ deftly renamed ‘Corona Bonds,’ by their advocates. For the fiscally responsible countries of Northern Europe, even the current crisis was insufficient for them to contemplate underwriting the prodigal South.

The compromise, agreed last week, included the use the ESM. The ESM itself, together with the outright monetary transactions (OMT) undertaken by the ECB, were forged in the 2010/2012 Eurozone crisis. At that time the convergence of Eurozone government bond yields, which had begun long before the advent of the Euro, was unravelling as investors realised that Europe would not collectively underwrite any individual state’s obligations. The North/South divide became a chasm, with Greek, Portuguese, Italian and Spanish bond yields rising sharply whilst German, Dutch and Finnish yields declined. The potential default of a Eurozone government was only averted by the actions of the then President of the ECB, Mario Draghi, when he stated that the central bank would do, ‘Whatever it takes.’

Once again, a motley deal has been forged, recriminations will follow. Whilst lower government financing costs remain a major attraction of EZ membership for newer members of the EU, the benefit is by no means guaranteed, as this 2017 paper – Eurozone Debt Crisis and Bond Yields Convergence: Evidence from the New EU Countries – by Minoas Koukouritakis, reveals: –

Based on the empirical results, there is some clear evidence of strong monetary policy convergence for each of the Czech Republic, Lithuania and Slovakia to Germany. Alternatively, under the UIP and ex-ante relative PPP conditions, the expected inflation rate of these three countries has converged to the expected inflation rate of Germany. This is an expected result not only because Lithuania and Slovakia are already Eurozone members, but also because Germany plays a very important role in the economies of these three countries. Furthermore, the empirical results provide evidence of weak monetary policy convergence for each of Croatia and Romania to Germany. In contrast, for the remaining seven new EU countries, namely Bulgaria, Cyprus, Hungary, Latvia, Malta, Poland and Slovenia, the empirical evidence suggests yields’ divergence for each of these countries in relation to Germany. For Cyprus, Latvia and Slovenia, which as Eurozone members they have common monetary policy with Germany, the empirical evidence could probably be attributed to the increased sovereign default risk of these countries, which in turn led to large and persistent risk premia.

In summary, the empirical evidence indicates that in the context of the Eurozone debt crisis, even though Germany has established its dominance and sets the macroeconomic policies in the Eurozone, several new EU countries are unable to follow these policies. And this conclusion addresses once more the issue of core-periphery in the Eurozone and, thus, the Eurozone’s future prospects.

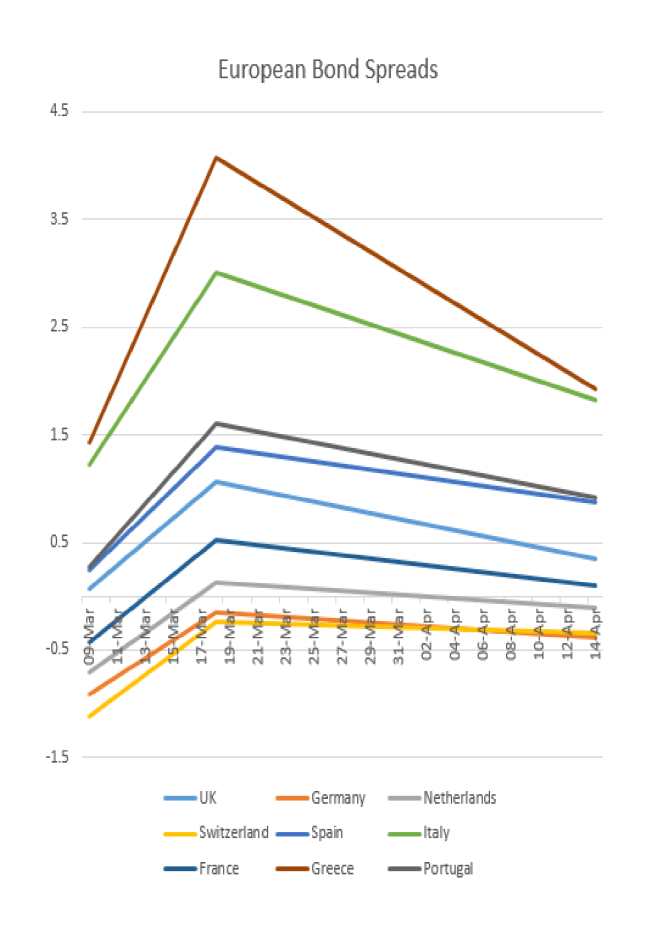

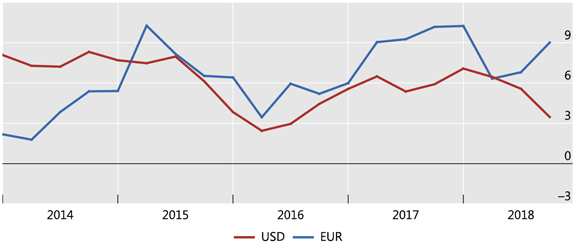

The past six weeks has seen a global fiscal response to the pandemic. Stock markets have declined and credit spreads in corporate bond markets have widened. In European government bonds the pattern has been similar, the migratory flight to quality saw flocks of investors head north, especially into Switzerland and Germany. The simplified chart below shows three data points;

March 9th, when German Bund yields reached their recent nadir,

March 18th, the date investors became spooked by the sheer magnitude of the fiscal response required by EZ governments: and

April 14th, the day on which Italy and Spain announced the first relaxation their lockdown restrictions: –

Source: Trading Economics, Investing.com

There are several observations; firstly, even as the lockdown comes towards its end, bond yields are higher, reflecting concerns about the impact of fiscal spending on government budgets as tax receipts collapse. Secondly, German Bund yields are now lower than Swiss Confederation bonds, despite expectations that Germany may end up footing the bill for the lion’s share of government borrowing across the EZ. This may be a reflection of the lower percentage fatality rate in Germany – 2.5% versus 4.4% in Switzerland – or simply a function of the greater liquidity available in the German bond market.

A third observation concerns the higher yielding countries of Greece, Italy, Portugal and Spain. Despite a larger number of Covid-19 infections, Spanish Bonos have maintained their lower yield relative to Italian BTPs, meanwhile, Greek bonds have converged towards Italy and Portuguese bonds trade within 4bp of Spain.

Convergence, divergence and political will

This is not the first macro letter on the topic of EZ bond convergence, the chart below is taken from Macro Letter – No 10 – 25-04-2014 – The Limits Of Convergence – Eurozone Bond Yield Compression Cracks the second of eight previous articles on subject: –

Source: Bloomberg

At that time I suggested three scenarios: –

The EZ crisis had finally disapated but the full impact of QE had not yet been appreciated, the table below shows the yield to maturity and spread over German Bunds of the 10 year bonds of Italy, Spain, Greece and Portugal traded on 24th April 2014 (roughly six years ago): –

Source: Bloomberg

In April 2014 I saw the second scenario as most likely. I anticipated limited ‘Eurobond’ issuance, this has not yet come to pass, but last week’s stimulus looks like a federal bail-out by any other name. Last month, as the Covid-19 pandemic took hold, the spread between German Bunds and Spanish Bonos touched 1.54%, whilst the spread against Greek bonds reached 4.22% and Portugal, 1.75%. Only Italy fared less well, the Bund/BTP spread reached 3.15; a marked deterioration since 2014.

Conclusions and Investment Opportunities

By the time I penned Macro Letter – No 73 – 24-03-2017 – Can a multi-speed European Union evolve? it was becoming clear that Italy was the focus of concern among fixed income investors. I concluded (a little too late) that: –

Spanish 10yr Bonos represents a better prospect than Italian 10yr BTPs, but one would have to endure negative carry to set up this spread trade: look for opportunities if the spread narrows towards zero.

The spread never returned to parity.

When I last wrote about EZ bonds, I focussed once again on Italy in Macro Letter – No 98 – 08-06-2018 – Italy and the repricing of European government debt. BTP yields had risen to a spread of 1.22% over Spanish Bonos and I expected a retracement. As the chart below reveals, BTP yields rose further before than regained composure: –

Source: Y-Charts

Eurobonds are still not on the agenda even in a time of pandemic, therefore, Italian indebtedness remains the single greatest risk to the stability of the EZ. The convergence trade is fraught with geopolitical risk as cracks in the European Project are patched and papered over. Now is not the time for revolution, but the ongoing fiscal strain of the pandemic means the policy of issuing Eurobonds backed by a European guarantor will not go away. I expect EZ government bond yield compression accompanied by occasional violent reversals to become the pattern during the next few years, together with increasing political tension between European countries north and south.

![]()

Macro Letter – No 125 – 17-01-2020

US Bonds – 2030 Vision – A decade in the doldrums

Having reached their yield low at 1.32% in July 2016, US 10yr bond yields have been locked in, just shy of, a 2% range for the last two and half years (subsequent high 3.25% and low 1.43%). For yields to fall again, supply must fall, demand rise or central banks, recommence their experimental monetary policies of negative interest rates and quantitative easing. For yields to rise, supply must rise, demand fall or central banks, reverse their multi-year largesse. Besides supply, demand and monetary policy there are, however, other factors to consider.

Demographics

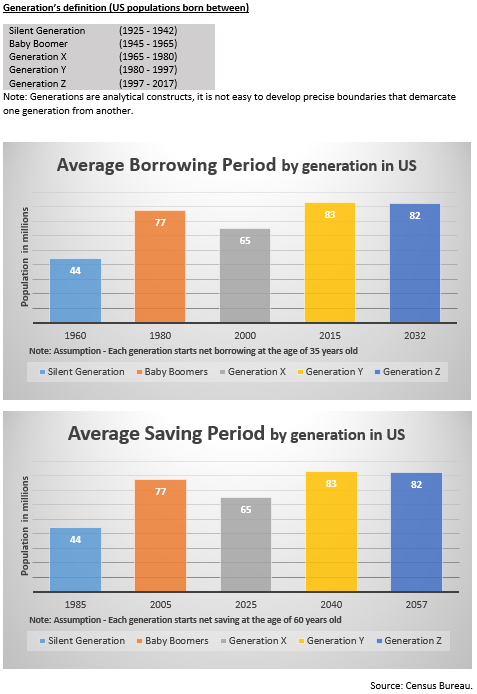

One justification for a rise in US bond yields would be an uptick in inflationary pressure. Aging demographic have been the principal driver of the downward trajectory of secular inflation. During the next decade, however, Generation Y borrowing will accelerate whilst Generation X has yet to begin their aggressive saving spree. The table below looks at the borrowing and saving patterns of the demographic cohorts in the US: –

Source: US Census Bureau

Excepting the obesity and opioid epidemics, life expectancy will, nonetheless, continue to extend. The Gen Y borrowing binge will not override the aging demographic effect. It’s influence on the inflation of the next decade is likely to be modest (on these grounds alone we will not see the return of double-digit inflation) and the longer term aging trend, bolstered by improvements in healthcare, will return with a vengeance during the 2030’s, undermining the last vestiges of current welfare provisions. Much more saving will be required to pay for the increasing cost of healthcare and pensions. With bond yields of less than 4%, an aging (and hopefully healthier) population will need to continue working well beyond current retirement age in order to cover the shortfall in income.

Technology

Another secular factor which has traditionally kept a lid on inflation has been technology. As Robert Solo famously observed back in 1987, ‘You can see the computer age everywhere but in the productivity statistics.’ Part of the issue is that productivity is measured in currency terms. If the price of a computer remains unchanged for a decade but its capacity to compute increases 10-fold over the same period, absent new buyers of computers, new sales are replacements. In this scenario, the improvement in productivity does not lead to an uptick in economic growth, but it does demonstrably improve our standard of living.

Looking ahead the impact of machine learning and artificial intelligence is just beginning to be felt. Meanwhile, advances in robotics, always a target of the Luddite fringe, have been significant during the last decade, spurred on by the truncation of global supply chains in the wake of the great financial crisis. This may be to the detriment of frontier economies but the developed world will reap the benefit of cheaper goods.

Central Bank Omnipotence

When Paul Volcker assumed the helm of the Federal Reserve in the late 1970’s, inflation was eroding any gains from investment in government bonds. Armed with Friedman’s monetary theories, the man who really did remove the punch-bowl, raised short-term rates to above the level of CPI and gradually forced the inflation genie back into its bottle.

After monetary aggregate targets were abandoned, inflation targeting was widely adopted by many central banks, but, as China joined the WTO (2001) and exported their comparative advantage in labour costs to the rest of the world, those same central bankers’, with Chairman Bernanke in the vanguard, became increasingly petrified by the prospect of price deflation. Memories of the great depression and the monetary constraints of the gold exchange standard were still fresh in their minds. For an economy to expand, it was argued, the supply of money must expand in order to maintain the smooth functioning of markets: a lack of cash would stifle economic growth. Inflation targets of around 2% were deemed appropriate, even as technological and productivity related improvements insured that the prices of many consumer goods actually declined in price.

Inflation and deflation can be benign or malign. Who does not favour a stock market rally? Yet, who cares to witness their grocery bill spiral into the stratosphere? Who cheers when the latest mobile device is discounted again? But does not panic when the value of their property (on which the loan-to-value is already a consumption-sapping 90%) falls, wiping out all their equity? Blunt inflation targeting is frankly obtuse, but it remains the mandate of, perhaps, the most powerful unelected institutions on the planet.

When economic historians look back on the period since the collapse of the Bretton Woods agreement, they will almost certainly conclude that the greatest policy mistake, made by central banks, was to disregard asset price inflation in their attempts to stabilise prices. Meanwhile, in the decade ahead, upside breaches of inflation targets will be largely ignored, especially if growth remains anaemic. Central bankers’, it seems, are determined to get behind the curve, they fear the severity of a recession triggered by their own actions. In the new era of open communications and forward guidance they are reticent to increase interest rates, too quickly or by too great a degree, in such a heavily indebted environment. I wrote more about this in November 2018 in The Self-righting Ship – Debt, Inflation and the Credit Cycle: –

The current level of debt, especially in the developed economies, seems to be acting rather like the self-righting ship. As economic growth accelerates and labour markets tighten, central banks gradually tighten monetary conditions in expectation of inflation. As short-term rates increase, bond yields follow, but, unlike the pattern seen in the higher interest rate era of the 1970’s and 1980’s, the effect of higher bond yields quickly leads to a tempering of credit demand.

Some commentators will rightly observe that this phenomenon has always existed, but, at the risk of saying ‘this time it’s different,’ the level at which higher bond yields act as a break on credit expansion are much lower today in most developed markets.

Conclusions and Investment Opportunities

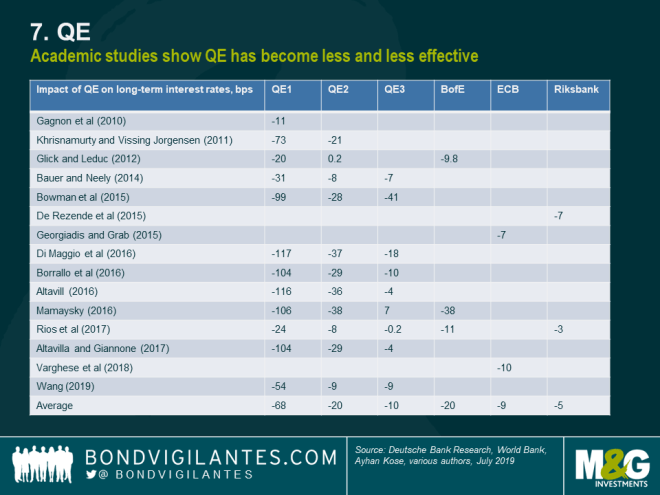

There have been several drivers of disinflation over the past decade including a tightening of bank regulation, increases in capital requirements and relative fiscal austerity. With short-term interest rates near to zero in many countries, governments will find themselves compelled to relax regulatory impediments to credit creation and open the fiscal spigot, at any sign of a recession, after all, central bank QE appears to have reached the limits of its effectiveness. The table below shows the diminishing returns of QE over time: –

Source: M&G, Deutsche Bank, World Bank

Of course the central banks are not out of ammunition just yet, the Bank of Japan experiment with qualitative easing (they currently purchase ETFs, common stock may be next on their agenda) has yet to be adopted elsewhere and the Federal Reserve has so far resisted the temptation to follow the ECB into corporate bond acquisition.

For the US bond market the next decade may well see yields range within a relatively narrow band. There is the possibility of new record lows, but the upside is likely to be constrained by the overall indebtedness of both the private and public sector.

![]()

Macro Letter – No 123 – 29-11-2019

Leveraged Loans – History Rhyming?

For those of you who have not read Michael Lewis’s, The Big Short, the great financial crisis of 2008/2009 was caused by too much debt. The sector which precipitated the great unravelling was the US mortgage market and the particular instrument of mass destruction was the collateralised debt obligation, a security that turned out to be far from secure.

Today, more than a decade on from the crisis, interest rates are close to historic lows throughout much of the developed world. The problem of too much debt has been solved with even more debt. The nature of the debt has changed, so too has the make-up of debtors and creditors, but the very low level of interest rates, when compared to 2008, means that small changes in interest rates have a greater impact the price of credit.

Here is a hypothetical example, to explain the changed relationship between interest rates and credit. Back in 2008 a corporate borrower might have raised capital by issuing debt paying 6%, today the same institution can borrow at 3%. This means they can double the amount of capital raised by debt financing without any change in their annual interest bill. Put another way, apart from the repayment of the principal, which can usually be rolled over, the cost of debt financing has halved over the course of the decade. Firms can raise capital by issuing equity or debt, but, as interest rates decline, debt has become cheaper than equity finance.

In the example above, however, assuming the corporation chooses to double its borrowings, it becomes twice as sensitive to changes in interest rates. A rise from 3% to 4% increases its interest payments by one third, whereas, previously, a rise from 6% to 7% amounted to an increase of just one sixth.

So much for the borrower, but what about the lender? Bonds and other interest bearing securities are generally purchased by investors who need to secure a stable, long-term, stream of fixed income. As interest rates fall they are faced with a dilemma, either accept a lower return or embrace greater risk of default to achieve the same income. At the heart of the financial crisis was the illusion of the free lunch. By securitising a diversified portfolio of high-risk debt, the individual default risk was supposed to be ameliorated. The supposition was that non-correlated investments would remain non-correlated. There is a saying in financial markets, ‘during a crisis, correlations all rise to one.’ In other words, diversification seldom works when you really need it because during a crisis every investor wants the same thing, namely liquidity. Even if the default risk remains unchanged, the market liquidity risk contrives to wipe the investor out.

An alternative to a fixed-income security, which may be especially attractive in a rising interest rate environment (remember the Fed was tightening for a while prior to 2019), is a floating-rate investment. In theory, as short-term interest rates rise the investor can reinvest at more attractive rates. If the yield curve is essentially flat, floating rate investments will produce similar income streams to longer maturity investments, but they will be less sensitive to systemic market risk because they have shorter duration. In theory, credit risk should be easier to manage.

What’s new?

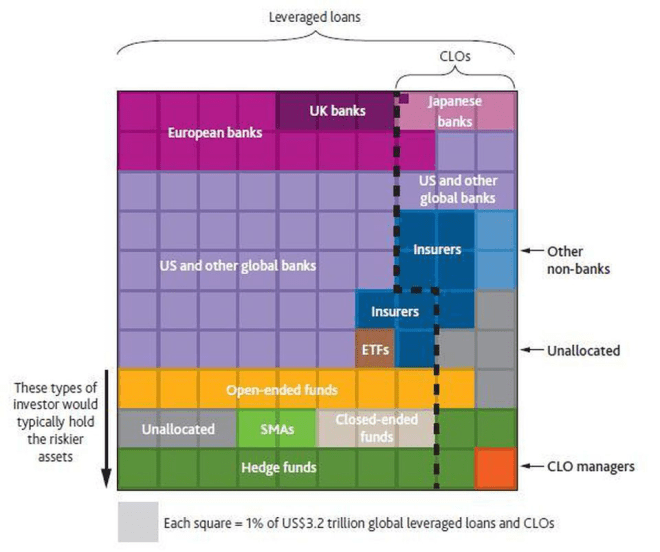

More than ten years into the recovery, we are witnessing one of the longest equity bull-markets in history, but it has been driven almost entirely by falling interest rates. The bond market has also been in a bull-trend, one which commenced in the early 1980’s. For investors, who cannot stomach the uncertainty of the equity market, the fixed income market is a viable alternative, however, as government bond yields have collapsed, income-yielding investments have been increasingly hard to find. With fixed income losing its lustre, credit products have sought to fill the void. Floating-rate leveraged loans, often repackaged as a collateralised loan obligation (CLO), are proving a popular alternative source of income.

The typical CLO is a floating-rate tradable security backed by a pool of, usually, first-lien loans. Often these are the debt of corporations with poor credit ratings, such as the finance used by private equity firms to facilitate leveraged buyouts. On their own, many of these loans rank on the margins of investment grade but, by bundling them together with better rated paper, CLO managers transform base metal into gold. The CLO manager does not stop there, going on to dole out tranches, with different credit risks, to investors with differing risk appetites. There are two general types of tranche; debt tranches, which pay interest and carry a credit rating from an independent agency, and equity tranches, which give the purchaser ownership in the event of the sale of the underlying loans. CLOs are hard to value, they are actively managed meaning their risk profile is in a constant state of flux.

CLOs are not new instruments and studies have shown that they are subject to lower defaults than corporate bonds. This is unsurprising since the portfolios are diversified across many businesses, whilst corporate bonds are the debt of a single issuer. CLO issuers argue that corporations are audited unlike the liar loans of the sub-prime mortgage debacle and that banks have passed ‘first loss’ risk on to third parties. I am not convinced this will save them from a general collapse in confidence. Auditors can be deceived and the owners of the ‘first loss’ exposure will need to hedge. CLOs may be diversified across multiple industry sectors but the market price of the underlying loans will remain highly dependent on that most transitory of factors, liquidity.

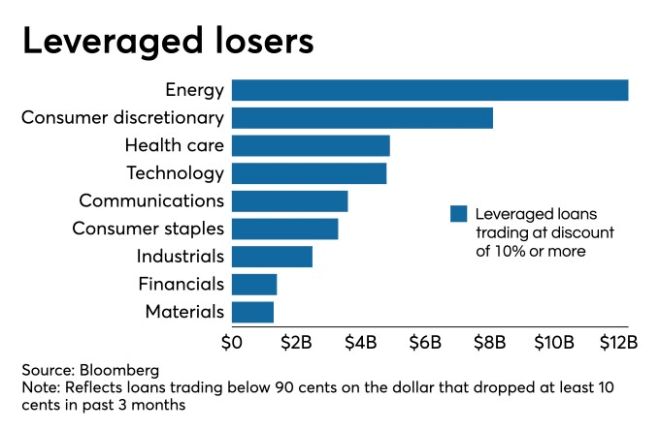

Where are we now?

Enough of the theory, in practice many CLOs are turning toxic. According to an October article in the American Banker – A $40 billion pile of leveraged loans is battered by big losses – the loans of more than 50 companies have seen their prices decline by more than 10%. The slowing economy appears to be the culprit, credit rating agencies are, as always, reactive rather than proactive, so the risk that many CLOs may soon cease to be investment grade is prompting further selling, despite the absence of actual credit downgrades. The table below shows magnitude of the problem as at the beginning of last month: –

Source: Bloomberg

It is generally agreed that the notional outstanding issuance of US$ leveraged loans is around $1.2trln, of which some $660bln (55%) are held in CLOs, however, a recent estimate from the Bank of England – How large is the leveraged loan market? suggests that the figure is closer to $1.8trln. The authors go on to state: –

We estimate that there is more than US$2.2 trillion in leveraged loans outstanding worldwide. This is larger than the most commonly cited estimate and comparable to US subprime before the crisis.

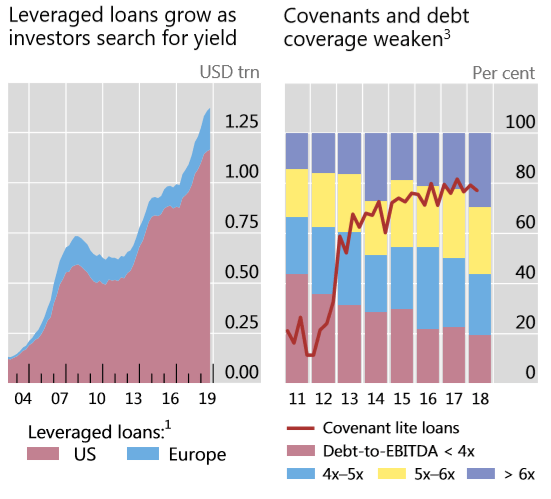

As global interest rates have declined the leveraged loan market has more than doubled in size since its post crisis low of $497bln in 2010. Being mostly floating-rate structures, enthusiasm for US$ loans accelerated further in the wake of Federal Reserve (Fed) tightening of short-term rates. This excess demand has undermined quality, it is estimated that around 80% of US$ and 90% of Euro issues are covenant-lite – in other words they have little detailed financial information, often relying on the EBITDA adjustments calculated by the executives of the corporations issuing the loans. Those loans not held by CLOs sit on the balance sheet of banks, insurance companies and pension funds together with mutual funds and ETFs. Several more recent issues, failing to find a home, sit on the balance sheets of the underwriting banks.

Here is a chart showing the evolution of the leveraged loan market over the last decade: –

Source: BIS

Whilst the troubled loans in the first table above amount to less than 4% of the total outstanding issuance, there appears to be a sea-change in sentiment as rating agencies begin to downgrade some issues to CCC – a notch below investment grade. This grade deflation is important because most CLO’s are not permitted to hold more than 7.5% of CCC rated loans in their portfolios. Some estimates suggest that 29% of leveraged loans are rated just one notch above CCC. Moody’s officially admits that 40% of junk-debt issuers rate B3 and lower. S&P announced that the number of issuers rated B- or lower, referred to as ‘weakest links’, rose from 243 in August to 263 in September, the highest figure recorded since 2009 when they peaked at 300. S&P go on to note that in the largest industry sector, consumer products, downgrades continue to outpace upgrades.

As the right-hand of the two charts above reveals, the debt multiple to earnings of corporate loans is at an all-time high. Not only has the number of issuer downgrades risen but the number of issuers has also increased dramatically. At the end of 2010 there were 658 corporate issuers, by October 2019 the number of issuers had swelled 56% to 1025.

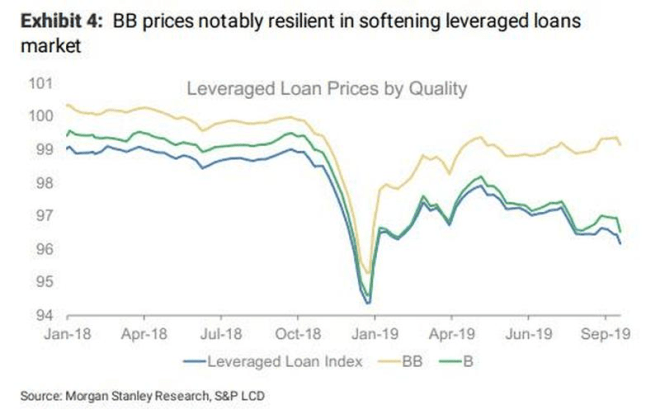

The credit spread between BB and the Leveraged Loan Index has been widening throughout the year despite three rate reductions from the Fed: –

Source: Morgan Stanley, FTSE

Q4 2018 saw a sharp decline in prices as the effect of previous Fed tightening finally took its toll. Then the Fed changed tack, higher grade credit recovered but the Leveraged Loan Index never followed suit.

Despite a small inflow into leveraged loan ETFs in September, the natural buyers of sub-investment grade paper have been unnaturally absent of late. Leveraged loan mutual funds have seen steady investment outflows for almost a year.

The inexperience of the new issuers is matched by the inexperience of the investor base. According to data from Prequin, between 2013 and 2017 a total of 322 funds made direct lending investments of which 71 had never entered the market before, during the previous five year only 85 funds had made investments of which just 19 were novices.

Inexperienced investors often move as one and this is evident in the recent absence of liquidity. The lack of willing buyers also highlights another weakness of the leveraged loan market, a lack of transparency. Many of the loans are issued by private companies, information about their financial health is therefore only available to existing holders of their equity or debt. Few existing holders are inclined to add to their exposure in the current environment. New purchasers are proving reticence to fly blind, as a result liquidity is evaporating further just at the moment it is most needed.

If the credit ratings of leveraged loans deteriorate further, contagion may spill over into the high-yield bond market. Whilst the outstanding issuance of high-yield bonds has been relatively stable, the ownership, traditionally insurers and pension funds, has been swelled by mutual fund investors and holders of ETFs. These latter investors prize liquidity more highly than longer-term institutions: the overall high-yield investor base has become less stable.

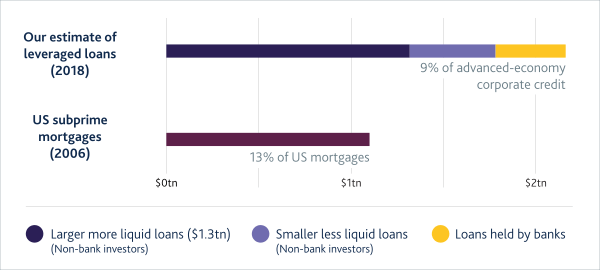

Inevitably, commentators are beginning to draw parallels with mortgage and CDO crisis. The table below, from the Bank of England report, compares leveraged loans today with sub-prime mortgages in 2006: –

Source: Bank of England

The comparisons are disquieting, the issuers and underlying assets of the leveraged loan market may be more diversified than the mortgages of 2006, but, with interest rates substantially lower today, the sensitivity of the entire market, to a widening of credit spreads, is considerably greater.

The systemic risks posed by a meltdown in the CLO market is not lost on the BIS, page 11 of the latest BIS Quarterly Review – Structured finance then and now: a comparison of CDOs and CLOs observes: –

…the deteriorating credit quality of CLOs’ underlying assets; the opacity of indirect exposures; the high concentration of banks’ direct holdings; and the uncertain resilience of senior tranches, which depend crucially on the correlation of losses among underlying loans.

These are all factors to watch closely. The authors’ remain sanguine, however, pointing out that CLOs are generally less complex than CDOs, containing little credit default swap or resecuritisation exposure. They also note that CLOs are less frequently used as collateral in repurchase agreements rendering them less likely to be funded by short-term capital. This last aspect is a double-edge sword, if a security has a liquid repo market it can easily be borrowed and lent. A liquid repo market allows additional leverage but it also permits short-sellers to provide essential liquidity during a buyers strike, in the absence of short-sellers there may be no one to provide liquidity at all.

In terms of counterparties, the table below shows which institutions have the largest exposure to leveraged loans: –

Source: Bank of England

Bank exposure is preeminent but the flow from CLOs will strain bank balance sheets, especially given the lack of repo market liquidity.

Conclusions and Investment Opportunities

The CLO and leveraged loan market has the capacity to destabilise the broader financial markets. Rate cuts from the Fed have been insufficient to support prices and economic headwinds look set to test the underlying businesses in the next couple of years. A further slashing of rates and balance sheet expansion by the Fed may be sufficient to stave off a 2008 redux but the warning signs are flashing amber. Total financial market leverage is well below the levels that preceded the financial crisis of 2008, but as Mark Twain is purported to have said, ‘History doesn’t repeat but it rhymes.’

Until the US election in November 2020 is past, equity markets should remain supported. Government bond yields are unlikely to rise and, should signs of economic weakness materialise, may plumb new lows. Credit spread widening, however, even as government bond yields decline, is a pattern which will become more prevalent as the cash-flow implications of floating-rate borrowing instil some much needed sobriety into the market for leveraged loans. With interest rates close to historic lows credit markets are, once again, the weakest link.

![]()

Macro Letter – No 118 – 12-06-2019

Low yield, no yield, negative yield – Buy now but don’t forget to sell

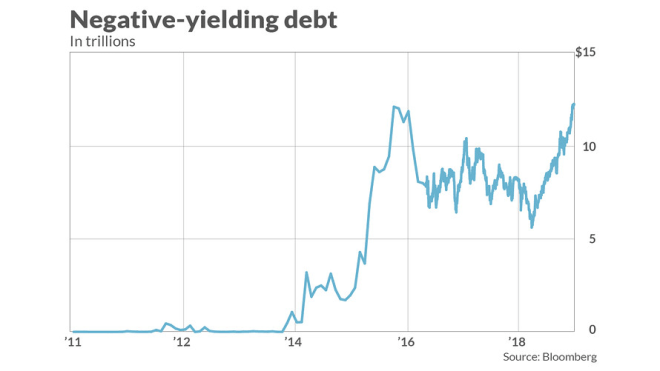

To many onlookers, since the great financial crisis, the world of fixed income securities has become an alien landscape. Yields on government bonds have fallen steadily across all developed markets. As the chart below reveals, there is now a record US$13trln+ of negative yielding fixed income paper, most of it issued by the governments’ of Switzerland, Japan and the Eurozone: –

Source: Bloomberg

The percentage of Eurozone government bonds with negative yields is now well above 50% (Eur4.3trln) and more than 35% trades with yields which are more negative than the ECB deposit rate (-0,40%). If one adds in investment grade corporates the total amount of negative yielding bonds rises to Eur5.3trln. Earlier this month, German 10yr Bund yields dipped below the deposit rate for the first time, amid expectations that the ECB will cut rates by another 10 basis points, perhaps as early as September.

The idea that one should make a long-term investment in an asset which will, cumulatively, return less at the end of the investment period, seems nonsensical, except in a deflationary environment. With most central banks committed to an inflation target of around 2%, the Chinese proverb, ‘we live in interesting times,’ springs to mind, yet, negative yielding government bonds are now ‘normal times’ whilst, to the normal fixed income investor, they are anything but interesting. As Keynes famously observed, ‘Markets can remain irrational longer than I can remain solvent.’ Do not fight this trend, yields will probably turn more negative, especially if the ECB cuts rates and a global recession arrives regardless.

Today, government and investment grade corporate debt has been joined by a baker’s dozen of short-dated high yield Euro names. This article from IFR – ‘High-yield’ bonds turn negative – explains: –

About 2% of the euro high-yield universe is now negative yielding, according to Bank of America Merrill Lynch.

That percentage would rise to 10% if average yields fall by a further 35bp, said Barnaby Martin, European credit strategist at the bank.

He said the first signs of negative yielding high-yield bonds emerged about two weeks ago in the wake of Mario Draghi’s speech in Sintra where the ECB president hinted at a further dose of bond buying via the central bank’s corporate sector purchase programme. There are now more than 10 high-yield bonds in negative territory…

The move to negative yields for European high-yield credits is unprecedented; it didn’t even happen in 2016 when the ECB began its bond buying programme.

During Q4, 2018, credit spreads widened (and stock markets declined) amid expectations of further Federal Reserve tightening and an end to ECB QE. Now, stoked by fears of a global recession, rate expectation have reversed. The Fed are likely to ease, perhaps as early as this month. The ECB, under their new broom, Christine Lagarde, is expected to embrace further QE. The corporate sector purchase program (CSPP) which commenced in June 2016, already holds Eur177.8bln of corporate bonds, but increased corporate purchases seem likely; it is estimated that the ECB holds between 25% and 30% of the outstanding Eurozone government bond in issue, near to its self-imposed ceiling of 33%. Whilst the amount in issues is less, the central bank has more flexibility with Supranational and Euro denominated non-EZ Sovereigns (50%) and greater still with corporates (70%). In this benign interest rate environment, a continued compression of credit spreads is to be expected.

Yield compression has been evident in Eurozone government bonds for decades, but now a change in relationship is starting become evident. Even if the ECB does not increase the range of corporate bonds it purchases, its influence, like the rising tide, will float all ships. Bund yields are likely to remain most negative and the government obligations of Greece, the least, but, somewhere between these two poles, corporate bonds will begin to assume the mantle of the ‘nearly risk-free.’ With many Euro denominated high-yield issues trading below the yield offered for comparable maturity Italian BTPs, certain high-yield corporate credit is a de facto alternative to poorer quality government paper.

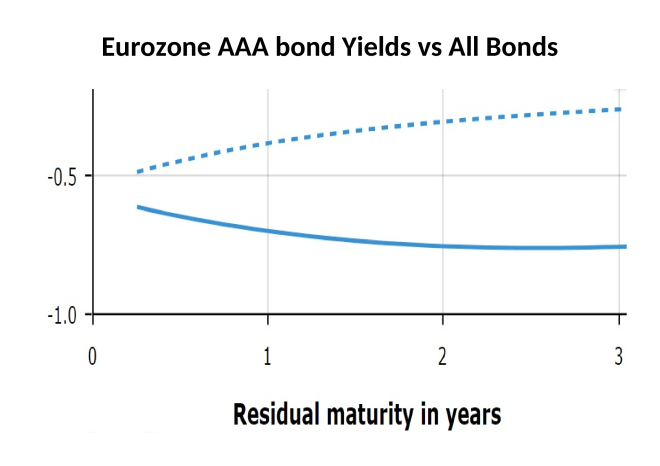

The chart below is a snap-shot of the 3m to 3yr Eurozone yield curve. The solid blue line shows the yield of AAA rated bonds, the dotted line, an average of all bonds: –

Source: ECB

It is interesting to note that the yield on AAA bonds, with a maturity of less than two years, steadily becomes less negative, whilst the aggregated yield of all bonds continues to decline.

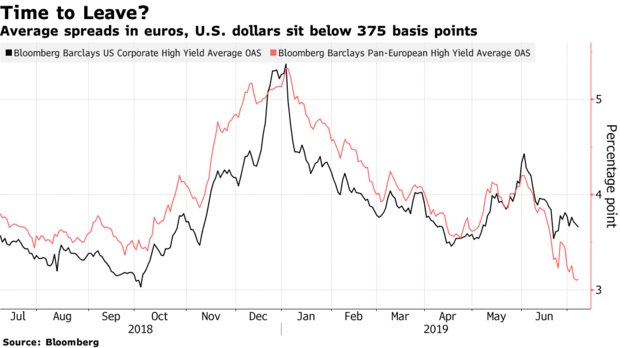

The broader high-yield market still offers positive yield but the Eurozone is likely to be the domicile of choice for new issuers, since Euro high-yield now trades at increasingly lower yields than the more liquid US market, the liquidity tail is wagging the dog: –

Source: Bloomberg, Barclays

The yield compression within the Eurozone has been more dramatic but it has been mirrored by the US where the spread between BBB and BB narrowed to a 12 year low of 60 basis points this month.

Wither away the dealers?

Forgotten, amid the inexorable bond rally, is dealer liquidity, yet it is essential, especially when investors rush for the exit simultaneously. For corporate bond market-makers and brokers the impact of QE has been painful. If the ECB is a buyer of a bond (and they pre-announce their intentions) then the market is guaranteed to rise. Liquidity is stifled in a game of devil take the hindmost. Alas, non-eligible issues, which the ECB does not deign to buy, find few natural buyers, so few institutions can justify purchases when credit default risk remains under-priced and in many cases the yield to maturity is negative.

An additional deterrent is the cost of holding an inventory of fixed income securities. Capital requirements for other than AAA government paper have increased since 2009. More damaging still is the negative carry across a wide range of instruments. In this environment, liquidity is bound to be impaired. The danger is that the underlying integrity of fixed income markets has been permanently impaired, without effective price intermediation there is limited price discovery: and without price discovery there is a real danger that there will be no firm, ‘dealable’ prices when they are needed most.

In this article from Bloomberg – A Lehman Survivor Is Prepping for the Next Credit Downturn – the interviewee, Pilar Gomez-Bravo of MFS Investment Management, discusses the problem of default risk in terms of terms of opacity (the emphasis is mine): –

Over a third of private high-yield companies in Europe, for example, restrict access to financial data in some way, according to Bloomberg analysis earlier this year. Buyers should receive extra compensation for firms that curb access to earnings with password-protected sites, according to Gomez-Bravo.

Borrowers still have the upper hand in the U.S. and Europe. Thank cheap-money policies and low defaults. Speculation the European Central Bank is preparing for another round of quantitative easing is spurring the rally — and masking fragile balance sheets.

Borrowers still have the upper hand indeed, earlier this month Italy issued a Eur3bln tranche of its 2.8% coupon 50yr BTP; there were Eur17bln of bids from around 200 institutions (bid/cover 5.66, yield 2.877%). German institutions bought 35% of the issue, UK investors 22%. The high bid/cover ratio is not that surprising, only 1% of Euro denominated investment grade paper yields more than 2%.

I am not alone in worrying about the integrity of the bond markets in the event of another crisis, last September ESMA – Liquidity in EU fixed income markets – Risk indicators and EU evidence concluded: –

Episodes of short-term volatility and liquidity stress across several markets over the past few years have increased concerns about the worsening of secondary market liquidity, in particular in the fixed income segment…

…our findings show that market liquidity has been relatively ample in the sovereign segment, potentially also due to the effects of supportive economic policies over more recent years. This is different from our findings in the corporate bond market, where in recent years we did not find systematic and significant drop in market liquidity but we observed episodes of decreasing market liquidity when market conditions deteriorated…

We find that in the sovereign bond segment, bonds that have a benchmark status and are characterised by larger outstanding amounts tend to be more liquid while market volatility is negatively related to market liquidity. Outstanding amounts are the main bond-level drivers in the corporate bond segment…

With reference to corporate bond markets, the sensitivity of bond liquidity to bond-specific and market factors is larger when financial markets are under stress. In particular, bonds characterised by more volatile market liquidity are found to be more vulnerable in periods of market stress. This empirical result is consistent with the market liquidity indicators developed for corporate bonds pointing at episodes of decreasing market liquidity when wider market conditions deteriorate.

ESMA steer clear of discussing negative yields and their impact on the profitability of market-making, but the BIS annual economic report, published last month, has no such qualms (the emphasis is mine): –

Household debt has reached new historical peaks in a number of economies that were not at the heart of the GFC, and house price growth has in many cases stalled. For a group of advanced small open economies, average household debt amounted to 101% of GDP in late 2018, over 20 percentage points above the pre-crisis level… Moreover, household debt service ratios, capturing households’ principal and interest payments in relation to income, remained above historical averages despite very low interest rates…

…corporate leverage remained close to historical highs in many regions. In the United States in particular, the ratio of debt to earnings in listed firms was above the previous peak in the early 2000s. Leverage in emerging Asia was still higher, albeit below the level immediately preceding the 1990s crisis. Lending to leveraged firms – i.e. those borrowing in either high-yield bond or leveraged loan markets – has become sizeable. In 2018, leveraged loan issuance amounted to more than half of global publicly disclosed loan issuance loans excluding credit lines.

… following a long-term decline in credit quality since 2000, the share of issuers with the lowest investment grade rating (including financial firms) has risen from around 14% to 45% in Europe and from 29% to 36% in the United States. Given widespread investment grade mandates, a further drop in ratings during an economic slowdown could lead investors to shed large amounts of bonds quickly. As mutual funds and other institutional investors have increased their holdings of lower-rated debt, mark-to-market losses could result in fire sales and reduce credit availability. The share of bonds with the lowest investment grade rating in investment grade corporate bond mutual fund portfolios has risen, from 22% in Europe and 25% in the United States in 2010 to around 45% in each region.

How financial conditions might respond depends also on how exposed banks are to collateralised loan obligations (CLOs). Banks originate more than half of leveraged loans and hold a significant share of the least risky tranches of CLOs. Of these holdings, US, Japanese and European banks account for around 60%, 30% and 10%, respectively…

…the concentration of exposures in a small number of banks may result in pockets of vulnerability. CLO-related losses could reveal that the search-for-yield environment has led to an underpricing and mismanagement of risks…

In the euro area, the deterioration of the growth outlook was more evident, and so was its adverse impact on an already fragile banking sector. Price-to-book ratios fell further from already depressed levels, reflecting increasing concerns about banks’ health…

Unfortunately, bank profitability has been lacklustre. In fact, as measured, for instance, by return-on-assets, average profitability across banks in a number of advanced economies is substantially lower than in the early 2000s. Within this group, US banks have performed considerably better than those in the euro area, the United Kingdom and Japan…

…persistently low interest rates and low growth reduce profits. Compressed term premia depress banks’ interest rate margins from maturity transformation. Low growth curtails new loans and increases the share of non-performing ones. Therefore, should growth decline and interest rates continue to remain low following the pause in monetary policy normalisation, banks’ profitability could come under further pressure.

Conclusion and investment opportunities

Back in 2006, when commodity investing, as part of a diversified portfolio, was taking the pension fund market by storm, I gave a series of speeches in which I beseeched fund managers to consider carefully before investing in commodities, an asset class which had for more than 150 years exhibited a negative expected real return.

An astonishingly large percentage of fixed income securities are exhibiting similar properties today. My advice, then for commodities and today, for fixed income securities, is this, ‘By all means buy, but remember, this is a trading asset, its long-term expected return is negative; in other words, please, don’t forget to sell.’

![]()

Macro Letter – No 111 – 15-03-2019

Capital Flows – is a reckoning nigh?

In Macro Letter – No 108 – 18-01-2019 – A world of debt – where are the risks? I looked at the increase in debt globally, however, there has been another trend, since 2009, which is worth investigating as we consider from whence the greatest risk to global growth may hail. The BIS global liquidity indicators at end-September 2018 – released at the end of January, provides an insight: –

The annual growth rate of US dollar credit to non-bank borrowers outside the United States slowed down to 3%, compared with its most recent peak of 7% at end-2017. The outstanding stock stood at $11.5 trillion.

In contrast, euro-denominated credit to non-bank borrowers outside the euro area rose by 9% year on year, taking the outstanding stock to €3.2 trillion (equivalent to $3.7 trillion). Euro-denominated credit to non-bank borrowers located in emerging market and developing economies (EMDEs) grew even more strongly, up by 13%.

The chart below shows the slowing rate of US$ credit growth, while euro credit accelerates: –

Source: BIS global liquidity indicators

The rising demand for Euro denominated borrowing has been in train since the end of the Great Financial Recession in 2009. Lower interest rates in the Eurozone have been a part of this process; a tendency for the Japanese Yen to rise in times of economic and geopolitical concern has no doubt helped European lenders to gain market share. This trend, however, remains over-shadowed by the sheer size of the US credit markets. The US$ has remained preeminent due to structurally higher interest rates and bond yields than Europe or Japan: investors, rather than borrowers, dictate capital flows.

The EC – Analysis of developments in EU capital flows in the global context from November 2018 concurs: –

The euro area (excluding intra-euro area flows) has been since 2013 the world’s leading net exporter of capital. Capital from the euro area has been invested heavily abroad in debt securities, especially in the US, taking advantage of the interest differential between the two jurisdictions. At the same time, foreign holdings of euro-area bonds fell as a result of the European Central Bank’s Asset Purchase Programme.

This bring us to another issue; a country’s ability to service its debt is linked to its GDP growth rate. Since 2009 the US economy has expanded by 34%, over the same period, Europe has shrunk by 2%. Putting these rates of expansion into a global perspective, the last decade has seen China’s economy grow by 139%, whilst India has gained 96%. Recent analysis suggests that Chinese growth may have been overstated by 2% per annum over the past decade, but the pace is still far in excess of developed economy rates. Concern about Chinese debt is not unwarranted, but with GDP rising by 6% per annum, its economy will be 80% larger in a decade, whilst India’s, growing at 7%, will have doubled.

Another excellent research paper from the BIS – The expansionary lower bound: contractionary monetary easing and the trilemma – investigates the problem of monetary tightening of developed economies on emerging markets. Here is part of the introduction, the emphasis is mine: –

…policy makers in EMs are often reluctant to lower interest rates during an economic downturn because they fear that, by spurring capital outflows, monetary easing may end up weakening, rather than boosting, aggregate demand.

An empirical analysis of the determinants of policy rates in EMs provides suggestive evidence about the tensions faced by monetary authorities, even in countries with flexible exchange rates.

…The results reveal that, even after controlling for expected inflation and the output gap, monetary authorities in EMs tend to hike policy rates when the VIX or US policy rates increase. This is arguably driven by the desire to limit capital outflows and the depreciation of the exchange rate.

…our theory predicts the existence of an “Expansionary Lower Bound” (ELB) which is an interest rate threshold below which monetary easing becomes contractionary. The ELB constrains the ability of monetary policy to stimulate aggregate demand, placing an upper bound on the level of output achievable through monetary stimulus.

The ELB can occur at positive interest rates and is therefore a potentially tighter constraint for monetary policy than the Zero Lower Bound (ZLB). Furthermore, global monetary and financial conditions affect the ELB and thus the ability of central banks to support the economy through monetary accommodation. A tightening in global monetary and financial conditions leads to an increase in the ELB which in turn can force domestic monetary authorities to increase policy rates in line with the empirical evidence presented…

The BIS research is focussed on emerging economies, but aspects of the ELB are evident elsewhere. The limits of monetary policy are clearly observable in Japan: the Eurozone may be entering a similar twilight zone.

The difference between emerging and developed economies response to a tightening in global monetary conditions is seen in capital flows and exchange rates. Whilst emerging market currencies tend to fall, prompting their central banks to tighten monetary conditions in defence, in developed economies the flow of returning capital from emerging market investments may actually lead to a strengthening of the exchange rate. The persistent strength of the Japanese Yen, despite moribund economic growth over the past two decades, is an example of this phenomenon.

Part of the driving force behind developed market currency strength in response to a tightening of global monetary conditions is demographic, a younger working age population borrows more, an ageing populous borrows less.

At the risk of oversimplification, lower bond yields in developing (and even developed) economies accelerate the process of capital repatriation. Japanese pensioners can hardly rely on JGBs to deliver their retirement income when yields are at the zero bound, they must accept higher risk to achieve a living income, but this makes them more likely to drawdown on investments made elsewhere when uncertainty rises. A 2% rise in US interest rates only helps the eponymous Mrs Watanabe if the Yen appreciates by less than 2% in times of stress. Japan’s pensioners face a dilemma, a fall in US rates, in response to weaker global growth, also creates an income shortfall; capital is still repatriated, simply with less vehemence than during an emerging market crisis. As I said, this is an oversimplification of a vastly more complex system, but the importance of capital flows, in a more polarised ‘risk-on, risk-off’ world, is not to be underestimated.

Returning to the BIS working paper, the authors conclude: –

The models highlight a novel inter-temporal trade-off for monetary policy since the level of the ELB is affected by the past monetary stance. Tighter ex-ante monetary conditions tend to lower the ELB and thus create more monetary space to offset possible shocks. This observation has important normative implications since it calls for keeping a somewhat tighter monetary stance when global conditions are supportive to lower the ELB in the future.

Finally, the models have rich implications for the use of alternative policy tools that can be deployed to overcome the ELB and restore monetary transmission. In particular, the presence of the ELB calls for an active use of the central bank’s balance sheet, for example through quantitative easing and foreign exchange intervention. Furthermore, the ELB provides a new rationale for capital controls and macro-prudential policies, as they can be successfully used to relax the tensions between domestic collateral constraints and capital flows. Fiscal policy can also help to overcome the ELB, while forward guidance is ineffective since the ELB increases with the expectation of looser future monetary conditions.

Conclusions and investment opportunities

The concept of the ELB is new, the focus of the BIS working paper is on its impact on emerging markets. I believe the same forces are evident in developed economies too, but the capital flows are reversed. For investors, the greatest risk of emerging market investment is posed by currency, however, each devaluation by an emerging economy inexorably weakens the position of developed economies, since the devaluation makes that country’s exports immediately more competitive.

At present the demographic forces favour repatriation during times of crisis and repatriation, at a slower rate, during times of EM currency appreciation. This is because the ageing economies of the developed world continue to drawdown on their investments. At some point this demographic effect will reverse, however, for Japan and the Eurozone this will not be before 2100. For more on the demographic deficit the 2018 Ageing Report: Europe’s population is getting older – is worth reviewing. Until demographic trends reverse, international demand to borrow in US$, Euros and Yen will remain popular. Emerging market countries will pay the occasional price for borrowing cheaply, in the form of currency depreciations.

For Europe and Japan a reckoning may be nigh, but it seems more likely that their economic importance will gradually diminish as emerging economies, with a younger working age population and higher structural growth rates, eclipse them.

![]()

Macro Letter – No 110 – 15-02-2019

Central bank balance sheet reductions – will anyone follow the Fed?

The Federal Reserve’s response to the great financial recession of 2008/2009 was swift by comparison with that of the ECB; the BoJ was reticent, too, due to its already extended balance sheet. Now that the other developed economy central banks have fallen into line, the question which dominates markets is, will other central banks have room to reverse QE?

Last month saw the publication of a working paper from the BIS – Risk endogeneity at the lender/investor-of-last-resort – in which the authors investigate the effect of ECB liquidity provision, during the Euro crisis of 2010/2012. They also speculate about the challenge balance sheet reduction poses to systemic risk. Here is an extract from the non-technical summary (the emphasis is mine): –

The Eurosystem’s actions as a large-scale lender- and investor-of-last-resort during the euro area sovereign debt crisis had a first-order impact on the size, composition, and, ultimately, the credit riskiness of its balance sheet. At the time, its policies raised concerns about the central bank taking excessive risks. Particular concern emerged about the materialization of credit risk and its effect on the central bank’s reputation, credibility, independence, and ultimately its ability to steer inflation towards its target of close to but below 2% over the medium term.

Against this background, we ask: Can central bank liquidity provision or asset purchases during a liquidity crisis reduce risk in net terms? This could happen if risk taking in one part of the balance sheet (e.g., more asset purchases) de-risks other balance sheet positions (e.g., the collateralized lending portfolio) by a commensurate or even larger amount. How economically important can such risk spillovers be across policy operations? Were the Eurosystem’s financial buffers at all times sufficiently high to match its portfolio tail risks? Finally, did past operations differ in terms of impact per unit of risk?…

We focus on three main findings. First, we find that (Lender of last resort) LOLR- and (Investor of last resort) IOLR-implied credit risks are usually negatively related in our sample. Taking risk in one part of the central bank’s balance sheet (e.g., the announcement of asset purchases within the Securities Market Programme – SMP) tended to de-risk other positions (e.g., collateralized lending from previous – longer-term refinancing operations LTROs). Vice versa, the allotment of two large-scale (very long-term refinancing operations) VLTRO credit operations each decreased the one-year-ahead expected shortfall of the SMP asset portfolio. This negative relationship implies that central bank risks can be nonlinear in exposures. In bad times, increasing size increases risk less than proportionally. Conversely, reducing balance sheet size may not reduce total risk by as much as one would expect by linear scaling. Arguably, the documented risk spillovers call for a measured approach towards reducing balance sheet size after a financial crisis.

Second, some unconventional policy operations did not add risk to the Eurosystem’s balance sheet in net terms. For example, we find that the initial OMT announcement de-risked the Eurosystem’s balance sheet by e41.4 bn in 99% expected shortfall (ES). As another example, we estimate that the allotment of the first VLTRO increased the overall 99% ES, but only marginally so, by e0.8 bn. Total expected loss decreased, by e1.4 bn. We conclude that, in extreme situations, a central bank can de-risk its balance sheet by doing more, in line with Bagehot’s well-known assertion that occasionally “only the brave plan is the safe plan.” Such risk reductions are not guaranteed, however, and counterexamples exist when risk reductions did not occur.

Third, our risk estimates allow us to study past unconventional monetary policies in terms of their ex-post ‘risk efficiency’. Risk efficiency is the notion that a certain amount of expected policy impact should be achieved with a minimum level of additional balance sheet risk. We find that the ECB’s Outright Monetary Transactions – OMT program was particularly risk efficient ex-post since its announcement shifted long-term inflation expectations from deflationary tendencies toward the ECB’s target of close to but below two percent, decreased sovereign benchmark bond yields for stressed euro area countries, while lowering the risk inherent in the central bank’s balance sheet. The first allotment of VLTRO funds appears to have been somewhat more risk-efficient than the second allotment. The SMP, despite its benefits documented elsewhere, does not appear to have been a particularly risk-efficient policy measure.

This BIS research is an important assessment of the effectiveness of ECB QE. Among other things, the authors find that the ‘shock and awe’ effectiveness of the first ‘quantitative treatment’ soon diminished. Liquidity is the methadone of the market, for QE to work in future, a larger and more targeted dose of monetary alchemy will be required.

The paper provides several interesting findings, for example, the Federal Reserve ‘taper-tantrum’ of 2013 and the Swiss National Bank decision to unpeg the Swiss Franc in 2015, did not appear to influence markets inside the Eurozone, once ECB president, Mario Draghi, had made its intensions plain. Nonetheless, the BIS conclude that (emphasis, once again, is mine): –

…collateralized credit operations imply substantially less credit risks (by at least one order of magnitude in our crisis sample) than outright sovereign bond holdings per e1 bn of liquidity owing to a double recourse in the collateralized lending case. Implementing monetary policy via credit operations rather than asset holdings, whenever possible, therefore appears preferable from a risk efficiency perspective. Second, expanding the set of eligible assets during a liquidity crisis could help mitigate the procyclicality inherent in some central bank’s risk protection frameworks.

In other words, rather than exacerbate the widening of credit spreads by purchasing sovereign debt, it is preferable for central banks to lean against the ‘flight to quality’ tendency of market participants during times of stress.

The authors go on to look at recent literature on the stress-testing of central bank balance sheets, mainly focussing on analysis of the US Federal Reserve. Then they review ‘market-risk’ methods as a solution to the ‘credit-risk’ problem, employing non-Gaussian methods – a prescient approach after the unforeseen events of 2008.

Bagehot thou shouldst be living at this hour (with apologies to Wordsworth)

The BIS authors refer on several occasions to Bagehot. I wonder what he would make of the current state of central banking? Please indulge me in this aside.

Walter Bagehot (1826 to 1877) was appointed by Richard Cobden as the first editor of the Economist. He is also the author of perhaps the best known book on the function of the 19th century money markets, Lombard Street (published in 1873). He is famed for inventing the dictum that a central bank should ‘lend freely, at a penalty rate, against good collateral.’ In fact he never actually uttered these words, they have been implied. Even the concept of a ‘lender of last resort’, to which he refers, was not coined by him, it was first described by Henry Thornton in his 1802 treatise – An Enquiry into the Nature and Effects of the Paper Credit of Great Britain.

To understand what Bagehot was really saying in Lombard Street, this essay by Peter Conti-Brown – Misreading Walter Bagehot: What Lombard Street Really Means for Central Banking – provides an elegant insight: –

Lombard Street was not his effort to argue what the Bank of England should do during liquidity crises, as almost all people assume; it was an argument about what the Bank of England should openly acknowledge that it had already done.

Bagehot was a classical liberal, an advocate of the gold standard; I doubt he would approve of the nature of central banks today. He would, I believe, have thrown his lot in with the likes of George Selgin and other proponents of Free Banking.

Conclusion and Investment Opportunities

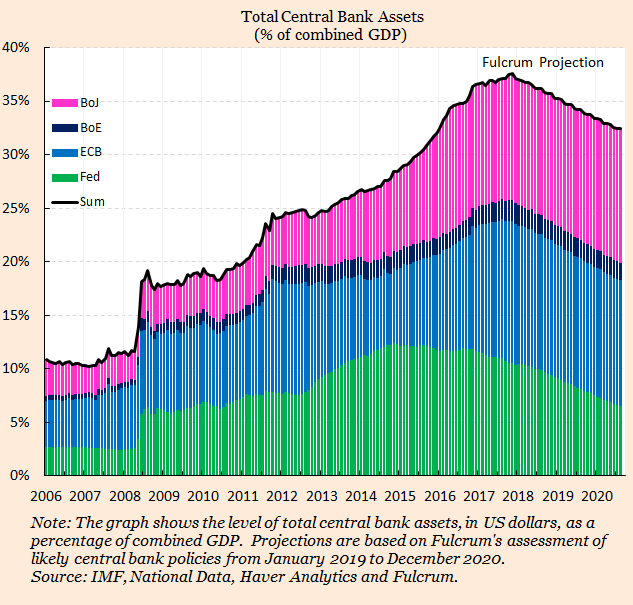

Given the weakness of European economies it seems unlikely that the ECB will be able to follow the lead of the Federal Reserve and raise interest rates in any meaningful way. The unwinding of, at least a portion of, QE might be easier, since many of these refinancing operations will naturally mature. For arguments both for and against CB balance sheet reduction this paper by Charles Goodhart – A Central Bank’s optimal balance sheet size? is well worth reviewing. A picture, however, is worth a thousand words, although I think the expected balance sheet reduction may be overly optimistic: –

Source: IMF, Haver Analytics, Fulcrum Asset Management

Come the next crisis, I expect the ECB to broaden the range of eligible securities and instruments that it is prepared to purchase. The ‘Draghi Put’ will gain greater credence as it encompasses a wider array of credits. The ‘Flight to Quality’ effect, driven by swathes of investors forsaking equities and corporate bonds, in favour of ‘risk-free’ government securities, will be shorter-lived and less extreme. The ‘Convergence Trade’ between the yields of European government bonds will regain pre-eminence; I can conceive the 10yr BTP/Bund spread testing zero.

None of this race to zero will happen in a straight line, but it is important not to lose sight of the combined power of qualitative and quantitative easing. The eventual ‘socialisation’ of common stock is already taking place in Japan. Make no mistake, it is already being contemplated by a central bank near you, right now.

![]()

Macro Letter – No 109 – 01-02-2019

Sustainable government debt – an old idea refreshed

The Peterson Institute has long been one of my favourite sources of original research in the field of economics. They generally support free-market ideas, although they are less than classically liberal in their approach. I was, nonetheless, surprised by the Presidential Lecture given at the annual gathering of the American Economic Association (AEA) by Olivier Blanchard, ex-IMF Chief Economist, now at the Peterson Institute – Public Debt and Low Interest Rates. The title is quite anodyne, the content may come to be regarded as incendiary. Here is part of his introduction: –

Since 1980, interest rates on U.S. government bonds have steadily decreased. They are now lower than the nominal growth rate, and according to current forecasts, this is expected to remain the case for the foreseeable future. 10-year U.S. nominal rates hover around 3%, while forecasts of nominal growth are around 4% (2% real growth, 2% inflation). The inequality holds even more strongly in the other major advanced economies: The 10-year UK nominal rate is 1.3%, compared to forecasts of 10-year nominal growth around 3.6% (1.6% real, 2% inflation). The 10-year Euro nominal rate is 1.2%, compared to forecasts of 10-year nominal growth around 3.2% (1.5% real, 2% inflation). The 10-year Japanese nominal rate is 0.1%, compared to forecasts of 10-year nominal growth around 1.4% (1.0% real, 0.4% inflation).

The question this paper asks is what the implications of such low rates should be for government debt policy. It is an important question for at least two reasons. From a policy viewpoint, whether or not countries should reduce their debt, and by how much, is a central policy issue. From a theory viewpoint, one of pillars of macroeconomics is the assumption that people, firms, and governments are subject to intertemporal budget constraints. If the interest rate paid by the government is less the growth rate, then the intertemporal budget constraint facing the government no longer binds. What the government can and should do in this case is definitely worth exploring.

The paper reaches strong, and, I expect, surprising, conclusions. Put (too) simply, the signal sent by low rates is that not only debt may not have a substantial fiscal cost, but also that it may have limited welfare costs.

Blanchard’s conclusions may appear radical, yet, in my title, I refer to this as an old idea, allow me to explain. In business it makes sense, all else equal, to borrow if the rate of interest paid on your loan is lower than the return from your project. At the national level, if the government can borrow at below the rate of GDP growth it should be sustainable, since, over time (assuming, of course, that it is not added to) the ratio of debt to GDP will naturally diminish.

There are plenty of reasons why such borrowing may have limitations, but what really interests me, in this thought provoking lecture, is the reason governments can borrow at such low rates in the first instance. One argument is that as GDP grows, so does the size of the tax base, in other words, future taxation should be capable of covering the on-going interest on today’s government borrowing: the market should do the rest. Put another way, if a government become overly profligate, yields will rise. If borrowing costs exceed the expected rate of GDP there may be a panicked liquidation by investors. A government’s ability to borrow will be severely curtailed in this scenario, hence the healthy obsession, of many finance ministers, with debt to GDP ratios.

There are three factors which distort the cosy relationship between the lower yield of ‘risk-free’ government bonds and the higher percentage levels of GDP growth seen in most developed countries; investment regulations, unfunded liabilities and fractional reserve bank lending.

Let us begin with investment regulations, specifically in relation to the constraints imposed on pension funds and insurance companies. These institutions are hampered by prudential measures intended to guarantee that they are capable of meeting payment obligations to their customers in a timely manner. Mandated investment in liquid assets are a key construct: government bonds form a large percentage of their investments. As if this was not sufficient incentive, institutions are also encouraged to purchase government bonds as a result of the zero capital requirements for holding these assets under Basel rules.

A second factor is the uncounted, unfunded, liabilities of state pension funds and public healthcare spending. I defer to John Mauldin on this subject. The 8th of his Train-Wreck series is entitled Unfunded Promises – the author begins his calculation of total US debt with the face amount of all outstanding Treasury paper, at $21.2trln it amounts to approximately 105% of GDP. This is where the calculations become disturbing: –

If you add in state and local debt, that adds another $3.1 trillion to bring total government debt in the US to $24.3 trillion or more than 120% of GDP.

Mauldin goes on to suggest that this still underestimates the true cost. He turns to the Congressional Budget Office 2018 Long-Term Budget Outlook – which assumes that federal spending will grow significantly faster than federal revenue. On the basis of their assumptions, all federal tax revenues will be consumed in meeting social security, health care and interest expenditures by 2041.

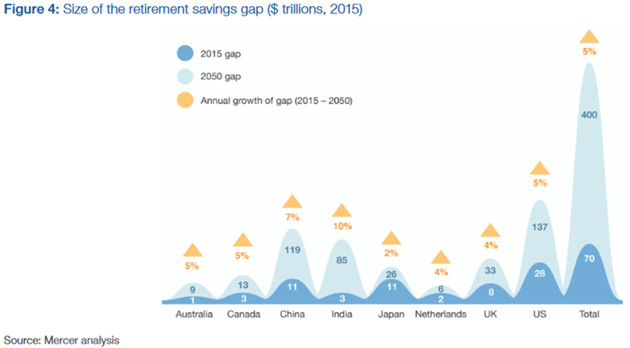

Extrapolate this logic to other developed economies, especially those with more generous welfare commitments than the US, and the outlook for rapidly aging, welfare addicted developed countries is bleak. In a 2017 white paper by Mercer for World Economic Forum – We Will Live to 100 – the author estimates that the unfunded liabilities of US, UK, Netherlands, Japan, Australia, Canada, China and India will rise from $70trln in 2015 to $400trln in 2050. These countries represent roughly 60% of global GDP. I extrapolate global unfunded liabilities of around $120trln today rising to nearer $650trln within 20 years: –

Source: Mercer analysis

For an in depth analysis of the global pension crisis this 2016 research paper from Citi GPS – The Coming Pensions Crisis – is a mine of information.

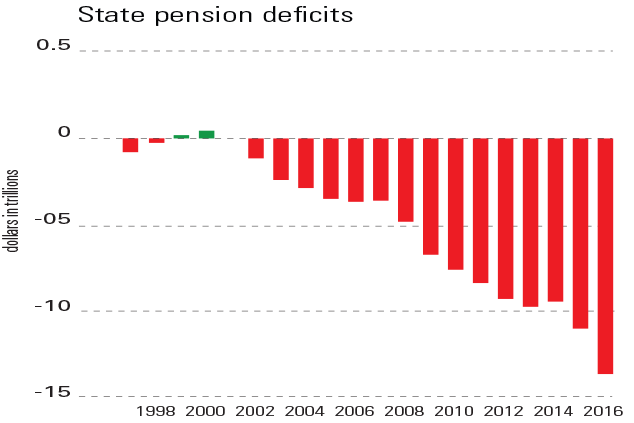

In case you are still wondering how, on earth, we got here? This chart from Money Week shows how a combination of increased fiscal spending (to offset the effect of the bursting of the tech bubble in 2000) combined with the dramatic fall in interest rates (since the great financial recession of 2008/2009) has damaged the US state pension system: –

Source: Moneyweek

The yield on US Treasury bonds has remained structurally higher than most of the bonds of Europe and any of Japan, for at least a decade.

The third factor is the fractional reserve banking system. Banks serve a useful purpose intermediating between borrowers and lenders. They are the levers of the credit cycle, but their very existence is testament to their usefulness to their governments, by whom they are esteemed for their ability to purchase government debt. I discuss – A history of Fractional Reserve Banking – or why interest rates are the most important influence on stock market valuations? in a two part essay I wrote for the Cobden Centre in October 2016. In it I suggest that the UK banking system, led by the Bank of England, has enabled the UK government to borrow at around 3% below the ‘natural rate’ of interest for more than 300 years. The recent introduction of quantitative easing has only exaggerated the artificial suppression of government borrowing costs.

Before you conclude that I am on a mission to change the world financial system, I wish to point out that if this suppression of borrowing costs has been the case for more than 300 years, there is no reason why it should not continue.

Which brings us back to Blanchard’s lecture at the AEA. Given the magnitude of unfunded liabilities, the low yield on government bonds is, perhaps, even more remarkable. More alarmingly, it reinforces Blanchard’s observation about the greater scope for government borrowing: although the author is at pains to advocate fiscal rectitude. If economic growth in developed economies stalls, as it has for much of the past two decades in Japan, then a Japanese redux will occur in other developed countries. The ‘risk-free’ rate across all developed countries will gravitate towards the zero bound with a commensurate flattening in yield curves. Over the medium term (the next decade or two) an increasing burden of government debt can probably be managed. Some of the new borrowing may even be diverted to investments which support higher economic growth. The end-game, however, will be a monumental reckoning, involving wholesale debt forgiveness. The challenge, as always, will be to anticipate the inflection point.

Conclusion and Investment Opportunities

Since the early-1990’s analysts have been predicting the end of the bond bull market. Until quite recently it was assumed that negative government bond yields were a temporary aberration reflecting stressed market conditions. When German schuldscheine (the promissory notes of the German banking system) traded briefly below the yield of German Bunds, during the reunification in 1989, the ‘liquidity anomaly’ was soon rectified. There has been a sea-change, for a decade since 2008, US 30yr interest rate swaps traded at a yield discount to US Treasuries – for more on this subject please see – Macro Letter – No 74 – 07-04-2017 – US 30yr Swaps have yielded less than Treasuries since 2008 – does it matter?

With the collapse in interest rates and bond yields, the unfunded liabilities of governments in developed economies has ballooned. A solution to the ‘pension crisis,’ higher bond yields, would sow the seeds of a wider economic crisis. Whilst governments still control their fiat currencies and their central banks dictate the rate of interest, there is still time – though, I doubt, the political will – to make the gradual adjustments necessary to right the ship.

I have been waiting for US 10yr yields to reach 4.5%, I may be disappointed. For investors in fixed income securities, the bond bull market has yet to run its course. Negative inflation adjusted returns will become the norm for risk-free assets. Stock markets may be range-bound for a protracted period as return expectations adjust to a structurally weaker economic growth environment.

![]()

Macro Letter – No 108 – 18-01-2019

A world of debt – where are the risks?

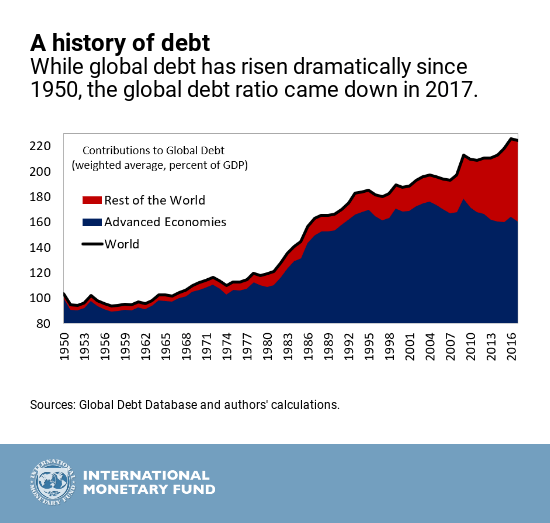

Since the financial crisis of 2008/2009 global debt has increased to reach a new all-time high. This trend has been documented before in articles such as the 2014 paper from the International Center for Monetary and Banking Studies – Deleveraging? What deleveraging? The IMF have also been built a global picture of the combined impact of private and public debt. In a recent publication – New Data on Global Debt – IMF – the authors make some interesting observations: –

Global debt has reached an all-time high of $184 trillion in nominal terms, the equivalent of 225 percent of GDP in 2017. On average, the world’s debt now exceeds $86,000 in per capita terms, which is more than 2½ times the average income per-capita.

The most indebted economies in the world are also the richer ones. You can explore this more in the interactive chart below. The top three borrowers in the world—the United States, China, and Japan—account for more than half of global debt, exceeding their share of global output.

The private sector’s debt has tripled since 1950. This makes it the driving force behind global debt. Another change since the global financial crisis has been the rise in private debt in emerging markets, led by China, overtaking advanced economies. At the other end of the spectrum, private debt has remained very low in low-income developing countries.

Global public debt, on the other hand, has experienced a reversal of sorts. After a steady decline up to the mid-1970s, public debt has gone up since, with advanced economies at the helm and, of late, followed by emerging and low-income developing countries.

The recent picture suggests that the old world order, dominated by advanced economies, may be changing. For investors, this is an important consideration. Total debt in 2017 had exceeded the previous all-time high by more than 11%, however, the global debt to GDP ratio fell by 1.5% between 2016 and 2017, led by developed nations.

Setting aside the absolute level of interest rates, which have finally begun to rise from multi-year lows, it makes sense for rapidly aging, developed economies, to begin reducing their absolute level of debt, unfortunately, given that unfunded pension liabilities and the escalating cost of government healthcare provision are not included in the data, the IMF are only be portraying a partial picture of the state of developed economy obligations.

For emerging markets, the trauma of the 1998 Asian Crisis has finally waned. In the decade since the great financial recession of 2008 emerging economies, led by China, have increased their borrowing. This is clearly indicated in the chart below: –

Source: IMF

The decline in the global debt to GDP ratio in 2017 is probably related to the change in Federal Reserve policy; the largest proportion of global debt is still raised in US$. Rather like the front-loaded US growth which transpired due the threat of tariff increases on US imports, I suspect, debt issuance spiked in expectation of a reversal of quantitative easing and an end to ultra-low US interest rates.

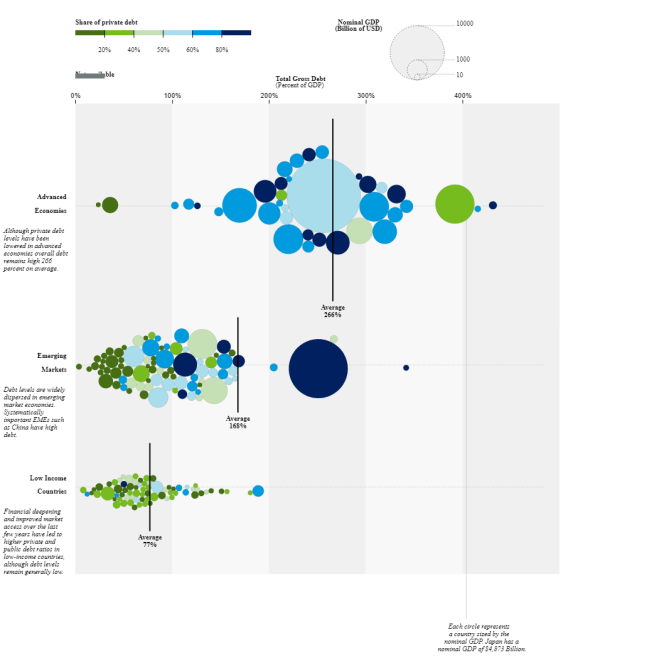

The IMF goes on to show the breakdown of debt by country, separating them into three groups; advanced economies, emerging markets and low income countries. The outlier is China, an emerging market with a debt to GDP ratio comparable to that of an advanced economy. The table below may be difficult to read (an interactive one is available on the IMF website): –

Source: IMF

At 81%, China’s private debt is much greater than its public debt, meanwhile its debt to GDP ratio is 254% – comparable with the US (256%). Fortunately, the majority of Chinese private debt is denominated in local currency. Advanced economies have higher debt to GDP ratios but their government debt ratios are relatively modest, excepting Japan. The Economist – Economists reconsider how much governments can borrow – provides food for thought on this subject.

Excluding China, emerging markets and low income countries have relatively similar levels of debt relative to GDP. In general, the preponderance of government debt in lower ratio countries reflects the lack of access to capital markets for private sector borrowers.

Conclusions and Investment Opportunities

Setting aside China, which, given its control on capital flows and foreign exchange reserves is hard to predict, the greatest risk to world financial markets appears to be from the private debt of advanced economies.