Macro Letter – No 69 – 27-01-2017

The Risks and Rewards of Asian Real Estate

- Shanghai house prices increased 26.5% in 2016

- International investment in Asian Real Estate is forecast to grow 64% by 2020

- Chinese and Indian Real Estate has underperformed US stocks since 2009

- Economic and demographic growth is supportive Real Estate in several Asian countries

Donald Trump may have torn up the Trans-Pacific Partnership trade agreement, but the economic fortunes of Asia are unlikely to be severely dented. This week Blackstone Group – which at $102bln AUM is one of the largest Real Estate investors in the world – announced that they intend to raise $5bln for a second Asian Real Estate fund. Their first $5bln fund – Blackstone Real Estate Partners (BREP) Asia – which launched in 2014, is now 70% invested and generated a 17% return through September 2016. Blackstone’s new vehicle is expected to invest over the next 12 to 18 months across assets such as warehouses and shopping malls in China, India, South-East Asia and Australia.

Last year 22 Asia-focused property funds raised a total of $10.6bln. Recent research by Preqin estimates that $33bln of cash is currently waiting to be allocated by existing Real Estate managers.

Blackrock, which has $21bln in Real Estate assets, predicts the amount invested in Real Estate assets will grow by 75% in the five years to 2020. In their March 2016 Global Real Estate Review they estimated that Global REITs returned 10% over five years, 6% over 10 years and 11% over 15 years.

This year – following the lead of countries such as Australia, Japan and Singapore – India is due to introduce Real Estate Investment Trusts (REITs) they also plan to permit infrastructure investment trusts (InvITs). Other Asian markets have introduced REITs but not many have been successful in achieving adequate liquidity. India, however, has the seventh highest home ownership rate in the world (86.6%) which bodes well for potential REIT investment demand.

UK asset manager M&G, make an excellent case for Asian Real Estate, emphasis mine:-

Exposure to a diversified and maturing region which accounts for a third of the world’s economic output and offers a sustainable growth premium over the US and Europe.

Diversification benefits. An allocation to Asian real estate boosts risk-adjusted returns as part of a global property portfolio; plus there are diverse opportunities within Asia itself.

Defensive characteristics, with underlying occupier demand supported by robust economic fundamentals, as showcased by Asia’s resilience during the European and US downturns of the recent financial crisis.

What M&G omit to mention is that investing in Real Estate is unlike investing in stocks (Companies can change and evolve) or Bonds which exhibit significant homogeneity – Real Estate might be termed the ultimate Fixed Asset – Location is a critical part of any investment decision. Mark Twain may have said, “Buy land. They’re not making it anymore.” but unless the land has commercial utility it is technically worthless.

The most developed regions of Asia, such as Singapore, Hong Kong, Japan and Australia, offer similar transparency to North America and Europe. They will also benefit from the growth of emerging Asian economies together with the expansion of their own domestic middle-income population. However, some of these markets, such as China, have witnessed multi-year price increases. Where is the long-term value and how great is the risk of contagion, should the US and Europe suffer another economic crisis?

In 2013 the IMF estimated that the Asia-Pacific Region accounted for approximately 30% of global GDP, by this juncture the region’s Real Estate assets had reached $4.2trln, nearly one third of the global total. During the past decade the average GDP growth of the region has been 7.4% – more than twice the rate of the US or Europe.

The problem for investors in Asia-Pacific Real Estate is the heavy weighting, especially for REIT investors, to markets which are more highly correlated to global equity markets. The MSCI AC Asia Pacific Real Estate Index, for example, is a free float-adjusted market capitalization index that consists of large and mid-cap equity across five Developed Markets (Australia, Hong Kong, Japan, New Zealand and Singapore) and eight Emerging Markets (China, India, Indonesia, Korea, Malaysia, the Philippines, Taiwan and Thailand) however, the percentage weighting is heavily skewed to developed markets:-

| Country |

Weight |

| Japan |

32.94% |

| Hong Kong |

26.40% |

| Australia |

19.81% |

| China |

9.62% |

| Singapore |

6.30% |

| Other |

4.93% |

Source: MSCI

Here is how the Index performed relative to the boarder Asia-Pacific Equity Index and ACWI, which is a close proxy for the MSCI World Index:-

Source: MSCI

The MSCI Real-Estate Index has outperformed since 2002 but it is more volatile and yet closely correlated to the Asia-Pacific Equity or the ACWI. The 2008-2009 decline was particularly brutal.

Under what conditions will Real Estate investments perform?

- There are several supply and demand factors which drive Real Estate returns, this list is not exhaustive:-

- Population growth – this may be due to internal demographic trends, such as higher birth rates, a rising working age population, inward migration or urbanisation.

- Geographic constraints – lack of space drives prices higher.

- Planning restrictions – limitations on development and redevelopment drive prices higher.

- Economic growth – this can be at the country level or on a per-capita basis.

- Economic policy – fiscal stimulus, in the form of infrastructure development, drives economic opportunity which in turn drives demand.

- Monetary policy – interest rates – especially real-interest rates – and credit controls, drive demand: although supply may follow.

- Taxation policy – transaction taxes directly impact liquidity – a decline in liquidity is detrimental to prices. Annual duties based on assessable value, directly reduce returns.

- Legal framework – uncertain security of tenure and risk of curtailment or confiscation, reduces demand and prices.

The markets and countries which will offer lasting diversification benefits are those which exhibit strong economic growth and have low existing international investment in their Real Estate markets. The UN predicts that 380mln people will migrate to cities around the world in the next five years – 95mln in China alone. It is these metropoles, in growing economies, which should be the focus of investment. Since 1990, an estimated 470 new cities have been established in Asia, of which 393 were in China and India.

In their January 2017 update, the IMF – World Economic Outlook growth forecasts for Asian economies have been revised downwards, except for China:-

| Country/Region |

2017 |

Change |

| ASEAN* |

4.90% |

-0.20% |

| India |

7.20% |

-0.40% |

| China |

6.50% |

0.40% |

*Indonesia, Malaysia, Philippines, Thailand, Vietnam

Source: IMF

The moderation of the Indian forecast is related to the negative consumption shock, induced by cash shortages and payment disruptions, associated with the recent currency note withdrawal. I am indebted to Focus Economics for allowing me to share their consensus forecast for February 2017. It is slightly lower for China (6.4%) and slightly higher for India (7.4%) suggesting that Indian growth will be less curtailed.

China and India

Research by Knight Frank and Sumitomo Mitsui from early 2016, indicates that the Prime Yield on Real Estate in Bengaluru was 10.5%, in Mumbai, 10% and 9.5% in Delhi. With lower official interest rates in China, yields in Beijing and Shanghai were a less tempting 6.3%. These yields remain attractive when compared to London and New York at 4%, Tokyo at 3.7% and Hong Kong 2.9%. They are also well above the rental yields for the broader residential Real Estate market – India 3.10% and China 3.20%: it’s yet another case of Location, Location, Location.

This brings us to three other risk factors which are especially pertinent for the international Real Estate investor: currency movements, capital flows and the correlation to US stocks.

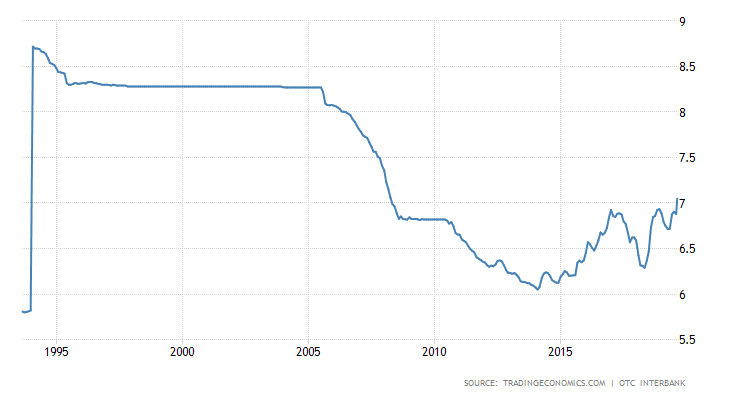

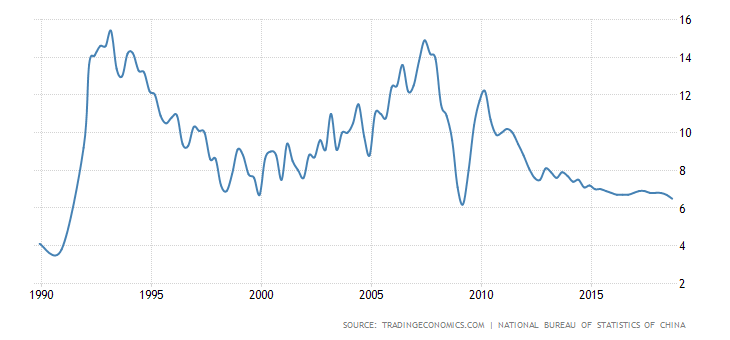

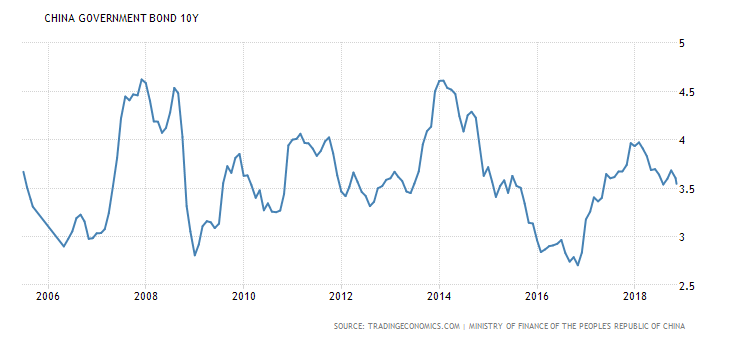

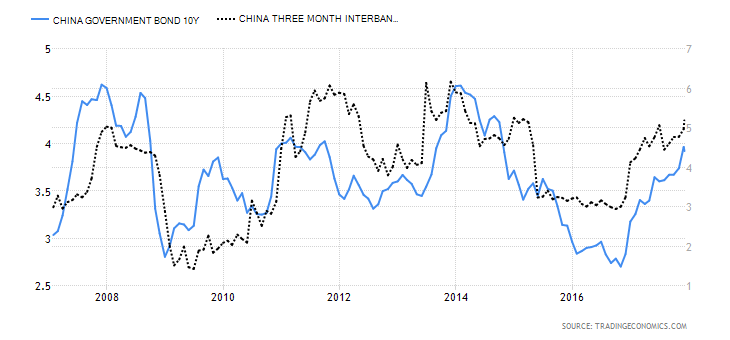

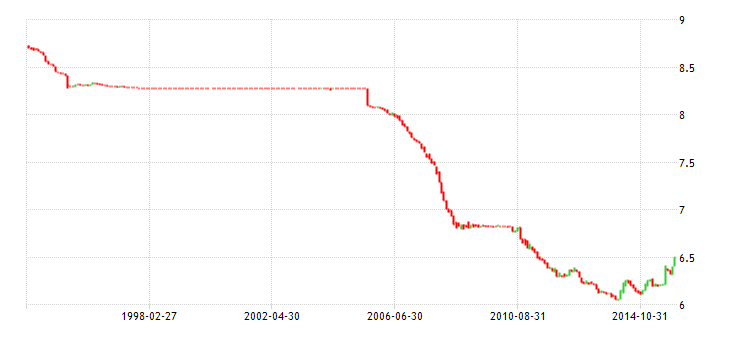

Since the Chinese currency became tradable in the 1990’s it has been closely pegged to the value of the US$. After 2006 the currency was permitted to rise from USDCNY 8.3 to reach USDCNY 6.04 in 2014. Since then the direction of the Chinese currency has reversed, declining by around 15%.

This recent currency depreciation may be connected to the reversal in capital flows since Q4, 2014. Between 2000 and 2014 China saw $3.6trln of inflows, around 60% of which was Foreign Direct Investment (FDI). Since 2014 these flows have reversed, but the rate of outflow has been modest; the trickle may become a spate, if the new US administration continues to shoot from the hip. A move back to USDCNY 8.3 is not inconceivable:-

Source: Trading Economics

Chinese inflation has averaged 3.86% since 1994, but since the GFC it has moderated to an annualised 2.38%.

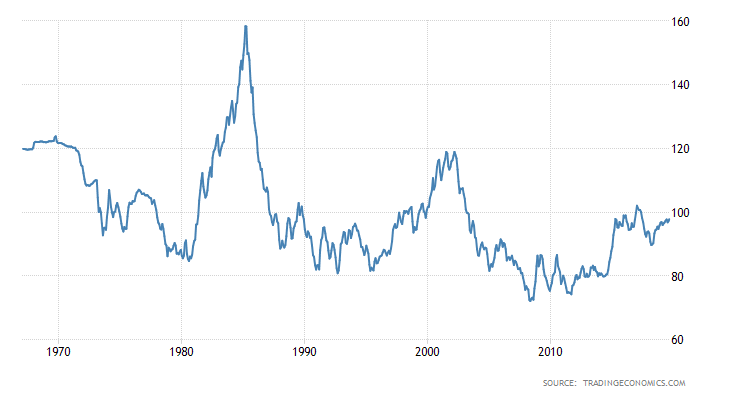

The Indian Rupee, which has been freely exchangeable since 1993, has been considerably more volatile: and more inclined to decline. The chart below covers the period since January 2007:-

Source: Trading Economics

Since 1993 Indian inflation has averaged 7.29%, but since 2008 it has picked up to 8.65%. The sharp currency depreciation in 2013 saw inflation spike to nearly 11% – last year it averaged 5.22% helped, by declining oil prices. Official rates, which hit 8% in 2014, are back to 6.25%, bond yields have fallen in their wake. Barring an external shock, Indian inflation should trend lower.

Capital flows have had a more dramatic impact on India than China, due to the absence of Indian exchange controls. A February 2016 working paper from the World Bank – Capital Flows and Central Banking – The Indian Experience concludes:-

Going forward, under the new inflation targeting framework, monetary policy will likely respond even more than before to meet the inflation target and adjust less than before to the capital flow cycles. One concern some people have with the move of a developing country such as India to inflation targeting is that it could result in greater exchange rate flexibility. Having liberalized the capital account progressively over the last two and a half decades, the scope to use capital flow measures countercyclically has perhaps diminished as well.

Thus in years ahead, reserve management and macroprudential measures are likely to play a more significant role in helping respond to capital flow cycles, just as the policy makers and the economy develop greater tolerance for exchange rate adjustments.

The surge and sudden stop nature of international capital flows, to and from India, are likely to continue; the most recent episode (2013) is sobering – the Rupee declined by 28% against the US$ in just four months, between May and August. The Sensex Stock Index fell 10.3% over the same period. The stock Index subsequently rallied 72%, making a new all-time high in March 2015. Since March 2015 the Rupee has weakened by a further 10.3% versus the US$ and the stock market has declined by 7.7% – although the Sensex was considerably lower during the Emerging Market rout of Q1, 2016.

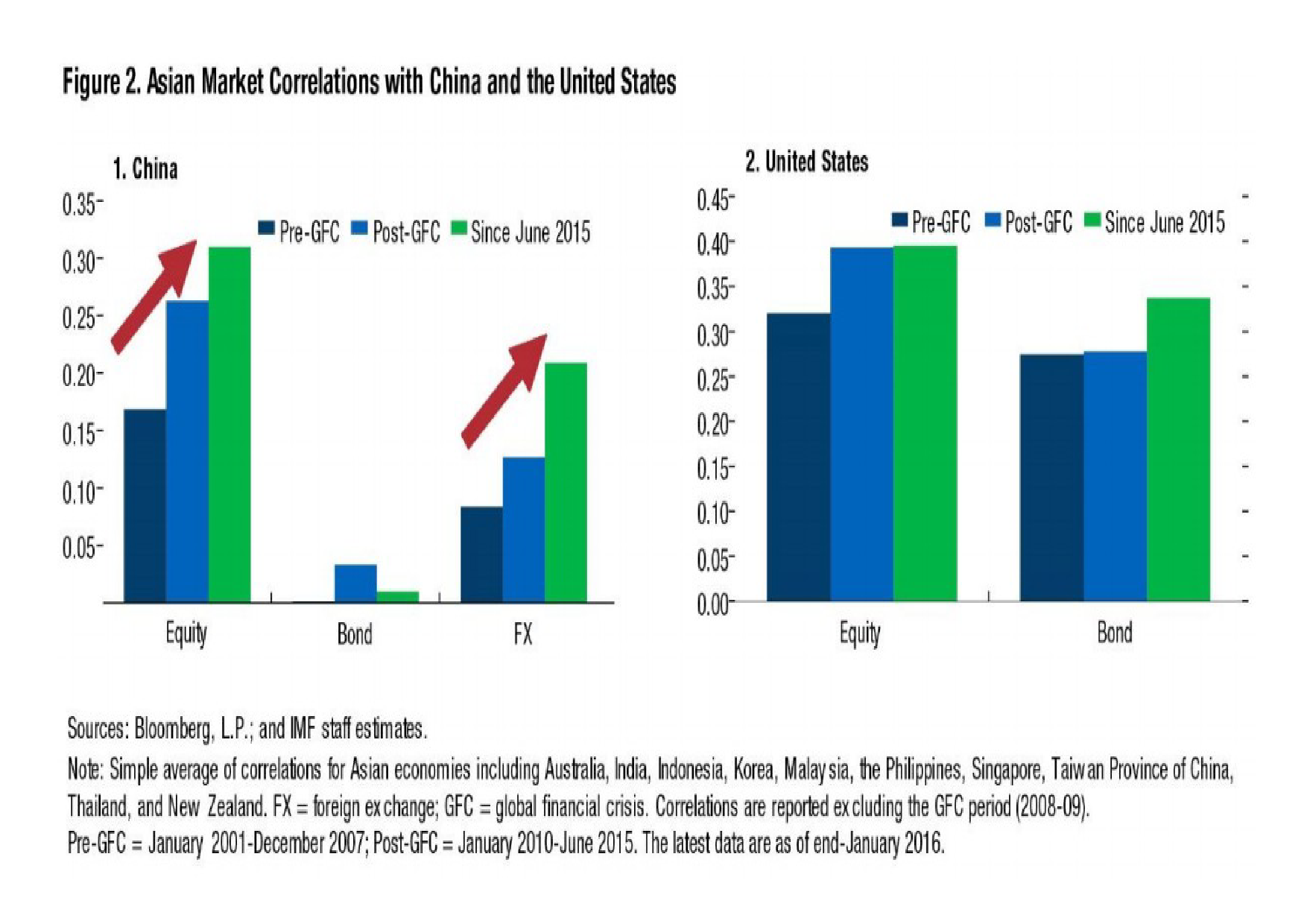

Stock market correlations are the next factor to investigate. The three year correlation between the S&P500 and China is 0.37 whilst for India it is 0.60. Since the Great Financial Crisis (GFC) however, the IMF has observed a marked increase in synchronicity between Asian markets and China. The IMF WP16/173 – China’s Growing Influence on Asian Financial Markets is insightful, the table below shows the rising correlation seen in Asian equity and bond markets:-

Source: IMF

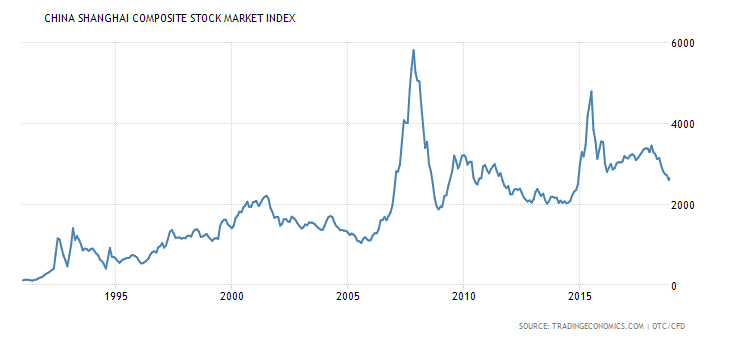

With so many variables, the best way to look at the relative merits, of China versus India and Real Estate versus Equities, is by translating their returns into US$. Since the GFC stock market low in March 2009, returns in US$ have been as follows. I have added the current dividend and residential rental yield:-

| Index |

Performance – March 09 – December 16 |

Performance in US$ |

Current Yield |

| S&P500 |

207% |

207% |

2% |

| FHFA House Price Index (US) |

9.70% |

9.70% |

2.20% |

| Shanghai Composite (China) |

50% |

49.20% |

4.20% |

| Shanghai Second Hand House Price Index |

74% |

72.85% |

3.20% |

| S&P BSE Sensex (India) |

204% |

135.25% |

1.50% |

| National Housing Bank Index (India) |

58%* |

38.45% |

3.10% |

| *Data to end Q1 2016 |

|

|

|

Source: Investing.com, FHFA, eHomeday, National Housing Bank, Global Property Guide

There are a number of weaknesses with this analysis. Firstly, it does not include reinvested income from dividends or rent – whilst the current yields are deceptively low. Data for the S&P500 suggests reinvested dividend income would have added a further 40% to the return over this period, however, I have been unable to obtain reliable data for the other markets. Secondly, the rental yield data is for residential property. You will note that Frank Knight estimate Prime Yields for Bengaluru at 10.5%, 10% for Mumbai and 9.5% for Delhi. Prime Yields in Beijing and Shanghai offer the investor 6.3% – Location, Location, Location.

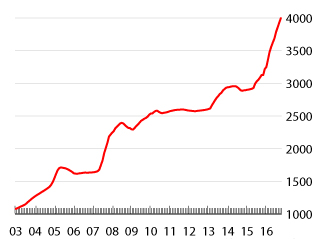

The chart below shows the evolution of the Shanghai Second Hand House Price Index since 2003:-

Source: eHomeday, Global Property Guide

For comparison here is the National Housing Bank Index since 2007:-

Source: National Housing Bank, Global Property Guide

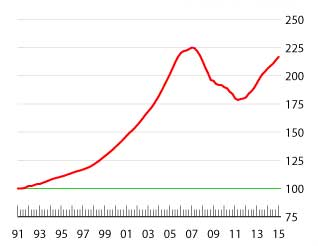

Finally, for global comparison, this is the FHFA – House Price Index going back to 1991:-

Source: FHFA, Global Property Guide

The Rest of Asia

In this Letter I have focused on China and India, but this article is about Asian Real Estate. The 2004-2014 annual return on Real Estate investment in Hong Kong was 14.4% – the market may have cooled but demand remains. Singapore has delivered 11.7% per annum over the same period. Cities such as Kuala Lumpur and Bangkok remain attractive. Vietnam, with a GDP forecast of 6.6% for 2017 and favourable demographics, offers significant potential – Hanoi and Ho Chi Minh are the cities on which to focus. Indonesia and the Philippines also offer economic and demographic potential, Jakarta and Manilla having obvious appeal. The table below, sorted by the Mortgage to Income ratio, compares the valuation for residential property and economic growth across the region:-

| Country |

Price/Income Ratio |

Rental Yield City |

Price/Rent Ratio City |

Mortgage As % of Income |

GDP f/c 2017 |

| Malaysia |

9.53 |

4.07 |

24.6 |

72.87 |

4% |

| Taiwan |

12.87 |

1.54 |

64.91 |

78.76 |

1.80% |

| South Korea |

12.38 |

2.04 |

49.1 |

85.47 |

2.40% |

| India |

10.28 |

3.08 |

32.44 |

123.44 |

7.40% |

| Singapore |

21.63 |

2.75 |

36.41 |

134.33 |

1.60% |

| Pakistan |

12.09 |

4.08 |

24.51 |

156.97 |

5.10% |

| Philippines |

16.91 |

3.75 |

26.69 |

162.87 |

6.60% |

| Bangladesh |

12.89 |

3.25 |

30.81 |

181.3 |

6.80% |

| China |

23.29 |

2.23 |

44.83 |

189.71 |

6.40% |

| Mongolia |

15.77 |

9.78 |

10.22 |

203.47 |

1.80% |

| Thailand |

24.43 |

3.8 |

26.29 |

212.03 |

3.30% |

| Hong Kong |

36.15 |

2.25 |

44.35 |

224.85 |

1.80% |

| Sri Lanka |

17.49 |

4.91 |

20.38 |

238.64 |

4.80% |

| Indonesia |

21.03 |

4.67 |

21.41 |

247.68 |

5.10% |

| Vietnam |

26.76 |

4.52 |

22.1 |

285.55 |

6.60% |

| Cambodia |

24.32 |

7.44 |

13.44 |

292.43 |

7% |

Source: Numbeo, Focus Economics, Trading Economics

There are opportunities and contradictions which make it difficult to draw investment conclusions from the table above: and this is just a country by country analysis.

Conclusions and Investment Opportunities

Real Estate, more so than any of the other major asset classes, is individual asset specific. Since we are looking for diversification we need to evaluate the two types of collective vehicle available to the investor.

Investing via REITs exposes you to the volatility of the stock market as well as the underlying asset. Investing directly via unlisted funds has been the preferred choice of pension fund managers in the UK for many years. There are pros and cons to this approach, but, for diversification, this is likely to be the less correlated strategy. Make sure, however, that you understand the liquidity constraints, not just of the fund, but also of the constituents of the portfolio. The GFC was, in particular, a crisis of liquidity: and property is not a liquid investment.

Unsurprisingly Norway’s $894bln Sovereign Wealth Fund – Norges Bank Investment Management – invests in Real Estate for the long run. This is how they describe their approach to the asset class, emphasis mine:-

The fund invests for future generations. It has no short term liabilities and is not subject to rules that could require costly adjustments at inopportune times.

…Our goal is to build a global, but concentrated, real estate portfolio…The strategy is to invest in a limited number of major cities in key markets.

According to Institutional Real Estate Inc. the largest investment managers in the Asia-Pacific Region at 31st December 2014 were. I’m sure they will be happy to take your call:-

| Investment Manager |

Asian AUM $Blns |

Total AUM $Blns |

| UBS Global Asset Management |

9.33 |

64.89 |

| Global Logistic Properties |

9.26 |

20.14 |

| CBRE Global Investors |

8.56 |

91.27 |

| LaSalle Investment Management |

8.05 |

55.75 |

| Blackstone Group |

7.58 |

121.88 |

| Alpha Investment Partners |

7.48 |

8.70 |

| Blackrock |

7.32 |

22.92 |

| Pramerica Real Estate Investors |

6.84 |

59.17 |

| Gaw Capital Partners |

6.64 |

9.16 |

| Prologis |

6.08 |

29.98 |

Source: Institutional Real Estate Inc.

In their August 2016 H2, 2016 Outlook, UBS Global Asset Management made the following observations:-

Although property yields across the APAC region are at, or close to, historical lows, demand for real estate exposure in a multi-asset context is set to remain healthy in the near-to-medium term. Capital inflows into the asset class will continue to be supported by broad structural shifts across the region related to demographics and demand for income producing assets on the one hand, and (ex-ante) excess supply of private (household and/or corporate) sector savings on the other. Part of this excess savings will continue to find its way into real estate, both in APAC and in other regions…

Real Estate investment in Asia offers opportunity in the long run, but for markets such as Shanghai (+26.5% in 2016) the next year may see a return from the ether. India, by contrast, has stronger growth, stronger demographics, higher interest rates and an already weak currency. The currency may not offer protection, inflation is still relatively high and the Rupee has been falling for decades – nonetheless, Indian cities offer a compelling growth story for Real Estate investors. Other developing Asian countries may perform better still but they are likely to be less liquid and less transparent. The developed countries of the region offer greater transparency and liquidity but their returns are likely to be lower. A specialist portfolio manager offers the best solution for most investors – that’s assuming you’re not a Sovereign Wealth Fund.