Macro Letter – No 62 – 30-09-2016

China – Coal, Steel, Water and Demographics – Which way now?

- The price of coking coal has risen 164% this year, doubling since July

- The NDRC is still attempting to reduce both coal and steel production this year

- The April stimulus package has boosted construction and infrastructure demand

- The pace of Chinese growth has stabilised but at a much reduced level

This year several commodity markets saw significant price increases. I discussed this in Macro Letter – No 51 – 11-3-2016 – How do we square the decline in trade with the rebound in industrial commodities?

The price of Iron Ore, Aluminium and other industrial metals has rallied sharply over the last few weeks – WTI now seems to have followed suit. Most commentators regard this as a short covering rally.

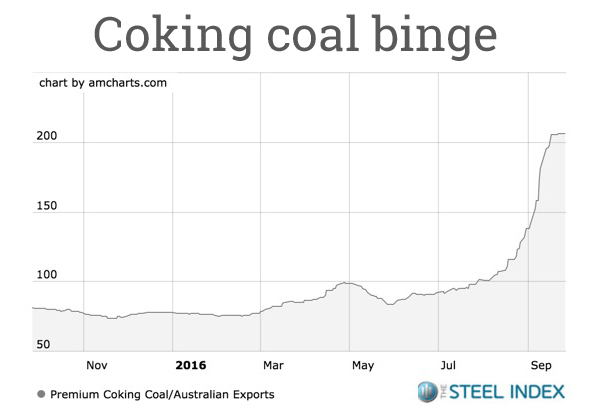

Over the last six months the US economy has maintaining momentum, albeit at a disappointingly modest pace. Elsewhere the economic headwinds are blowing harder, with Europe and Japan still mired in a “slow-growth/no-growth” environment. Yet during the last few weeks the spot price of premium coking coal – one of the key inputs for steel production – has doubled to more than $200/tonne. Although this is from multi-year lows seen in 2015, coking coal is now the top performing commodity market year to date:-

Source: Steel Index, Amcharts.com

According to CME data, the futures curve for Australian Coking Coal is in steep backwardation out to December 2017 delivery. This suggests a short-term supply shortage rather than a generalised increase in demand. Mining.com – Stunning coking coal rally wreaks havoc in steel, iron ore explains what has been happening:-

The rise in the price of coking is upending the economics of the iron ore and steel markets with the Australian export benchmark price climbing 164% so far this year.

Metallurgical coal was exchanging hands at $206.40 on Monday according to data provided by Steel Index as it consolidates at higher levels following weeks of panic buying not seen since 2011, when floods in key export region in Queensland sent the price surging to $335 a tonne (albeit not for long).

The rally was triggered by Beijing’s decision to limit coal mines’ operating days to 276 or fewer a year from 330 before as it seeks to restructure the industry. Safety closures and weather related supply curbs in China and Australia only added fuel to the fire.

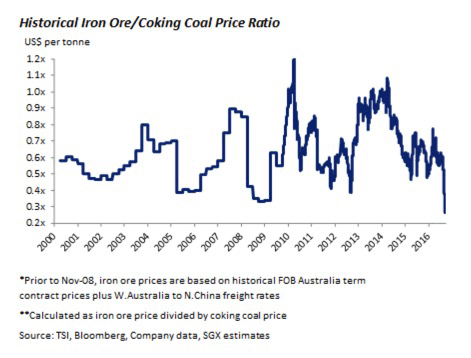

Source: TSI, Bloomberg, SGX

The price of Iron Ore has also risen by 31% to around $55/tonne, but, as the chart above makes clear, the ratio between the price of iron ore and coking coal is now at its lowest this century.

China’s coking coal output has fallen more than 10% due to the government edict to curtail domestic production. In response import volumes rose 45% in August alone. Goldman Sachs and Macquarie have both increased their price forecasts for 2017 and 2018.

The National Development and Reform Commission (NDRC) – the agency responsible for implementing production cuts – had achieved only 39% of the annual target for reducing coal capacity and 47% of the annual reduction in steel capacity as of the end of July. The Peterson – Institute – State of Play in the Chinese Steel Industry explains the reasons for this policy. Suffice to say, China’s domestic steel production tripled between 2005 and 2015 taking its share of global steel production from 31% to 50%. Under WTO rules it will have Market Economy Status from December 2016 – a wave of anti-dumping laws suits may well follow unless it curtails production.

Despite common knowledge of official policy, commentators have suggested that the recent production cut was intended to deliberately squeeze coal prices, allowing heavily indebted coal producers to repay loans to domestic Chinese banks. After two meetings between the China Iron and Steel Association and the NDRC, coal producers will now be allowed to produce an additional 50 tonne/day from October to alleviate shortages.

The steel industry was under margin pressure even before the rise in coal prices – the government has been forcing an industry wide consolidation. The high price of coal accelerates this “oligopolisation” of the sector. It is part of a broader reform and consolidation of State Owned Enterprises (SOEs). The Peterson Institute – China’s SOE Reform—The Wrong Path takes issue with this policy. It has its attractions in the short-term nonetheless – consolidation reduces competition within industries, the pricing power of these consolidated “oligopolies” should rise, enabling them to increase profitability and reduce their indebtedness. President Xi has called for “Stronger, bigger, better” state-owned enterprises. I fear for the squeezed private sector in this environment.

A more important structural reform was announced last month when the Supreme People’s Court ordered the establishment of more special divisions to handle liquidation and bankruptcy cases in intermediate courts. China has an undeveloped bankruptcy code – defaulting borrowers linger, acting as a drag on the economy. At the G20 summit President Xi said, “China has taken the most robust and solid measures in cutting excess capacity and we will honour our commitment with actions”. An efficient method of “zombie corporation liquidation” would expedite this process.

Another explanation for the government’s decision to reduce the number working days at coal mines is its commitment to reducing pollution. Brookings – The end of coal-fired growth in China looks at the bigger picture:-

China’s coal consumption grew from 1.36 billion tons per year in 2000 to 4.24 billion tons per year in 2013, an annual growth rate of 12 percent. As of 2015, the country accounts for approximately 50 percent of global demand for coal. In other words, China’s economic miracle was fueled primarily by coal.

…China’s coal consumption decreased by 2.9 percent in 2014 and 3.6 percent in 2015, and the economy has maintained a moderate speed of growth. This indicates that there is a decoupling of economic growth from the growth in coal consumption. China’s coal consumption might have in fact already peaked.

Over the past 35 years, coal powered the engine of China’s rapidly developing economy. Coal represented 75 percent of overall energy consumption. This number decreased to 64.4 percent in 2015—the lowest in China’s modern history—as the country’s energy intensity decreased by 65 percent relative to 35 years ago. In fact, though rarely noticed until the recent peak, this has been part of a fundamental shift in the Chinese economy’s relationship with coal.

The authors present three arguments to support their view that China’s reliance on coal is in structural decline. Firstly, a decrease in manufacturing and construction, which have seen over-investment during the last decade or more. Second, policies on climate change and air pollution—especially the Paris Agreement’s, signed this month, which calls for a 20% clean energy target by 2030. Read China-United States Exchange Foundation – After the Paris Climate Agreement, What’s Next? for more details. Finally, China’s adoption of technological innovation in energy, communications, and manufacturing.

In his G20 speech President Xi said “…green mountains and clear water are as good as mountains of gold and silver”. The problem of clean water is probably the single greatest resource challenge facing China today as this article from CEAC – China that once thrived on water, faces water problems today points out:-

The total amount of water resources in China is so huge as to reach 2325.85 billion cubic meters, which is the 4th largest in the world. However, Chinese population is so large that the per capita amount of water resources is only 1730.4 cubic meters. This is extremely small in the world. Moreover, water resources are distributed unevenly by the region. Generally speaking, water is scarce in northern parts of China, including the Northeast, the North, and the Northwest regions. Beijing is in the North region. On the other hand, water is abundant in the South Central, the South, and the Southwest regions. The problem is that water is growing scarcer, while its consumption is rising. Particularly, people in Northwest China suffer from chronic shortage of water.

…It is not the quantity of water that matters critically in China. The quality of water is deteriorating rapidly. According to “The Monthly Report of Ground Water” which was released by the Ministry of Water Resources of China this January, they conducted water quality observation researches of 2,103 wells in the Songliao plain of the Northeast region and the Jianghan plain in an inland area last year, and it turned out that 80% of ground water is too severely contaminated to drink. Ground water pollution is serious, particularly in the regions of water scarcity.

In the shorter-term there has been some increase in demand. Steel usage has risen in response to the mini-stimulus package implemented in April. It was aimed largely at railway and housing construction. Electricity demand picked up again in May +2.1% from April +1.9%, fuelling an increase in demand for thermal coal. Other leading indicators, also suggest that the slowdown in Chinese growth may have run its course. There has been an increase in railway freight volumes and pickup in copper output:-

Source: Market Realist, National Bureau of Statistics

Outside China the picture looks mixed. LME stocks of Copper and Zinc have recovered but Nickle and Aluminium stocks remain depleted. Global demand still appears to be subdued.

Chinese economy is unlikely to return to the double digit growth rates seen prior to the great recession, but, despite its indebtedness, the world’s largest command economy may be able to avoid an imminent banking crisis.

The Debt to GDP ratio continues to rise. A source of grave concern which is noted in the BIS Quarterly Review, September 2016. At the end of July total Chinese debt reached $28trln – greater than the government debt of the US and Japan combined. Corporate debt, which is fortunately denominated primarily in local currency, now stands at 171% of GDP whilst total debt stands at 255%. A favourite BIS measure is the Credit to GDP gap. A figure above 10 is a warning signal that an economy may be approaching a “Minsky Moment” – China scores 30.1, the highest of any large economy.

China has also continued to reduce its vast foreign exchange reserves, although at a more moderate pace than in 2014 and 2015. In July it reduced its holding of US Treasuries by $22bln – the largest one month decline in three years. It also released information about its gold holdings which, as many market participants had predicted, have risen substantially – it last reported this information in 2009. The US Bond sales may, therefore, have been to insure the stability of the RMB versus the US$ ahead of the G20 summit which was hosted by China this month.

Should we be concerned about a Chinese banking crisis? According to Michael Pettis – China Financial Markets – Does it matter if China cleans up its banks? banking solvency is not the issue, but the indebtedness of the economy is:-

The only “solution” to excessive debt within the economy is to allocate the costs of that debt, and not to transfer it from one entity to another.

The recapitalization of the banks is nice, in other words, but it is hardly necessary if we believe, and most of us do, that the banks are effectively guaranteed by the local governments and ultimately the central government, and that depositors have a limited ability to withdraw their deposits from the banking system. “Cleaning up the banks” is what you need to do when lending incentives are driven primarily by market considerations, because significant amounts of bad loans substantially change the way banks operate, and almost always to the detriment of the real economy.

…If we change our very conservative assumptions so that debt is equal to 280% of GDP, and is growing at 20% annually, and that debt-servicing capacity is growing at half the rate of GDP (3.0-3.5%, which I think is probably still too high), then for China to reach the point at which debt-servicing costs rise in line with debt-servicing capacity, Beijing’s reforms must deliver an improvement in productivity that either:

Causes each unit of new debt to generate 18 times as much GDP growth as it is doing now, or

Causes all assets backed by the total stock of debt (280% of GDP) to generate 50% more GDP growth than they do now.

Pettis remains pessimistic about China’s ability to grow its way out of debt. History is certainly on his side in this respect, however, policies such as the One Belt One Road Initiative, which aims to improve cross-border infrastructure in order to reduce transportation costs between China and its trading partners, still makes sense at this stage of China’s development. Comparisons have been made with the US Marshall Plan which helped to regenerate Europe after WWII but with an indicated aim of financing $4trln of new projects, its scale is much larger. Chatham House – Westward ho—the China dream and ‘one belt, one road’: Chinese foreign policy under Xi Jinping reviews the policy in detail, as does Peterson Institute – China’s Belt and Road Initiative.

Meanwhile, the great rebalancing towards domestic consumption continues, at what, in other countries, would be considered break-neck speed. This may, nonetheless, be too slow for China – the mini-stimulus package, in April, was a clear political capitulation. The Kansas City Federal Reserve – Consumer Spending in China: The Past and the Future looks at the success of rebalancing to date and the prospects going forward. They point out that Chinese consumption as a share of GDP declined between 1970 and 2000 largely as a result of demographic forces – low birth rate and aging population – together with urbanisation. Post 2000 rapid house price appreciation accelerated this trend. Since 2010 consumption has begun to rise from a low point of 37% of GDP, this coincides with the peak in household savings at 42% – it is now around 38.5%. The authors predict:-

In a benchmark scenario of relatively stable income growth and a further modest decline in the household saving rate, consumption growth in China remains at around 9 percent per year over the next five years, causing the share of Chinese consumption in GDP to increase by about 5 percentage points to 44 percent by 2020. This scenario has two implications. First, it suggests that strong consumption growth is sustainable in the near future, allowing China to continue transitioning toward a consumption-driven economy. Second, it suggests that strength in near-term Chinese consumption growth will partly rely on a further decline in the household saving rate. As the household saving rate cannot decline indefinitely, consumption growth may need to rely more heavily on household income to be sustainable in the long run.

Parallels have been made with Japan where the savings rate has declined from 40% to 19% of GDP since 1970. If China follows this pattern, savings as a percentage of income will continue to decline. The transition could be relatively smooth provided the residential property market does not collapse in the interim. The FRBKC article concludes:-

The declining saving rate in China reflects both a changing demographic structure—an expected increase in the young dependency ratio after multiple decades of decline—and a changing consumption pattern of young people, who face less pressure to save thanks to financial support from their parents and grandparents.

In the long run, transitioning to a consumption-driven economy may require some policy changes. Specifically, China may need to implement successful supply-side reforms—which are on the government’s agenda but haven’t yet been significantly pushed forward—to enable domestic production to meet rising domestic demand. Although the Chinese household saving rate is declining from a very high level, the downward trend cannot last forever. A truly consumption-driven economy must rely on strong household income growth, which is ultimately driven by improved technology and investment.

In the long run, demographic forces will affect China more than any other factor. According to the Ministry of Human Resources China’s working population hit a record 774.5mln in 2015, however, the UN estimate China will have 212mln fewer workers by 2050. The UN Demographic Profile is found on page 189.

Market impact and investment opportunities

Next week the RMB will be included in the SDR – the Peterson Institute – China’s Renminbi Is about to Break the Financial Glass Ceiling discusses this in more detail. There is widespread speculation that the PBoC will widen the RMB currency bands at any moment. In other respects the PBoC is in a more difficult position. The RMB has already weakened by 5% against the US$ this year. Cutting interest rates would probably cause the currency to weaken further, riling the US voters ahead of the election. They are not impotent, however, and injected a record RMB 310bln into the money market in August – part of an overt policy to support the official banking sector, diminishing the influence of shadow banks.

Domestic investors have favoured bonds over equities for the past couple of months, while the spread between corporate bonds and government bonds has narrowed. Chinese 10yr government bond yields have fallen around 50bp this year, but official policy, encouraging investors to purchase higher yielding bonds and reduce their exposure to leveraged wealth management products and other non-standard assets, is boosting demand for corporate issues.

Retail investors, who were badly burnt in the stock market collapse of 2015, remain obsessed with the property market despite massive over-supply. Equity broker margin balances remain low. Institutional portfolio managers have reduced exposure to stocks from 62% in July to 49% this month. In the post-crash environment IPO issuance has been subdued with only RMB 955bln of capital raised in the seven months to July. This compares to RMB 1.55trln in 2015. The final quarter may see better sentiment. Stocks may get a boost from local government spending in Q3 and Q4 – if only to insure their budgets are not reduced next year. The table below, from Star Capital, ranks forty of the world’s major stock markets. Using their metrics, China is second cheapest and has the lowest PE, Price to Cash flow and Price to Book:-

| Country | CAPE | PE | PC | PB | PS | DY | Rank |

| Russia | 4.9 | 7.5 | 3.6 | 0.8 | 0.8 | 4.10% | 1 |

| China | 12.4 | 6.1 | 3.2 | 0.8 | 0.6 | 4.70% | 2 |

| Brazil | 8.5 | 44.1 | 6.6 | 1.4 | 1.1 | 3.40% | 3 |

| South Korea | 12.6 | 11 | 5.5 | 1 | 0.6 | 1.80% | 5 |

| Hungary | 9.9 | ? | 5.1 | 1.2 | 0.6 | 2.80% | 6 |

| Czech | 8.7 | 11.8 | 5.5 | 1.2 | 1 | 7.50% | 8 |

| Turkey | 9.7 | 10.8 | 6.2 | 1.3 | 0.9 | 2.70% | 9 |

Source: Starcapital.de

The Shanghai Composite Index (SHCOMP) is down 8.85% YTD and by 41.84% since its high in June 2015, however it is up 48.25% from June 2014. Russia’s RTS Index by contrast is up 72.81% from its December 2014 low but still 29.68% below its level of June 2014.

Looking outside China, several Australia-centric mining stocks have already risen on the back of the move in coking coal but it seems unlikely that the supply imbalance will prove protracted. Anglo American (AAL) is still looking to sell more of its Australian coal mines – they may well find Chinese buyers.

Outside of China, infrastructure investment across Asia Pacific is on the rise, which is supportive for industrial commodities in general. KPMG – 10 emerging trends in 2016, published in January, takes a very optimistic long term view:-

Ultimately, however, we believe that this may well be the tipping point that ushers in 50 years (or more) of prosperity as capital starts to match up with projects which, in turn, will drive economic growth in the developing world and shore up retirement savings in the mature markets.

Commodity markets tend to exhibit very individual characteristics, however, several industrial and agricultural commodities have formed a longer term base this year. Is this the beginning of the next commodity super-cycle? It’s too soon to call, but without a rise in global demand the prospects for substantial gains are likely to be limited – Indian GDP growth is slowing. The IMF WEO July update revised its India GDP forecast for 2016 to 7.4% from 7.5% – in 2015 it was 7.6%. Its China forecast was revised up 0.1% and its overall Emerging Market and Developing Economy forecast for 2016 and 2017 was unchanged at 4.1% and 4.6%, although, world economic growth was revised 0.1% lower.

China’s stock market remains cheap by many metrics, but the level of indebtedness is an impediment to economic growth. The property market, although over-supplied, continues to attract investment, but this is economically unproductive in the long run. Government policy is attempting to steer the economy towards higher domestic consumption and technologically driven, productivity enhancing, investments. Environmental issues are finally being addressed, yet the challenge of clean water remains substantial.

Near term, debt reduction – and it has yet to begin – will hamper growth, which will, in turn, reduce the attractiveness of Chinese stocks. Reform of the SOEs will involve consolidation into a smaller number of vast enterprises. Private enterprises will suffer. “Zombie” companies will start to be dealt with as bankruptcy procedures become standardised, but, as with all policy in China, a gradualist approach is likely to be implemented. Commodity markets may continue to rise due to supply side factors but I doubt that Chinese demand will rebound even to the level of 2013/2014, let alone the early part of the century.