At the beginning on January I wrote this article for the AIER. Whilst much has changed, the trends have accelerated.

https://www.aier.org/article/the-dangers-to-prosperity-all-around-us/

At the beginning on January I wrote this article for the AIER. Whilst much has changed, the trends have accelerated.

https://www.aier.org/article/the-dangers-to-prosperity-all-around-us/

![]()

Macro Letter – No 126 – 14-02-2020

When the facts change

My title is the first part of JM Keynes famous remark, ‘When the facts change, I change my mind.’ This phrase has been nagging at my conscience ever since the Coronavirus epidemic began to engulf China and send shockwaves around the world. From an investment perspective, have the facts changed? Financial markets have certainly behaved in a predictable manner. Government bonds rallied and stocks declined. Then the market caught its breath and stocks recovered. There have, of course been exceptions, while the S&P 500 has made new highs, those companies and sectors most likely to be effected by the viral outbreak have been hardest hit.

Is the impact of Covid-19 going to be seen in economic data? Absolutely. Will economic growth slow? Yes, though it will be felt most in Wuhan and the Hubei region, a region estimated to account for 4.5% in Chinese GDP and 7% of autopart manufacture. The impact will be less pronounced in other parts of the world, although Korea’s Hyundai has already ceased vehicle production at its factories due to a lack of Chinese car parts.

Will there be a longer-term impact on the global supply chain and will this affect stock and bond prices? These are more difficult questions to answer. Global supply chains have been shortening ever since the financial crisis, the Sino-US trade war has merely added fresh impetus to the process. As for financial markets, stock prices around the world declined in January but those markets farthest from the epicentre of the outbreak have since recovered in some cases making new all-time highs. The longer-term impact remains unclear. Why? Because the performance of the stock market over the last decade has been driven almost entirely by the direction of interest rates, whilst economic growth, since the financial crisis, has been anaemic at best. As rates have fallen and central banks have purchased bonds, so bond yields have declined making stocks look relatively more attractive. Some central banks have even bought stocks to add to their cache of bonds, but I digress.

Returning to my title, from an investment perspective, have the facts changed? Global economic growth will undoubtedly take a hit, estimates of 0.1% to 0.2% fall in 2020 already abound. In order to mitigate this downturn, central banks will cut rates – where they can – and buy progressively longer-dated and less desirable bonds as they work their way along the maturity spectrum and down the credit-structure. Eventually they will emulate the policy of the Japanese and the Swiss, by purchasing common stocks. In China, where the purse strings have been kept tight during the past year, the PBoC has already ridden to the rescue, flooding the domestic banking system with $173bln of additional liquidity; it seems, the process of saving the stock market from the dismal vicissitudes of a global economic slow-down has already begun.

Growth down, profits down, stocks up? It sounds absurd but that is the gerrymandered nature of the current marketplace. It is comforting to know, the central banks will not have to face the music alone, they can rely upon the usual allies, as they endeavour to keep the everything bubble aloft. Which allies? The corporate executives of publically listed companies. Faced with the dilemma of expanding capital expenditure in the teeth of an economic slowdown – which might turn into a recession – the leaders of publically listed corporations can be relied upon to do the honourable thing, pay themselves in stock options and buyback more stock.

At some point this global Ponzi scheme will inflect, exhaust, implode, but until that moment arrives, it would be unwise to step off the gravy-train. The difficulty of staying aboard, of course, is the same one as always, the markets climb a wall of fear. If there is any good news amid the tragic Covid-19 pandemic, it is that the January correction has prompted some of the weaker hands in the stock market to fold. When markets consolidate on a high plateau, should they then turn down, the patient investor may be afforded time to exit. This price action is vastly preferable to the hyperbolic rise, followed by the sharp decline, an altogether more cathartic and less agreeable dénouement.

Other Themes and Menes

As those of you who have been reading my letters for a while will know, I have been bullish on the US equity market for several years. That has worked well. I have also been bullish on emerging markets in general – and Asia in particular – over a similar number of years. A less rewarding investment. With the benefit of hindsight, I should have been more tactical.

Looking ahead, Asian economies will continue to grow, but their stock markets may disappoint due to the uncertainty of the US administrations trade agenda. The US will continue to benefit from low interest rates and technological investment, together with buy-backs, mergers and privatisations. Elsewhere, I see opportunity within Europe, as governments spend on green infrastructure and other climate conscious projects. ESG investing gains more advocates daily. Socially responsible institutions will garner assets from socially responsible investors, while socially responsible governments will award contracts to those companies whose behaviour is ethically sound. It is a virtuous circle of morally commendable, albeit not necessarily economically logical, behaviour.

The UK lags behind Europe on environmental issues, but support for business and three years of deferred capital investment makes it an appealing destination for investment, as I explained last December in The Beginning of the End of Uncertainty for the UK.

Conclusions

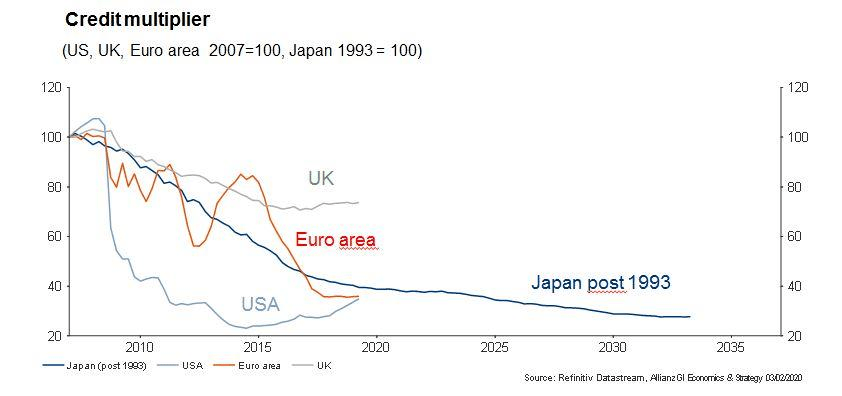

Returning once more to my title, the facts always change but, unless the Covid-19 pandemic should escalate dramatically, the broad investment themes appear largely unchanged. Central banks still weld awesome power to drive asset prices, although this increasingly fails to feed through to the real economy. The chart below shows the diminishing power of the credit multiplier effect – Japan began their monetary experiment roughly a decade earlier than the rest of the developed world: –

Source: Allianz/Refinitiv

Like an addictive drug, the more the monetary stimulus, the more the patient needs in order to achieve the same high. The direct financial effect of lower interest rates is a lowering of bond yields; lower yields spur capital flows into higher yielding credit instruments and equities. However, low rates also signal an official fear of recession, this in turn prompts a reticence to lend on the part of banking intermediaries, the real-economy remains cut off from the credit fix it needs. Asset prices keep rising, economic growth keeps stalling; the rich get richer and the poor get deeper into debt. Breaking the market addiction to cheap credit is key to unravelling this colossal misallocation of resources, a trend which has been in train since the 1980’s, if not before. The prospect of reserving course on subsidised credit is politically unpalatable, asset owners, especially indebted ones, will suffer greatly if interest rates should rise, they will vote accordingly. The alternative is more of the same profligate policy mix which has suspended reality for the past decade. From an investment perspective, the facts have not yet changed and I have yet to change my mind.

![]()

Macro Letter – No 110 – 15-02-2019

Central bank balance sheet reductions – will anyone follow the Fed?

The Federal Reserve’s response to the great financial recession of 2008/2009 was swift by comparison with that of the ECB; the BoJ was reticent, too, due to its already extended balance sheet. Now that the other developed economy central banks have fallen into line, the question which dominates markets is, will other central banks have room to reverse QE?

Last month saw the publication of a working paper from the BIS – Risk endogeneity at the lender/investor-of-last-resort – in which the authors investigate the effect of ECB liquidity provision, during the Euro crisis of 2010/2012. They also speculate about the challenge balance sheet reduction poses to systemic risk. Here is an extract from the non-technical summary (the emphasis is mine): –

The Eurosystem’s actions as a large-scale lender- and investor-of-last-resort during the euro area sovereign debt crisis had a first-order impact on the size, composition, and, ultimately, the credit riskiness of its balance sheet. At the time, its policies raised concerns about the central bank taking excessive risks. Particular concern emerged about the materialization of credit risk and its effect on the central bank’s reputation, credibility, independence, and ultimately its ability to steer inflation towards its target of close to but below 2% over the medium term.

Against this background, we ask: Can central bank liquidity provision or asset purchases during a liquidity crisis reduce risk in net terms? This could happen if risk taking in one part of the balance sheet (e.g., more asset purchases) de-risks other balance sheet positions (e.g., the collateralized lending portfolio) by a commensurate or even larger amount. How economically important can such risk spillovers be across policy operations? Were the Eurosystem’s financial buffers at all times sufficiently high to match its portfolio tail risks? Finally, did past operations differ in terms of impact per unit of risk?…

We focus on three main findings. First, we find that (Lender of last resort) LOLR- and (Investor of last resort) IOLR-implied credit risks are usually negatively related in our sample. Taking risk in one part of the central bank’s balance sheet (e.g., the announcement of asset purchases within the Securities Market Programme – SMP) tended to de-risk other positions (e.g., collateralized lending from previous – longer-term refinancing operations LTROs). Vice versa, the allotment of two large-scale (very long-term refinancing operations) VLTRO credit operations each decreased the one-year-ahead expected shortfall of the SMP asset portfolio. This negative relationship implies that central bank risks can be nonlinear in exposures. In bad times, increasing size increases risk less than proportionally. Conversely, reducing balance sheet size may not reduce total risk by as much as one would expect by linear scaling. Arguably, the documented risk spillovers call for a measured approach towards reducing balance sheet size after a financial crisis.

Second, some unconventional policy operations did not add risk to the Eurosystem’s balance sheet in net terms. For example, we find that the initial OMT announcement de-risked the Eurosystem’s balance sheet by e41.4 bn in 99% expected shortfall (ES). As another example, we estimate that the allotment of the first VLTRO increased the overall 99% ES, but only marginally so, by e0.8 bn. Total expected loss decreased, by e1.4 bn. We conclude that, in extreme situations, a central bank can de-risk its balance sheet by doing more, in line with Bagehot’s well-known assertion that occasionally “only the brave plan is the safe plan.” Such risk reductions are not guaranteed, however, and counterexamples exist when risk reductions did not occur.

Third, our risk estimates allow us to study past unconventional monetary policies in terms of their ex-post ‘risk efficiency’. Risk efficiency is the notion that a certain amount of expected policy impact should be achieved with a minimum level of additional balance sheet risk. We find that the ECB’s Outright Monetary Transactions – OMT program was particularly risk efficient ex-post since its announcement shifted long-term inflation expectations from deflationary tendencies toward the ECB’s target of close to but below two percent, decreased sovereign benchmark bond yields for stressed euro area countries, while lowering the risk inherent in the central bank’s balance sheet. The first allotment of VLTRO funds appears to have been somewhat more risk-efficient than the second allotment. The SMP, despite its benefits documented elsewhere, does not appear to have been a particularly risk-efficient policy measure.

This BIS research is an important assessment of the effectiveness of ECB QE. Among other things, the authors find that the ‘shock and awe’ effectiveness of the first ‘quantitative treatment’ soon diminished. Liquidity is the methadone of the market, for QE to work in future, a larger and more targeted dose of monetary alchemy will be required.

The paper provides several interesting findings, for example, the Federal Reserve ‘taper-tantrum’ of 2013 and the Swiss National Bank decision to unpeg the Swiss Franc in 2015, did not appear to influence markets inside the Eurozone, once ECB president, Mario Draghi, had made its intensions plain. Nonetheless, the BIS conclude that (emphasis, once again, is mine): –

…collateralized credit operations imply substantially less credit risks (by at least one order of magnitude in our crisis sample) than outright sovereign bond holdings per e1 bn of liquidity owing to a double recourse in the collateralized lending case. Implementing monetary policy via credit operations rather than asset holdings, whenever possible, therefore appears preferable from a risk efficiency perspective. Second, expanding the set of eligible assets during a liquidity crisis could help mitigate the procyclicality inherent in some central bank’s risk protection frameworks.

In other words, rather than exacerbate the widening of credit spreads by purchasing sovereign debt, it is preferable for central banks to lean against the ‘flight to quality’ tendency of market participants during times of stress.

The authors go on to look at recent literature on the stress-testing of central bank balance sheets, mainly focussing on analysis of the US Federal Reserve. Then they review ‘market-risk’ methods as a solution to the ‘credit-risk’ problem, employing non-Gaussian methods – a prescient approach after the unforeseen events of 2008.

Bagehot thou shouldst be living at this hour (with apologies to Wordsworth)

The BIS authors refer on several occasions to Bagehot. I wonder what he would make of the current state of central banking? Please indulge me in this aside.

Walter Bagehot (1826 to 1877) was appointed by Richard Cobden as the first editor of the Economist. He is also the author of perhaps the best known book on the function of the 19th century money markets, Lombard Street (published in 1873). He is famed for inventing the dictum that a central bank should ‘lend freely, at a penalty rate, against good collateral.’ In fact he never actually uttered these words, they have been implied. Even the concept of a ‘lender of last resort’, to which he refers, was not coined by him, it was first described by Henry Thornton in his 1802 treatise – An Enquiry into the Nature and Effects of the Paper Credit of Great Britain.

To understand what Bagehot was really saying in Lombard Street, this essay by Peter Conti-Brown – Misreading Walter Bagehot: What Lombard Street Really Means for Central Banking – provides an elegant insight: –

Lombard Street was not his effort to argue what the Bank of England should do during liquidity crises, as almost all people assume; it was an argument about what the Bank of England should openly acknowledge that it had already done.

Bagehot was a classical liberal, an advocate of the gold standard; I doubt he would approve of the nature of central banks today. He would, I believe, have thrown his lot in with the likes of George Selgin and other proponents of Free Banking.

Conclusion and Investment Opportunities

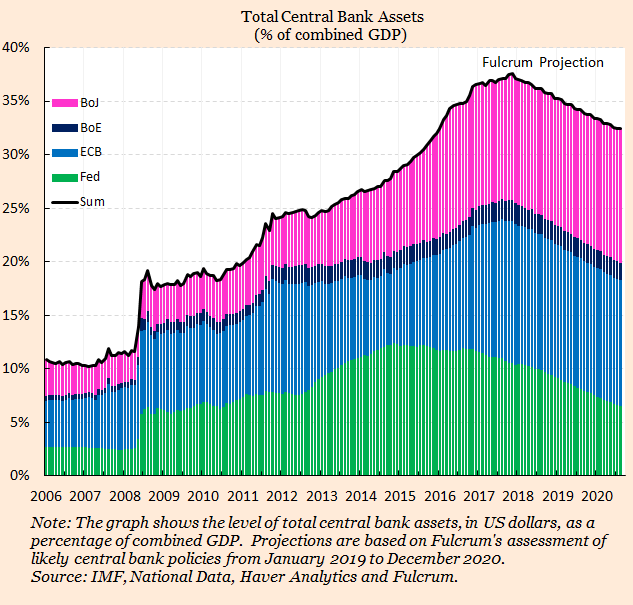

Given the weakness of European economies it seems unlikely that the ECB will be able to follow the lead of the Federal Reserve and raise interest rates in any meaningful way. The unwinding of, at least a portion of, QE might be easier, since many of these refinancing operations will naturally mature. For arguments both for and against CB balance sheet reduction this paper by Charles Goodhart – A Central Bank’s optimal balance sheet size? is well worth reviewing. A picture, however, is worth a thousand words, although I think the expected balance sheet reduction may be overly optimistic: –

Source: IMF, Haver Analytics, Fulcrum Asset Management

Come the next crisis, I expect the ECB to broaden the range of eligible securities and instruments that it is prepared to purchase. The ‘Draghi Put’ will gain greater credence as it encompasses a wider array of credits. The ‘Flight to Quality’ effect, driven by swathes of investors forsaking equities and corporate bonds, in favour of ‘risk-free’ government securities, will be shorter-lived and less extreme. The ‘Convergence Trade’ between the yields of European government bonds will regain pre-eminence; I can conceive the 10yr BTP/Bund spread testing zero.

None of this race to zero will happen in a straight line, but it is important not to lose sight of the combined power of qualitative and quantitative easing. The eventual ‘socialisation’ of common stock is already taking place in Japan. Make no mistake, it is already being contemplated by a central bank near you, right now.

![]()

Macro Letter – No 109 – 01-02-2019

Sustainable government debt – an old idea refreshed

The Peterson Institute has long been one of my favourite sources of original research in the field of economics. They generally support free-market ideas, although they are less than classically liberal in their approach. I was, nonetheless, surprised by the Presidential Lecture given at the annual gathering of the American Economic Association (AEA) by Olivier Blanchard, ex-IMF Chief Economist, now at the Peterson Institute – Public Debt and Low Interest Rates. The title is quite anodyne, the content may come to be regarded as incendiary. Here is part of his introduction: –

Since 1980, interest rates on U.S. government bonds have steadily decreased. They are now lower than the nominal growth rate, and according to current forecasts, this is expected to remain the case for the foreseeable future. 10-year U.S. nominal rates hover around 3%, while forecasts of nominal growth are around 4% (2% real growth, 2% inflation). The inequality holds even more strongly in the other major advanced economies: The 10-year UK nominal rate is 1.3%, compared to forecasts of 10-year nominal growth around 3.6% (1.6% real, 2% inflation). The 10-year Euro nominal rate is 1.2%, compared to forecasts of 10-year nominal growth around 3.2% (1.5% real, 2% inflation). The 10-year Japanese nominal rate is 0.1%, compared to forecasts of 10-year nominal growth around 1.4% (1.0% real, 0.4% inflation).

The question this paper asks is what the implications of such low rates should be for government debt policy. It is an important question for at least two reasons. From a policy viewpoint, whether or not countries should reduce their debt, and by how much, is a central policy issue. From a theory viewpoint, one of pillars of macroeconomics is the assumption that people, firms, and governments are subject to intertemporal budget constraints. If the interest rate paid by the government is less the growth rate, then the intertemporal budget constraint facing the government no longer binds. What the government can and should do in this case is definitely worth exploring.

The paper reaches strong, and, I expect, surprising, conclusions. Put (too) simply, the signal sent by low rates is that not only debt may not have a substantial fiscal cost, but also that it may have limited welfare costs.

Blanchard’s conclusions may appear radical, yet, in my title, I refer to this as an old idea, allow me to explain. In business it makes sense, all else equal, to borrow if the rate of interest paid on your loan is lower than the return from your project. At the national level, if the government can borrow at below the rate of GDP growth it should be sustainable, since, over time (assuming, of course, that it is not added to) the ratio of debt to GDP will naturally diminish.

There are plenty of reasons why such borrowing may have limitations, but what really interests me, in this thought provoking lecture, is the reason governments can borrow at such low rates in the first instance. One argument is that as GDP grows, so does the size of the tax base, in other words, future taxation should be capable of covering the on-going interest on today’s government borrowing: the market should do the rest. Put another way, if a government become overly profligate, yields will rise. If borrowing costs exceed the expected rate of GDP there may be a panicked liquidation by investors. A government’s ability to borrow will be severely curtailed in this scenario, hence the healthy obsession, of many finance ministers, with debt to GDP ratios.

There are three factors which distort the cosy relationship between the lower yield of ‘risk-free’ government bonds and the higher percentage levels of GDP growth seen in most developed countries; investment regulations, unfunded liabilities and fractional reserve bank lending.

Let us begin with investment regulations, specifically in relation to the constraints imposed on pension funds and insurance companies. These institutions are hampered by prudential measures intended to guarantee that they are capable of meeting payment obligations to their customers in a timely manner. Mandated investment in liquid assets are a key construct: government bonds form a large percentage of their investments. As if this was not sufficient incentive, institutions are also encouraged to purchase government bonds as a result of the zero capital requirements for holding these assets under Basel rules.

A second factor is the uncounted, unfunded, liabilities of state pension funds and public healthcare spending. I defer to John Mauldin on this subject. The 8th of his Train-Wreck series is entitled Unfunded Promises – the author begins his calculation of total US debt with the face amount of all outstanding Treasury paper, at $21.2trln it amounts to approximately 105% of GDP. This is where the calculations become disturbing: –

If you add in state and local debt, that adds another $3.1 trillion to bring total government debt in the US to $24.3 trillion or more than 120% of GDP.

Mauldin goes on to suggest that this still underestimates the true cost. He turns to the Congressional Budget Office 2018 Long-Term Budget Outlook – which assumes that federal spending will grow significantly faster than federal revenue. On the basis of their assumptions, all federal tax revenues will be consumed in meeting social security, health care and interest expenditures by 2041.

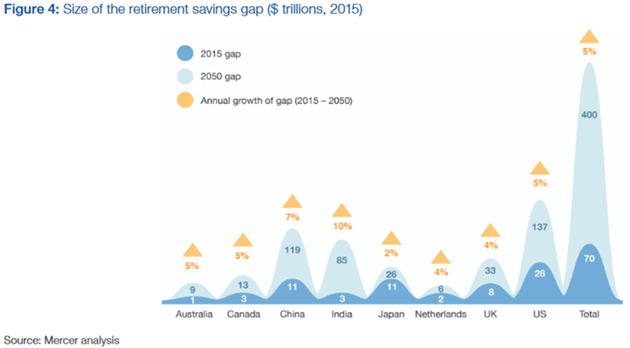

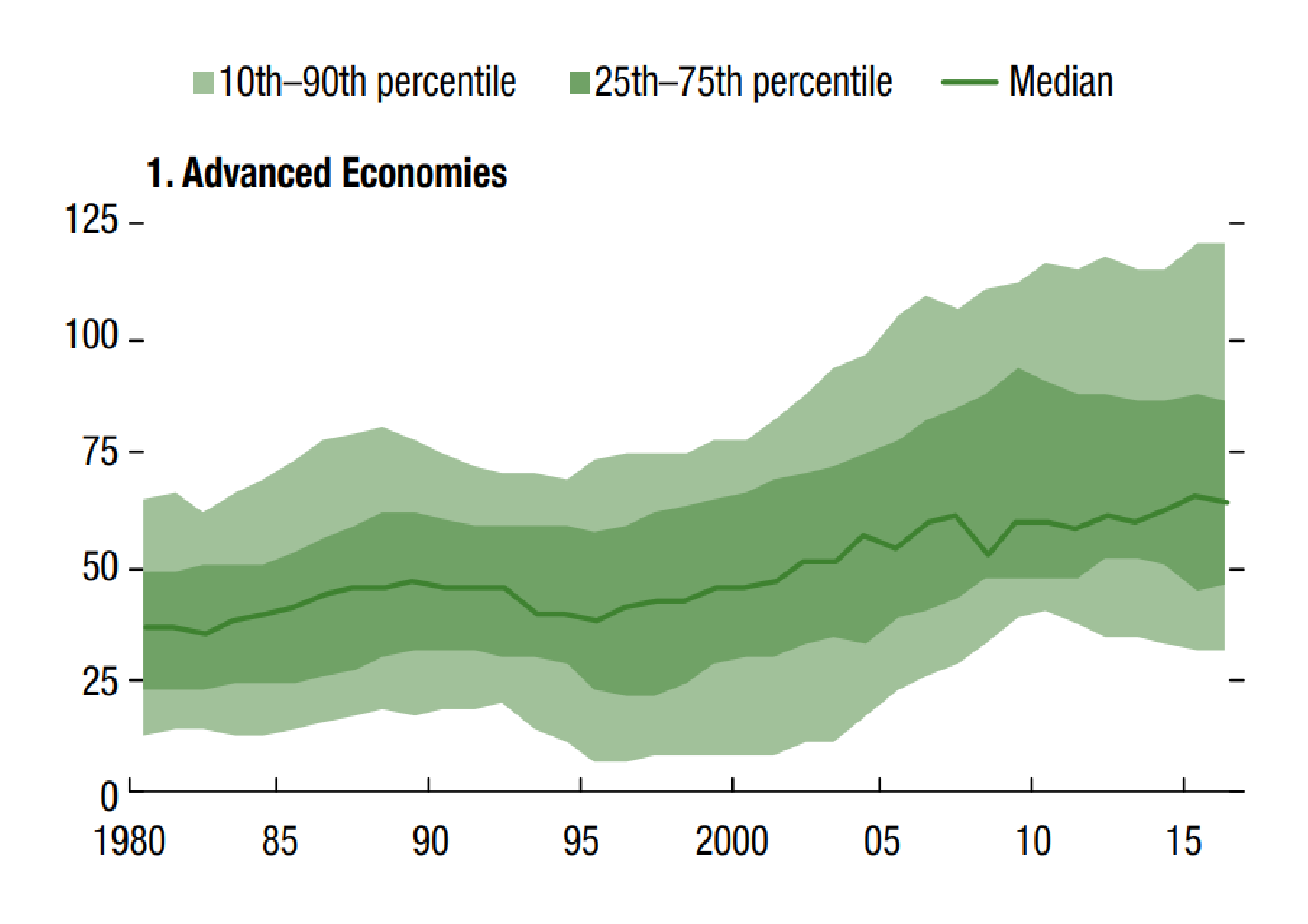

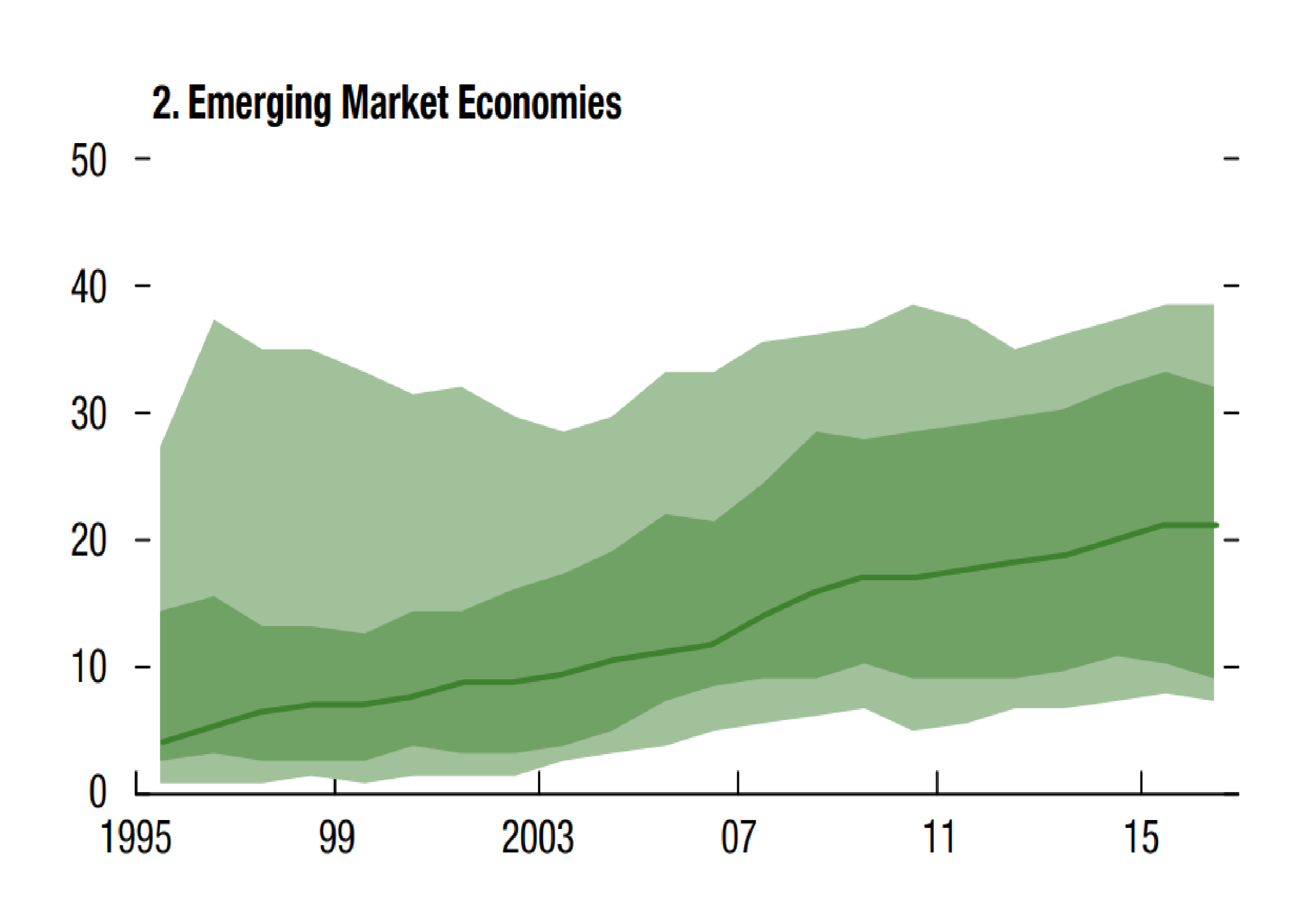

Extrapolate this logic to other developed economies, especially those with more generous welfare commitments than the US, and the outlook for rapidly aging, welfare addicted developed countries is bleak. In a 2017 white paper by Mercer for World Economic Forum – We Will Live to 100 – the author estimates that the unfunded liabilities of US, UK, Netherlands, Japan, Australia, Canada, China and India will rise from $70trln in 2015 to $400trln in 2050. These countries represent roughly 60% of global GDP. I extrapolate global unfunded liabilities of around $120trln today rising to nearer $650trln within 20 years: –

Source: Mercer analysis

For an in depth analysis of the global pension crisis this 2016 research paper from Citi GPS – The Coming Pensions Crisis – is a mine of information.

In case you are still wondering how, on earth, we got here? This chart from Money Week shows how a combination of increased fiscal spending (to offset the effect of the bursting of the tech bubble in 2000) combined with the dramatic fall in interest rates (since the great financial recession of 2008/2009) has damaged the US state pension system: –

Source: Moneyweek

The yield on US Treasury bonds has remained structurally higher than most of the bonds of Europe and any of Japan, for at least a decade.

The third factor is the fractional reserve banking system. Banks serve a useful purpose intermediating between borrowers and lenders. They are the levers of the credit cycle, but their very existence is testament to their usefulness to their governments, by whom they are esteemed for their ability to purchase government debt. I discuss – A history of Fractional Reserve Banking – or why interest rates are the most important influence on stock market valuations? in a two part essay I wrote for the Cobden Centre in October 2016. In it I suggest that the UK banking system, led by the Bank of England, has enabled the UK government to borrow at around 3% below the ‘natural rate’ of interest for more than 300 years. The recent introduction of quantitative easing has only exaggerated the artificial suppression of government borrowing costs.

Before you conclude that I am on a mission to change the world financial system, I wish to point out that if this suppression of borrowing costs has been the case for more than 300 years, there is no reason why it should not continue.

Which brings us back to Blanchard’s lecture at the AEA. Given the magnitude of unfunded liabilities, the low yield on government bonds is, perhaps, even more remarkable. More alarmingly, it reinforces Blanchard’s observation about the greater scope for government borrowing: although the author is at pains to advocate fiscal rectitude. If economic growth in developed economies stalls, as it has for much of the past two decades in Japan, then a Japanese redux will occur in other developed countries. The ‘risk-free’ rate across all developed countries will gravitate towards the zero bound with a commensurate flattening in yield curves. Over the medium term (the next decade or two) an increasing burden of government debt can probably be managed. Some of the new borrowing may even be diverted to investments which support higher economic growth. The end-game, however, will be a monumental reckoning, involving wholesale debt forgiveness. The challenge, as always, will be to anticipate the inflection point.

Conclusion and Investment Opportunities

Since the early-1990’s analysts have been predicting the end of the bond bull market. Until quite recently it was assumed that negative government bond yields were a temporary aberration reflecting stressed market conditions. When German schuldscheine (the promissory notes of the German banking system) traded briefly below the yield of German Bunds, during the reunification in 1989, the ‘liquidity anomaly’ was soon rectified. There has been a sea-change, for a decade since 2008, US 30yr interest rate swaps traded at a yield discount to US Treasuries – for more on this subject please see – Macro Letter – No 74 – 07-04-2017 – US 30yr Swaps have yielded less than Treasuries since 2008 – does it matter?

With the collapse in interest rates and bond yields, the unfunded liabilities of governments in developed economies has ballooned. A solution to the ‘pension crisis,’ higher bond yields, would sow the seeds of a wider economic crisis. Whilst governments still control their fiat currencies and their central banks dictate the rate of interest, there is still time – though, I doubt, the political will – to make the gradual adjustments necessary to right the ship.

I have been waiting for US 10yr yields to reach 4.5%, I may be disappointed. For investors in fixed income securities, the bond bull market has yet to run its course. Negative inflation adjusted returns will become the norm for risk-free assets. Stock markets may be range-bound for a protracted period as return expectations adjust to a structurally weaker economic growth environment.

![]()

Macro Letter – No 98 – 08-06-2018

Italy and the repricing of European government debt

I have never been a great advocate of long-term investment in fixed income securities, not in a world of artificially low official inflation indices and fiat currencies. Given the de minimis real rate of return I regard them as trading assets. I will freely admit that this has led me to make a number of investment mistakes, although these have generally been sins of omission rather than actual investment losses. The Italian political situation and the sharp rise in Italian bond yields it precipitated, last week, is, therefore, some justification for an investor like myself, one who has not held any fixed income securities since 2010.

An excellent overview of the Italian political situation is contained in the latest essay from John Mauldin of Mauldin Economics – From the Front Line – The Italian Trigger:-

Italy had been without a government since its March 4 election, which yielded a hung parliament with no party or coalition holding a majority. The Five Star Movement and Lega Nord finally reached a deal, to most everyone’s surprise since those two parties, while both broadly populist, have some big differences. Nonetheless, they found enough common ground to propose a cabinet to President Sergio Mattarella.

Italian presidents are generally seen as rubberstamp figureheads. They really aren’t supposed to insert themselves into the process. Yet Mattarella unexpectedly rejected the coalition’s proposed finance minister, 81-year-old economist Paolo Savona, on the grounds Savona had previously opposed Italy’s eurozone membership. This enraged Five Star and Lega Nord, who then ended their plans to form a government and threatened to impeach Mattarella.

The whole article is well worth reading and goes on to look at debt from a global perspective. John anticipates what he calls, ‘The Great Reset,’ when the reckoning for the excessive levels of debt arrives.

Returning to the repricing of Eurozone (EZ) debt last month, those readers who have followed my market commentaries since the 1990’s, might recall an article I penned about the convergence of European government bond yields in the period preceding the introduction of the Euro. At that juncture (1998) excepting Greece, every bond market, whose government was about to adopt the Euro, was trading at a narrower credit spread to 10yr German bunds than the yield differential between the highest and lowest credit in the US municipal bond market. The widest differential in the muni-market at that time was 110bp. It was between Alabama and California – remember this was prior to the bursting of the Tech bubble.

In my article I warned about the risk of a significant repricing of European credit spreads once the honeymoon period of the single currency had ended. I had to wait more than a decade, but in 2010/2011 it looked as if I might be vindicated – this column is not entitled In the Long Run without just cause – then what one might dub the Madness of Crowds of Central Bankers intervened, saved the EZ and consigned my cautionary oracles, on the perils of the quest for yield, to the dustbin of history.

In the intervening period, since 2011, I have watched European yields inexorably converge and absolute yields turn negative, in several EZ countries, with a temerity which smacks of permanence. I have also arrived at a new conclusion about the limits of credit risk within a currency union: that they are governed by fiat in much the same manner as currencies. As long as the market believes that Mr Draghi will do, ‘…whatever it takes,’ investors will be enticed by relatively small yield enhancements.

Let me elaborate on this newly-minted theory by way of an example. Back in March 2012, Greek 10yr yields reached 41.77% at that moment German 10yr yields were a mere 2.08%. The risk of contagion was steadily growing, as other peripheral EZ bond markets declined. Greece, in and of itself, was and remains, a small percentage of EZ GDP, but, as Portuguese and Spanish bonds began to follow the lead of Greece, the fear at the ECB – and even at the Bundesbank – was that Italy might succumb to contagion. Due to its size, the Italian bond market, was then, and remains today, the elephant in the room.

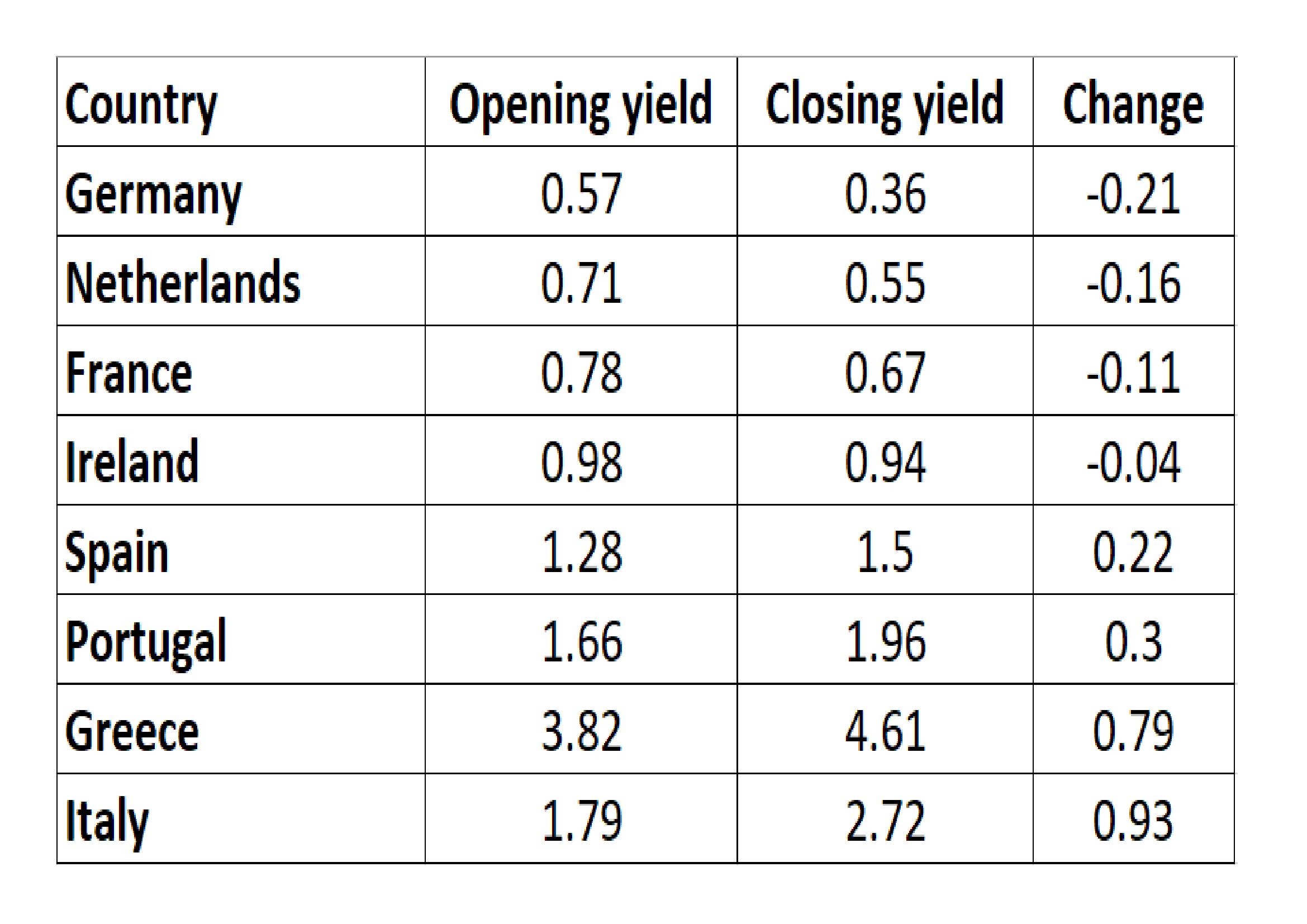

During the course of last month, European bond markets diverged. The table below shows the change in 10yr yields between 1st and 31st May:-

Source: Investing.com

A certain degree of contagion is evident, although the PIGS have lost an ‘I’ as Irish Gilts have escaped the pejorative acronym.

At the peaks of the previous crisis, Irish 10yr Gilts made a yield high of 14.61% in July 2011, at which point their spread versus 10yr Bunds was 11.34%. When Italy entered her own period of distress, in November of that year, the highest 10yr BTP yield recorded was 7.51% and the spread over Germany reached 5.13%. By the time Greek 10yr yields reached their zenith, in March 2012, German yields were already lower and Irish and Italian spreads had begun to narrow.

During the course of last month the interest rate differential between 10yr Bunds and their Irish, Greek and Italian counterparts widened by 41, 100 and 114bp respectively. Italian 10yr yields closed at 4.25% over Bunds, less than 100bp from their 2011 crisis highs. With absolute yields significantly lower today (German 10yr yields were 2.38% in November 2011 they ended May 2018 at 36bp) the absolute percentage return differential is even higher than during the 2011 period. At 2.72% BTPs offer a return which is 7.5 times greater than 10yr Bunds. Back in 2011 the 7.51% yield was a little over three times the return available from 10yr Bunds.

I am forced to believe the reaction of the BTP market has been excessive and that spreads will narrow during the next few months. If I am incorrect in my expectation, it will fall to Mr Draghi to intervene. The Outright Monetary Transactions – OMT – policy of the ECB allows it to purchase a basket of European government bonds on a GDP weighted basis. If another crisis appears immanent they could adjust this policy to duration weight their purchases. It would then permit them to buy a larger proportion of the higher yielding, higher coupon bonds of the southern periphery. There would, no doubt, be complaints from those countries that practice greater fiscal rectitude, but the policy shift could be justified on investment grounds. If the default risk of all members of the EZ is equal due to the political will of the European Commission, then it makes sense from an investment perspective for the ECB to purchase higher yielding bonds if they have the same credit risk. A new incarnation of the Draghi Put could be implemented without too many objections from Frankfurt.

Conclusions and investment opportunities

I doubt we will see a repeat of the 2011/2012 period. Lightening seldom strikes twice in the same way. The ECB will continue with its QE programme and this will ensure that EZ government bond yields remain at artificially low levels for the foreseeable future.

Unusually, I have an actionable trade idea: caveat emptor! I believe the recent widening of the 10yr Italian BTP/Spanish Bonos spread has been excessive. If there is bond market contagion, as a result of the political situation in Italy, Bonos yields may have difficulty defying gravity. If the Italian political environment should improve, the over-sold BTP market should rebound. If the ECB are forced to act to avert a new EZ crisis by increasing OMT or implementing a duration weighted approach to QE, Italy should benefit more than Spain until the yield differential narrows.

![]()

Macro Letter – No 96 – 04-05-2018

Is the US exporting a recession?

After last week’s ECB meeting, Mario Draghi gave the usual press conference. He confirmed the continuance of stimulus and mentioned the moderation in the rate of growth and below-target inflation. He also referred to the steady expansion in money supply. When it came to the Q&A he revealed rather more:-

It’s quite clear that since our last meeting, broadly all countries experienced, to different extents of course, some moderation in growth or some loss of momentum. When we look at the indicators that showed significant, sharp declines, we see that, first of all, the fact that all countries reported means that this loss of momentum is pretty broad across countries.

It’s also broad across sectors because when we look at the indicators, it’s both hard and soft survey-based indicators. Sharp declines were experienced by PMI, almost all sectors, in retail, sales, manufacturing, services, in construction. Then we had declines in industrial production, in capital goods production. The PMI in exports orders also declined. Also we had declines in national business and confidence indicators.

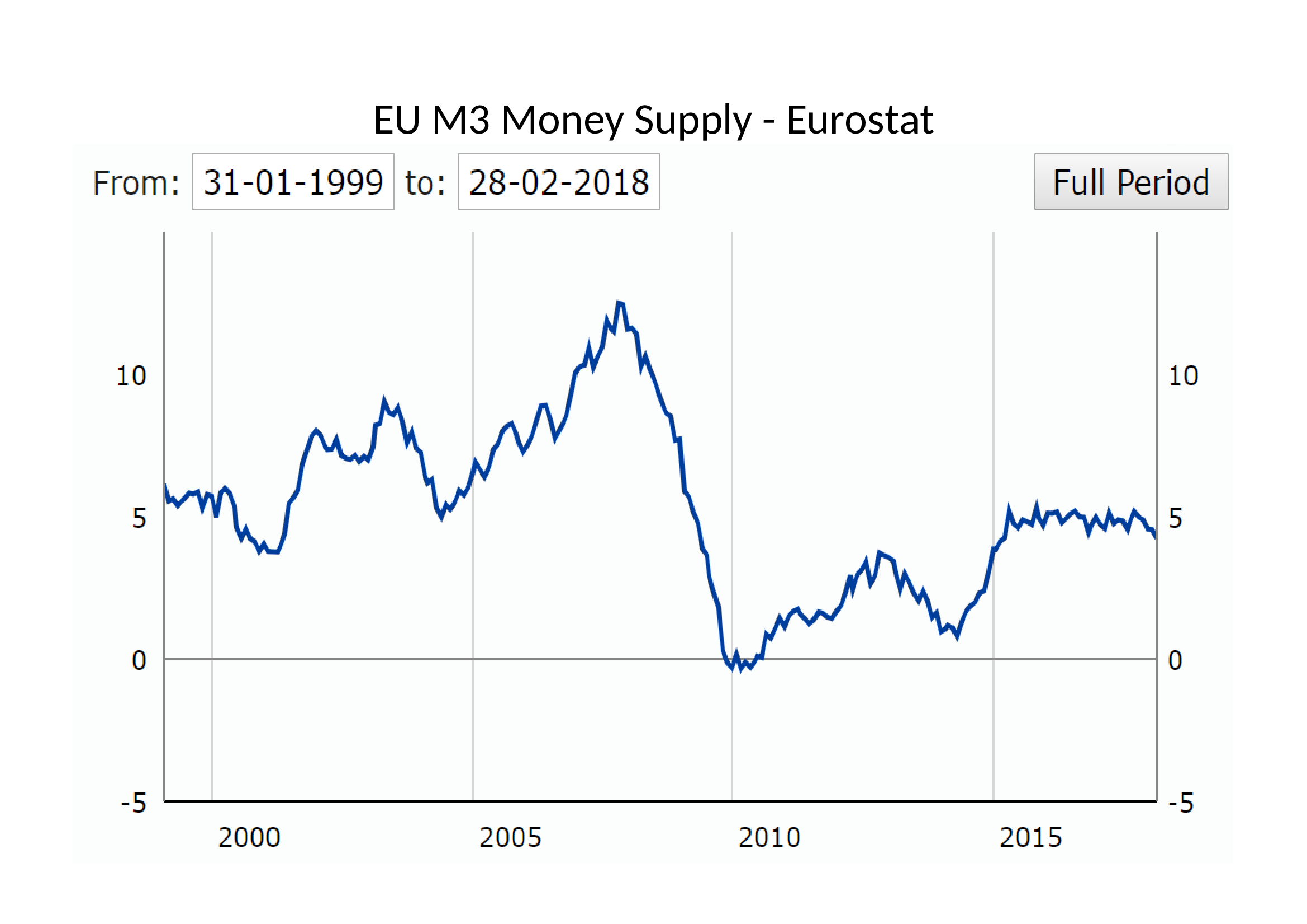

I quote this passage out of context because the entire answer was more nuanced. My reason? To highlight the difference between the situation in the EU and the US. In Europe, money supply (M3) is growing at 4.3% yet inflation (HICP) is a mere 1.3%. Meanwhile in the US, inflation (CPI) is running at 2.4% and money supply (M2) is hovering a fraction above 2%. Here is a chart of Eurozone M3 since 1999:-

Source: Eurostat

The recent weakening of momentum is a concern, but the absolute level is consistent with a continued expansion.

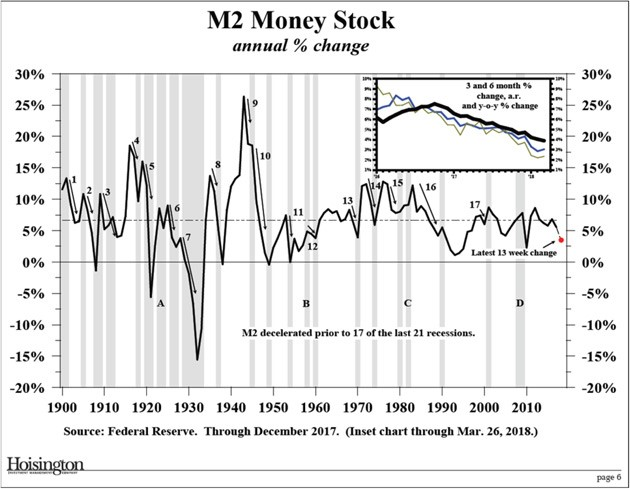

Looked at over a rather longer time horizon, here is a chart of US M2 since 1900:-

Source: Hoisington Asset Management, Federal Reserve

The letters A, B, C, D denote the only occasions, during the last 118 years, when a decline in the expansion (or, during the 1930’s, contraction) of M2 did not lead to a recession. 17 out of 21 is a quite compelling record.

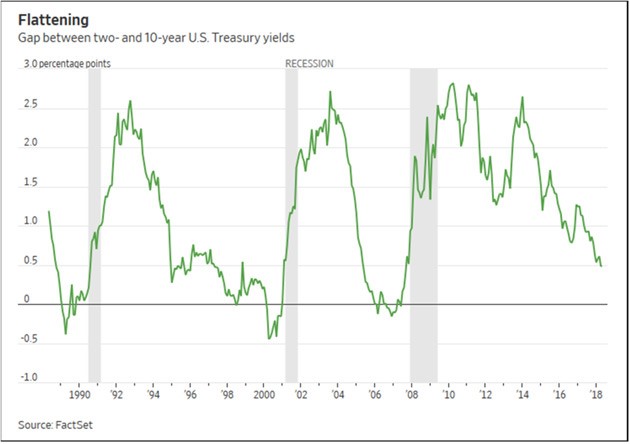

Another concern for markets is the flatness of the US yield curve. Here is the 2yr – 10yr yield differential since 1990:-

Source: Factset, Mauldin Economics

More importantly, for international borrowers, the 6-month LIBOR rate has risen by more than 60 basis points since the start of the year (from 1.8% to 2.5%) whilst 30yr Swap rates have increased by only 40 basis points (2.6% to 3%). The 10yr – 30yr Swap curve is now practically flat.

Also worthy of comment, as US Treasury yields have risen, the relationship between Bonds and Swaps has begun to normalise – 30yr T-Bond yields are only 40 basis points above their level of January and roughly at the same level as in the spring of last year. In April 2017 I wrote in Macro Letter – No 74 – US 30yr Swaps have yielded less than Treasuries since 2008 – does it matter?:-

Today the IRS market increasingly determines the cost of finance, during the next crisis IRS yields may rise or fall by substantially more than the same maturity of US T-bond, but that is because they are the most liquid instruments and are only indirectly supported by the Central Bank.

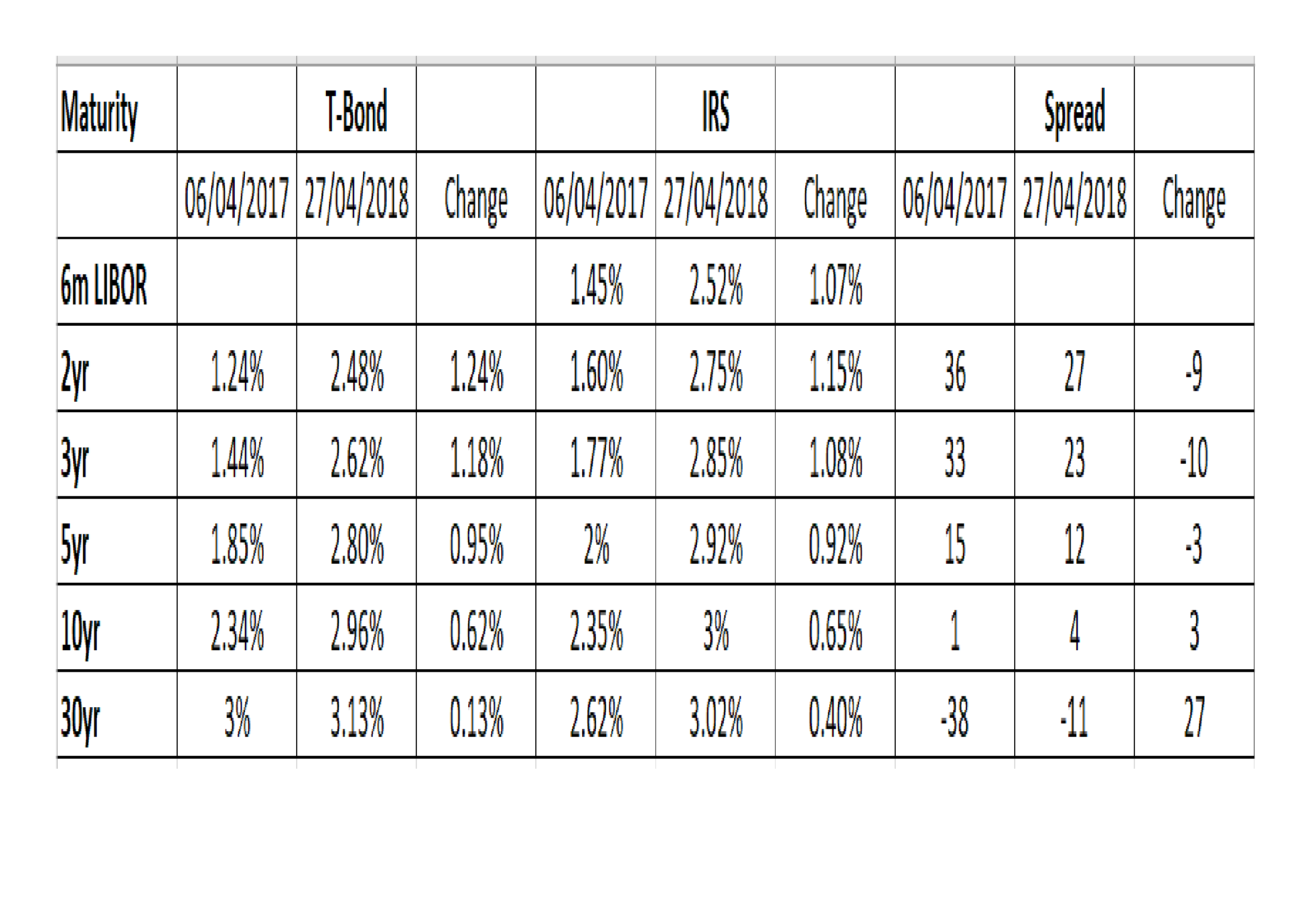

It looks like I may have to eat my words, here is the Bond vs Swap table revisited:-

Source: Investing.com, Interestrateswaps.com, BBA

What is evident is that the Bond/Swap inversion in the longer maturities has closed substantially even as shorter maturity spreads have narrowed. Federal Reserve policy has been the dominate factor.

Why is it, however, that the effect of higher US rates is, seemingly, felt more poignantly in Europe than the US? Does this bring us back to protectionism? Perhaps, but in less contentious terms, the US has run a capital account surplus for many years. Outside the US investment is closely tied to LIBOR financing costs, these have remained higher, except in the longest maturities, and these rates have risen most precipitously this year. Looked at another way, the higher interest rate policies of the Federal Reserve, despite the continued largesse of other central banks, is exporting the next recession to the rest of the world.

I ended Macro Letter – No 74 back in April 2017 – saying:-

Meanwhile, although interest rates have risen from historic lows they remain far below their long run average. Pension funds and other long-term investors still require 7% or more in annualised returns in order to meet their liabilities. They are being forced to continuously increase their investment risk and many have chosen to use the swap market. The next crisis is likely to see an even more pronounced unravelling than in 2008/2009. The unravelling may not happen for some while but the stresses are likely to be focused on the IRS market.

One year on, cracks in the capital markets edifice are beginning to become more evident. GDP growth has started to rollover in the US, Eurozone and Japan. Yields are still relatively low but the absolute increase in rates for shorter maturities (e.g. the near doubling of US 2yr yields from 1.25% to 2.5% in a single year) is guaranteed to take its toll on corporate interest servicing costs. US capital markets are the envy of the world. They are deep and allow borrowers to finance far into the future. The rest of the world is forced to borrow at shorter tenors. A three basis point narrowing of 5yr spreads between Swaps and Bonds is hardly compensation for the near 1% increase in interest rates, or, put in starker terms, a 46% increase in absolute borrowing costs.

Conclusion and investment opportunities

How is the rise in borrowing costs impacting the US stock market? Volatility is back, but earnings are robust. Factset – S&P 500 Earnings Season Update: April 27, 2018 – described it thus:-

To date, 53% of the companies in the S&P 500 have reported actual results for Q1 2018. In terms of earnings, more companies are reporting actual EPS above estimates (79%) compared to the five-year average. If 79% is the final percentage for the quarter, it will mark the highest percentage of S&P 500 companies reporting actual EPS above estimates since FactSet began tracking this metric in Q3 2008. In aggregate, companies are reporting earnings that are 9.1% above the estimates, which is also above the five-year average. In terms of sales, more companies (74%) are reporting actual sales above estimates compared to the five-year average. In aggregate, companies are reporting sales that are 1.7% above estimates, which is also above the five-year average. If 1.7% is the final percentage for the quarter, it will mark the largest revenue surprise percentage since FactSet began tracking this metric in Q3 2008.

… The blended (combines actual results for companies that have reported and estimated results for companies that have yet to report), year-over-year earnings growth rate for the first quarter is 23.2% today, which is higher than the earnings growth rate of 18.5% last week. Positive earnings surprises reported by companies in multiple sectors (led by the Information Technology sector) were responsible for the increase in the earnings growth rate for the index during the past week. All 11 sectors are reporting year-over-year earnings growth. Nine sectors are reporting double-digit earnings growth, led by the Energy, Materials, Information Technology, and Financials sectors.

We are more than halfway through Q1 earnings (I’m writing this letter on Wednesday 2nd May). Results have generally been above forecast and now the Fed seems conscious that they must not be too hasty to reverse the effects of both zero rates and QE. Added to which, while US stocks have been languishing mid-range, European stocks have recently broken out of their recent ranges to the upside, despite discouraging economic data.

The US stock market looks less expensive than it did in January 2017, when I wrote Macro Letter – 68 – Equity valuation in a de-globalising world. Then I was looking for stock markets with a low correlation to the US: they were (and remain) hard to find.

Other indicators to watch which exert a strong influence on stocks include the US PMI Index – last at 54.8 up from 54.2 in March. Above 50 there is little cause for concern. For the Eurozone it is even higher at 55.2, whilst throughout G20 no economy is recording a PMI below 50.

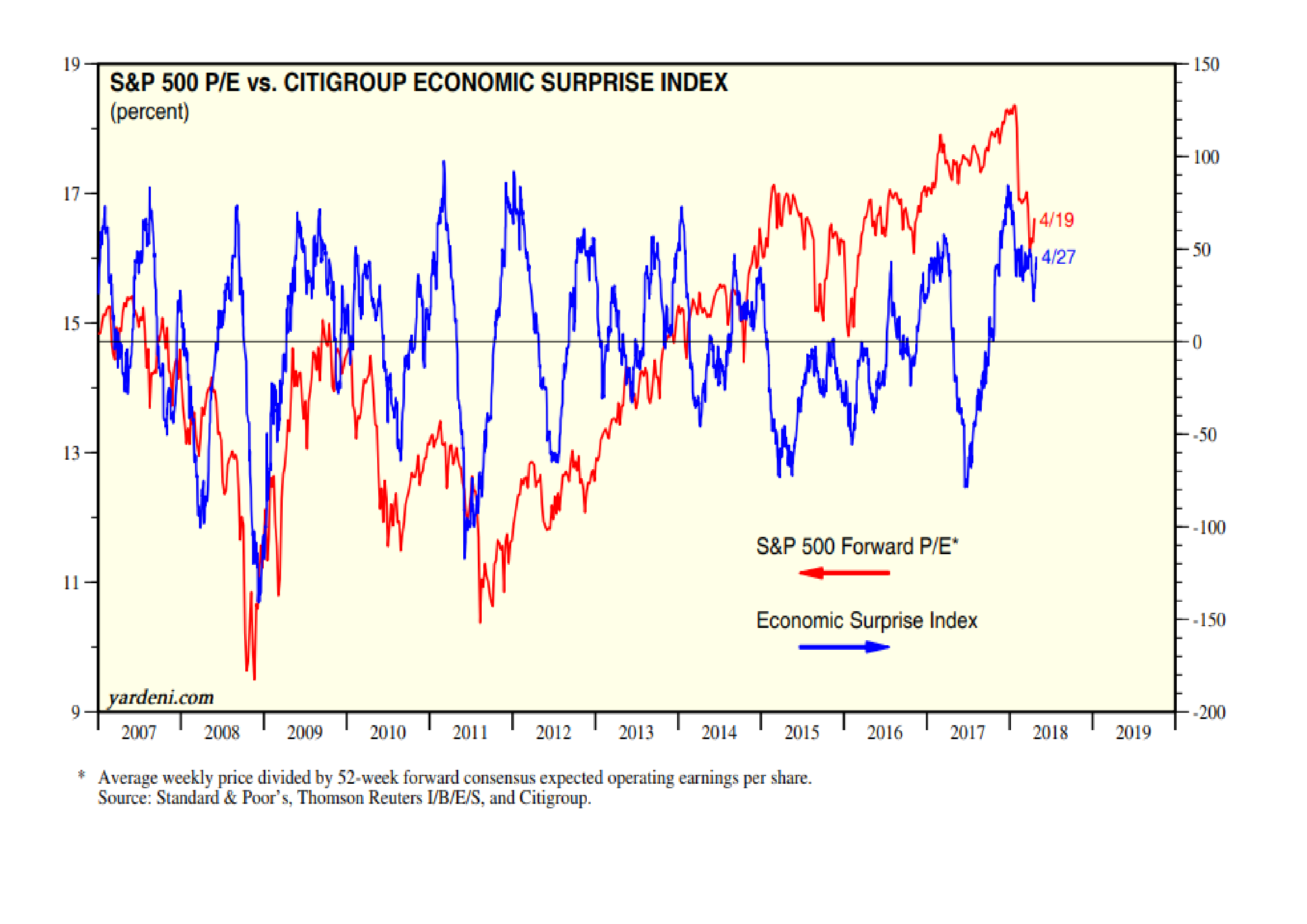

The chart below shows the Citigroup Economic Surprises Index (blue) vs the S&P500 Forward P/E estimates (red):-

Source: Yardeni Research, S&P, Thompson Reuters, Citigroup

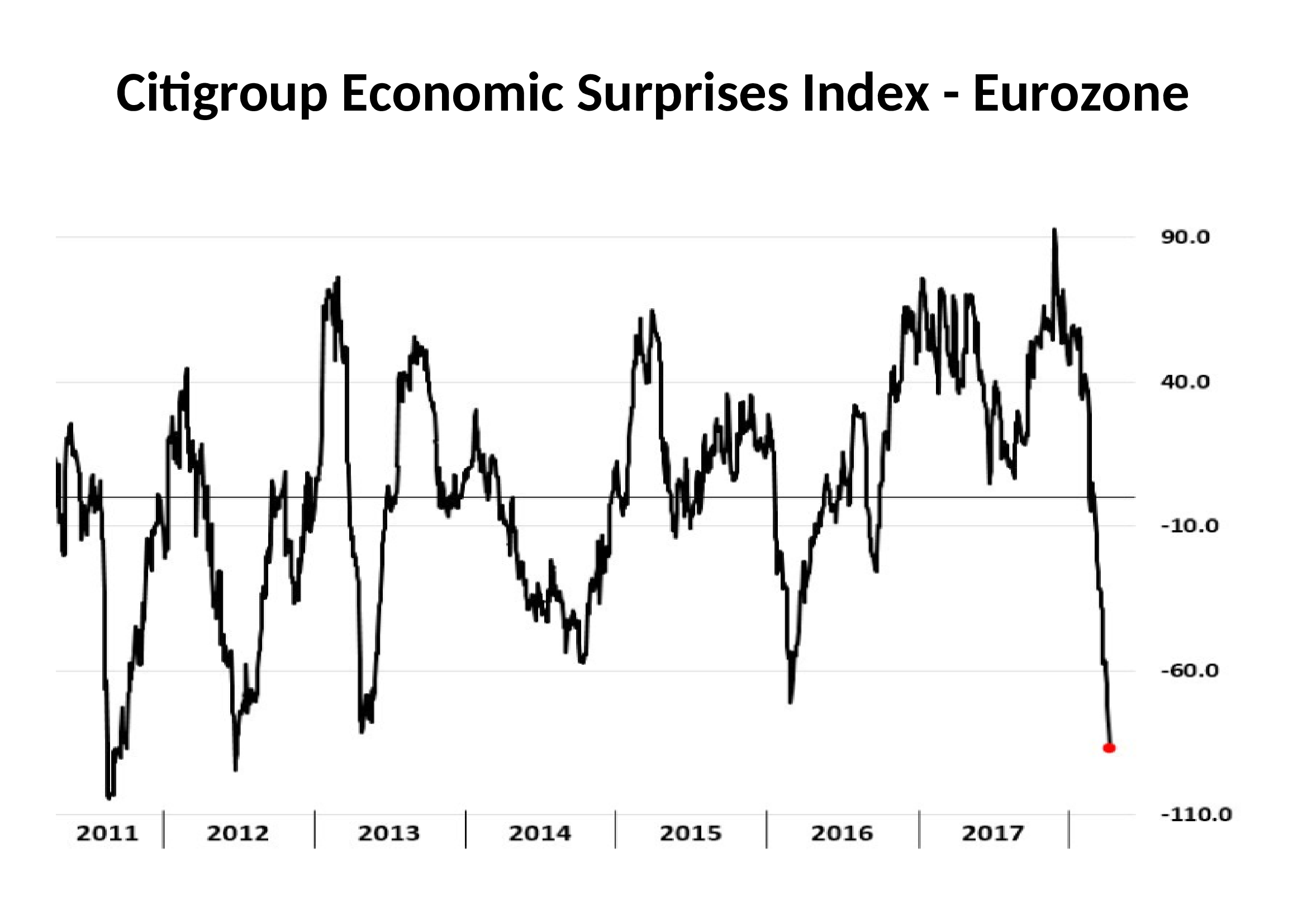

Economic surprises remain positive rather than negative for the US. In the Eurozone it is quite another matter:-

Source: Bloomberg, Citigroup

A number of economic indicators are pointing to a slowdown, yet US stocks are beating estimates. To judge from price action, the market appears to be unimpressed by earnings. I am reminded of the old adage, ‘When all the buyers are in the market it’s time to sell.’ From a technical perspective it makes sense to be patient, but the market has failed to rise substantially on a positive slew of earnings news. This may be because there is a more important factor driving sentiment: the direction of US rates. It certainly appears to have engendered a revival of the US$. It rallied last month having been in a downtrend since January 2017 despite a steadily tightening Federal Reserve. For EURUSD the move from 1.10 to 1.25 appears to have taken its toll. On the basis of the CESI chart, above, if Wall Street sneezes, the Eurozone might catch pneumonia.

![]()

Macro Letter – No 86 – 03-11-2017

Global Real Estate and the end of QE – Is it time to be afraid?

During the past two months two of the world’s leading central banks have begun the process of unwinding or, at least, tapering the quantitative easing which was first initiated after the great financial recession of 2008/2009. The Federal Reserve FOMC statement for September and their Addendum to the Policy Normalization Principles and Plans from June contain the details of the US bank’s policy change. The ECB Monetary policy decision from last week explains the European position.

Whilst the Federal Reserve is reducing its balance sheet by allowing US treasury holdings to mature, the US government has already breached its debt ceiling and will need to issue new bonds. The pace of US money supply growth is unlikely to be reversed. Nonetheless, 10yr US bond yields have risen from a low of 1.35% in July 2016 to more than 2.6% earlier this year. They currently yield around 2.4%. Over the same period 2yr US bond yields have risen from 0.49% to a new high, this week, of 1.60% – their highest since October 2008.

Back in April I wrote about the anomaly in the US interest rate swaps market – US 30yr Swaps have yielded less than Treasuries since 2008 – does it matter? What is interesting to note, in relation to global real estate, is that the 10yr Swap spread over US Treasuries (which is currently negative) has remained stable at -8bp during the recent rise in yields. Normally as interest rates on government bonds declines credit spreads tighten – as rates rise these spreads widen. So far, this has not come to pass.

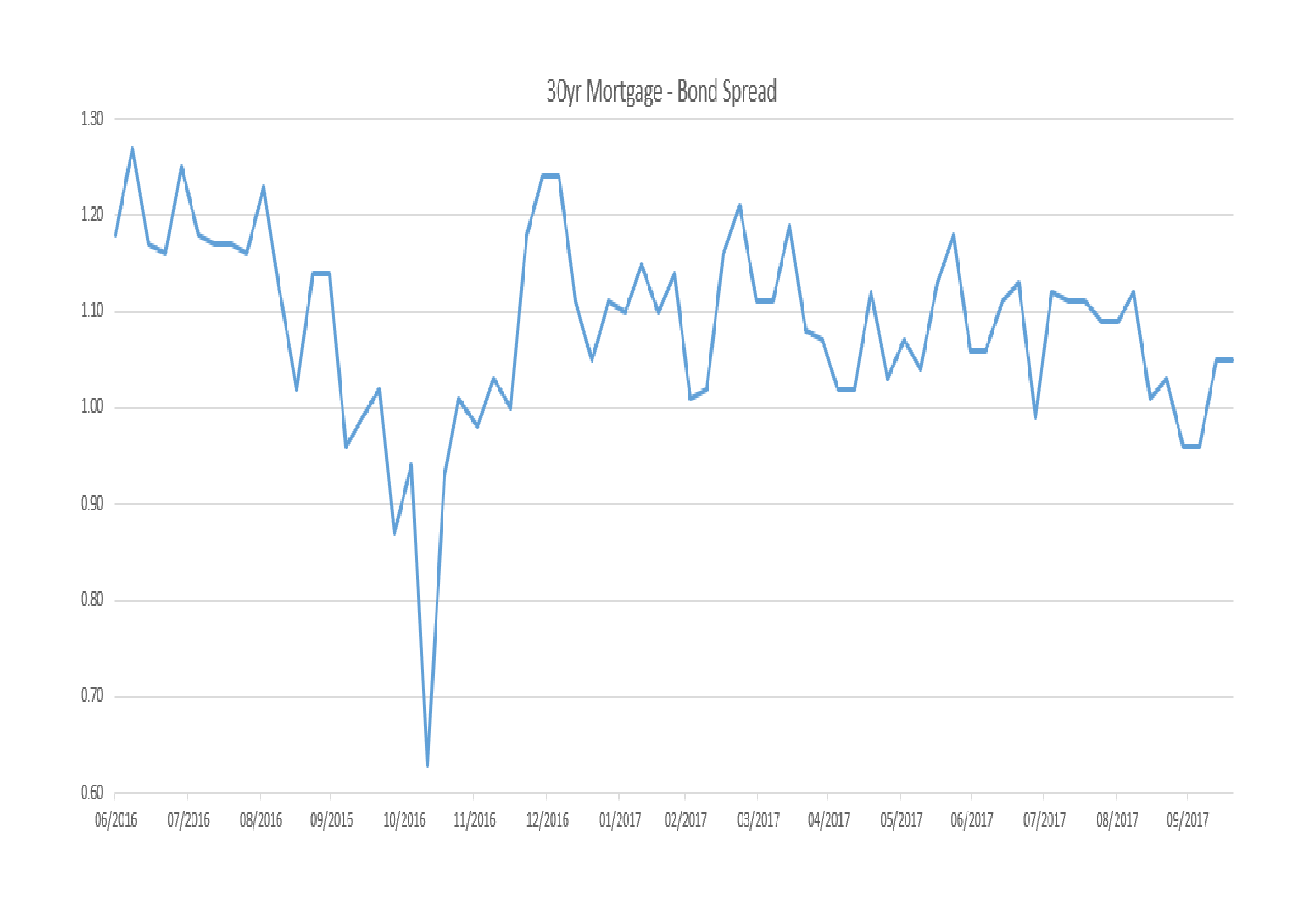

In the US, mortgages are, predominantly, long-term and fixed rate. US 30yr mortgage rates has also risen since July 2016 – from 2.09% to 3.18% at the end of December. Since then rates have moderated, they now stand at 2.89%, approximately 1% above US 30yr bonds. The chart below shows the spread since July 2016:-

Source: Federal Reserve Bank of St Louis

Apart from the aberration during the US presidential elections the spread between 30yr US Treasuries and 30yr Mortgages has been steadily narrowing despite the tightening of short term interest rates and the increase in yields across the maturity spectrum.

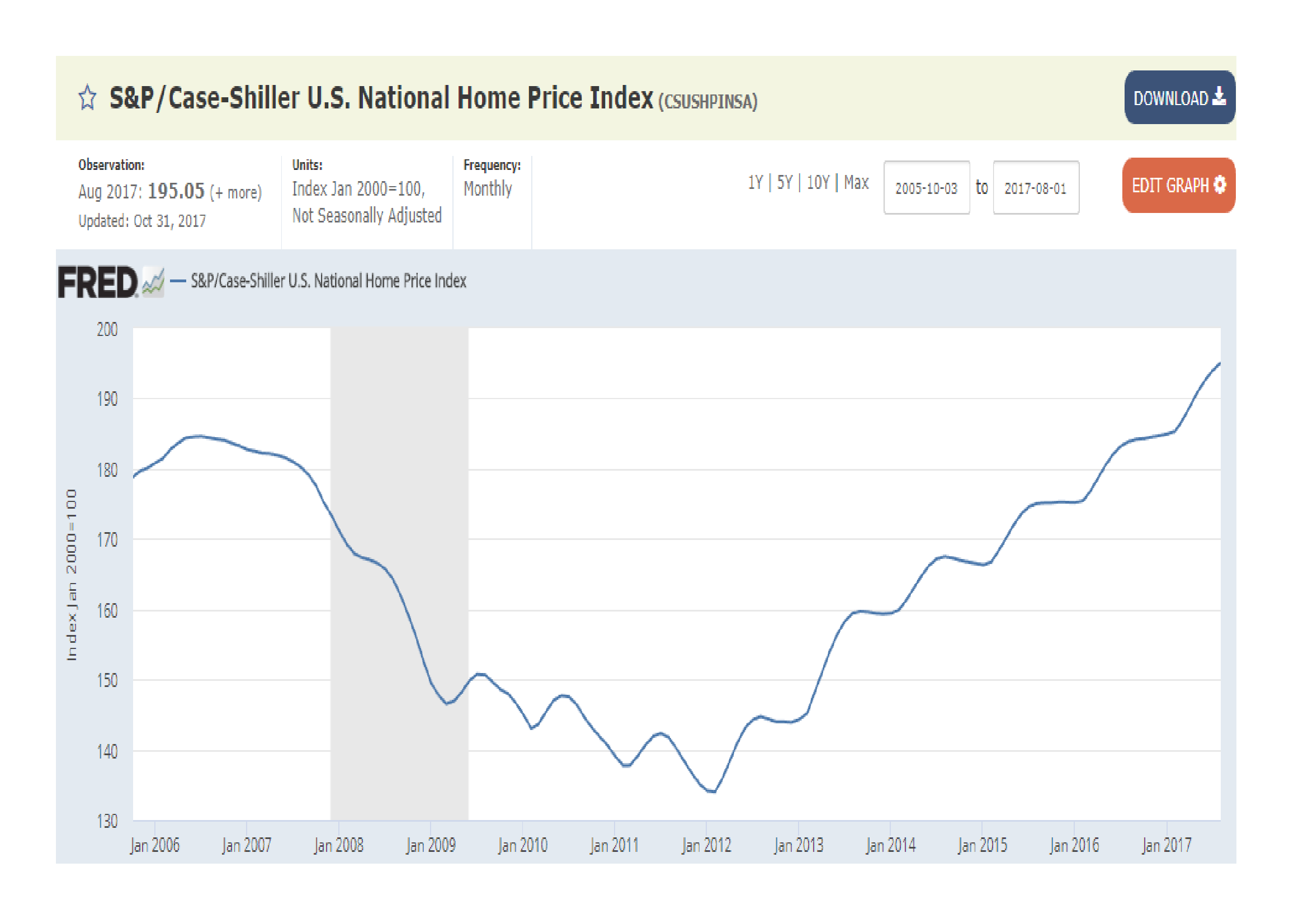

Mortgage finance costs have increased since July 2016 but by less than 50bp. What impact has this had on real estate prices? The chart below shows the S&P Case-Shiller House Price Index since 2006, the increase in mortgage rates has failed to slow the rise in prices. The year on year increase is currently running at 5.6% and forecasters predict this rate to increase to 5.8% when September data is released:-

Source: Federal Reserve Bank of St Louis, S&P Case-Shiller

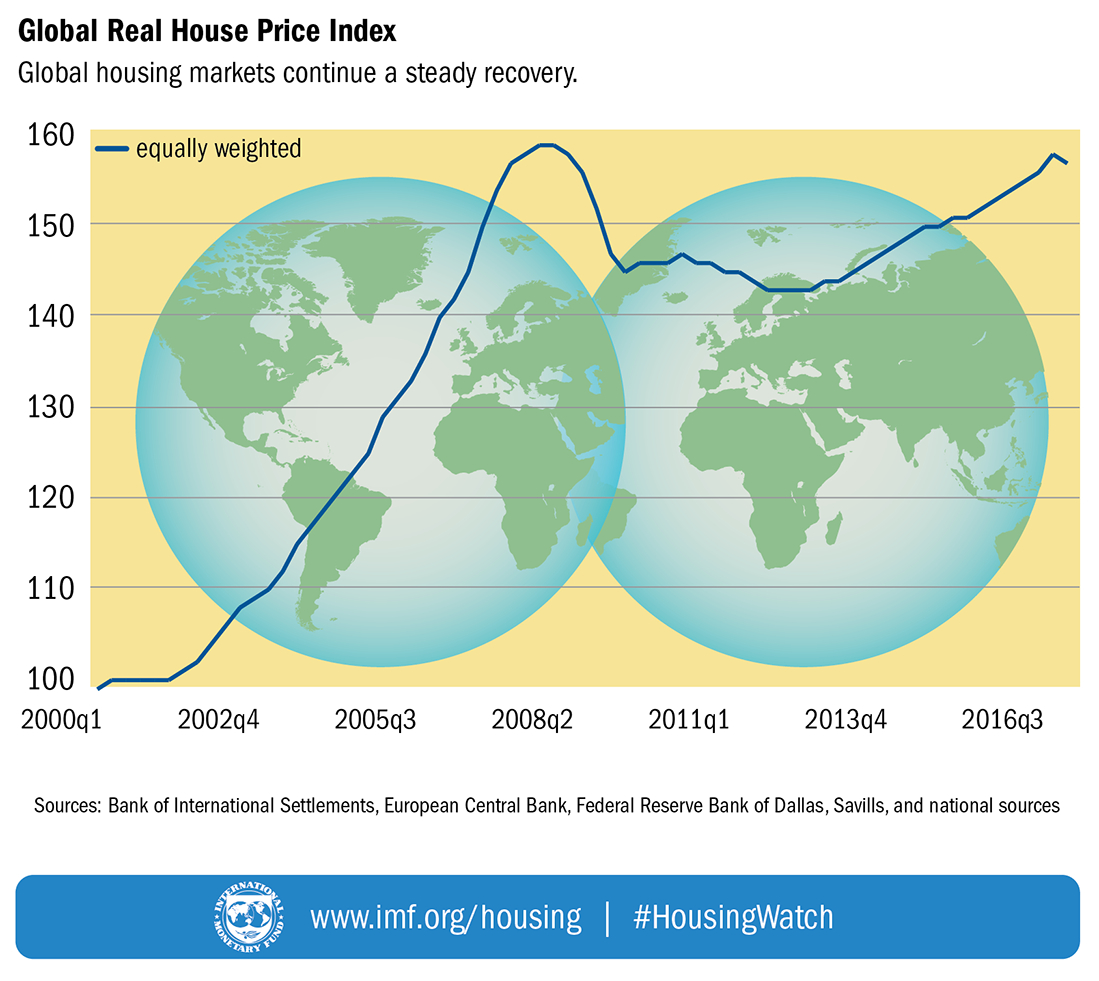

At the global level house prices have not taken out their pre-crisis highs, as this chart from the IMF reveals:-

Source: IMF, BIS, ECB, Federal Reserve, Savills

The latest IMF – Global Housing Watch – report for Q2 2017 is sanguine. They take comfort from the broad range of macroprudential measures which have been introduced during the past decade.

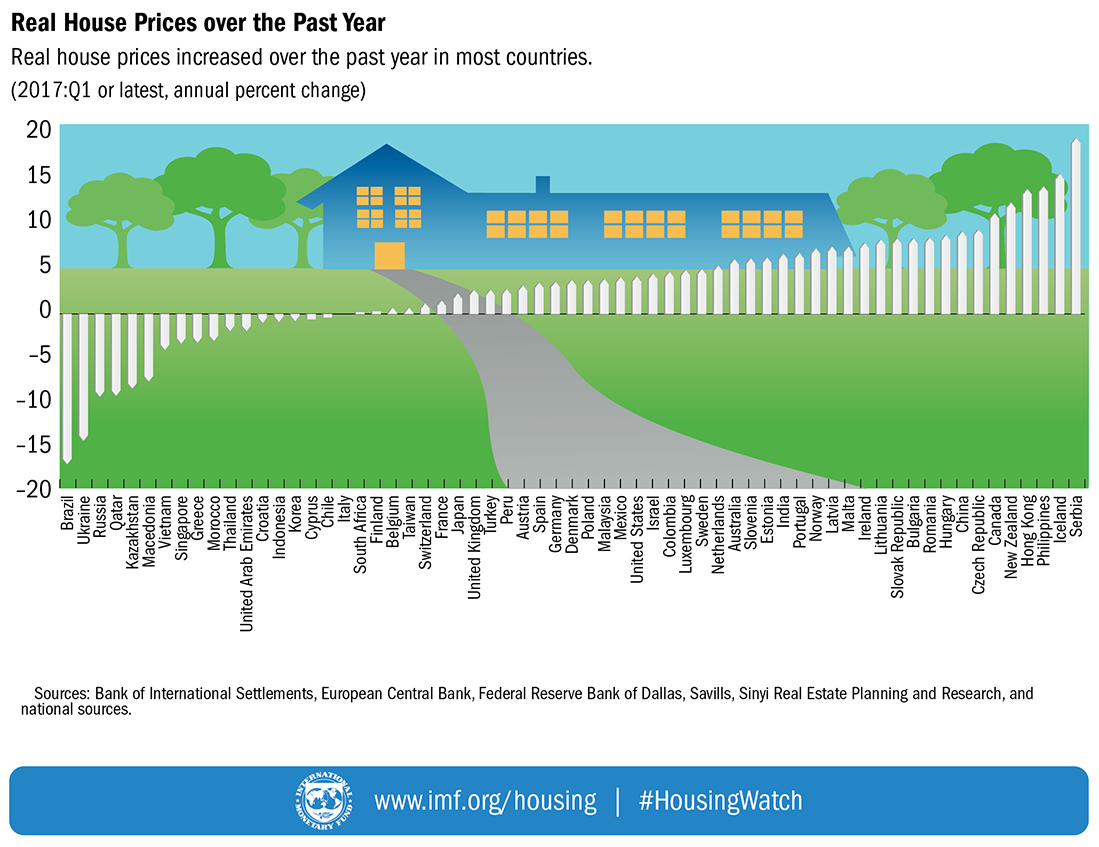

The IMF go on to examine house price increases on a country by country basis:-

Source: IMF, BIS, ECB, Federal Reserve, Savills, Sinyl Real Estate

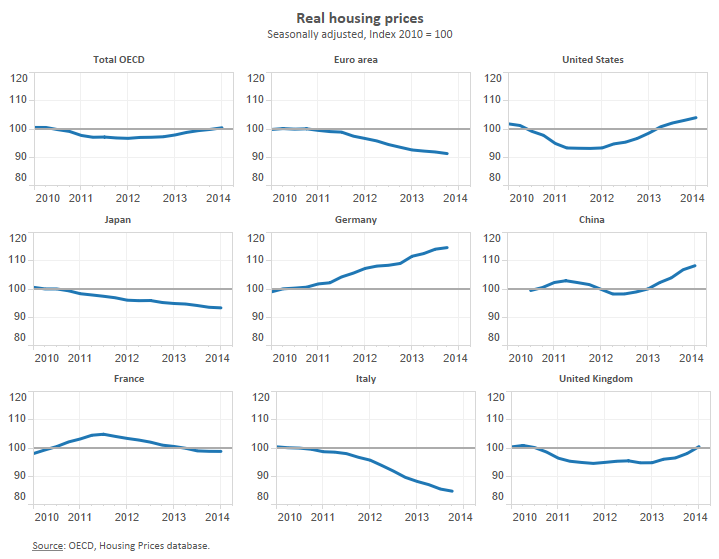

The OECD – Focus on house prices – looks at a variety of different metrics including changes in real house prices: the OECD average is more of less where it was in 2010 having dipped during 2011/2012 – here is breakdown across a selection of regions. Please note the charts are rather historic they stop at January 2014:-

Source: OECD

The continued fall in Japanese prices is not entirely surprising but the steady decline of the Euro area is significant.

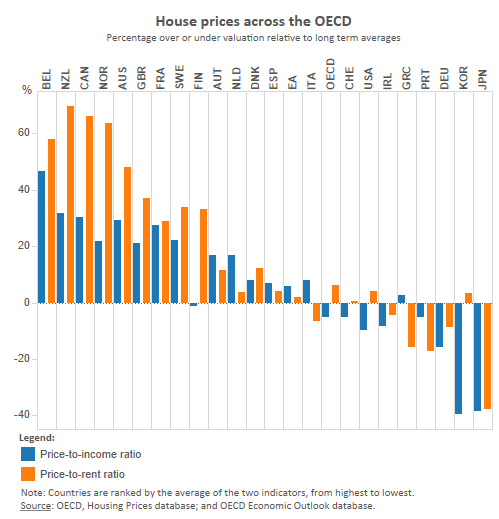

Similarly historic data is contained in the chart below which ranks countries by Price to Income and Price to Rent. Portugal, Germany, South Korea and Japan remain inexpensive by these measures, whilst Belgium, New Zealand, Canada, Norway and Australia remain expensive. The UK market also appears inflated but the decline in Sterling may be a supportive factor: international capital is flowing into the UK after the devaluation:-

Source: OECD

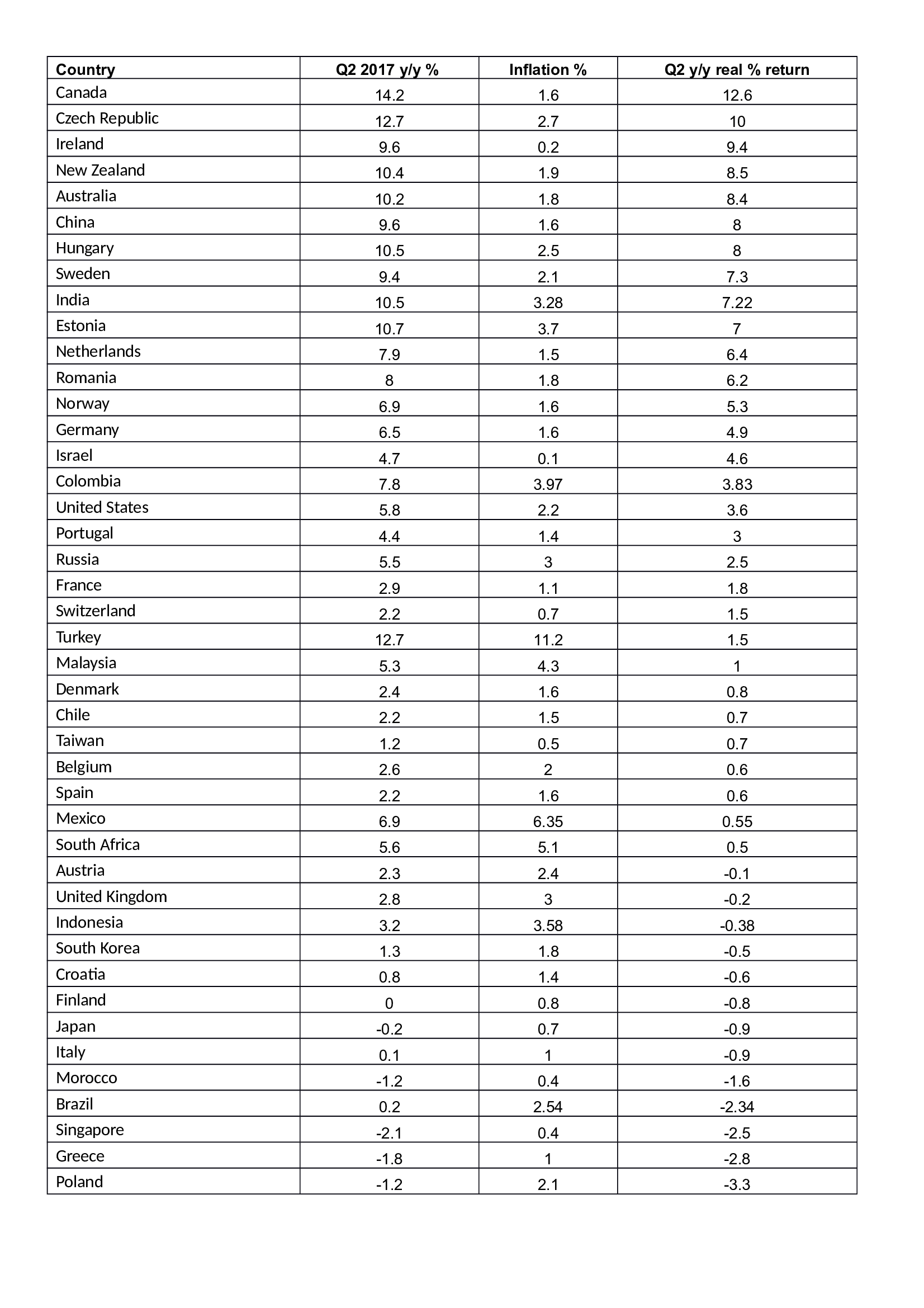

Bringing the data up to date is the Knight Frank’s global house price index, for Q2 2017. The table below is sorted by real return:-

Source: Knight Frank, Trading Economics

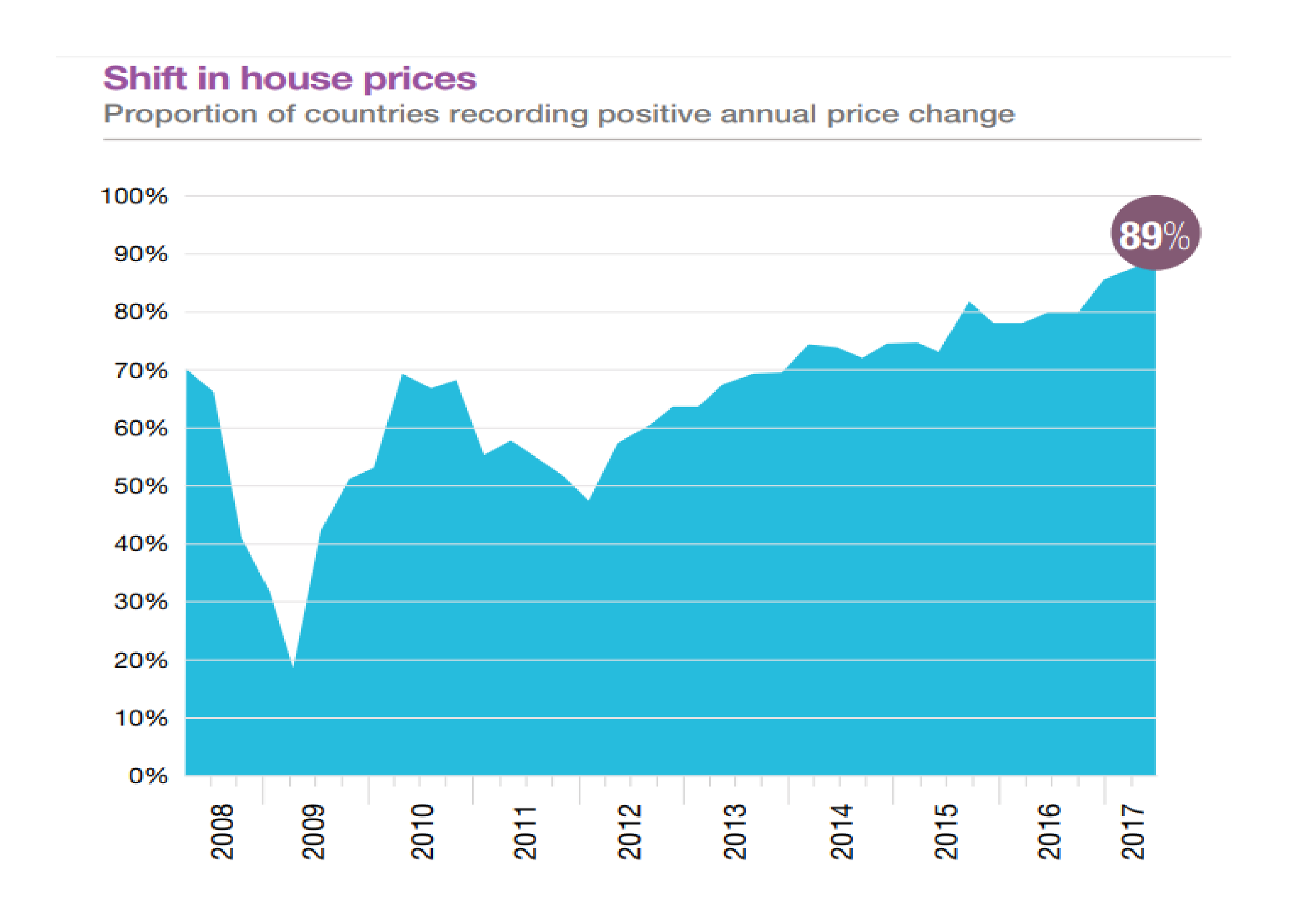

There is a saying in the real estate market, ‘all property is local’. Prices vary from region to region, from street to street, however, the data above paints a picture of a global real estate market which has performed strongly in response to the lowering of interest rates. As the table below illustrates, the percentage of countries recording positive annual price changes is now at 89%, well above the levels of 2007, when interest rates were higher:-

Source: Knight Frank

The low interest rate environment has stimulated a rise in household debt, especially in advanced economies. The IMF – Global Financial Stability Report October 2017 makes sombre reading:-

Although finance is generally believed to contribute to long-term economic growth, recent studies have shown that the growth benefits start declining when aggregate leverage is high. At business cycle frequencies, new empirical studies—as well as the recent experience from the global financial crisis—have shown that increases in private sector credit, including household debt, may raise the likelihood of a financial crisis and could lead to lower growth.

These two charts show the rising trend globally but the relatively undemanding levels of indebtedness typical of the Emerging Market countries:-

Source: IMF

Source: IMF

As long ago at February 2015 – McKinsey – Debt and (not too much) deleveraging – sounded the warning knell:-

Seven years after the bursting of a global credit bubble resulted in the worst financial crisis since the Great Depression, debt continues to grow. In fact, rather than reducing indebtedness, or deleveraging, all major economies today have higher levels of borrowing relative to GDP than they did in 2007. Global debt in these years has grown by $57 trillion, raising the ratio of debt to GDP by 17 percentage points.

According to the Institute of International Finance Q2 2017 global debt report – debt hit a new all-time high of $217 trln (327% of global GDP) with China leading the way:-

Source: IIF

Household debt is growing in China but from a relatively low base, it is as the IMF observe, the advanced economies where households are becoming addicted to low interest rates and cheap finance.

Conclusions and investment opportunities

Source: The Economist

The chart above shows a few of the winners since 1980. The real estate market remains sanguine, trusting that the end of QE will be a gradual process. Although as a recent article by Frank Shostak – Can gradual interest rate tightening prevent shocks? reminds us, ‘…there is no such thing as “shock-free” monetary policy’:-

Can a gradual tightening prevent an economic bust?

Since monetary growth, whether expected or unexpected, gives rise to the redirection of real savings it means that any monetary tightening slows down this redirection. Various economic activities, which sprang-up on the back of strong monetary pumping, because of a tighter monetary stance get now less real funding. This in turn means that these activities are given less support and run the risk of being liquidated. It is the liquidation of these activities what an economic bust is all about.

Obviously, then, the tighter monetary stance by the Fed must put pressure on various false activities, or various artificial forms of life. Hence, the tighter the Fed gets the slower the pace of redirection of real savings will be, which in turn means that more liquidation of various false activities will take place. In the words of Ludwig von Mises,

‘The boom brought about by the banks’ policy of extending credit must necessarily end sooner or later. Unless they are willing to let their policy completely destroy the monetary and credit system, the banks themselves must cut it short before the catastrophe occurs. The longer the period of credit expansion and the longer the banks delay in changing their policy, the worse will be the consequences of the malinvestments and of the inordinate speculation characterizing the boom; and as a result the longer will be the period of depression and the more uncertain the date of recovery and return to normal economic activity.’

Consequently, the view that the Fed can lift interest rates without any disruption doesn’t hold water. Obviously if the pool of real savings is still expanding then this may mitigate the severity of the bust. However, given the reckless monetary policies of the US central bank it is quite likely that the US economy may already has a stagnant or perhaps a declining pool of real savings. This in turn runs the risk of the US economy falling into a severe economic slump.

We can thus conclude that the popular view that gradual transparent monetary policies will allow the Fed to tighten its stance without any disruptions is based on erroneous ideas. There is no such thing as a “shock-free” monetary policy any more than a monetary expansion can ever be truly neutral to the market.

Regardless of policy transparency once a tighter monetary stance is introduced, it sets in motion an economic bust. The severity of the bust is conditioned by the length and magnitude of the previous loose monetary stance and the state of the pool of real savings.

If world stock markets catch a cold central banks will provide assistance – though not perhaps to the same degree as they did last time around. If, however, the real estate market begins to unravel the impact on consumption – and therefore on the real economy – will be much more dramatic. Central bankers will act in concert and with determination. If the problem is malinvestment due to artificially low interest rates, then further QE and a return to the zero bound will not cure the malady: but this discussion is for another time.

What does quantitative tightening – QT – mean for real estate? In many urban areas, the increasing price of real estate is a function of geography and the limitations of infrastructure. Shortages of supply are difficult (and in some cases impossible) to alleviate; it is unlikely, for example, that planning consent would be granted to develop Central Park in Manhattan or Hyde Park in London.

Higher interest rates and weakness in household earnings growth will temper the rise in property prices. If the markets run scared it may even lead to a brief correction. More likely, transactional activity will diminish. A price collapse to the degree we witnessed in 2008/2009 is unlikely to recur. Those markets which have risen most may exhibit a greater propensity to decline, but the combination of steady long term demand and supply constraints, will, if you’ll pardon the pun, underpin global real estate.

Macro Letter – No 79 – 16-6-2017

Central Bank balance sheet adjustment – a path to enlightenment?

The Federal Reserve (Fed) is about to embark on a reversal of the Quantitative Easing (QE) which it first began in November 2008. Here is the 14th June Federal Reserve Press Release – FOMC issues addendum to the Policy Normalization Principles and Plans. This is the important part:-

For payments of principal that the Federal Reserve receives from maturing Treasury securities, the Committee anticipates that the cap will be $6 billion per month initially and will increase in steps of $6 billion at three-month intervals over 12 months until it reaches $30 billion per month.

For payments of principal that the Federal Reserve receives from its holdings of agency debt and mortgage-backed securities, the Committee anticipates that the cap will be $4 billion per month initially and will increase in steps of $4 billion at three-month intervals over 12 months until it reaches $20 billion per month.

The Committee also anticipates that the caps will remain in place once they reach their respective maximums so that the Federal Reserve’s securities holdings will continue to decline in a gradual and predictable manner until the Committee judges that the Federal Reserve is holding no more securities than necessary to implement monetary policy efficiently and effectively.

On the basis of their press release, the Fed balance sheet will shrink until it is nearer $2.5trln versus $4.4trln today. If they stick to their schedule that should take until the end of 2021.

The Fed is likely to be followed by the other major Central Banks (CBs) in due course. Their combined deleveraging is unlikely to go unnoticed in financial markets. What are the likely implications for bonds and stocks?

To begin here are a series of charts which tell the story of the Central Bankers’ response to the Great Recession:-

Source: Yardeni Research, Haver Analytics

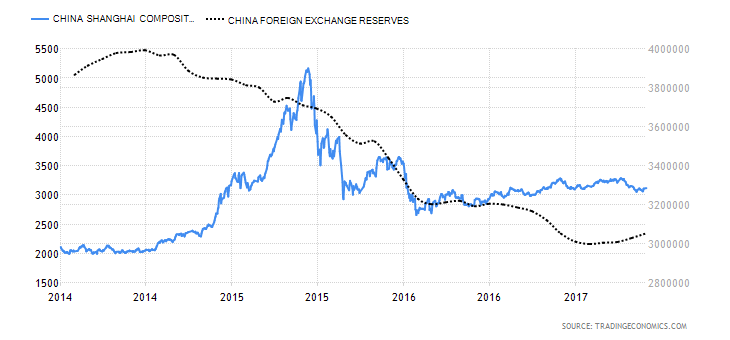

Since 2008 the balance sheets of the four major CBs have grown from around $6.5trln to $18.4trln. In the case of the People’s Bank of China (PBoC), a reduction began in 2015. This took the form of a decline in its foreign exchange reserves in order to support the weakening RMB exchange rate against the US$. The next chart shows the path of Chinese FX reserves and the Shanghai Stock index since the beginning of 2014. Lagged response or coincidence? Your call:-

Source: Trading Economics

At a global level, the PBoC balance sheet reduction has been more than offset by the expansion of the balance sheets of the Bank of Japan (BoJ) and European Central Bank (ECB), however, a synchronous balance sheet contraction by all the major CBs is likely to be of considerable concern to financial market participants globally.

An historical perspective

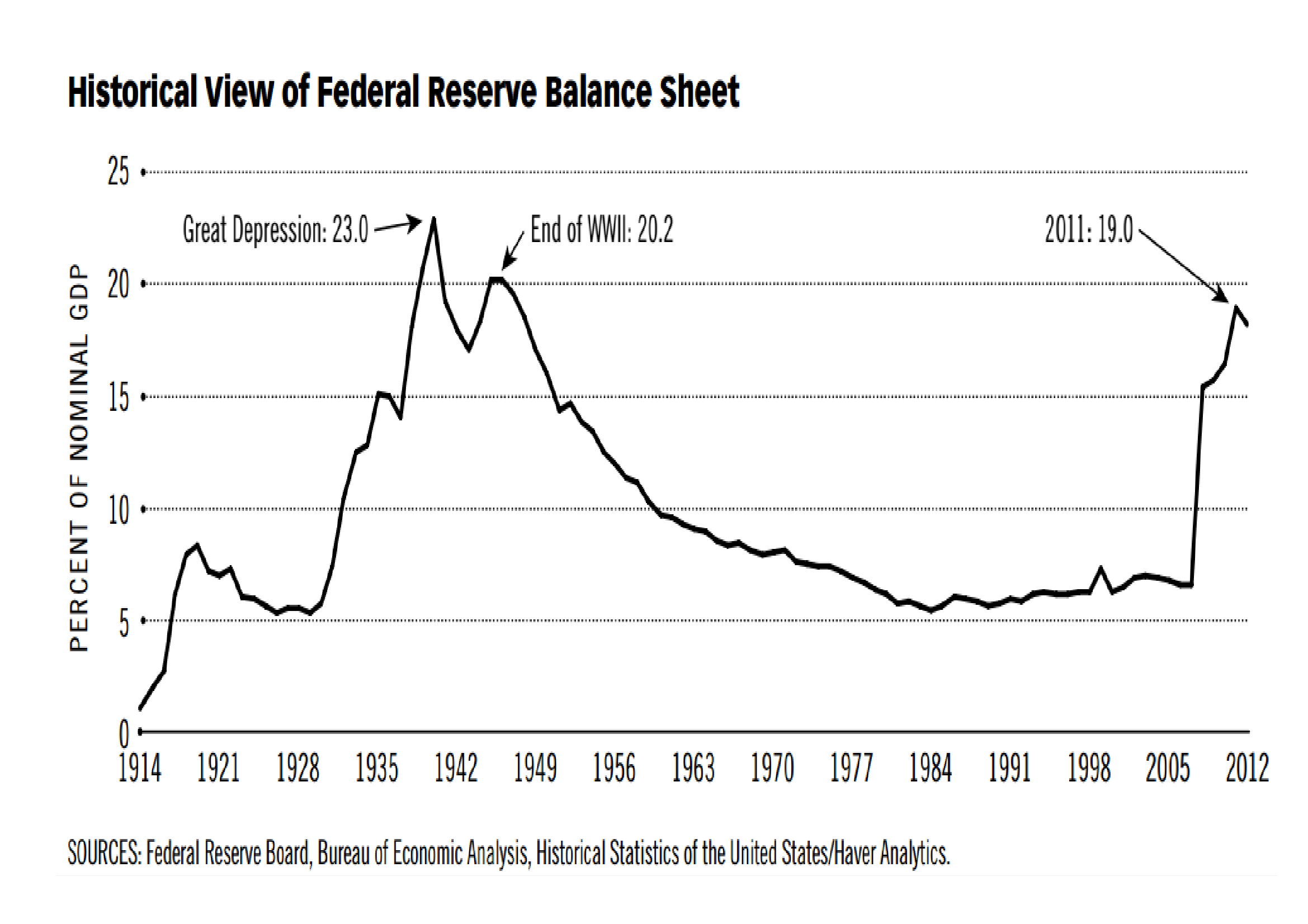

Have CB balance sheets ever been as large as they are today? Indeed they have. The chart below which terminates in 2011, shows the evolution of the Fed balance sheet since its inception in 1913:-

Source: Federal Reserve, Haver Analytics

The increase in the size of the Fed balance sheet during the period of the Great Depression and WWII was related to a number of factors including: gold inflows, what Friedman and Schwartz termed “precautionary demand” for reserves by commercial banks, lack of alternative assets, changes in reserve requirements, expansion of income and war financing.

For a detailed review of all these factors, this paper from 2016 – How was the Quantitative Easing Program of the 1930s Unwound? By Matthew Jaremski and Gabriel Mathy – makes fascinating reading, here’s the abstract:-

Outside of the recent past, excess reserves have only concerned policymakers in one other period: The Great Depression of the 1930s. This historical episode thus provides the only guidance about the Fed’s current predicament of how to unwind from the extensive Quantitative Easing program. Excess reserves in the 1930s were never actively unwound through a reduction in the monetary base. Nominal economic growth swelled required reserves while an exogenous reduction in monetary gold inflows due to war embargoes in Europe allowed banks to naturally reduce their excess reserves. Excess reserves fell rapidly in 1941 and would have unwound fully even without the entry of the United States into World War II. As such, policy tightening was at no point necessary and likely was even responsible for the 1937-1938 recession.

During the period from April 1937 to April 1938 the Dow Jones Industrial Average fell from 194 to 100. Monetarists, such as Friedman, blamed the recession on a tightening of money supply in 1936 and 1937. I don’t believe Friedman’s censure is lost on the FOMC today: past Fed Chair, Ben Bernanke, is regarded as one of the world’s leading authorities on the causes and policy errors of the Great Depression.

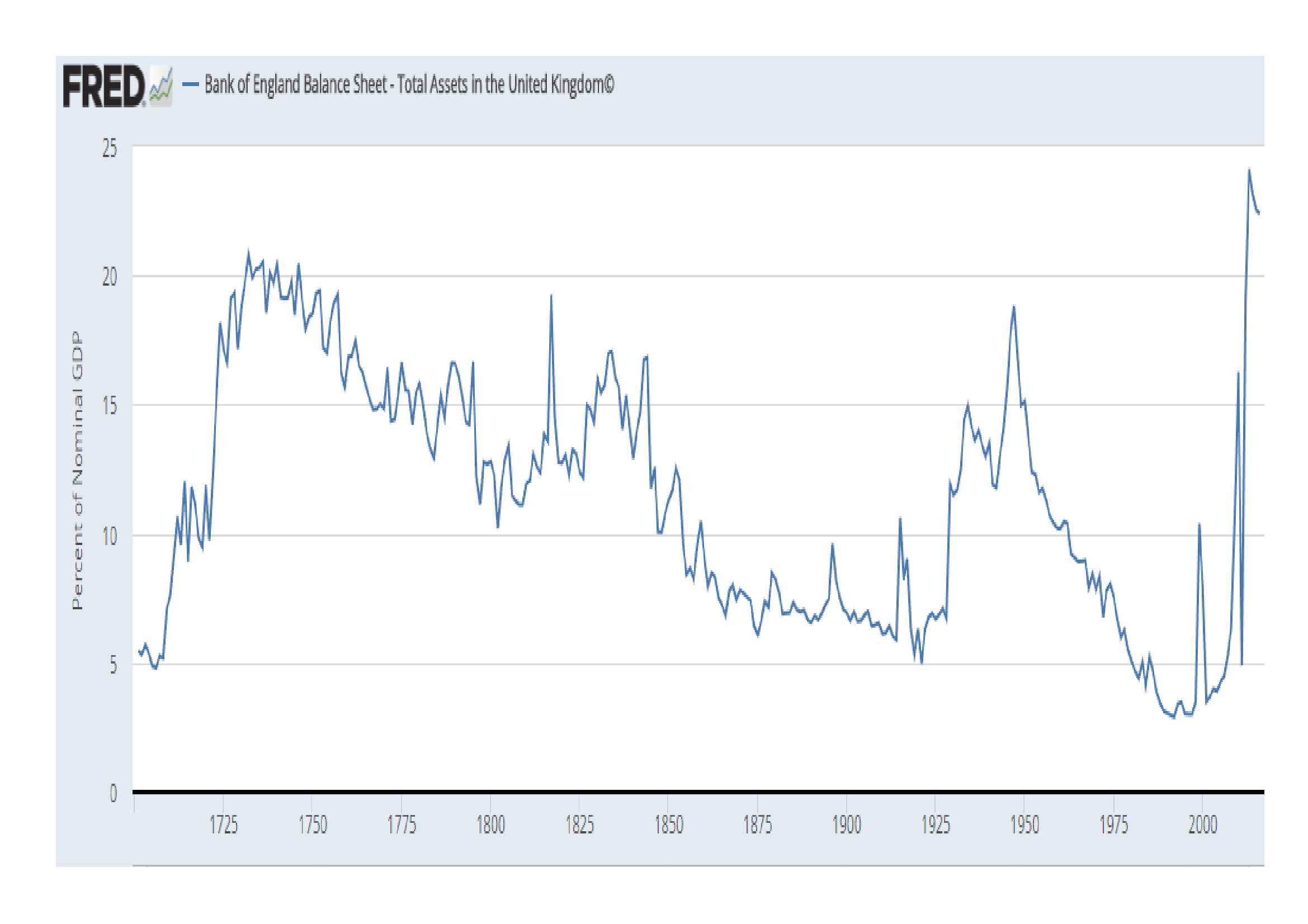

But is the size of a CB balance sheet a determinant of the direction of the stock market? A richer data set is to be found care of the Bank of England (BoE). They provide balance sheet data going back to 1694, although the chart below, care of FRED, starts in 1701:-

Source: Federal Reserve, Bank of England

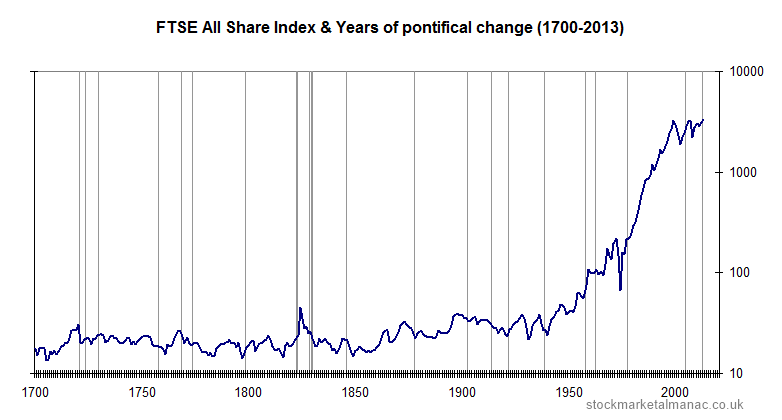

The BoE really only became a CB, in the sense we might recognise today, as a result of the Banking Act of 1844 which granted it a monopoly on the issuance of bank notes. The chart below shows the performance of the FT-All Share Index since 1700 (please ignore the reference to the Pontifical change, this was the only chart, offering a sufficiently long history, which I was able to discover in the public domain):-

Source: The Stock Almanac

The first crisis to test the Bank’s resolve was the panic of 1857. During this period the UK stock market barely changed whilst the BoE balance sheet expanded by 21% between 1857 and 1859 to reach 10.5% of GDP: one might, however, argue that its actions were supportive.

The next crisis, the recession of 1867, was precipitated by the end of the American Civil War and, of more importance to the financial system, the demise of Overund and Gurney, “the Bankers Bank”, which was declared insolvent in 1866. Perhaps surprisingly, the stock market remained relatively calm and the BoE balance sheet expanded at a more modest 20% over the two years to 1858.

Financial markets became a little more interconnected during the Panic of 1873. This commenced with the “Gründerzeit” or “Founders” crash on the Vienna Stock Exchange. It sent shockwaves around the world. The UK stock market declined by 31% between 1873 and 1878. The BoE may have exacerbated the decline, its balance sheet contracted by 14% between 1873 and 1875. Thereafter the trend reversed, with an expansion of 30% over the next four years.

I am doubtful about the BoE balance sheet contraction between 1873 and 1875 being a policy mistake. 1873 was in fact the beginning of the period known as the Long Depression. It lasted until 1896. Nine years before the end of this 20 year depression the stock market bottomed (1887). It then rose by 74% over the next 11 years.

The First World War saw the stock market decline, reaching its low in 1917. From juncture it rallied, entirely ignoring the post-war recession of 1919 to 1921. Its momentum was only curtailed by the Great Crash of 1929 and subsequent Great Depression of 1930-1931.

Part of the blame for the severity of the Great Depression may be levelled at the BoE, its balance sheet expanded by 77% between 1928 and 1929. It then remained relatively stable despite Sterling’s departure from the Gold Standard in 1931 and only began to expand again in 1933 and 1934. Its balance sheet as a percentage of GDP was by this time at its highest since 1844, due to the decline in GDP rather than any determined effort to expand the balance sheet on the part of the Old Lady of Threadneedle Street. At the end of 1929 its balance sheet stood at £537mln, by the end of 1934 it had reached £630mln, an increase of just 17% over five traumatic years. The UK stock market, which had bottomed in 1931 – the level it had last traded in 1867 – proceeded to rally for the next five years.

Adjustment without tightening

History, on the basis of the data above, is ambivalent about the impact the size of a CB’s balance sheet has on the financial markets. It is but one of the factors which influences monetary conditions, the others are the availability of credit and its price.

George Selgin described the Fed’s situation clearly in a post earlier this year for The Cato Institute – On Shrinking the Fed’s Balance Sheet. He begins by looking at the Fed pre-2008:-

…the Fed got by with what now seems like a modest-sized balance sheet, the liabilities of which consisted mainly of circulating Federal Reserve notes, supplemented by Treasury and GSE deposit balances and by bank reserve balances only slightly greater than the small amounts needed to meet banks’ legal reserve requirements. Because banks held few excess reserves, it took only modest adjustments to the size of the Fed’s balance sheet, achieved by means of open-market purchases or sales of short-term Treasury securities, to make credit more or less scarce, and thereby achieve the Fed’s immediate policy objectives. Specifically, by altering the supply of bank reserves, the Fed could influence the federal funds rate — the rate banks paid other banks to borrow reserves overnight — and so keep that rate on target.

Then comes the era of QE – the sea-change into something rich and strange. The purchase of long-term Treasuries and Mortgage Backed Securities is funded using the excess reserves of the commercial banks which are held with the Fed. As Selgin points out this means the Fed can no longer use the federal funds rate to influence short-term interest rates (the emphasis is mine):-

So how does the Fed control credit now? Instead of increasing or reducing the availability of credit by adding to or subtracting from the supply of Fed deposit balances, the Fed now loosens or tightens credit by controlling financial institutions’ demand for such balances using a pair of new monetary control devices. By paying interest on excess reserves (IOER), the Fed rewards banks for keeping balances beyond what they need to meet their legal requirements; and by making overnight reverse repurchase agreements (ON-RRP) with various GSEs and money-market funds, it gets those institutions to lend funds to it.

Between them the IOER rate and the implicit ON-RRP rate define the upper and lower limits, respectively, of an effective federal funds rate target “range,” because most of the limited trading that now goes on in the federal funds market consists of overnight lending by GSEs (and the Federal Home Loan Banks especially), which are not eligible for IOER, to ordinary banks, which are. By raising its administered rates, the Fed encourages other financial institutions to maintain larger balances with it, instead of trading those balances for other interest-earning assets. Monetary tightening thus takes the form of a reduced money multiplier, rather than a reduced monetary base.

Selgin goes on to describe this as Confiscatory Credit Control:-

…Because instead of limiting the overall availability of credit like it did in the past, the Fed now limits the credit available to other prospective borrowers by grabbing more for itself, which it then passes on to the U.S. Treasury and to housing agencies whose securities it purchases.

The good news is that the Fed can adjust its balance sheet with relative ease (emphasis mine):-

It’s only because the Fed has been paying IOER at rates exceeding those on many Treasury securities, and on short-term Treasury securities especially, that banks (especially large domestic and foreign banks) have chosen to hoard reserves. Even today, despite rate increases, the IOER rate of 75 basis points exceeds yields on most Treasury bills. Were it not for this difference, banks would trade their excess reserves for Treasury securities, causing unwanted Fed balances to be passed around like so many hot-potatoes, and creating new bank deposits in the process. Because more deposits means more required reserves, banks would eventually have no excess reserves to dispose of.

Phasing out ON-RRP, on the other hand, would eliminate the artificial boost that program has been giving to non-bank financial institutions’ demand for Fed balances.

Because phasing out ON-RRP makes more reserves available to banks, while reducing IOER rates reduces banks’ own demand for such reserves, both policies are expansionary. They don’t alter the total supply of Fed balances. Instead they serve to raise the money multiplier by adding to banks’ capacity and willingness to expand their own balance sheets by acquiring non-reserve assets. But this expansionary result is a feature, not a bug: as former Fed Vice Chairman Alan Blinder observed in December 2013, the greater the money multiplier, the more the Fed can shrink its balance sheet without over-tightening. In principle, so long as it sells enough securities, the Fed can reduce its ON-RRP and IOER rates, relative to prevailing market rates, without missing its ultimate policy targets.

Selgin expands, suggesting that if the Fed decide to announce a fixed schedule for adjustment (which they have) then they may employ another tool from their armoury, the Term Deposit Facility:-

…to the extent that the Fed’s gradual asset sales fail to adequately compensate for a multiplier revival brought about by its scaling-back of ON-RRP and IOER, the Fed can take up the slack by sufficiently raising the return on its Term Deposits.

And the Fed’s federal funds rate target? What happens to that? In the first place, as the Fed scales back on ON-RRP and IOER, by allowing the rates paid through these arrangements to decline relative to short-term Treasury rates, its administered rates will become increasingly irrelevant. The same changes, together with concurrent assets sales, will make the effective federal funds rate more relevant, by reducing banks’ excess reserves and increasing overnight borrowing. While the changes are ongoing, the Fed would continue to post administered rates; but it could also revive its pre-crisis practice of announcing a single-valued effective funds rate target. In time, the latter target could once again be more-or-less precisely met, making it unnecessary for the Fed to continue referring to any target range.

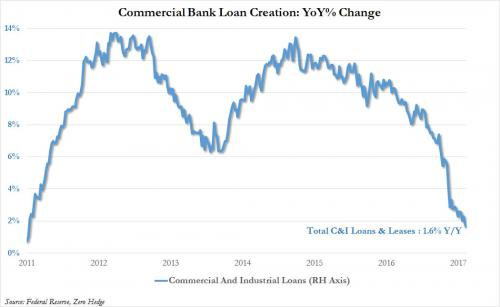

With unemployment falling and economic growth steady the Fed are expected to tighten monetary policy further but the balance sheet adjustment needs to be handled carefully, conditions may look benign but the Fed ultimately holds more of the nation’s deposits than at any time since the end of WWII. Bank lending (last at 1.6%) is anaemic at best, as the chart below makes clear:-

Source: Federal Reserve, Zero Hedge

The global perspective

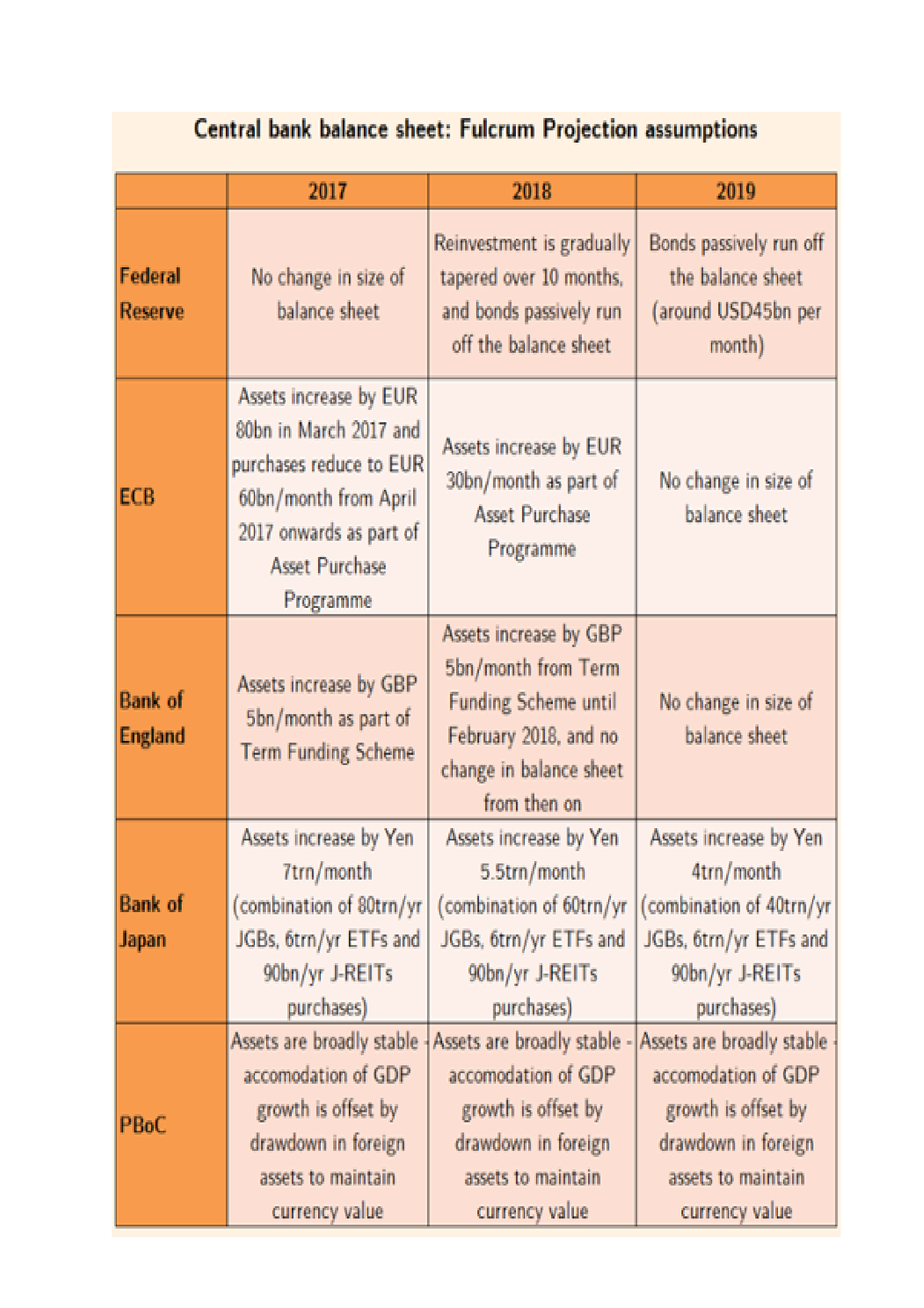

The implications of balance sheet adjustment for the US have been discussed in detail but what about the rest of the world? In an FT Article – The end of global QE is fast approaching – Gavyn Davies of Fulcrum Asset Management makes some projections. He sees global QE reaching a plateau next year and then beginning to recede, his estimate for the Fed adjustment is slightly lower than the schedule announced last Wednesday:-

Source: FT, Fulcrum Asset Management

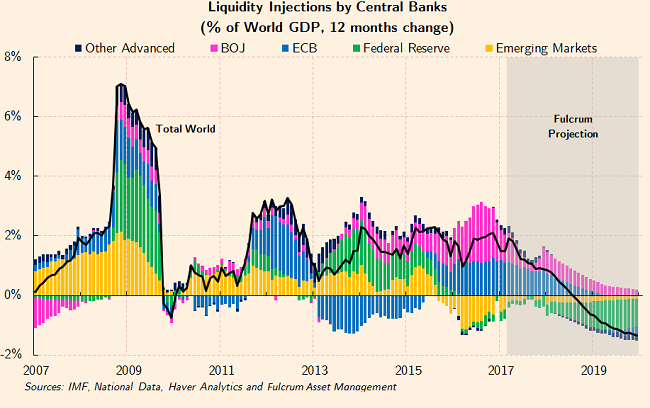

He then looks at the previous liquidity injections relative to GDP – don’t forget 2009 saw the world growth decline by -0.8%:-

Source: IMF, National Data, Haver Analytics, Fulcrum Asset Management

It is worth noting that the contraction of Emerging Market CB liquidity during 2016 was principally due to the PBoc reducing their foreign exchange reserves. The ECB reduction of 2013 – 2015 looks like a policy mistake which they are now at pains to rectify.

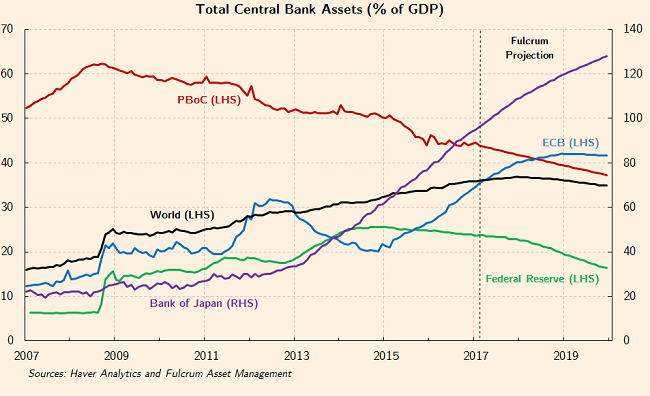

Finally Davies looks at the breakdown by institution. The BoJ continues to expand its balance sheet, rising above 100% of GDP, whilst eventually the ECB begins to adjust as it breaches 40%:-

Source: Haver Analytics, Fulcrum Asset Management

I am not as confident as Davies about the ECB’s ability to reverse QE. They were never able to implement a European equivalent of the US Emergency Economic Stabilization Act of 2008, which incorporated the Troubled Asset Relief Program – TARP and the bailout of Fannie Mae and Freddie Mac. Europe’s banking system remains inherently fragile.

ProPublica – Bailout Costs – gives a breakdown of cost of the US bailout. The policies have proved reasonable successful and at little cost the US tax payer. Since initiation in 2008 outflows have totalled $623.4bln whilst the inflows amount to $708.4bln: a net profit to the US government of $84.9bln. Of course, with $455bln of troubled assets still outstanding, there is still room for disappointment.

The effect of TARP was to unencumber commercial banks. Freed of their NPL’s they were able to provide new credit to the real economy once more. European banks remain saddled with an abundance of NPL’s; her governments have been unable to agree on a path to enlightenment.

Conclusions and Investment Opportunities

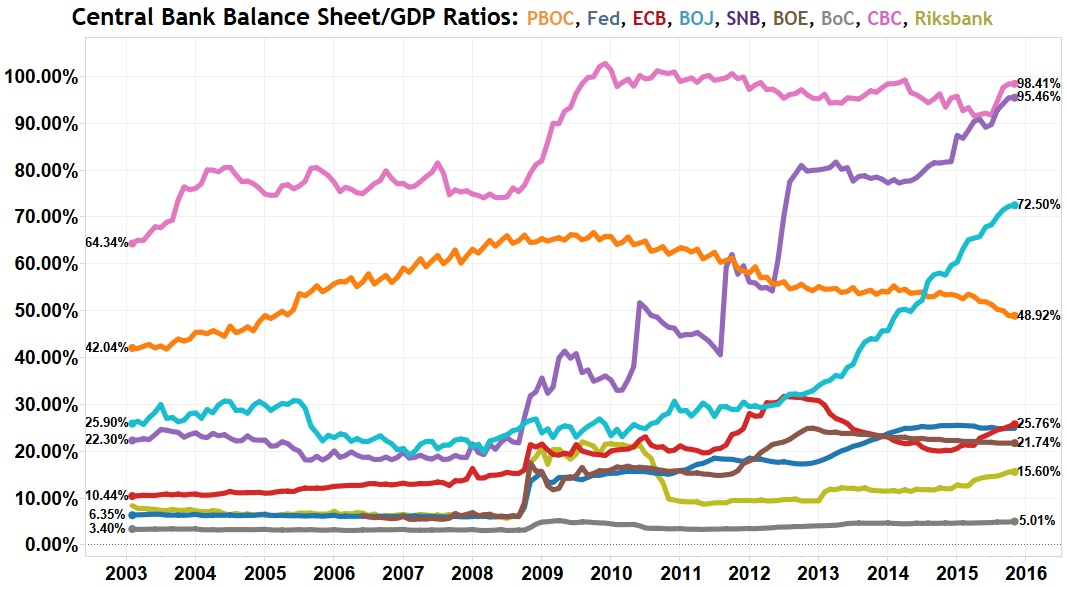

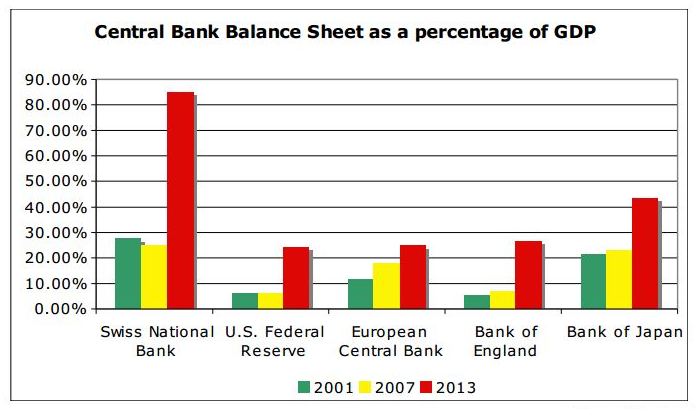

The chart below shows a selection of CB balance sheets as a percentage of GDP. It is up to the end of 2016:-

SNB: Swiss National Bank, BoC: Bank of Canada, CBC: Central Bank of Taiwan, Riksbank: Swedish National Bank

Source: National Inflation Association

The BoJ has since then expanded its balance sheet to 95.5% and the ECB, to 32%. With the Chinese economy still expanding (6.9% March 2017) the PBoC has seen its ratio fall to 45.4%.

More important than the sheer scale of CB balance sheets, the global expansion has changed the way the world economy works. Combined CB balance sheets ($22trln) equal 21.5% of global GDP ($102.4trln). The assets held are predominantly government and agency bonds. The capital raised by these governments is then invested primarily in the public sector. The private sector has been progressively crowded out of the world economy ever since 2008.

In some ways this crowding out of the private sector is similar to the impact of the New Deal era of 1930’s America. The private sector needs to regain pre-eminence but the transition is likely to be slow and uneven. The tide may be about to turn but the chance for policy mistakes, as flows reverse, is extremely high.

For stock markets the transition to QT – quantitative tightening – may be neutral but the risks are on the downside. For government bond markets there are similar concerns: who will buy the bonds the CBs need to sell? If interest rates normalise will governments be forced to tighten their belts? Will the private sector be in a position to fill the vacuum created by reduced public spending, if they do?

There is an additional risk. Yield curve flattening. Banks borrow short and lend long. When yield curves are positively sloped they can quickly recapitalise their balance sheets: when yield curves are flat, or worse still inverted, they cannot. Increases in reserve requirements have made government bonds much more attractive to hold than other securities or loans. The Commercial Bank Loan Creation chart above may be seen as a warning signal. The mechanism by which CBs foster credit expansion in the real economy is still broken. A tapering or an adjustment of CB balance sheets, combined with a tightening of monetary policy, may have profound unintended consequences which will be magnified by a severe shakeout in over-extended stock and bond markets. Caveat emptor.

Macro Letter – No 65 – 11-11-2016

Yield Curve Control – the road to infinite QE

Zero Yield 10 year

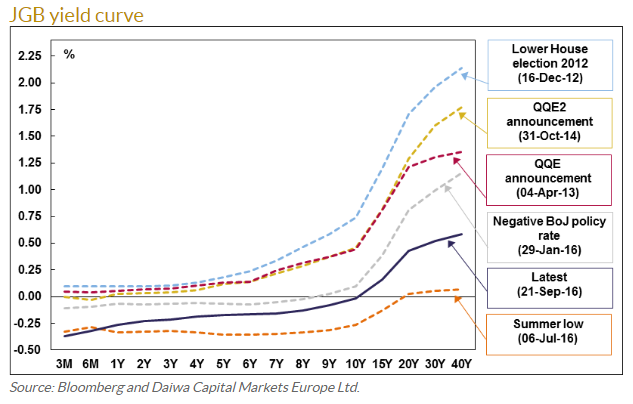

Ever since central banks embarked on quantitative easing (QE) they were effectively taking control of their domestic government yield curves. Of course this was de facto. Now, in Japan, it has finally been declared de jure since the Bank of Japan (BoJ) announced the (not so) new policy of “Yield Curve Control”. New Framework for Strengthening Monetary Easing: “Quantitative and Qualitative Monetary Easing with Yield Curve Control”, published on 21st September, is a tacit admission that BoJ intervention in the Japanese Government Bond market (JGB) is effectively unlimited. This is how they described it (the emphasis is mine):-

The Bank will purchase Japanese government bonds (JGBs) so that 10-year JGB yields will remain more or less at the current level (around zero percent). With regard to the amount of JGBs to be purchased, the Bank will conduct purchases more or less in line with the current pace — an annual pace of increase in the amount outstanding of its JGB holdings at about 80 trillion yen — aiming to achieve the target level of a long-term interest rate specified by the guideline. JGBs with a wide range of maturities will continue to be eligible for purchase…

By the end of September 2016 the BoJ owned JPY 340.9trln (39.9%) of outstanding JGB issuance – they cannot claim to conduct purchases “more of less in line with the current pace” and maintain a target 10 year yield. Either they will fail to maintain the 10 year yield target in order to maintain their purchase target of JPY 80trln/annum or they will forsake their purchase target in order to maintain the 10 year yield target. Either they are admitting that the current policy of the BoJ (and other central banks which have embraced quantitative easing) is a limited form of “Yield Curve Control” or they are announcing a sea-change to an environment where the target yield will take precedence. If it is to be the latter, infinite QE is implied even if it is not stated for the record.

Zero Coupon Perpetuals

I believe the 21st September announcement is a sea-change. My concern is how the BoJ can ever hope to unwind the QE. One suggestion coming from commentators but definitely not from the BoJ, which gained credence in April – and again, after Ben Bernanke’s visit to Tokyo in July – is that the Japanese government should issue Zero Coupon Perpetual bonds. Zero-coupon bonds are not a joke – 28th August – by Edward Chancellor discusses the subject:-

Bernanke’s latest bright idea is that the Bank of Japan, which has bought up close to half the country’s outstanding government debt, should convert its bond holdings into zero-coupon perpetual securities – that is, financial instruments with no intrinsic value.