The Giant Debt-for-Equity Swap

I wrote this article in December 2019. Much has changed but with bond yields heading lower on the back of more QE, it still seems surprisingly valid.

The Giant Debt-for-Equity Swap

I wrote this article in December 2019. Much has changed but with bond yields heading lower on the back of more QE, it still seems surprisingly valid.

Macro Letter – No 68 – 13-01-2017

Equity valuation in a de-globalising world

In this Macro Letter I review stock market valuation. I conclude with some general recommendations but the main purpose of my letter is to investigate different methods of valuation and consider the benefits and dangers of diversification. I begin by looking at the US market and the prospects for the US economy. Then I turn to global equity markets, where I consider the benefits and perils of diversification into Frontier stocks. I go on to review global industry sectors, before returning to examine the long term value to be found in developed markets. I finish by looking at the recent outperformance of Value versus Growth.

US Stocks and the Yield Gap

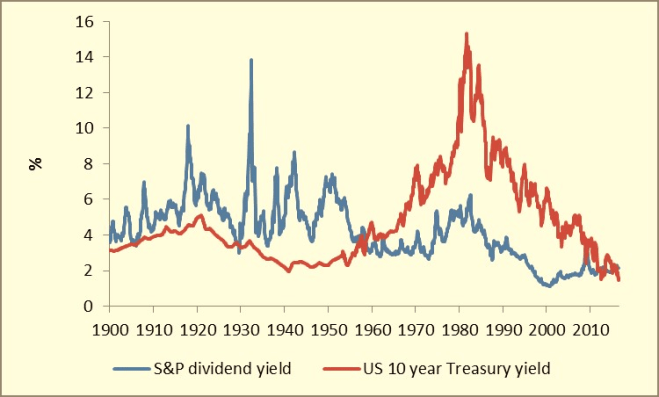

The Equity bull market is entering its eighth year and for US stocks this is the second longest bull-market since WWII – the longest being, between 1987 and 2000. The current bull-market has differed from the 1987-2000 period in that interest rates have fallen throughout the period. Bond yields have also declined to historically low levels. The Yield Gap – the premium of dividend yields over bond yields – which had been inverted since the mid-1950’s, turned positive once more. The chart below shows the yield of the S&P500 and 10yr T-Bonds since 1900:-

Source: Reuters

What this chart shows most clearly is that the return to a positive Yield Gap has been a function of falling bond yields rather than any substantial rise in dividend pay-out.

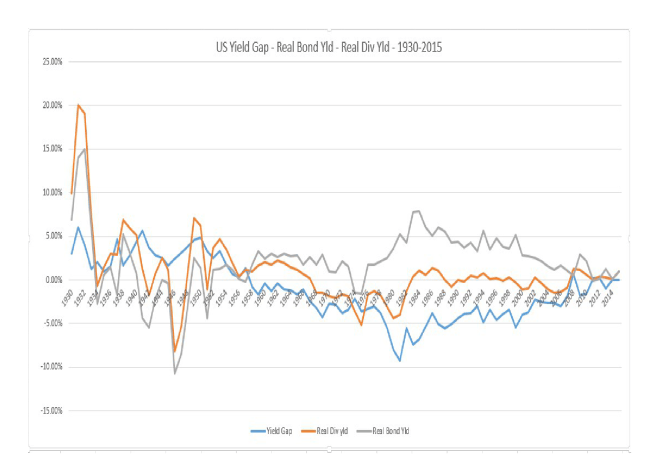

The chart below looks at the relationships between the Yield Gap and the real return on US 10yr Treasuries and S&P500 dividends since 1930 – I have used the Implicit Price Deflator as the measure of inflation:-

Source: Multpl, St Louis Federal Reserve

The decline in the real dividend yield was a response to rising inflation from the late 1950’s onwards. The return to a positive Yield Gap has been a recent phenomenon. The average Yield Gap since 1900 is -0.51%, since 1930 it has been -1.17%. It has been below its long-run average at -0.37% since 2008. The executive officers of US corporations will continue to favour share buy-backs over increased dividends – I do not expect dividend yields to keep pace with any pick-up in inflation in the near-term, but, share buy-backs will continue to support stocks in general.

S&P 500 forecasts for 2017

What does this mean for the return on the S&P 500 in 2017? According to Bloomberg, the consensus forecast is for a rise of 4% but the range of forecasts is a rather narrow +1.3% to +8.3%. As at the close on 11th January we were already up 1.6% from the 30th December close.

Corporate earnings continue to rise although the pace of increase has moderated. Factset Earning Insight – January 6th – makes the following observations:-

Earnings Growth: For Q4 2016, the estimated earnings growth rate for the S&P 500 is 3.0%. If the index reports earnings growth for Q4, it will mark the first time the index has seen year-over-year growth in earnings for two consecutive quarters since Q4 2014 and Q1 2015.

Earnings Revisions: On September 30, the estimated earnings growth rate for Q4 2016 was 5.2%. Ten of the eleven sectors have lower growth rates today (compared to September 30) due to downward revisions to earnings estimates, led by the Materials sector.

Earnings Guidance: For Q4 2016, 77 S&P 500 companies have issued negative EPS guidance and 34 S&P 500 companies have issued positive EPS guidance.

Valuation: The forward 12-month P/E ratio for the S&P 500 is 17.1. This P/E ratio is above the 5-year average (15.1) and the 10-year average (14.4).

Earnings Scorecard: As of today (with 4% of the companies in the S&P 500 reporting actual results for Q4 2016), 73% of S&P 500 companies have beat the mean EPS estimate and 36% of S&P 500 companies have beat the mean sales estimate.

…For Q1 2017, analysts are projecting earnings growth of 11.0% and revenue growth of 7.9%.

For Q2 2017, analysts are projecting earnings growth of 10.5% and revenue growth of 6.0%.

For all of 2017, analysts are projecting earnings growth of 11.5% and revenue growth of 5.9%.

…At the sector level, the Energy (33.2) sector has the highest forward 12-month P/E ratio, while the Telecom Services (14.2) and Financials (14.2) sectors have the lowest forward 12-month P/E ratios. Nine sectors have forward 12-month P/E ratios that are above their 10-year averages, led by the Energy (33.2 vs. 17.9) sector. One sector (Telecom Services) has a forward 12-month P/E ratio that is below the 10-year average (14.2 vs. 14.6).

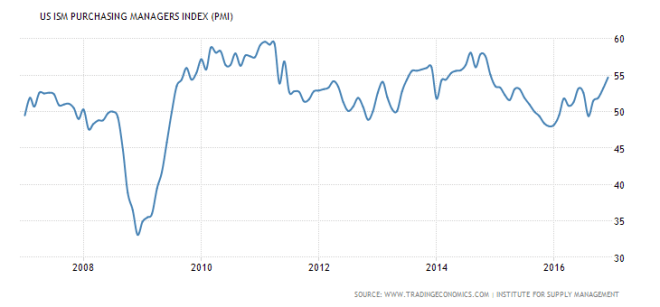

Other indicators, which should be supportive for the US economy, include the ISM – PMI Index which is closely correlated to the business cycle. It came in at 54. 7 the highest since November 2014. Here is a 10 year chart:-

Source: Trading Economics, Institute for Supply Management

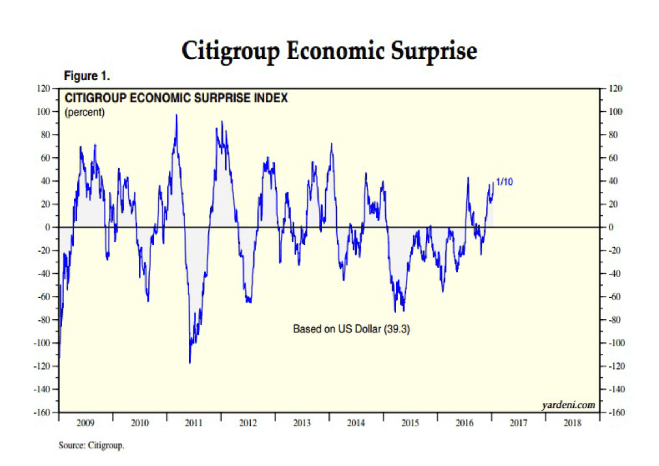

A shorter-term indicator for the US economy is the Citigroup Economic Surprise Index – CESI. The chart below suggests that the surprise caused by Trump’s presidential victory is still gathering momentum:-

Source: Yardeni, Citigroup

With both the ISM and the CESI indices rising, even the most bearish of macro-economist is likely to be “sceptically positive” on the US economy and this should be supportive for the US stock market.

Global Stocks

I have focussed on the US stock market because of the close correlation between the US and other major stock markets around the world.

As the world becomes less globalised, or as one moves away from the major stock markets, the diversification benefits of a global portfolio, such as the one Andrew Craig describes in his book “How to Own the World”, becomes more enticing. Andrew recommends diversification by asset class, but even a diversified equity portfolio – without the addition of bonds, commodities, real-estate and infrastructure – can offer an enhanced Sharpe Ratio. The table below looks at the three year monthly correlations of emerging and frontier stock markets with a correlation of less than 0.40 to the US market:-

| Country | Correlations < 0.40 to US stocks – 36 months |

| Malawi | -0.12 |

| Iraq | -0.12 |

| Panama | -0.01 |

| Cambodia | 0.00 |

| Rwanda | 0.01 |

| Venezuela | 0.01 |

| Uganda | 0.01 |

| Trinidad and Tobago | 0.02 |

| Tunisia | 0.02 |

| Botswana | 0.07 |

| Mauritius | 0.07 |

| Tanzania | 0.08 |

| Palestine | 0.09 |

| Laos | 0.09 |

| Ghana | 0.10 |

| Zambia | 0.10 |

| Peru | 0.11 |

| Bahrain | 0.13 |

| Jordan | 0.15 |

| Cote D’Ivoire | 0.15 |

| Sri Lanka | 0.16 |

| Argentina | 0.17 |

| Nigeria | 0.17 |

| Qatar | 0.21 |

| Kenya | 0.21 |

| Pakistan | 0.24 |

| Jamaica | 0.24 |

| Oman | 0.25 |

| Colombia | 0.27 |

| Saudi Arabia | 0.31 |

| Kuwait | 0.36 |

| China | 0.37 |

| Bermuda | 0.38 |

| Egypt | 0.38 |

| Vietnam | 0.39 |

Source: Investment Frontier

Many of these stock markets are illiquid or suffer from investment restrictions: but here you will find some of the fastest growing economies in the world. These correlations look beguilingly low but remember that during broad-based market declines short-term correlations tend to rise – the illusory nature of liquidity drives this process. The price of a financial asset is driven by investment flows, cognitive behavioural biases drive investment decisions. Herd instinct rises dramatically when fear replaces greed.

Industry Sectors

The major stock markets also offer opportunities. Looking globally by industry sector there are some attractive longer-term value propositions. The table below ranks the major markets by sector as at 30th December 2016. The sectors have been sorted by trailing P/E ratio (mining and alternative energy P/E data is absent but by other measures mining is relatively cheap):-

| Industry Sector | PE | PC | PB | PS | DY |

| Real Est Serv | 11.2 | 14.9 | 1 | 2.2 | 2.70% |

| Auto | 12.1 | 5.7 | 1.4 | 0.6 | 2.50% |

| Banks | 13.8 | 9.6 | 1.1 | 3.30% | |

| Life Insur | 14.2 | 6.4 | 1.1 | 0.7 | 3.00% |

| Electricity | 14.9 | 5.6 | 1.3 | 1.1 | 4.00% |

| Forest & Paper | 15.1 | 7.1 | 1.6 | 0.9 | 2.90% |

| Nonlife Ins | 16.2 | 10.4 | 1.3 | 1 | 2.40% |

| Financial Serv | 16.7 | 13.8 | 1.8 | 2.3 | 2.20% |

| Telecom (fxd) | 17.5 | 5.5 | 2.3 | 1.4 | 4.20% |

| Travel & Leisure | 17.6 | 9.1 | 2.9 | 1.4 | 2.10% |

| Tech HW & Equ | 18.3 | 10.7 | 3 | 1.8 | 2.30% |

| Chemicals | 18.8 | 10.1 | 2.4 | 1.3 | 2.60% |

| Household Gds | 18.8 | 15 | 2.8 | 1.7 | 2.40% |

| Gen Ind | 19 | 11.3 | 1.9 | 1.1 | 2.40% |

| REITs | 20.4 | 16.7 | 1.7 | 7.7 | 4.50% |

| Construction | 20.9 | 11.4 | 1.9 | 0.9 | 2.10% |

| Telecom (mob) | 21.4 | 5.6 | 1.9 | 1.5 | 3.30% |

| Tobacco | 21.5 | 21.1 | 9.8 | 4.9 | 3.60% |

| Media | 21.6 | 10.9 | 2.9 | 2 | 2.10% |

| Food Retail | 21.6 | 10.2 | 2.8 | 0.4 | 2.00% |

| Eltro & Elect Equ | 21.7 | 12.2 | 2.2 | 1 | 1.70% |

| Pharma & Bio | 22.4 | 16.3 | 3.4 | 3.5 | 2.30% |

| Food Prod | 23.2 | 14.3 | 2.6 | 1.2 | 2.20% |

| Healthcare | 23.7 | 13.1 | 3.2 | 1.4 | 1.10% |

| Leisure Gds | 23.9 | 8.4 | 2 | 1.1 | 1.20% |

| Inds Transport | 23.9 | 10.4 | 2.5 | 1.3 | 2.50% |

| Aero & Def | 23.9 | 14.9 | 5 | 1.3 | 2.10% |

| Inds Eng | 24.6 | 12.4 | 2.5 | 1.1 | 2.00% |

| Personal Gds | 24.7 | 16.8 | 4.3 | 2 | 2.00% |

| Gen Retail | 25.8 | 14 | 4.2 | 1 | 1.70% |

| Support Serv | 26.4 | 11.9 | 2.8 | 1.1 | 1.90% |

| Beverages | 27 | 14.9 | 4.2 | 2.4 | 2.70% |

| SW & Comp Serv | 27.3 | 15.9 | 4.5 | 3.8 | 1.10% |

| Oil Service | 73.9 | 11.8 | 1.9 | 1.7 | 3.70% |

| Oil&Gas Prod | 116.9 | 8.2 | 1.4 | 1 | 3.10% |

| Inds Metal | 165.7 | 7.7 | 1.1 | 0.7 | 2.40% |

| Mining | 8.9 | 1.6 | 1.5 | 1.90% | |

| Alt Energy | 10.5 | 1.7 | 0.9 | 1.20% |

Source: Star Capital

A number of sectors have been out of favour since 2008 and may remain so in 2017 but it is useful to know where under-performance can be found.

Developed Market Opportunities

At a country level there is better long-term valuation to be found outside the US, even among the developed countries. Here is Star Capital’s 10 to 15 year total annual return forecast for the major markets and regions:-

| Country | CAPE | Forecast | PB | Forecast | ø Forecast |

| Italy | 12.7 | 9.10% | 1.2 | 10.40% | 9.70% |

| Spain | 11.7 | 9.70% | 1.4 | 8.80% | 9.30% |

| United Kingdom | 14.8 | 8.00% | 1.8 | 7.20% | 7.60% |

| France | 18.3 | 6.60% | 1.6 | 8.10% | 7.30% |

| Australia | 16.8 | 7.10% | 2 | 6.60% | 6.90% |

| Germany | 18.6 | 6.40% | 1.8 | 7.40% | 6.90% |

| Japan | 24.9 | 4.40% | 1.3 | 9.40% | 6.90% |

| Netherlands | 19.8 | 6.00% | 1.8 | 7.20% | 6.60% |

| Canada | 20.5 | 5.70% | 1.9 | 6.90% | 6.30% |

| Sweden | 20.6 | 5.70% | 2.1 | 6.20% | 5.90% |

| Switzerland | 21.5 | 5.40% | 2.4 | 5.30% | 5.30% |

| United States | 26.4 | 4.00% | 2.9 | 4.10% | 4.00% |

| Emerging Markets | 14 | 8.40% | 1.6 | 7.90% | 8.20% |

| Developed Europe | 16.6 | 7.20% | 1.8 | 7.40% | 7.30% |

| World AC | 20.8 | 5.60% | 2 | 6.70% | 6.20% |

| Developed Markets | 21.9 | 5.30% | 2 | 6.50% | 5.90% |

Source: Star Capital, Bloomberg, Reuters

I have sorted this data based on Star Capital’s composite annual return forecast. The first three countries, Italy, Spain and the UK, all face uncertainty linked to the future of the EU. Interestingly Switzerland offers better long-term returns than the US – with considerably less currency risk for the international investor.

Value Investing

Since the financial crisis in 2008 through to 2015 Growth stocks outperformed Value stocks. I predict a sea-change. The fathers of Value Investing, Ben Graham and David Dodd first published Securities Analysis in 1934. Towards the end of his career Graham opined (emphasis is mine):-

I am no longer an advocate of elaborate techniques of security analysis in order to find superior value opportunities. This was a rewarding activity, say, 40 years ago, when our textbook “Graham and Dodd” was first published; but the situation has changed a great deal since then. In the old days any well-trained security analyst could do a good professional job of selecting undervalued issues through detailed studies; but in the light of the enormous amount of research now being carried on, I doubt whether in most cases such extensive efforts will generate sufficiently superior selections to justify their cost. To that very limited extent, I’m on the side of the “efficient market” school of thought now generally accepted by the professors.

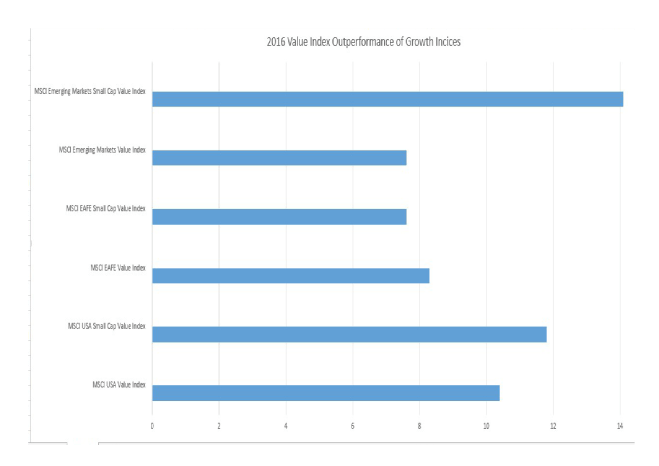

As we embrace the “Big Data” era, the cost of analysing vast amounts of data will collapse, whilst, at the same time, the amount of available data will grow exponentially. I believe we are at the dawn of a new age for Value Investing where the quantitative analysis of a vast array of qualitative factors will allow investors to defy the Efficient Market Hypothesis, even if we cannot satisfactorily refute Eugene Fama’s premise. In 2016, for the first time in seven years, Value beat Growth across all major categories:-

Source: MSCI, Bloomberg

Value stocks tend to exhibit higher volatility than growth stocks, but volatility is only one aspect of risk: buying Value offers long-term protection, especially during an economic downturn. According to Bloomberg’s Nir Kaissar, Value has consistently underperformed Growth since the financial crisis except in US Small Cap’s – his article – Value Investing Hits Back – is insightful.

Conclusion and Investment Opportunities

When I first began investing in stocks the one of the general rules was to buy when the P/E ratio was below 10 and sell when it rose above 20. Today, of the world’s major stock markets, only Russia and China offer single digit P/Es – low ratios are a structural feature of these markets. I wrote about Russia last month in – Russia – Will the Bear come in from the cold? My conclusion was that one should be cautiously optimistic:-

The Russian stock market has already factored in much of the positive economic and political news. The OPEC deal took shape in a series of well publicised stages. The “Trump Effect” is unlikely to be as significant as some commentators hope. The ending of sanctions is the one factor which could act as a positive price shock, however, the Russian economy has suffered a severe recession and now appears to be recovering of its own accord.

Interest rates in the US will rise, though probably not by as much, nor as quickly as the market is currently betting. A value based approach to stock selection offers greater protection and greater return in the long run.

The US stock market continues to rise. The US economy looks set to grow more rapidly in 2017 due to tax cuts and fiscal stimulus, but, for international companies which export to the US, the threat of protectionism is likely to temper enthusiasm for their stocks.

US financial services firms were a big winner after the Trump election result, they should continue to benefit even as interest rates increase – yield curves will steepen, increasing return on capital. US telecommunications stocks have a performed well since the election along with biotechnology – I have no specific view on these industries. Energy stocks have also rallied, perhaps as much on the OPEC deal as the Trump triumph – many new technologies are starting to be implemented by the energy industry but enthusiasm for these stocks may be tempered by a decline in oil prices once the rig count rebounds. The Baker-Hughes Rig Count ended the year at 525 up from a low of 316 in May. The old high of 1,609 was set back in October 2014 – there is plenty of spare capacity which will exert downward pressure on oil prices.

Indian economic growth will outpace China for another year. Despite a weakening Chinese Yuan, Vietnam remains competitive – it is on the cusp of moving from Frontier to Emerging Market status. Indonesia also looks likely to perform well during 2017, GDP forecasts are around 5%; however, Indonesia’s strong reliance on commodity exports makes it more vulnerable than some of its South and East Asian neighbours.

Macro Letter – No 45 – 06-11-2015

Have technological advances offset the reduction in capital allocated to financial markets trading?

Liquidity in financial markets means different things to different participants. A sharp increase in trading volume is no guarantee that liquidity will persist. Before buying (or selling) any financial instrument the first thing one should ask is “how easy will it be to liquidate my exposure?” This question was at the heart of a recent paper by the UK Government – The future of computer trading in financial markets – 2012 – here are some of the highlights:-

…The Project has found that some of the commonly held negative perceptions surrounding HFT are not supported by the available evidence and, indeed, that HFT may have modestly improved the functioning of markets in some respects. However, it is believed that policy makers are justified in being concerned about the possible effects of HFT on instability in financial markets.

There will be increasing availability of substantially cheaper computing power, particularly through cloud computing: those who embrace this technology will benefit from faster and more intelligent trading systems in particular.

Special purpose silicon chips will gain ground from conventional computers: the increased speed will provide an important competitive edge through better and faster simulation and analysis, and within transaction systems.

Computer-designed and computer-optimised robot traders could become more prevalent: in time, they could replace algorithms designed and refined by people, posing new challenges for understanding their effects on financial markets and for their regulation.

Opportunities will continue to open up for small and medium-sized firms offering ‘middleware’ technology components, driving further changes in market structure: such components can be purchased and plugged together to form trading systems which were previously the preserve of much larger institutions.

The extent to which different markets embrace new technology will critically affect their competitiveness and therefore their position globally: The new technologies mean that major trading systems can exist almost anywhere. Emerging economies may come to challenge the long-established historical dominance of major European and US cities as global hubs for financial markets if the former capitalise faster on the technologies and the opportunities presented.

The new technologies will continue to have profound implications for the workforce required to service markets, both in terms of numbers employed in specific jobs, and the skills required: Machines can increasingly undertake a range of jobs for less cost, with fewer errors and at much greater speed. As a result, for example, the number of traders engaged in on-the-spot execution of orders has fallen sharply in recent years, and is likely to continue to fall further in the future. However, the mix of human and robot traders is likely to continue for some time, although this will be affected by other important factors, such as future regulation.

Markets are already ‘socio-technical’ systems, combining human and robot participants. Understanding and managing these systems to prevent undesirable behaviour in both humans and robots will be key to ensuring effective regulation…

…While the effect of CBT (Computer Based Trading) on market quality is controversial, the evidence available to this Project suggests that CBT has several beneficial effects on markets, notably:

liquidity, as measured by bid-ask spreads and other metrics, has improved;

transaction costs have fallen for both retail and institutional traders, mostly due to changes in trading market structure, which are related closely to the development of HFT in particular;

market prices have become more efficient, consistent with the hypothesis that CBT links markets and thereby facilitates price discovery.

…While overall liquidity has improved, there appears to be greater potential for periodic illiquidity: The nature of market making has changed, with high frequency traders now providing the bulk of such activity in both futures and equities. However, unlike designated specialists, high frequency traders typically operate with little capital, hold small inventory positions and have no obligations to provide liquidity during periods of market stress. These factors, together with the ultra-fast speed of trading, create the potential for periodic illiquidity. The US Flash Crash and other more recent smaller events illustrate this increased potential for illiquidity.

…Three main mechanisms that may lead to instabilities and which involve CBT are:

nonlinear sensitivities to change, where small changes can have very large effects, not least through feedback loops;

incomplete information in CBT environments where some agents in the market have more, or more accurate, knowledge than others and where few events are common knowledge;

internal ‘endogenous’ risks based on feedback loops within the system.

The crux of the issue is whether market-makers have been replaced by traders. This trend is not new. On the LSE the transition occurred at “Big Bang” in October 1986. The LSE was catching up with the US deregulation which prompted the formation of NASDAQ in 1971.

Electronic trading, once permitted, soon eclipsed the open-outcry of futures pits and traditional practices of stock exchange floors. Transactions became cheaper, audit trails, more accurate and error incidence declined. Commission rates fell, bid/offer spreads narrowed, volumes increased, in an, almost, entirely virtuous circle.

The final development which was needed to insure liquidity, was the evolution of an efficient repurchase market for securities – sadly this market-place remains remarkably opaque. Nonetheless, the perceived need for designated market-makers, with an obligation to make a two-way price, has diminished. It has been replaced by proprietary trading firms, which forgo the privileges of the market-maker – principally lower fees or preferential access to supply – for the flexibility to abstain from providing liquidity at their own discretion.

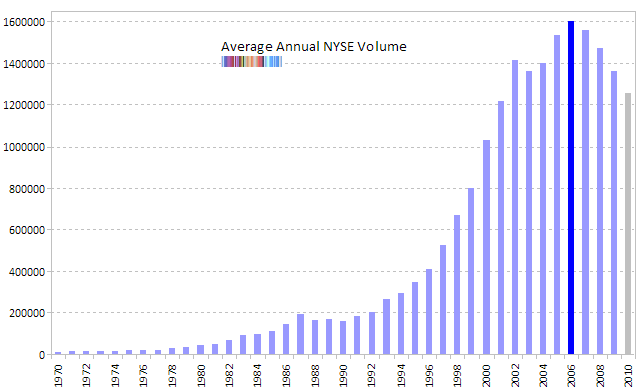

In the late 1990’s I remember a conversation with a partner at NYSE Specialist – Foster, Marks & Natoli – he had joined the firm in 1953 and sold his business to Spear, Leeds Kellogg in 1994. He told me that during his career he estimated the amount of capital relative to size of the trading portfolio had declined by a factor of five times.

Since the mid-1990’s stock market volumes have increased dramatically as the chart below shows:-

Source: NYSE

The recommendations of the UK Government report include:-

European authorities, working together, and with financial practitioners and academics, should assess (using evidence-based analysis) and introduce mechanisms for managing and modifying the potential adverse side-effects of CBT and HFT.

Coordination of regulatory measures between markets is important and needs to take place at two levels: Regulatory constraints involving CBT in particular need to be introduced in a coordinated manner across all markets where there are strong linkages.

Regulatory measures for market control must also be undertaken in a systematic global fashion to achieve in full the objectives they are directed at. A joint initiative from a European Office of Financial Research and the US Office of Financial Research (OFR), with the involvement of other international markets, could be one option for delivering such global coordination.

Legislators and regulators need to encourage good practice and behaviour in the finance and software engineering industries. This clearly involves the need to discourage behaviour in which increasingly risky situations are regarded as acceptable, particularly when failure does not appear as an immediate result.

Standards should play a larger role. Legislators and regulators should consider implementing accurate, high resolution, synchronised timestamps because this could act as a key enabling tool for analysis of financial markets. Clearly it could be useful to determine the extent to which common gateway technology standards could enable regulators and customers to connect to multiple markets more easily, making more effective market surveillance a possibility.

In the longer term, there is a strong case to learn lessons from other safety-critical industries, and to use these to inform the effective management of systemic risk in financial systems. For example, high-integrity engineering practices developed in the aerospace industry could be adopted to help create safer automated financial systems.

Making surveillance of financial markets easier…The development of software for automated forensic analysis of adverse/extreme market events would provide valuable assistance for regulators engaged in surveillance of markets. This would help to address the increasing difficulty that people have in investigating events

At no point do they suggest that all market participants – especially those with principal or spread risk – be required to increase their capital. This will always remain an option. An alternative solution, the reinstatement of designated market-makers with obligations and privileges, is also absent from the report – this may prove to be a mistake.

An example of technological emancipation

In this paper, Review of Development Finance – The impact of technological improvements on developing financial markets: The case of the Johannesburg Stock Exchange – Q3 – 2013 – the authors investigate how the adoption of the SETS trading platform transformed the volume traded on the JSE:-

The adoption of the SETS trading platform was supposed to represent a watershed moment in the history of the Johannesburg Stock Exchange. The JSE is more liquid after SETS. The JSE has nearly doubled its trading activity (volume), trading is cheaper, and there are more trades at JSE after SETS.

Overall, average daily returns are higher. We posit that this is mainly because the returns are increased to the levels demanded for the associated risk. With the new trading platform, it would also be expected that there would be improvements in market efficiency. Higher numbers of investors, more listed companies, faster trading and more trade (evidenced with trading activity and liquidity), all would imply more market efficiency. Contrary to our expectations, however, market-wide and individual-level stock returns are still somewhat predictable; this is a clear violation of market efficiency.

If market participants had been required to increase their capital in line with the increased volume, the transformation would have been far less dramatic. This is not to say that increased trading volume equates to increased risk. Technology has improved access, traders are able to liquidate positions more easily, most of the time, due to improved technology. At any point in the trading day they may hold the same open position size, but by turning over their positions more frequently they may be able to increase their return on capital (and risk) employed.

Federal Reserve concern

The Federal Reserve Bank of New York – Introduction to a series on Liquidity published eleven articles on different aspects of liquidity during the last three months, here are some of the highlights:-

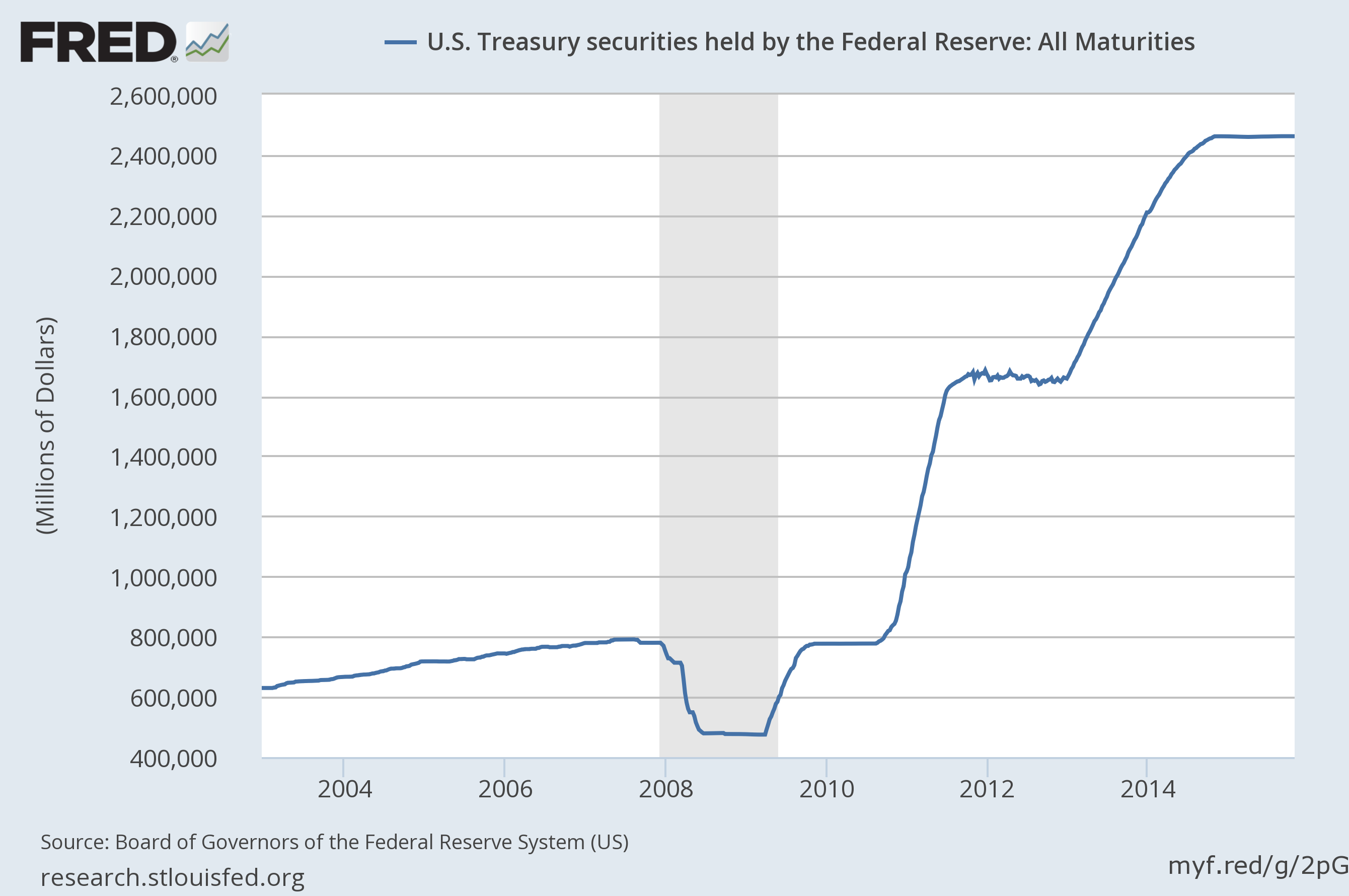

Has U.S. Treasury Market Liquidity Deteriorated? …it might be that liquidity concerns reflect anxiety about future liquidity conditions, with a possible imbalance between liquidity supply and demand. On the demand side, the share of Treasuries owned by mutual funds, which may demand daily liquidity, has increased. On the supply side, the primary dealers have pared their financing activities sharply since the crisis and shown no growth in their gross positions despite the sharp increase in Treasury debt outstanding.

This seems to ignore the effect of QE on the “free-float” of T-Bonds. The chart below shows the growth of the Federal Reserve holdings during the last decade:-

Source: St Louis Federal Reserve

Liquidity during Flash Events…all three events exhibited strained liquidity conditions during periods of extreme price volatility but the Treasury market event arguably exhibited a greater degree of price continuity, consistent with descriptions of the flash rally as “slow-moving.”

Unlike the FX and equity market, the US government still appoint primary dealers who have privileged access to the issuer. This probably explains much of the improved price continuity.

High-Frequency Cross-Market Trading in U.S. Treasury Markets. Cross-market trading by now accounts for a significant portion of trading in Treasury instruments in both the cash and futures markets. This reflects improvements in trading technology that allow for high-frequency trading within and across platforms. In particular, nearly simultaneous trading between the cash and futures platforms now accounts for up to 20 percent of cash market activity on many days. Market participants often presume that price discovery happens in Treasury futures. However, our findings show that this is not always the case: Although futures usually lead cash, the reverse is also often true. Therefore, from a price discovery point of view, the two markets can effectively be seen as one.

For many years the T-Bond future was regarded as the most liquid market and was therefore the preferred means of liquidation in times of stress. The most extreme example I have witnessed was in the German bond market during re-unification (1988). The Bund future was the most liquid market in which to lay off risk. As a result, Bund futures traded more than 10 bps cheap to cash and cash Bunds offered a yield premium of 13bps to bank Schuldschein – unsecured promissory notes.

The introduction of electronic trading in T-Bond cash markets has created competing pools of liquidity which should be additive in times of stress. The increasing use of Central Counter Party (CCP) clearing has allowed new market participants to operate with a smaller capital base.

This evolution has also been sweeping through the Interest Rate Swap market, reducing pressure on the T-Bond futures market further still.

The Evolution of Workups in the U.S. Treasury Securities Market. The workup is a unique feature of the interdealer cash Treasury market. Over time, the details of the workup have changed in response to changing market conditions, with the abandonment of the private phase and the shortening of the default duration to 3 seconds. While some market participants may consider it an anachronism, given the increased trading activity in benchmark Treasuries and the tight link to the extremely liquid Treasury futures market, the workup has not only remained an important feature of the interdealer market; it has actually grown in importance, now accounting for almost two-thirds of trading volume in the benchmark ten-year Treasury note.

On the Frankfurt stock exchange each Bund issue is “fixed” at around 13:00 daily. This process creates a liquidity concentration. A similar “clearing” process occurs at the end of LME rings. For spread traders, the ability to “lean” against a relatively un-volatile market – such as during a workup – whilst making an aggressive market in the correspondingly more volatile companion, represents an enhanced trading opportunity. One side of the potential spread price is provided “risk-free”.

What’s Driving Dealer Balance Sheet Stagnation? …The growing role of electronic trading has likely narrowed bid-ask spreads and reduced dealers’ profits from intermediating customer order flow, causing dealers to step back from making markets and reducing their need for large balance sheets. The changing competitive landscape of market making, as manifested by the entry of nondealer firms since the early 2000s, may therefore also play a role in the post-crisis dealer balance sheet dynamics. …The picture that emerges is that post-crisis dealer asset growth represents the confluence of several issues. Our findings suggest that business-cycle factors (the hangover from the housing boom and bust and subsequent risk aversion) and secular trends (electronification and competitive entry) should be considered alongside tighter regulation in explaining stagnating dealer balance sheets.

I refer back to my conversation with Mr Foster, the NYSE Specialist; in asset markets – equities and to a lesser extent bonds – as volume increases during a bull-market, the number of market participants increases. In this environment “liquidity providers” trade more frequently with the same capital base. Subsequently, as volatility declines – provided trading volume is maintained – these liquidity providers increase their trading size in order to maintain the same return on capital. When the bear-market arrives, the new participants, who arrived during the bull-market, liquidate. The remaining “liquidity providers” – those that haven’t exited the gene pool – are left passing the parcel among themselves as the return on capital declines precipitously (the chart, some way below, shows this evolution quite clearly).

Has U.S. Corporate Bond Market Liquidity Deteriorated? …price-based liquidity measures—bid-ask spreads and price impact—are very low by historical standards, indicating ample liquidity in corporate bond markets. This is a remarkable finding, given that dealer ownership of corporate bonds has declined markedly as dealers have shifted from a “principal” to an “agency” model of trading. These findings suggest a shift in market structure, in which liquidity provision is not exclusively provided by dealers but also by other market participants, including hedge funds and high-frequency-trading firms.

Given the “quest for yield” and the reduction in T-Bond supply due to QE, this shift in market structure is unsurprising, however the relatively illiquid nature of the Corporate bond repo market means much of the activity is based around “carry” returns. Participants are cognizant of the dangers of swift reversals of sentiment in carry trading.

Has Liquidity Risk in the Corporate Bond Market Increased? …We measure market liquidity risk by counting the frequency of large day-to-day increases in illiquidity and price volatility, where “large” is defined relative to measures of recent liquidity and volatility changes (details are described here). We refer to the illiquidity jumps as “liquidity risk” and to the volatility jumps as “vol-of-vol.” Counting the number of such jumps in an eighteen-month trailing window shows that liquidity risk and vol-of-vol have declined substantially from crisis levels…

…Current metrics indicate ample levels of liquidity in the corporate bond market, and liquidity risk in the corporate bond market seems to have actually declined in recent years. This is in contrast to liquidity risk in equity and Treasury markets…

The Fed methodology is contained in a four page paper A Note on Measuring Illiquidity Jumps. It may be of interest to those with an interest in exotic option pricing. I’m not convinced that I agree with their conclusions about Liquidity Risk – it is difficult to measure that which is unseen.

Has Liquidity Risk in the Treasury and Equity Markets Increased? …While current levels of liquidity appear similar to those observed before the crisis, sudden spikes in illiquidity—like the equity market flash crash of 2010, the recent equity market volatility on August 24, and the flash rally in Treasury yields on October 15, 2014—seem to have become more common. Such spikes in illiquidity tend to coincide with spikes in option-implied volatility, in both equity and Treasury markets…

…we refer to these liquidity jumps as “liquidity risk” and volatility jumps as “vol-of-vol.” Counting the number of such jumps in an eighteen-month trailing window reveals a recent uptick in liquidity risk and vol-of-vol, and confirms the link between them… The evidence that liquidity risk in equities and Treasuries is elevated contrasts with our earlier post, which found no such increase for corporate bonds.

…Our findings suggest a trade-off between liquidity levels and liquidity risk: while equity and Treasury markets have been highly liquid in recent years, liquidity risk appears elevated. This change has gone hand in hand with an apparent increase in the vol-of-vol of asset prices, so that illiquidity spikes seem to coincide with volatility spikes. Our findings further suggest that the increase in liquidity risk is more likely attributable to changes in market structure and competition than dealer balance sheet regulations, since the latter would also have caused corporate bond liquidity risk to rise. Moreover, evidence from option markets suggests that this seeming rise in liquidity risk is not reflected in the price of volatility.

Market liquidity in a given market is never constant, the trading volume may remain the same but the market participants, wholly different. In the 1980’s Japanese institutions were a significant influence on the US bond market, today it is the Federal Reserve. Changes, such as minimum price increments and exchange trading hours are significant; the list of factors is long and ever changing. The increase in Liquidity Risk has as much to do with the increase in systematic trading and the relative consistency of approach these traders take to risk management. These traders and their methods have become increasingly prevalent. Whilst cognizant of skewness they see the world through a Gaussian lense. They measure strategy success by Sharpe and Sortino ratio, assessing it by the minute or the hour and being “flat” by market close.

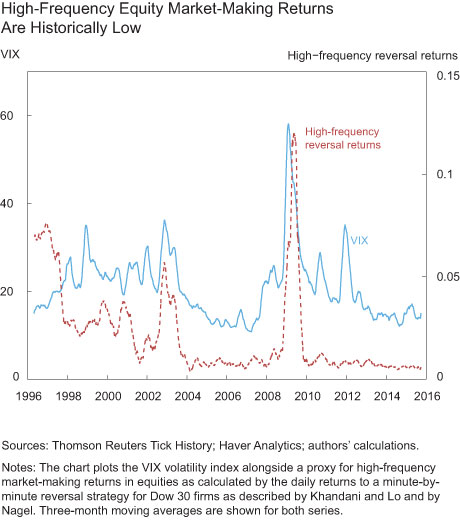

Changes in the Returns to Market Making. We show estimated returns to market making to be at historically low levels—a finding that seems inconsistent with market analysts’ argument that higher capital requirements have reduced market liquidity. The picture that emerges from our analysis is of a change in the risk-sharing arrangement among trading institutions. We uncover a compression in expected returns to market making in the corporate bond market, where dealers remain the predominant market makers, as well as the equity market, where dealers are less important. The compression of market making returns may be tied to competitive pressures, with high-frequency trading competition being important in the equity market.

Source: Reuters, Haver Analytics

The chart above looks at one minute reversals on the Dow. As long ago as 2003, the HFT customers I dealt with were operating on sub-second reversal time horizons. Nonetheless, the pattern of profitability may be broadly similar.

Redemption Risk of Bond Mutual Funds and Dealer Positioning. Mutual funds’ share of corporate bond ownership has increased sharply in recent years, while dealers’ share has declined substantially. Because mutual funds are subject to redemption risk, this shift in ownership patterns raises the concern that redemption risk might have increased. However, we find no evidence that the net flow volatility of bond funds has increased. Likewise, we uncover no evidence of contrarian behavior by dealers relative to bond fund flows. Therefore, even if we do observe large mutual fund redemptions in the future, our evidence does not suggest that reduced dealer positions will exacerbate the effects on corporate bond pricing and liquidity.

Since the Mutual Fund “Late Trading” scandal of 2003, arbitrage operators have maintained a low-profile. The “flight-to-quality” properties of T-Bonds should also mean mass-redemption is a much lower probability – “mass-subscription” is a higher risk.

The Liquidity Mirage. While low-latency cross-market trading has undoubtedly led to more consistent pricing of Treasury securities and derivatives, there is strong evidence that it has also resulted in a more complex and dynamic nature of market liquidity. Under the new market structure, it has arguably become more challenging for large investors to accurately assess available liquidity based on displayed market depth across venues. The striking cross-market patterns in trading and order book changes suggest that quote modifications/cancellations by high-frequency market makers rather than preemptive aggressive trading are an important contributing factor to the liquidity mirage phenomenon.

In the days of open-outcry trading on futures exchanges “local” traders would frequently cancel and replace bids and offers. These participants were visible, their reliability, or otherwise, was known to the market-place. In an electronic order book there is less transparency. Algorithmic trading solutions have developed, over the last twenty years, to enable efficient execution in this more opaque environment.

“Cost plus” pricing for equity and futures execution is still quite rare outside the HFT world but it has had a dramatic influence on stock market micro-structure and liquidity since the 1990’s.

In a recent speech by Minouche Shafik of the Bank of England – Dealing with change: Liquidity in evolving market structures – suggested that the changes in liquidity are a natural process:-

The reduction in the relative size of dealer balance sheets may also be a natural process of evolution as the market-making industry matures and emphasis is placed on using its warehousing capacity efficiently rather holding lots of inventory. Market making wouldn’t be the first industry to go through such a change: Just In Time management swept through manufacturing in the 70s and 80s with its focus on minimising waste, eliminating inventories, and quickly responding to changing market demand. More recently, supermarkets have reversed their once relentless expansion of retail space, and started moving away from inventory-intensive hypermarkets toward smaller retail units.

Indeed, moving toward smaller in-store inventories is not the only parallel between retailing and market making: both have also been dramatically changed by innovation. Just as the rise of internet shopping has given consumers access to a broader choice of shops and much easier means of price comparison, so has electronic trading facilitated new ways of matching buyers and sellers in financial markets, and added to the data generally available for price discovery.

The Deputy Governor goes on to remind us that the BoE acted as Market-Maker of Last Resort during the last crisis and would do so again.

Conclusion – Financial markets – for the benefit of whom

Financial markets evolve to allow investors to provide capital in exchange for a financial reward. Technology has increased the speed and reliability of market access whilst reducing the cost, however these benefits change the underlying structure of markets, be it co-location of servers in the last decade or block-chain technology in the next.

Politicians seek to encourage long-term investment; high frequency trading is a very short-term investment strategy indeed, but without short-term investors – shall we call them speculators – the ability to transfer of capital is severely impaired. Even the most jaundiced politician will admit, speculators are a necessary evil.

Innovation has democratized financial markets, it has enabled individual investors to create complex portfolios and implement strategies which were once the preserve of hedge funds and investment banks, however the experience has not been an unmitigated success, in the process it purportedly enabled one man from Hounslow to wipe $750bln off the value of the US stock market in May 2010. That this was possible defies credulity for many; I believe it indicates how technology has more than offset the decline in capital allocated to financial market trading, nonetheless, when it comes to financial market liquidity, I concur with Deputy Governor Shakif – “caveat emptor”.