Macro Letter – No 17 – 15-08-2014

The Spanish Renaissance

- Spanish government bond yields have fallen to the lowest since 1789

- Non-performing loans continue to increase

- The two main political parties have lost support due to austerity

Last month I spent two weeks visiting Catalunya, the North Eastern province of Spain which has Barcelona as it capital. The region contains 16% of Spain’s population and generates 19% of national GDP, according to this OECD report. As an economic region it remains the wealthiest in the country although it is fourth by per capita GDP. Its economic prowess is matched by it levels of debt – in 2012 it had the highest debt of any of the 17 autonomous regions of Spain. It remains one of the most industrialised regions of Spain having developed its industrial base in the second half of the 19th century. As traditional industry declined Barcelona led the industrial renaissance developing new businesses in biotechnology and design. It is a member of the “Four Motors of Europe” group which includes Rhone-Alps, Lombardy and Baden Wurttemberg.

Aside from the new industry the region has a large agricultural sector and a substantial tourist industry. Supporting these industries is an array of regional financial institutions including La Caixa – Europe’s largest savings bank and Spain third largest banking institution.

Bordering France and Andorra to the north there is strong political support for Catalan separatism or a federation of Spanish states.

Catalunya – land of contrasts

During my visit I spent time Blanes, a popular local Costa Brava resort, 60 miles north of Barcelona. This is just beyond the commuter belt but the tourist business appeared robust. Property prices are lower than in 2008 but this, predominantly Spanish, resort has gradually developed over several decades; over-supply does not seem to be the issue it is in areas such as the Costa del Sol. There was little evidence of new property development but the bars and restaurants were busy and the main shopping areas had a prosperous feel with new stores opening for the summer season.

From the east coast I drove west to Lleira which is the geographic centre of a large agricultural region irrigated by rivers which rise in the Pyrenees. The city was ravaged during the Spanish civil war but since the death of Franco (1975) it has witnessed a demographic revival as immigrants have arrived, predominantly from Andalusia. My journey then took me north to the Vall D’Aran. This district contains Spain’s premier ski resort, Baqueira-Beret. The town was originally developed in the 1970’s and 1980’s but has been significantly added to in the last decade. Property prices, while substantially lower than similar accommodation in the Alpes, are being offered at significant discounts. This reflects the dramatic increase in new properties, the limited skiing area, the less reliable snowfall and the domestic nature of the clientele – yet Toulouse airport is only a two hour drive. Aside from the tourist industry and farming the region produces a significant amount of hydro-electric power, according to data from 2001 Catalunya is the second largest producer in Spain – I couldn’t find more recent data, but generating capacity appears to have been fairly static for the past decade. Spain is ranked sixth in Europe for hydro-electric generation and hyrdo accounts for 12% of Spain’s installed generating capacity.

Catalunya – a surrogate for Spain

Despite high levels of debt, Catalunya is a dynamic economic region. The tourist industry remains strong. The agricultural sector is stable, benefitting from excellent road links to the rest of Spain and France to the north. The relative proximity to the Mediterranean seaboard enables export to a wider international market. It’s worth noting that Spanish exports are up 7% on 2013.

Newer industries in the Barcelona area benefit from a highly educated workforce and the attraction of a cosmopolitan city with a desirable climate. In some ways Catalunya resembles the Lombardy region of Italy, held back by its less successful provinces. However Spain’s Fascist regime retained control until 1975 and political stability was properly established only in October 1982 when the PSOE won the general election. During the period from 1939, and especially during the Francoist “Spanish Miracle” of the 1960’s, Spain was essentially a command economy. Those institutions which were supported by the state, thrived and became larger than their Italian counterparts. This structure makes Catalunya, and for that matter the rest of Spain, less quick to adapt.

I believe Catalunya can be viewed as a leading indicator of the direction in which the Spanish economy might travel if Spain embraces economic reform and addresses the problem of property related non-performing debt which continues to stymie their banking system.

Spain – The Economy

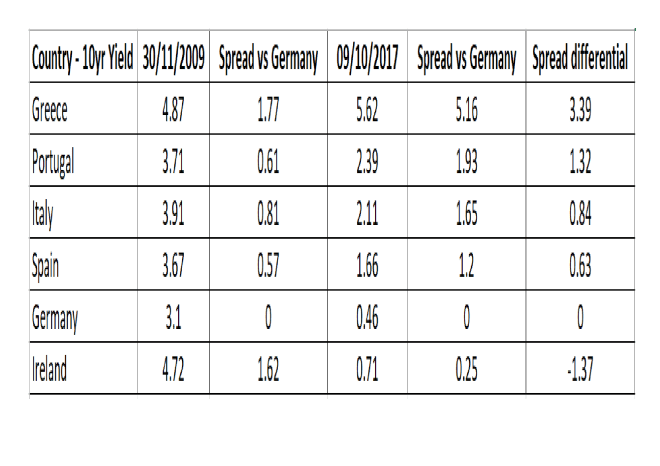

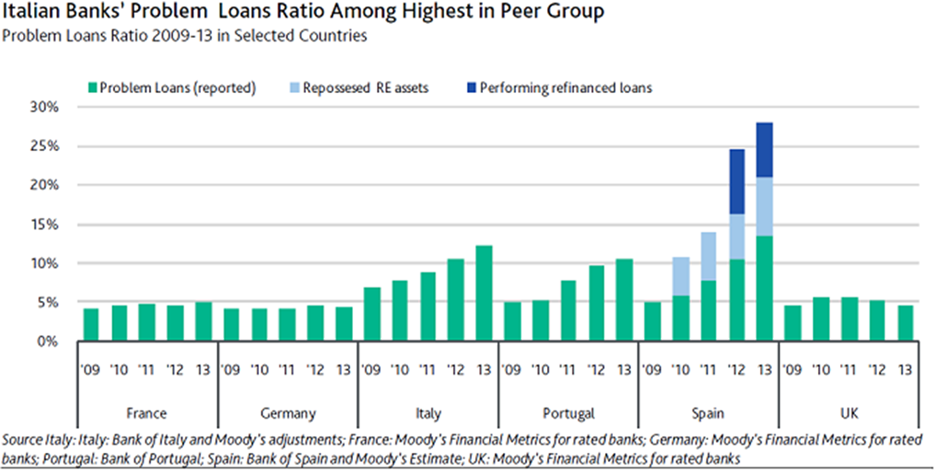

The table below comes from the American Enterprise Institute – the AEI are concerned about Italy and also Portugal where reported problem loans are rising. The same is true in Spain despite considerable efforts to refinance or repossess assets.

Source: AEI and Moody’s

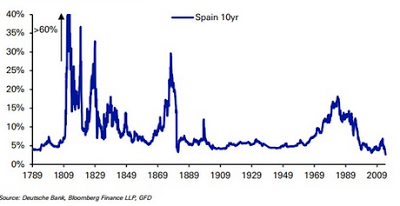

This doesn’t paint the picture of an economy in rude health. The level of non-performing loans continues to grow despite government bond yields which are at the lowest yields since 1789.

Source: Deutsche Bank and Bloomberg

The IMF 2014 Article IV – Staff Report on Spain, published in June, reflects some of the contradictions I observed during my visit, they go on to propose several policy recommendations, including a further bolstering of financial institutions at the expense of shareholders: –

Context. Spain has turned the corner. Growth has resumed, labor market trends are improving, the current account is in surplus, banks are healthier, and sovereign yields are at record lows. But unemployment is unacceptably high, incomes have fallen, trend productivity growth is low, and the deleveraging of high debt burdens—public and private—is weighing on growth.

Policies. Spain’s overarching policy priority must be to ensure the recovery is strong, long-lasting, and most pressingly, job-rich. This requires:

- Reducing the drag on domestic demand from private sector deleveraging with a more comprehensive, coordinated, approach to corporate debt restructuring, and by introducing a personal insolvency framework.

- Bolstering banks’ ability to support the recovery by continuing to raise capital levels over time, including by limiting cash dividends and bonuses.

- Creating jobs for the low skilled by sharply cutting the fiscal cost of employing them, compensated by higher indirect revenues.

- Making the labor market more inclusive and responsive to economic conditions by striking a better balance between highly-protected/permanent and precarious/temporary contracts, and further helping firms adapt working conditions (wages, hours) to their specific circumstances.

- Helping the unemployed improve their skills and enhancing the support they receive to find a job.

- Removing regulatory barriers that prevent firms from growing, hiring, and becoming more productive, especially at the regional level.

- Gradually, but steadily, reducing the fiscal deficit to keep debt on a sustainable path, and making the tax system more growth and job friendly.

- Policies by Spain’s European partners, in particular, sufficient monetary easing by the ECB to achieve its inflation targets.

For a closer look at the current state of the Spanish economy the Banco de Espana – Quarterly Report – July 2014 makes interesting reading. The central bank is broadly positive, here are some of the highlights: –

GDP is estimated to have increased at a quarter-on-quarter rate of 0.5% (compared with 0.4% in Q1). Following four consecutive quarters of quarterly increases in output, the year-on-year rate of change in GDP is expected to stand at 1.1% (0.5% in the previous quarter).

…the update of these projections points to GDP growth rates of 1.3% in 2014 and 2% in 2015, 0.1 pp and 0.3 pp up on those previously projected

…financial market conditions continued improving in Q2, underpinned by brighter economic expectations and the effect of the measures adopted by the ECB. There were further cuts in the yields on Spanish public debt and a narrowing in the related spread over the German benchmark (at the cut-off date for this report the risk premium stood at 151 bp, after having risen slightly in recent days). Yields and risk premia on fixed-income securities issued by the private sector also fell. Lastly, stock markets continued on a rising trend, meaning the IBEX-35 has posted gains of 1.3% since end-March (and of 5.6% since the start of the year). Against this background, bank lending interest rates fell slightly, but remain excessively high given the expansionary monetary policy stance.

Both external and financial factors contributed to bolstering the increase in spending by the non-financial private sector in Q2. Household consumption is estimated to have increased by 0.4% quarter-on-quarter, in line with the rate for the previous quarter, and on the back of improved confidence and the recovery in employment. In contrast, other determinants of consumption moved on a somewhat less positive path. In particular, on information to March, the decline in disposable income intensified, meaning that the saving ratio dropped sharply to 9.4% in cumulated four-quarter terms (compared with 10.4% the previous quarter). That is illustrative of the delicate financial situation from which households are addressing their spending decisions in the early stages of the recovery. The rise in household financial wealth perhaps marked a counterpoint to the weakness of disposable income, but it did not prevent the expansion in consumption from having to be made at the expense of the disposal of financial assets, according to information from the financial accounts.

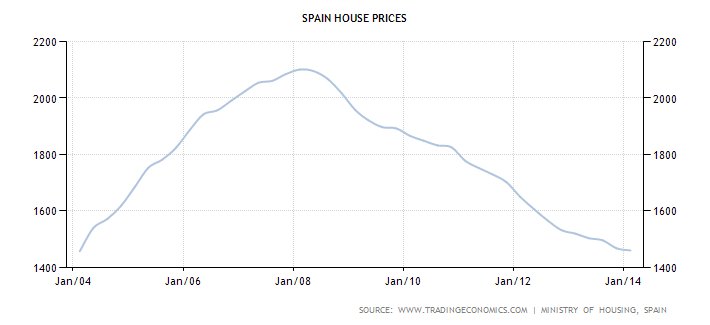

The contractionary profile of residential investment eased in Q2, posting an estimated quarter-on-quarter decline of 0.8% (a similar rate to Q1), in a setting in which the main real estate market indicators began to evidence a significance moderation in the adjustment of the sector. Housing transactions showed a degree of stabilisation, with notable momentum in purchases by foreigners, and the declining trend in the number of mortgages arranged was checked. The number of building permits ceased to move on a declining path, hovering in recent months at values slightly higher than their historical low. However, the absorption of the sizeable stock of unsold houses is advancing but slowly, which is hampering the start of the new construction cycle. Lastly, the pace of the year-on-year decline in house prices eased in 2014 Q1 to -3.8% according to Spanish Ministry of Development figures, placing the cumulative loss in the value of this asset since early 2008 at 31%, in nominal terms. This behaviour at the aggregate level was, however, compatible with price increases in certain regions.

As a result of the developments in household saving and investment, households’ net lending moved once more onto a declining course in Q1, following the pause observed in 2013, to stand at 1.9% of GDP in cumulated four-quarter terms. The pace of the contraction in financing extended to households slackened slightly in Q2, posting a year-on-year rate of change of -4.6% in May (-4.8% in March

In the corporate arena, productive investment is expected to have risen in Q2, as the sustained recovery in investment in capital goods discernible since 2013 Q1 has been accompanied by the more favourable behaviour of investment in non-residential construction, following its fall the previous quarter. Overall, the improvement in the business climate, along with the favourable trend in foreign orders and the recovery in domestic demand, accounts for this acceleration in business expenditure. According to the non-financial accounts of the institutional sectors for Q1, the increase in investment was accompanied by a break in the rising course of non-financial corporations’ saving, leading to a slight reduction in their net lending, which stood at 4% of GDP in cumulated four-quarter terms, 0.3 pp down on end-2013. On information updated to May, the pace of the decline in total funds obtained by non-financial corporations lessened by 0.6 pp compared with March to a rate of 5%.

Spain has a more flexible labour market than many of its EZ neighbours, although, as the IMF state, this situation could be further improved. The crisis affected workers more quickly than institutions. Unemployment rose dramatically and wages, for those still in employment, remains under pressure as a result: –

Source: Trading Economics, Spanish Ministry of Finance

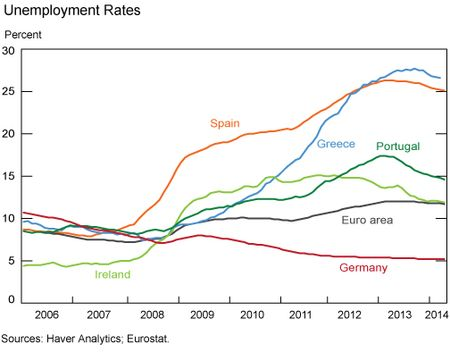

Unemployment remains stubbornly high but historically Spain has had a large “informal” economy which is not captured by official statistics. The first chart looks at the recent evolution of the unemployment across the EU and the second looks at the longer run pattern specific to Spain: –

Source: NY Fed, Haver Analytics, Eurostat

Source: Trading Economics, National Statistics Institute – Spain

On the bright side, Spain is now toying with deflation as this, tongue in cheek, table from Charles Butler – Ibex Salad illustrates: –

| CPI Category |

Oct CPI |

Rationale for delaying spending in anticipation of lower prices |

| Electronics |

-8.1 |

I’m lining up at the Apple Store waiting for lower prices. |

| Communications |

-7.5 |

Let’s talk next month. It’ll be cheaper. |

| Vehicles |

-3.3 |

This one’s got potential (too bad sales are up 34% YoY) |

| Vehicle parts & repairs |

-2.3 |

Spreadsheet > calculate fuel savings on 3 cylinders vs cost of repair. |

| Electricity |

-2 |

Watch this week’s Walking Dead…. next week. |

| Household Appliances |

-1.7 |

No problem. I like sushi. |

| Hospital services |

-1.2 |

They’re offering a special on biopsies in August. |

| Personal articles |

-1.2 |

In the meantime, just tear up a few rags. |

| Household textiles |

-1.1 |

(see previous) |

| Sports & recreation goods |

-0.9 |

Trending > air football |

| Home rent |

-0.5 |

If we don’t pay, the landlord’ll charge us less next month. |

| Home repairs |

-0.4 |

Leak? No problem. Cut the mains. |

| Sports & recreation services |

-0.4 |

I’ll exercise twice as much next month (multipurpose rationalization). |

| Hotels |

-0.2 |

I love Benidorm in January. |

| Personal goods & services |

-0.1 |

Let hair grow.Call myself an indignao.(Won’t work for Luís de Guindos.) |

| Medicines |

0 |

I’ll hedge my insulin habit with a Viagra short. |

| Financial services |

0 |

Cash is king, anyway. |

Source: Ibex Salad

Which brings us back to house prices; six years after the financial crisis, prices are back to the level of 2004.

Source: Trading Economics, Spanish Ministry of Housing

Whilst the environment was different in the UK in the late 1980’s the chart below is an indication of the time it can take for housing prices to recover. In the UK interest rates rose and then declined sharply making mortgages significantly more affordable. Spain has seen interest rates fall already, a rise from these levels might prolong the agony: –

Source: Trading Economics and HBOS

With Spanish bond yields at record lows the fear of higher rates is a disincentive investment. The debt overhang and rising level of non-performing loans will continue to undermine any lasting recovery. Since the financial crisis many Spanish nationals have emigrated in search of work. At the same time the rising trend of non-Spanish immigration has reversed. During the boom years Spain’s population was swelled by an influx of nearly six million immigrants – with unemployment at nearly 25% they are no longer arriving. In the longer term, like many other European countries, Spain has to deal with an ageing population. The IMF Spain – selected issues document published last month noted: –

Demographics have turned negative. After expanding at a fast pace until 2007, population growth slowed significantly and turned negative in 2012. This is likely to be a new trend, as INE projects working-age population to continue to decline over the next years.

…Labor dynamics will make a much weaker contribution to potential output. Demographics will be a drag on growth due to declining working-age population (emigration and ageing). The Spanish statistical agency (INE) expects working-age population to fall by 1 percent a year over the medium term.

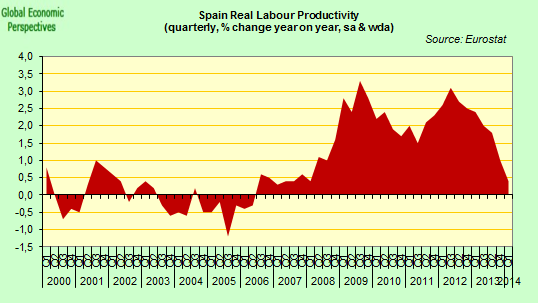

Another issue of concern is productivity. The productivity gains derived from the recession have reversed as this chart shows: –

Source: Eurostat

To some extent these TFP gains are illusory since the fall in employment has been bourne by the least productive employees. As the economy recovers these workers will find new employment and TFP will decline.

Politics and Institutional Reform

What wasn’t discussed by the IMF or the BdE is the changing political landscape. In the recent European Elections the two main parties which have governed Spain since 1982 saw a significant decline in support. Historically they have garnered 70% of the vote, in theses elections they captured only 49%.

Edward Hugh – Spanish Economy Watch captures the mood: –

What people are missing about Spain is the way the credibility of the institutional structure is weakening. Voices talking about a constitutional crisis are growing. The economic crisis basically coincided with the moment when the set up established – including the return of the monarchy – during the transition from Franco’s dictatorship to democracy was increasingly seen as having “run its course”. Many observers recognise that major constitutional reform is needed and some kind of “rebirth” and renovation in the political system. Last months EU elections were the latest warning signal. The two main political parties (the so called institutional parties) for the first time since the transition failed to get over 50% of the popular vote between them, while the Syriza-like Podemos – who hadn’t even been listed in the opinion surveys – surged from nowhere to take 5 seats and 9% of the vote. And in Catalonia a large majority of voters voted for parties who are actively campaigning for independence from Spain. A general election is coming next year, but it is hard to see either of the “old” parties getting a majority without a complex set of coalition partners.

With respect to the politics of Catalunya, the rivals to the main Spanish parties are in favour of a range of measurers ranging from Separatist to Federalist .

A further sign of the need for reform is the significant decline in the popularity of the Spanish Royal family. Juan-Carlos abdicated in favour of his son earlier this year amid a corruption scandal. Six years after the financial crisis Spain is still in need of a Renaissance.

Conclusion and market implications

Unlike several other EZ countries, Spain is likely to see a continued pick-up in economic growth. This may be tempered by economic slow-down in their main export markets Italy (7.7%) Germany (10%) and France (15%): the French Finance Ministry halved their GDP forecast to +0.5% this week. The principal drag on the economy still emanates from the housing market bust and the problem of non-performing loans. In the longer run, institutional reform is needed to head-off the demographic effect of a shrinking working age population. In the past this has been achieved through immigration but the long term solution is to concentrate on productivity growth through investment in education and other policies.

For investors there is an opportunity to acquire dynamic companies especially in new industries such as biotechnology – for those investors looking for company specific information Biotech Spain is a useful resource – however, financial institutions – 42% of the IBEX35 index – remain vulnerable due to the debt overhang. The IBEX 35 and the Italian MIB index have moved in tandem since the initial recovery in 2010 but the prospects for Spanish growth are better over the next couple of years. Last month the Banca D’Italia revised their GDP forecast for 2014 down to 0.2% and for 2015 to 1.3%. My preference is to take a relative value approach to Spanish stocks given the slow-down in EZ growth.

Spanish 10 year government bonds offer little value at 2.5% although they may remain around these levels from a significant time. Yields have fallen from 7.74% in July 2012 to 2.45% last month. During the same period German 10 yr Bunds (Europe’s “Risk-Free” asset) have ranged between 2.05% (September 2013) and 1.02% this month. The record low yield on Bunds is a response to general concern about EZ growth – Germany’s ZEW Indicator of Economic Sentiment showed it seventh monthly decline in July although it is still above its long run average. France also looks vulnerable as witnessed by a new high of 3.398mln unemployed in June and Q2 GDP at zero.

Spanish Real-Estate is down 31% since the crisis according to the BdE. Inevitably, property is always about location and there are some opportunities which look tempting, especially in areas where foreign buyers are active, but with non-performing loan rates still rising. I don’t envisage a broad based recovery for some while.