Macro Letter – No 21 – 10-10-2014

The Scotian experiment and European fragmentation

- Scotland voted to remain part of the Union but the devolution debate doesn’t end there

- Further European integration risks breaking the European Union

- Economic growth in the UK and Eurozone will be damaged by long-term uncertainty

The Scottish decision to remain part of the Union, by such a slim margin – 55% to 45% on an 85% turnout – caught me by surprise. On reflection it should not have been unexpected – it was as much about the “hearts” as the “minds” of the Scottish electorate. Now that the dust has settled, I wonder what this vote means for the United Kingdom and for other regions of Europe.

In this month’s issue of The World Today, Chatham House – A result that resolves little Malcolm Chambers – Research Director at the Royal United Services Institute (RUSI) made the following observations: –

The Scottish referendum was supposed to settle the UK’s constitutional uncertainties, but the result has raised more questions than it answers. How Britain addresses the devolution issue and the question mark over its commitment to Europe will shape perceptions of its ability to wield influence and hard power abroad for years to come.

Britain’s 2010 National Security Strategy, published shortly after the coalition government took office, was entitled ‘A Strong Britain in an Age of Uncertainty’. It made no mention of the two existential challenges – the possible secession of Scotland from the United Kingdom, and the risk of a British withdrawal from the European Union. Yet either event would be a fundamental transformation in the very nature of the British state, with profound impact on its foreign and security policy.

The article goes on to discuss the promises made to Scotland by Westminster’s political elite, from all the main parties, which may now create the conditions for eventual independence: –

Devolution max could have a similar effect, making the final step from ‘devo-max’ to ‘indy-light’ appear less traumatic, even as it still allows Westminster to be blamed for any ills that remain. If a further referendum is to be avoided five or ten years from now, it will not be enough to make constitutional changes.

Prime Minister Cameron took the opportunity to raise the issue of Scottish MPs voting on English issues; whilst this was politically expedient, it sows the seeds for regional calls for devolution of power to the poorer areas of Britain: –

Yet growing awareness of the constitutional imbalances created by devolution to Scotland – and, to a lesser extent, to Wales and Northern Ireland – is creating a series of shockwaves that will not dissipate easily. The UK, as a result, could now see a long period of constitutional experimentation and controversy, with profound effects on the governance of the country as a whole.

Chambers then turns to investigate the “European Question”. Here he sees a parallel between the UKs relationship with the EU and the Scottish desire for independence: –

Britain’s relationship with the European Union is similar, in important respects, to Scotland’s position in the United Kingdom. It has a special financial arrangement, involving a rebate of most of its net contribution, that is not available to other member states. It retains its own currency and border controls, and has a permanent exemption from the common currency and passport-free travel to which other states have agreed. As in Scotland, there is strong political pressure for the UK to be allowed special treatment in further areas, such as immigration controls. In both cases, attempts to construct ‘variable geometry’ governance frameworks are made more difficult by the asymmetry in size between the opting-out nation and the political union as a whole.

From the Brussels’ perspective the issue of devolution is not just restricted to the “Sceptred Isle”: –

While the nature of the Britain’s constitutional crises is unique, they are part of a wider crisis of European politics. Over the past five years, the eurozone has faced successive crises as it has sought to find a way to reconcile vast differences in economic interest and viewpoint between its member states. Relations between Germany and the southern states have worsened as the former takes on a more openly hegemonic role.

Without further significant sharing of political sovereignty – for example through a banking union – the risk that one or more member states could leave the eurozone will remain very substantial. Yet further political integration could bring its own challenges, with powerful nationalistic parties in northern Europe already pushing against those who argue that all the answers must come from Brussels. One of the reasons that Britain’s European allies were so worried about the Scotland vote was precisely their concern as to the example that a Yes vote could have sent to separatist movements in Spain, Belgium, Italy or Bosnia. This concern will not have been entirely dissipated, both because of the precedent set by London’s willingness to hold the vote, and by the closeness of the margin.

In conclusion Chambers states: –

It is still far from likely that the United Kingdom will perish, or that it will abandon its commitment to the European Union. But the possibility of one or both of these separations taking place seems set to be a central part of British politics for a decade or more.

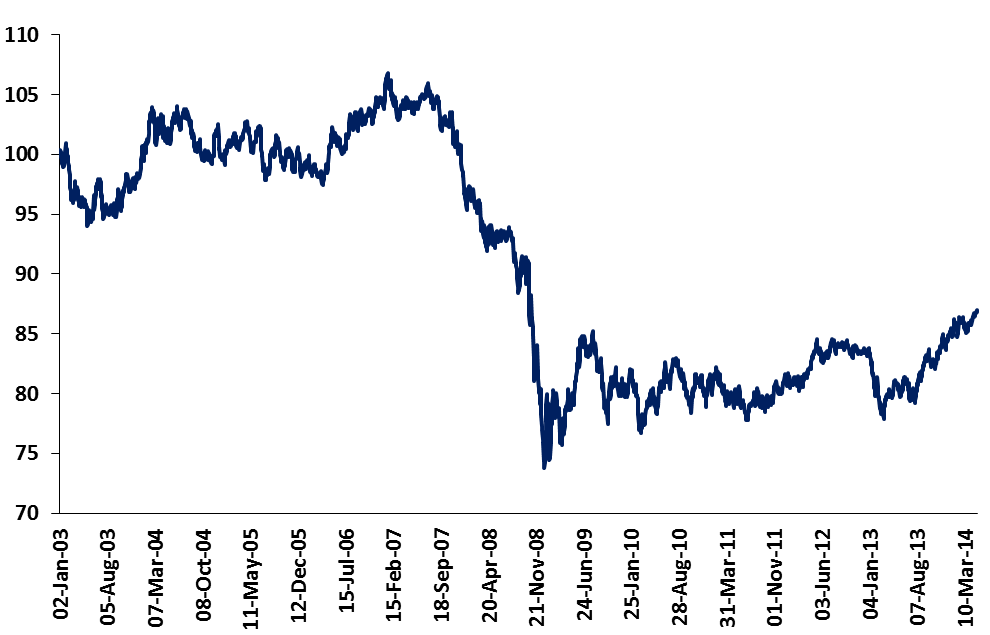

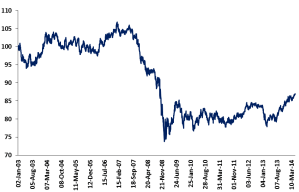

The impact on Sterling

Sterling is still some way below its longer-term average on a trade weighted basis as this chart of the Sterling Effective Exchange Rate (ERI) Index shows, however, it’s worth noting that the average between 1994 and 2013 is around 90: –

Source: Bank of England

Uncertainty always undermines the stability of ones currency and the Scottish referendum was no different, although its impact proved relatively minor. In a recent speech, Bank of England – The economic impact of sterling’s recent moves: more than a midsummer night’s dream – Kristin Forbes – MPC member, downplayed what could have been a dramatic decline in the value of the GBP:-

There has been some volatility in sterling recently, especially around the time of the Scottish referendum, but sterling is currently only 1% weaker than its recent peak in July 2014.

In her conclusion she points to the appreciation of the GBP since the Great Recession and cautions those who fail to anticipate the negative inflationary consequences of a weaker exchange rate: –

Where sterling’s recent moves may have had the greatest economic impact is on prices and inflation. A “top down” analysis estimating the pass-through from exchange rate movements to prices suggests that the lagged effect of sterling’s appreciation during 2013 and early 2014 may have acted as a powerful dampening effect on inflation. Although model simulations may be overestimating the magnitude of the effect, sterling’s past moves have reduced the risk of inflation increasing sharply, despite the strong growth in employment and the overall economy.

This dampening effect of sterling’s past appreciation, however, will peak at the end of 2014 and then begin to fade. As a result, it is becoming increasingly important to monitor trends in domestically-generated inflation – and especially unit labour costs – so that monetary policy can be adjusted appropriately and also be allowed to work through the economy with its own set of lags. Unfortunately, understanding recent trends in the domestic component of inflation – especially the slow growth in wages – has been challenging. A “bottom up” analysis of inflation that focuses on current measures of domestically-generated inflation (which attempt to minimize the dampening effect of sterling’s moves) show price pressures that are well contained and little evidence of imminent inflationary risks.

These “bottom up” indicators present a very different story then the “top down” estimates of inflation after adjusting for sterling’s recent appreciation. Has sterling’s appreciation had less of a dampening effect on prices than has traditionally occurred – perhaps due to structural changes in the UK or global economy? Or are the measures of domestic inflation understating current inflationary risks – perhaps due to the long lags before timely data is available? To answer these questions, it is critically important to monitor measures of prospective inflation to determine the appropriate path for monetary policy.

If concern about political devolution of power to the regions, at the expense of the power-house of the UK’s South East, and expectation of rising Euro-scepticism, are destined to be the pre-eminent political issues for the next decade, then an appreciation in the value of Sterling is likely to be tempered. Since the UK economy is closely integrated to Europe this persistent undervaluation will be less obvious in the GBP/EUR exchange rate but hopes of the trade weighted value of GBP rising like the USD due to structurally stronger growth will be muted.

In the aftermath of the referendum RUSI – Never the Same Again – What the Referendum Means for the UK and the World – observed:-

Having, for the first time, looked at what a ‘yes’ vote might mean for them, private investors and businesses are now more sensitised than ever before to the risks that a further referendum could pose. If some of them were to begin to hedge their bets accordingly, there could be a risk of an extended period of underinvestment in Scotland, with serious consequences for its prosperity.

Better together?

The campaign slogan of the Westminster elite was “Better Together” but, setting aside the rhetoric of power hungry politicians, what are the pros and cons of devolution versus Union? Writing ahead of the referendum Adam Posen of the Peterson Institute – The Huge Costs of Scotland Getting Small made a valiant case for continued integration: –

When is it ever a good idea for a small nation to set up on its own? Leaving aside cases of colonization and outright oppression, there is little good reason ever to shrink on the world scene by leaving a larger unit. The internal politics of democracies always get better deals for regions within them than small sovereigns can elicit from identity-ignoring market forces. The few small nations that did gain in welfare by seceding from transnational entities are those that escaped failed autocratic systems. The Baltic countries escaping the former Soviet Union’s dominance can be seen in this light. But setting out on your own is only beneficial when the system left behind has directly constrained your nation’s human potential. Whatever else, that cannot be said of the current Scottish situation in the United Kingdom.

It is a fact of life in today’s world that a small economy on its own is always buffeted by the forces of the global economy more than a region within a larger union. Even well-run small states like Singapore and Estonia are subject to huge swings in their economy resulting from capricious capital flows in and out. These swings disrupt employment, investment, and competitiveness via real exchange rate fluctuations. More important, small economies are fundamentally undiversified because of their small scale, and they risk their specializations falling out of favor in world markets. Events beyond their control can overwhelm the small nation’s high value-added industries, no matter how good it is at those things, be they oil extraction or banking or whisky distilling. Scottish independence in form will instead mean increased vulnerability in fact, because, inherently, smaller means more exposure when the markets turn—and turn they will.

…The economic debate over independence has tended to focus on the one-time transfer costs: setting up a new government administration, apportioning the accumulated public debt, grabbing as much oil as possible. But these issues are of minimal importance, however one chooses to measure them, compared to the ongoing costs of permanently greater insecurity to households and businesses. Even if an independent Scotland were to start out with the Scottish National Party (SNP) fantasy of relatively low public debt and a relatively high share of remaining oil revenues, it would have to save more, pay higher interest rates, and keep more space in its budget for self-insurance, hampered by a narrow tax base, in order to cope with the vicissitudes of the global economy on its own.

When one looks at the economic austerity foisted on the population of Greece and at the hopeless prospects much of the unemployed youth of Europe I wonder whether there is an alternative to the “integrationist” approach.

Looking for an answer I went back to the forging of the United Kingdom. This is how John Lancaster describes the events which led to the Act of Union in 1707:-

During the 17th century, Scottish investors had noticed with envy the gigantic profits being made in trade with Asia and Africa by the English charter companies, especially the East India Company. They decided that they wanted a piece of the action and in 1694 set up the Company of Scotland, which in 1695 was granted a monopoly of Scottish trade with Africa, Asia and the Americas. The Company then bet its shirt on a new colony in Darien – that’s Panama to us – and lost. The resulting crash is estimated to have wiped out a quarter of the liquid assets in the country, and was a powerful force in impelling Scotland towards the 1707 Act of Union with its larger and better capitalised neighbour to the south. The Act of Union offered compensation to shareholders who had been cleaned out by the collapse of the Company; a body called the Equivalent Society was set up to look after their interests. It was the Equivalent Society, renamed the Equivalent Company, which a couple of decades later decided to move into banking, and was incorporated as the Royal Bank of Scotland. In other words, RBS had its origins in a failed speculation, a bail-out, and a financial crash so big it helped destroy Scotland’s status as a separate nation.”

The above passage, taken from Lancaster’s 2009 book It’s Finished, is quoted near the opening of a recent article by Tim Price – Let’s Stick Together in which he refers to Leopold Kohr – The Breakdown of Nations. The forward by Kirkpatrick Sale describes the problem of size when nation building: –

What matters in the affairs of a nation, just as in the affairs of a building, say, is the size of the unit. A building is too big when it can no longer provide its dwellers with the services they expect – running water, waste disposal, heat, electricity, elevators and the like – without these taking up so much room that there is not enough left over for living space, a phenomenon that actually begins to happen in a building over about ninety or a hundred floors. A nation becomes too big when it can no longer provide its citizens with the services they expect – defence, roads, post, health, coins, courts and the like – without amassing such complex institutions and bureaucracies that they actually end up preventing the very ends they are intending to achieve, a phenomenon that is now commonplace in the modern industrialized world. It is not the character of the building or the nation that matters, nor is it the virtue of the agents or leaders that matters, but rather the size of the unit: even saints asked to administer a building of 400 floors or a nation of 200 million people would find the job impossible.

Kohr grew up in a small village which may have helped him to recognise one of the intrinsic weaknesses of democracy: that it works best on a small scale.

Taking this theme further and applying it to an independent Scotland, John Butler – From bravery to prosperity: A six-year plan to make Scotland the wealthiest Anglosphere region of all makes the case for a smaller more flexible approach. Here is an abbreviated version of his six point plan:-

Debt Repayment

The Scots’ legendary bravery is equalled by legendary parsimony, the first essential element of success. There is no growth without investment and no sustainable investment without savings. It stands to reason that you aren’t a parsimonious society if you carry around a massive, accumulating national debt. Debt service is also a drag on future growth. Thus if the Scots want to prosper long-term, they are going to need to pay down their share of the UK national debt.

Tax Reduction

There are several policies that would quickly create an investment boom. Most important, Scotland should do better than celtic rival Ireland, with a low corporate tax rate, and abolish the corporate income tax altogether. Yes, you read that right: The effective corporate income tax in many countries now approaches zero anyway, due to all manner of creative cross-border accounting.

Human Capital

Developing human capital, at which the Scots excelled in the 19th century, is the third element. Consider which industries are most likely to relocate to Scotland: Those requiring neither natural resources nor extensive industrial infrastructure, that is, those comprised primarily of human capital. Although financial services comes to mind, there is tremendous overcapacity in this area in England and Ireland, including in unproductive yet risky activities, so that is better left to the English and Irish for now. Better would be to concentrate on health care, for example, an industry faced with soaring costs and stifling regulation in much of the world.

Scotland could, inside of six years, become the world’s premier desination for so-called ‘healthcare tourism’. Scotland lies directly under some of the world’s busiest airline routes, an ideal location.

Sound Banking

A fourth essential element to success is to implement Scottish Enlightenment principles for sound banking. This is of utmost importance due to the potential monetary and financial instability of the UK and much of the broader Anglosphere.

As a first step, Scotland should forbid any bank from conducting business in Scotland if they receive any direct financial assistance from the Bank of England or from the UK government. In turn, Scotland should make clear to Westminster that Scottish residents will not contribute to any taxpayer bail out of any UK financial institution. No ‘lender of last resort’ function will exist for financial activities in Scotland, unless such action, if formally requested by a bank, is approved by the Scots in a referendum. (Taxpayers are always on the hook for bailouts one way or the other; why not make this explicit?)

Self-Reliance

The fifth element reaches particularly deep into Scottish history: Self-Reliance. Peoples that inhabit relatively inhospitable or infertile lands tend to establish cultures with self-reliance at the core. No, this does not make them culturally backward, but it does tend to contribute to a distrust of foreign or central authority. The Scots, while brave, were frequently disunited in their opposition to English rule, something that had unfortunate consequences for many, not just William Wallace.

Scottish Presbyterianism

Finally, there is the sixth element: the collective cultural traditions of Scottish Presbyterianism. There are few religions in the world that hold not only faith, but hard work, thrift and charity in such high regard as that of traditional Presbyterianism. Yes, as with most all Europeans, the Scots have become more secular in recent decades. But the same could be said of the Germans, who nevertheless cling to their own, solid Protestant work ethic and associated legal and moral anti-corruption traditions.

To be fair to Adam Posen of the Peterson Institute, none of the arguments for a non-integrated Scotland solve the problems of vulnerability to external shocks. The crux of the issue is whether a larger, more integrated unit, is more effective than a smaller more flexible one.

The Politics of Empires

“Power tends to corrupt, and absolute power corrupts absolutely. Great men are almost always bad men.” Lord Acton – 1834-1902.

Throughout history successful nations have grown through expansion and integration. The process is cyclical, however, and success sows the seeds of its own demise. Europe emerged from the dark ages to conquer much of the known world. Since then it has imploded during two world wars and may now be embarking on a further wave of integration. Or, perhaps, this is the last attempt to assimilate a multitude of disparate cultures before the “long withdrawing breath” into smaller, more dynamic, self-reliant units.

In the opening chapter of Edward Gibbon’s “Decline and Fall of the Roman Empire” he says:-

…but it was reserved for Augustus (who became Caesar in BC 44) to relinquish the ambitious design of subduing the whole earth and to introduce a spirit of moderation into the public councils.

However, I believe the seeds of destruction, which eventually created the conditions for the establishment of A NEW Europe, stem from Diocletian’s introduction of the Tetrarchy in AD 284. It divided the Roman Empire in four regions.

Diocletian’s son, Constantine attempted to slow this fragmentation by adopting Christianity as the official religion of the empire, however, his decision to move the seat of government from Rome to Byzantium in AD 324 set the stage for the final schism into the Eastern and Western Empires which occurred in AD395 on the demise of Theodosius.

The Western Empire sustained continuous assaults from Vandals, Alans, Suebis and Visigoths leading to the second sack of Rome in AD 410 by Alaric. The Western Empire finally collapsed in AD 476 when the Germanic Roman general Odoacer deposed the last emperor, Romulus . Europe had descended into a “dark age” of constant wars between rival tribes. The sole pan-European administrative organization after the fall of the Western Empire was the Catholic Church, which adopted the remnants of its infrastructure.

The creation of the Europe we recognise today began with the conversion to Christianity of Clovis – King of the Franks – in AD 498, but it was not until the re-uniting of the Frankish kingdoms in AD 751 under Pepin The Short and the subsequent appointment of his son Charlemagne as Holy Roman Emperor in AD 800 that the idea of a Christian “Western Europe” began to emerge. When viewed from this long historical perspective the current development of the EU is still in its infancy.

In the East, Constantinople remained the administrative center of the Byzantine Empire. Under Emperor Justinian in AD 526 the Empire expanded. Challenges from the Lombards in AD 568 saw the loss of Northern Italy, but the rise of Islam after AD 623 proved a more terminal event. Although Byzantium went into decline, due to many assailants – not least the Western Empire – it limped on until 1453 when it to finally succumbed to the Ottoman Turks.

Why the history lesson? The spark of the industrial revolution was kindled in Europe. It developed out of the chaotic collapse of the Western Roman Empire, the warring between a plethora of tribes and the rise of independent city states. It was built on the fragmented polity of petty fiefdoms and the desire to trade despite national borders and political restrictions on the movement of labour and goods. The renaissance began in Italy where the competition between small city states stimulated “animal spirits”. The flowering of art and culture that this democratisation of prosperity set in motion goes some way to support the idea that “small is beautiful”.

During the dark ages the concept of “Nationhood” was fluid, as exemplified by the Dukes of Normandy’s fealty after 1066 to the King of France, but only in respect of their French domains. As nation states began to coalesce international trade developed further. Nations waxed and waned, alliances were made and broken but no single nation succeeded in dominating the whole region. Demographic growth encouraged voyages of discovery. Colonisation followed, and finally the conditions were propitious for the birth of the industrial revolution from which we continue to benefit today.

These processes were gradual, running their course over many generations. I believe Europe is now fragmenting once more; painful for our own time but filled with promise for future generations. Calls for self-government from many regions within the EU will increase. The more Brussels attempts to make its citizens feel European the more its citizens will yearn for self-determination.

This trend will be driven by a number of factors aside from the declining effectiveness of central government. Bruegal – The Economics of big cities articulates one of these economic paradoxes, how globalisation has made the world more local: –

Local economies in the age of globalization

Enrico Moretti writes that the growing divergence between cities with a well-educated labor force and innovative employers and the rest of world points to one of the most intriguing paradoxes of our age: our global economy is becoming increasingly local. At the same time that goods and information travel at faster and faster speeds to all corners of the globe, we are witnessing an inverse gravitational pull toward certain key urban centers. We live in a world where economic success depends more than ever on location. Despite all the hype about exploding connectivity and the death of distance, economic research shows that cities are not just a collection of individuals but are complex, interrelated environments that foster the generation of new ideas and new ways of doing business.

Enrico Moretti writes that, historically, there have always been prosperous communities and struggling communities. But the difference was small until the 1980’s. The sheer size of the geographical differences within a country is now staggering, often exceeding the differences between countries. The mounting economic divide between American communities – arguably one of the most important developments in the history of the United States of the past half a century – is not an accident, but reflects a structural change in the American economy. Sixty years ago, the best predictor of a community’s economic success was physical capital. With the shift from traditional manufacturing to innovation and knowledge, the best predictor of a community’s economic success is human capital.

Human Capital may be defined as “the skills, knowledge, and experience possessed by an individual or population”. In the internet age this resource can be located almost anywhere and need not be isolated due to email, telephone or video conference technology, however, the advantages of physical proximity and social interaction favour cities.

Another, and related, issue is the increasingly disruptive effect of technology on employment. Bruegal – 54% of EU jobs at risk of computerisation – highlights one of the greatest economic challenges to the social fabric of the EU, but this is a global phenomenon: –

Based on a European application of Frey & Osborne (2013)’s data on the probability of job automation across occupations, the proportion of the EU work force predicted to be impacted significantly by advances in technology over the coming decades ranges from the mid-40% range (similar to the US) up to well over 60%.

Those authors expect that key technological advances – particular in machine learning, artificial intelligence, and mobile robotics – will impact primarily upon low-wage, low-skill sectors traditionally immune from automation. As such, based on our application it is unsurprising that wealthy, northern EU countries are projected to be less affected than their peripheral neighbours.

European governments are caught between the competing needs of an aging population and a younger generation who have little prospect of finding gainful full-time employment. Meanwhile city workers are paying for the regions where unemployment is highest. The tension between “wealth makers” and “wealth takers” are destined to increase.

Conclusion

Scotland voted to remain part of the Union. The Independence campaign was ill prepared failing to consider such issues as what currency they would use or how they would avoid a run on their banking system. The next time the Scots vote – and there will be a next time – I believe they will leave the Union because these questions will have been addressed. Other regions around the UK and Europe have taken note – the spirit of devolution is abroad. Prosperous regions, such as Catalunya and Northern Italy – Padania as it is sometimes called – crave independence from their poorer neighbours. Poorer regions resent the straight jacket of a single currency – be it the GBP for regions like the North East of England or the EUR for Greece and Portugal. To the poorer regions, the flexibility of a floating exchange rate is beguiling; as the EU stumbles through an era of debt laden low growth devolution pressures will increase.

For the GBP and EUR the Scottish “No” vote will fail to diminish the potential for social and political tension. The value of these currencies will reflect that uncertainty. Longer-term foreign direct investment will be lower. This will place an additional burden on EU budgets. A larger percentage of central government spending will be directed to regions where calls for devolution are highest rather than to economically productive projects in more prosperous areas.

European and UK equities are likely to under-perform in this environment whilst the increased indebtedness of EU governments is likely to increase their real borrowing costs.

Will this happen soon and will it be possible to measure? I think it is already happening but, given the very long-term nature of the fragmentation of nations, it will be difficult to measure except during constitutional crises. The shorter-term business cycles will still exist. Trading and investment opportunities will continue to arise. For the investor, however, it is essential to be aware of the risks and rewards which this fragmentation process will present.