The Pension Fund Apocalypse

This is the first of two articles about negative real interest rates.

https://www.aier.org/article/pension-fund-apocalypse

This is the first of two articles about negative real interest rates.

https://www.aier.org/article/pension-fund-apocalypse

![]()

Macro Letter – No 117 – 28-06-2019

Interest Rates, Global Value Chains and Bank Reserve Requirements

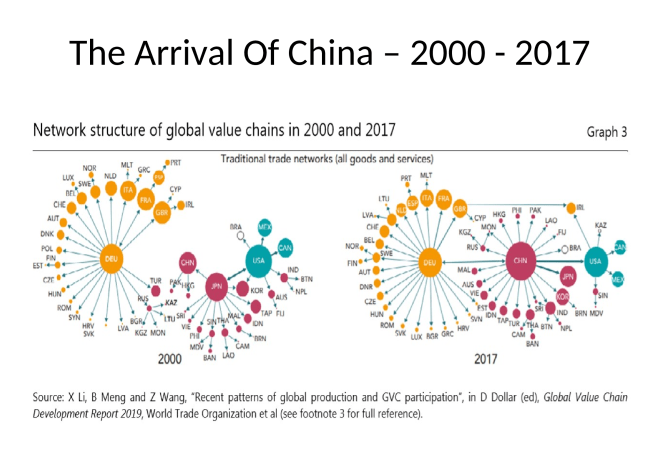

In a recent speech, Hyun Song Shin, Head of Research at the BIS, discussed – What is behind the recent slowdown? The speech focused on the weakening of global value chains (GVC’s) in manufactured goods. The manufacturing sector is critical, since it accounts for 70% of global merchandise trade: –

During the heyday of globalisation in the late 1980s and 1990s, trade grew at twice the pace of GDP. In turn, trade growth in manufactured goods was driven by the growing importance of multinational firms and the development of GVCs that knit together the production activity of firms around the world.

The chart below reveals the transformation of the world economy over the past 17 years: –

Source: BIS, X Li, B Meng and Z Wang, “Recent patterns of global production and GVC participation”, in D Dollar (ed), Global Value Chain Development Report 2019, World Trade Organization et al.

Hyun’s next chart tracks the sharp reversal in the relationship between world trade and GDP growth as a result of the Great Financial Crisis (GFC): –

Sources: IMF, World Economic Outlook; World Trade Organization; Datastream; national data; BIS calculations

The important point, highlighted by Hyun, is that the retrenchment in trade occurred almost a decade before the trade war began. China, growing at 6% plus, has captured an increasing share of global trade at the expense of the developed nations, most notably the US. Europe went through a similar transition during the second half of the 19th century, as the US transformed from an agrarian to an industrial society.

Returning to the present, supporting GVCs is capital intensive. Historically low interest rates have allowed these chains to flourish, but the recent reversal of interest rate policy by the Federal Reserve has caused structural cracks to emerge in the edifice. The BIS describes the situation for multi-national manufacturing firms in this way (the emphasis is mine): –

…firms enmeshed in global value chains could be compared to jugglers with many balls in the air at the same time. Long and intricate GVCs have many balls in the air, necessitating greater financial resources to knit the production process together. More accommodative financial conditions then act like weaker gravity for the juggler, who can throw many more balls into the air, including large balls that represent intermediate goods with large embedded value. However, when the shadow price of credit rises, the juggler has a more difficult time keeping all the balls in the air at once.

When financial conditions tighten, very long and elaborate GVCs will no longer be viable economically. A rationalisation of supply chains through “on-shoring” and “re-shoring” of activity towards domestic suppliers, or to suppliers that are closer geographically, will help reduce the credit costs of supporting long GVCs.

It is interesting to note the use of the phrase ‘shadow price of credit,’ this suggests that concern about the intermediation process by which changes in the ‘risk-free’ rate disseminate into the real-economy. In a 2014 study, the BIS Committee on the Global Financial System (CGFS) found that 65% of world trade is still financed through ‘open account financing’ or through the buyer paying in advance. For GVC’s, short-term US interest rates matter, especially when 80% of trade finance is still transacted in the US$. Even when rates reached their nadir, banks were reluctant to lend at such favourable terms as they had prior to the GFC. The recent rise in short-term interest rates has supported the US$, accelerating the reversal in the trade to GDP ratio.

A closer investigation of bank lending since the GFC reveals structural weakness in the intermediation process. Since 2009, at the same time as interest rates fell, bank capital requirements rose. The impact of this fiscal offsetting of monetary accommodation can be seen most clearly in the global collapse the velocity of circulation of money supply: –

Source: Tom Drake, National Data, Macrobond

The mechanism by which credit reaches the real economy has been choked. Banks have gradually repaired their balance sheets, but the absurd incentives, such as the inducement to purchase zero risk-weighted government debt rather than lending to corporates, have been given fresh impetus through a combination of structurally higher capital requirements and lower interest rates.

In their January 2018 publication – Structural changes in banking after the crisis – the BIS examines how credit intermediation has changed (the emphasis is mine): –

The crisis revealed substantial weaknesses in the banking system and the prudential framework, which had led to excessive lending and risk-taking unsupported by adequate capital and liquidity buffers…

There is no clear evidence of systematic and long-lasting retrenchment of banks from credit intermediation. The severity of the crisis was not uniform across banks and systems. Weaker banks cut back credit more strongly, and riskier borrowers saw their access to credit more tightly curtailed. In the immediate aftermath of the crisis the response of policymakers and bank managers was also differentiated across systems, with some moving more decisively than others to address the problems revealed. Bank credit has since grown relative to GDP in most jurisdictions, but has not returned to pre-crisis highs in the most affected countries, reflecting necessary deleveraging and the unwinding of pre-crisis excesses. While disentangling demand and supply drivers remains a challenging exercise, the evidence gathered by the Working Group does not point to systematic change in the willingness of banks to lend locally. In line with the objectives of post-crisis reforms, lenders have become more sensitive to risk and more discriminating across borrowers…

The last two sentences appear to contradict, but measuring of loan quality from without is always a challenge. The authors’ continue to perceive credit quality and intermediation, through a glass darkly (once again, the emphasis is mine): –

If anything, the shift towards commercial banking activities suggests that banks are putting more emphasis on lending than trading activities. Still, given the range of changes in the banking sector over the past decade, policymakers should remain attentive to potential unintended “gaps” in credit to the real economy. Legacy asset quality problems can be an obstacle to credit growth. Excessive pre-crisis credit growth left a legacy of problem assets, especially high levels of NPLs, which continue to distort the allocation of fresh credit in several countries…

Persistently high NPLs are likely to lead to greater ultimate losses, impede credit growth and distort credit reallocation, potentially incentivising banks to take on more risk….

Again, the evidence seems to be contradictory. What is different between the cyclical patterns of the past and the current state of affairs? The tried and tested central bank solution to previous crises, stretching all the way back to the 1930’s, if not before, is to cut short-term interest rates – regardless of the level of inflation. The yield curve steepens sharply and banks rapidly repair their balance sheets by borrowing short-term and lending long-term. In the wake of the GFC, however, rates declined yet the economy failed to respond to the stimulus, at least in part, because the central banks accommodative actions were being negated by the tightening of regulatory conditions. Collectively the central banks and the national regulators were robbing Peter to pay Paul. The result (please pardon my emphasis once more): –

Post-crisis bank profitability has remained subdued. This reflects many factors, including bank-specific drivers (eg business model choices), cyclical macroeconomic drivers (eg low growth and interest rates) and structural drivers that will have a more persistent impact. An example of this latter group includes regulatory reforms that have implied lower leverage and the curbing of certain higher risk activities, and a reduction of implicit subsidies for large or systemically important banks…

…all else constant, lower leverage and reduced risk-taking should reduce return on equity. Sluggish revenues have dampened profits and, combined with low interest rates, may have contributed to the slower progress made by some banks in dealing with legacy problem assets…

Sufficient levels of capital are needed for banks to deal with unexpected shocks, and low profitability can weaken banks’ ability to maintain sufficient buffers. Banks that lack a steady stream of earnings to repair their capital base after an unexpected loss will have to rely on fresh equity issuance. Yet, markets are usually an expensive source of capital for banks, when accessed under duress….

In this scenario banks have an incentive to extend and reschedule zombie loans in order to avoid right-downs. Companies which should have been forced into administration linger on, banks’ ability to make new loans is curtailed and new ventures are starved of cash.

The BIS go on to make a number of suggestions in order to deal with low bank profitability and the problem of non-performing legacy assets: –

If overcapacity is a key driver of low profitability, institutional barriers to mergers must be reviewed and exit regimes applied. If the problem lies with legacy assets (such as NPLs), these should be fully addressed, which might entail a dialogue between prudential authorities and other policymakers (eg those in charge of mechanisms dealing with insolvency)…

The exit of financial institutions might be politically costly in the short run, but may pay off in the longer term through more stable banking systems, sounder lending and better allocation of resources. The implicit subsidisation of non-viable business models might have lower short-term costs but could lead to resource misallocation. Similarly, any assessment of consolidation trends needs to take into account potential trade-offs between efficiency and stability, as well as examine the nature and impact of barriers to exit for less profitable banks.

These suggestions make abundant sense but that is no guarantee the BIS recommendations will be heeded.

I am also concerned that the authors’ may be overly optimistic about the resilience of the global banking system: –

Compared with the pre-crisis period, banks are better capitalised and have lower exposure to liquidity and funding risks. They have also reduced activities that contributed to the build-up of vulnerabilities, such as exposure to high-risk assets, and excessive counterparty risk through OTC derivatives and repo transactions, among others. That said, given that markets have not yet evolved through a full financial cycle, bank restructuring efforts remain under way. In addition, as many relevant reforms have not yet been fully implemented, it is too early to assess their full effect.

Thankfully the BIS outlook is not entirely rose-tinted, they do acknowledge: –

…some trends in banking systems that we have observed since the crisis, such as the decline in wholesale funding, might be affected by unconventional monetary policy and may not persist. Success in addressing prior problems does not guarantee that banks will be able to respond to future risks…

Problems of bank governance and risk management contributed to the crisis and have been a key focus of reform. Given that the sources of future vulnerabilities are hard to predict, banks need to have robust frameworks of risk governance and management to identify and understand emerging risks and their potential impacts for the firm.

The BIS choose to gloss over the fact that many banks are still far too big to fail. They avoid discussing whether artificially low interest rates and the excessive flatness of yield curves may be contributing to a different breed of systemic risk. Commercial banks are for-profit institutions, higher capital requirements curtail their ability to achieve acceptable returns on capital. The adoption of central counterparties for the largest fixed income market in the world, interest rate swaps, whilst it reduces the risk for individual banking institutions, increases systemic risk for the market as a whole. The default of a systemically important central counterparties could prove catastrophic.

Conclusions and investment opportunities

The logical solution to the problem of the collapse of global value chains is to create an environment in which the credit cycle fluctuates less violently. A gradual normalisation of interest rates is the first step towards redemption. This could be accompanied by the removal of the moral hazard of central bank and government intervention. The reality? The societal pain of such a gargantuan adjustment would be protracted. It would be political suicide for any democratically elected government to commit to such a meaningful rebalancing. The alternative? More of the same. Come the next crisis central banks will intervene, if they fail to avert disaster, governments’ will resort to the fiscal spigot.

US interest rates will converge towards those of Europe and Japan. Higher stock/earnings multiples will be sustainable, leverage will increase, share buy-backs will continue: and the trend rate of economic growth will decline. Economics maybe the dismal science, but this gloomy economic prognosis will be quite marvellous for assets.

![]()

Macro Letter – No 113 – 19-04-2019

Global Real Estate – Has the tide begun to recede?

I last wrote about the prospects for global real estate back in February 2018 in Macro Letter – No 90 – A warning knell from the housing market – inciting a riot? I concluded: –

The residential real estate market often reacts to a fall in the stock market with a lag. As commentators put it, ‘Main Street plays catch up with Wall Street.’ The Central Bank experiment with QE, however, makes housing more susceptible to, even, a small rise in interest rates. The price of Australian residential real estate is weakening but its commodity rich cousin, Canada, saw major cities price increases of 9.69% y/y in Q3 2017. The US market also remains buoyant, the S&P/Case-Shiller seasonally-adjusted national home price index rose by 3.83% over the same period: no sign of a Federal Reserve policy mistake so far.

As I said at the beginning of this article, all property investment is ‘local’, nonetheless, Australia, which has not suffered a recession for 26 years, might be a leading indicator. Contagion might seem unlikely, but it could incite a riot of risk-off sentiment to ripple around the globe.

More than a year later, central bank interest rates seem to have peaked (if indeed they increased at all) bond yields in most developed countries are falling again and, another round of QE is hotly anticipated, at the first hint of a global, or even regional, slowdown in growth.

In the midst of this sea-change from tightening to easing, an article from the IMF – Assessing the Risk of the Next Housing Bust – appeared earlier this month, in which the authors remind us that housing construction and related spending account for one sixth of US and European GDP. A boom and subsequent bust in house prices has been responsible for two thirds of recessions during the past few decades, nonetheless, they find that: –

…in most advanced economies in our sample, weighted by GDP, the odds of a big drop in inflation-adjusted house prices were lower at the end of 2017 than 10 years earlier but remained above the historical average. In emerging markets, by contrast, riskiness was higher in 2017 than on the eve of the global financial crisis. Nonetheless, downside risks to house prices remain elevated in more than 25 percent of these advanced economies and reached nearly 40 percent in emerging markets in our study.

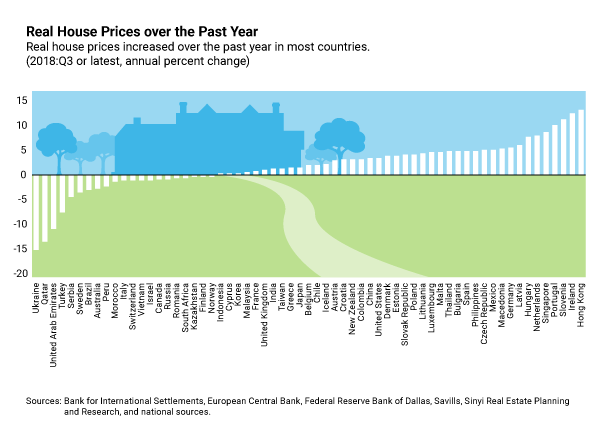

The authors see a particular risk emanating from China’s Eastern provinces but overall they expect conditions to remain reasonably benign in the short-term. The January 2019 IMF – Global Housing Watch – presents the situation as at Q2 and Q3 2018: –

Source: IMF, BIS, Federal Reserve, ECB, Savills, Sinyl, National Data

Hong Kong continues to boom and Ireland to rebound.

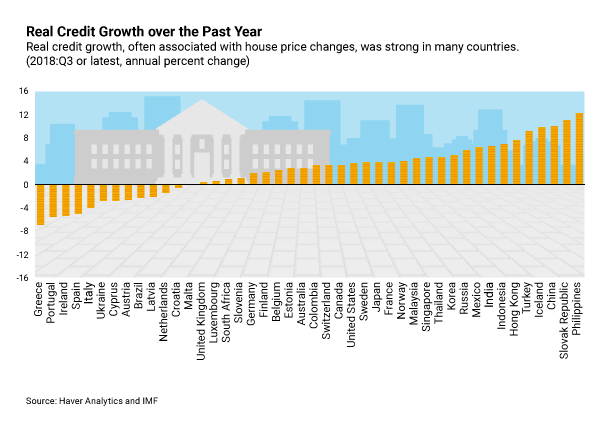

They go on to analyse real credit growth: –

Source: IMF, Haver Analytics

Interestingly, for several European countries (including Ireland) credit conditions have been tightening, whilst Hong Kong’s price rises seem to be underpinned by credit growth.

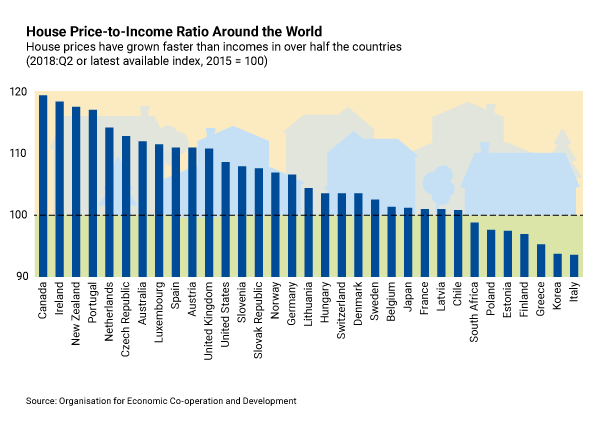

Then the IMF compare house prices to average income: –

Source: IMF, OECD

Canada comes to the fore-front but Ireland is close second with New Zealand and Portugal not far behind.

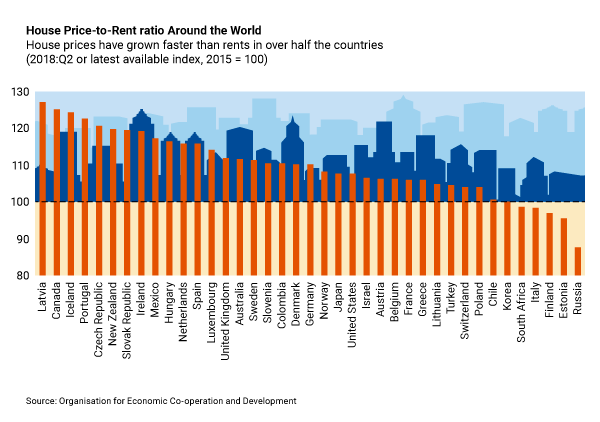

Finally the authors assess House price/Rent ratios: –

Source: IMF, OECD

Both Canada, Portugal and New Zealand are prominent as is Ireland.

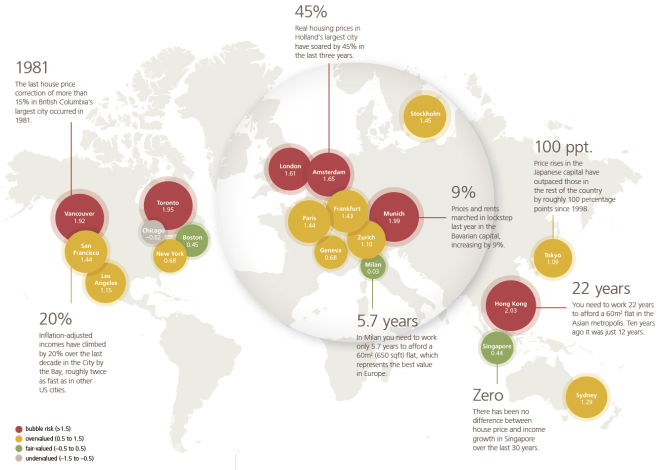

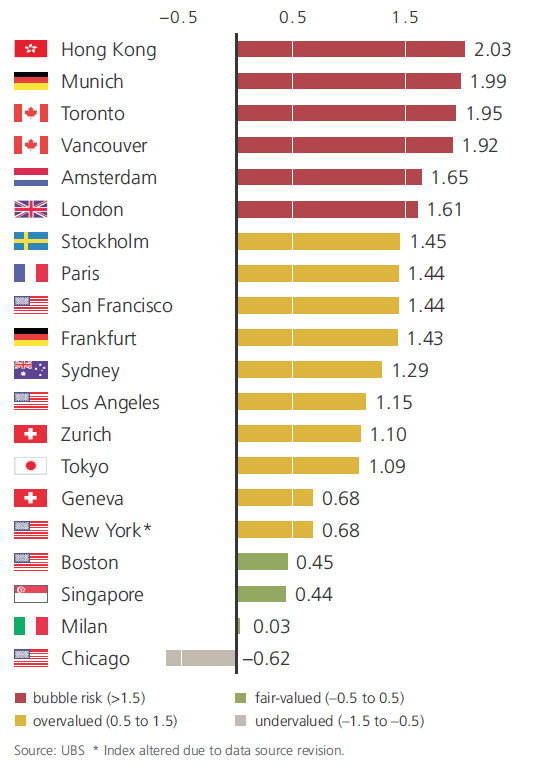

This one year snap-shot disguises some lower term trends. The following chart from the September 2018 – UBS Global Real Estate Bubble Index puts the housing market into long-run perspective.

Source: UBS

UBS go on to rank most expensive cities for residential real estate, pointing out that top end housing prices declined in half of the list:-

Source: UBS

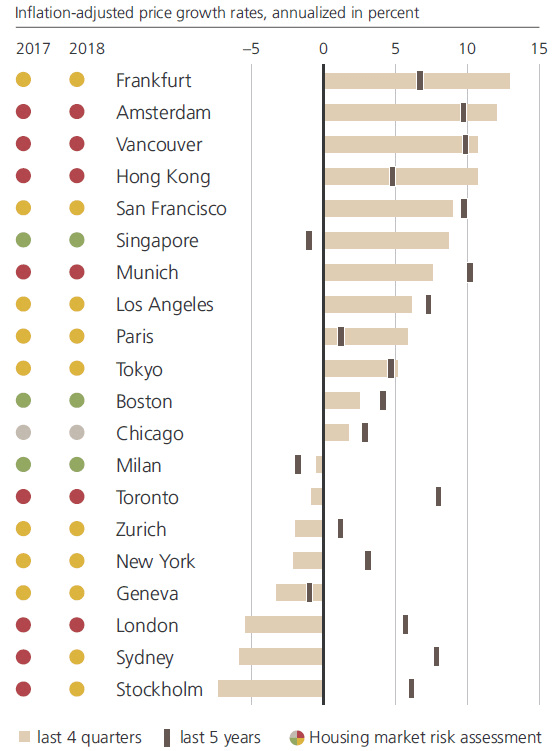

Over the 12 months to September 2018 UBS note that house prices declined in Milan, Toronto, Zurich, New York, Geneva, London, Sydney and Stockholm. The chart below shows the one year change (light grey bar) and the five year change (dark grey line): –

Source: UBS

Is a global correction coming or is property, as always, local? The answer? Local, but with several local markets still at risk.

The US market is generally robust. According to Peter Coy of Bloomberg – America Isn’t Building Enough New Housing – the effect of the housing collapse during the financial crisis still lingers, added to which zoning rules are exacerbating an already small pool of construction-ready lots. Non-credit factors are also corroborated by a recent Fannie Mae survey of housing lenders which found only 1% blaming tight credit, whilst 48% pointed to lack of supply.

North of the border, in Canada, the outlook has become less favourable, partly due to official intervention which began in 2017. Since 2012, house price increases in Toronto accelerated away from other cities, Vancouver followed with a late rush after 2015 and price increases only stalled in the last year.

In their February 2019 report Moody Analytics – 2019 Canada Housing Market Outlook: Slower, Steadier – identify the risks as follows: –

Interventions by the BoC, OSFI, and the British Columbia and Ontario governments were by no means a capricious attempt to deflate a house price bubble for the mere sake of deflation. Financial and macroeconomic aggregates point to the possibility that the mortgage credit needed to sustain house price appreciation may be unsustainable. Since 2002, the ratio of mortgage debt service payments to disposable income has gone from a historical low point of little more than 5% in 2003 to almost 6.6% by the end of last year…

The authors go on to highlight the danger of the overall debt burden, should interest rates rise, or should the Canadian economy slow, as it is expected to do next year. They expect the ratio of household interest payments to disposable income to rise and the percentage of mortgage arrears to follow a similar trajectory. In reality the rate of arrears is still forecast to reach only 0.3%, significantly below its historical average.

External factors could create the conditions for a protracted slump in Canadian real estate. Moody’s point to a Chinese real estate crash, a no-deal Brexit, renewed austerity in Europe and a continuation of the US/China trade dispute as potential catalysts. In this scenario 4% of mortgages would be in arrears. For the present, however, Canadian housing prices remain robust.

Switching to China, the CBRE – Greater China Real Estate Market Outlook 2019 – paints a mixed picture of commercial real estate in the year ahead: –

Office: U.S.–China trade conflict and the ensuing economic uncertainty are set to dent office demand in mainland China and Hong Kong. Leasing momentum in Taiwan will be less affected. Office rents will likely soften in oversupplied and trade and manufacturing-driven cities in 2019.

Retail: The amalgamation of online and offline will continue to drive the evolution of retail demand on the mainland. Retailers in Hong Kong and Taiwan will adopt a conservative approach towards expansion due to the diminishing wealth effect. Retail rents are projected to stay flat or grow slightly in most markets across Greater China.

Logistics: Tight land and warehouse supply will translate into steady logistics rental growth in the Greater Bay Area, Yangtze River Delta and Pan-Beijing area. Risks include potential weaker leasing demand stemming from the U.S.-China trade conflict and the gradual migration to self-built warehouses by major e-commerce companies.

The Chinese housing market, by contrast, has suffered from speculative over-supply. Estimates last year suggested that 22% of homes, amounting to around 50 million dwellings, are unoccupied. Government intervention has been evident for several years in an attempt to moderate price fluctuations. Earlier this month the National Development and Reform Commission (NDRC) said it aims to increase China’s urbanization rate by at least 1% with the aim of tackling the surfeit of supply. This is part of a longer-term goal to bring 100 million people into the cities over the five years to 2020. As of last year, 59.6% of China’s population lived in urban areas. According to World Bank data high middle income countries average 65% rising to 82% for high income countries. For China to reach the average high middle income average, another 70mln people need to move from rural to urban regions.

The new NDRC strategy will include the scrapping of restrictions on household registration permits for non-residents in cities of one to three million. For cities of three to five million, restrictions will be “comprehensively relaxed,” although the NDRC did not specify the particulars. Banks will be incentivised to provide credit and the agency also stated that it will support the establishing of real estate investment trusts (REITs) in order to promote a deepening of the residential rental market.

The NDRC action might seem unnecessary, average prices of new homes in the 70 largest Chinese cities rose 10.4% in February, up from 10.0% the previous month. This is the 46th straight monthly price increase and the strongest annual gain since May 2017. Critics point to cheap credit as the principal driver of this trend, they highlight the danger to domestic prices should the government decide to constrain credit growth. The key to maintaining prices is to open the market to foreign capital, this month’s NDRC policy announcement is a gradual step in that direction. It is estimated that at least $50bln of foreign capital will flow China over the next five years.

Despite the booming residential property market, the Chinese government has been tightening credit conditions and cracking down on illegal financial outflows. This has had impacted Australia in particular, investment fell more than 36% to $.8.2bln last year, down from $13bln in 2017. Mining investment fell 90%, while commercial real estate investment declined by 32%, to $3bln from $4.4bln the previous year. Investment in the US and Canada fell even more, declining by 83% and 47% respectively. Globally, however, Chinese investment has continued to grow, rising 4.2%.

Australian residential housing prices, especially in the major cities, have suffered from this downdraft. According to a report, released earlier this month by Core Logic – Falling Property Values Drags Household Wealth Lower – the decline in prices, the worst in more than two decades, is beginning to bite: –

According to the ABS (Australian Bureau of Statistics), total household assets were recorded at a value of $12.6 trillion at the end of 2018. Total household assets have fallen in value over both the September and December 2018 quarters taking household wealth -1.6% lower relative to June 2018. While the value of household assets have fallen by -1.6% over the past two quarters, liabilities have increased by 1.5% over the same period to reach $2.4 trillion. As a result of falling assets and rising liabilities, household net worth was recorded at $10.2 trillion, the lowest it has been since September 2017…

As at December 2018, household debt was 189.6% of disposable income, a record high and up from 188.7% the previous quarter. Housing debt was also a record high 140.2% of disposable income and had risen from 139.5% the previous quarter.

In 2018 the Australian Residential Property Price Index fell 5.1%, worst hit was Sydney, down 7.8% followed by Melbourne, off 6.4%, Darwin, down 3.5% and Perth, which has been in decline since 2015, which shed a further 2.5%. The ABS cited tightening credit conditions and reduced demand from investors and owner occupiers.

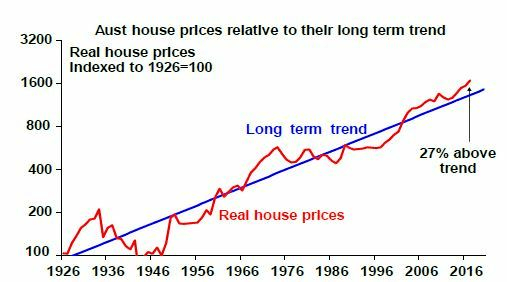

According to many commentators, Australian property has been ready to crash since the bursting of the tech bubble but, as this chart shows, prices are rich but not excessive: –

Source: AMP Capital

Conclusions and Investment Opportunities

The entire second chapter of the IMF – Global Financial Stability Report – published on 10th April, focusses on housing: –

Large house price declines can adversely affect macroeconomic performance and financial stability, as seen during the global financial crisis of 2008 and other historical episodes. These macro-financial links arise from the many roles housing plays for households, small firms, and financial intermediaries, as a consumption good, long-term investment, store of wealth, and collateral for lending, among others. In this context, the rapid increase in house prices in many countries in recent years has raised some concerns about the possibility of a decline and its potential consequences…

Capital inflows seem to be associated with higher house prices in the short term and more downside risks to house prices in the medium term in advanced economies, which might justify capital flow management measures under some conditions. The aggregate analysis finds that a surge in capital inflows tends to increase downside risks to house prices in advanced economies, but the effects depend on the types of flows and may also be region- or city-specific. At the city level, case studies for Canada, China, and the United States find that flows of foreign direct investment are generally associated with lower future risks, whereas other capital inflows (largely corresponding to banking flows) or portfolio flows amplify downside risks to house prices in several cities or regions. Altogether, when nonresident buyers are a key risk for house prices, contributing to a systemic overvaluation that may subsequently result in higher downside risk, capital flow measures might help when other policy options are limited or timing is crucial. As in the case of macroprudential policies, these measures would not amount to targeting house prices but, instead, would be consistent with a risk management approach to policy. In any case, these conditions need to be assessed on a case-by-case basis, and any reduction in downside risks must be weighed against the direct and indirect benefits of free and unrestricted capital flows, including better smoothing of consumption, diversification of financial risks, and the development of the financial sector.

Aside from some corrections in certain cities (notably Vancouver, Toronto, Sydney and Melboune) prices continue to rise in most regions of the world, spurred on by historically low interest rates and generally benign credit conditions. As I said in last month’s Macro Letter – China in transition – From manufacturer to consumer – China will need to open its borders to foreign investment as its current account switches from surplus to deficit. Foreign capital will flow into Chinese property and, when domestic savings are permitted to exit the country, Chinese capital will support real estate elsewhere. The greatest macroeconomic risk to global housing markets stems from a tightening of financial conditions. Central banks appear determined to lean against the headwinds of a recession. In the long run they may fail but in the near-term the global housing market still looks unlikely to implode.

![]()

Macro Letter – No 111 – 15-03-2019

Capital Flows – is a reckoning nigh?

In Macro Letter – No 108 – 18-01-2019 – A world of debt – where are the risks? I looked at the increase in debt globally, however, there has been another trend, since 2009, which is worth investigating as we consider from whence the greatest risk to global growth may hail. The BIS global liquidity indicators at end-September 2018 – released at the end of January, provides an insight: –

The annual growth rate of US dollar credit to non-bank borrowers outside the United States slowed down to 3%, compared with its most recent peak of 7% at end-2017. The outstanding stock stood at $11.5 trillion.

In contrast, euro-denominated credit to non-bank borrowers outside the euro area rose by 9% year on year, taking the outstanding stock to €3.2 trillion (equivalent to $3.7 trillion). Euro-denominated credit to non-bank borrowers located in emerging market and developing economies (EMDEs) grew even more strongly, up by 13%.

The chart below shows the slowing rate of US$ credit growth, while euro credit accelerates: –

Source: BIS global liquidity indicators

The rising demand for Euro denominated borrowing has been in train since the end of the Great Financial Recession in 2009. Lower interest rates in the Eurozone have been a part of this process; a tendency for the Japanese Yen to rise in times of economic and geopolitical concern has no doubt helped European lenders to gain market share. This trend, however, remains over-shadowed by the sheer size of the US credit markets. The US$ has remained preeminent due to structurally higher interest rates and bond yields than Europe or Japan: investors, rather than borrowers, dictate capital flows.

The EC – Analysis of developments in EU capital flows in the global context from November 2018 concurs: –

The euro area (excluding intra-euro area flows) has been since 2013 the world’s leading net exporter of capital. Capital from the euro area has been invested heavily abroad in debt securities, especially in the US, taking advantage of the interest differential between the two jurisdictions. At the same time, foreign holdings of euro-area bonds fell as a result of the European Central Bank’s Asset Purchase Programme.

This bring us to another issue; a country’s ability to service its debt is linked to its GDP growth rate. Since 2009 the US economy has expanded by 34%, over the same period, Europe has shrunk by 2%. Putting these rates of expansion into a global perspective, the last decade has seen China’s economy grow by 139%, whilst India has gained 96%. Recent analysis suggests that Chinese growth may have been overstated by 2% per annum over the past decade, but the pace is still far in excess of developed economy rates. Concern about Chinese debt is not unwarranted, but with GDP rising by 6% per annum, its economy will be 80% larger in a decade, whilst India’s, growing at 7%, will have doubled.

Another excellent research paper from the BIS – The expansionary lower bound: contractionary monetary easing and the trilemma – investigates the problem of monetary tightening of developed economies on emerging markets. Here is part of the introduction, the emphasis is mine: –

…policy makers in EMs are often reluctant to lower interest rates during an economic downturn because they fear that, by spurring capital outflows, monetary easing may end up weakening, rather than boosting, aggregate demand.

An empirical analysis of the determinants of policy rates in EMs provides suggestive evidence about the tensions faced by monetary authorities, even in countries with flexible exchange rates.

…The results reveal that, even after controlling for expected inflation and the output gap, monetary authorities in EMs tend to hike policy rates when the VIX or US policy rates increase. This is arguably driven by the desire to limit capital outflows and the depreciation of the exchange rate.

…our theory predicts the existence of an “Expansionary Lower Bound” (ELB) which is an interest rate threshold below which monetary easing becomes contractionary. The ELB constrains the ability of monetary policy to stimulate aggregate demand, placing an upper bound on the level of output achievable through monetary stimulus.

The ELB can occur at positive interest rates and is therefore a potentially tighter constraint for monetary policy than the Zero Lower Bound (ZLB). Furthermore, global monetary and financial conditions affect the ELB and thus the ability of central banks to support the economy through monetary accommodation. A tightening in global monetary and financial conditions leads to an increase in the ELB which in turn can force domestic monetary authorities to increase policy rates in line with the empirical evidence presented…

The BIS research is focussed on emerging economies, but aspects of the ELB are evident elsewhere. The limits of monetary policy are clearly observable in Japan: the Eurozone may be entering a similar twilight zone.

The difference between emerging and developed economies response to a tightening in global monetary conditions is seen in capital flows and exchange rates. Whilst emerging market currencies tend to fall, prompting their central banks to tighten monetary conditions in defence, in developed economies the flow of returning capital from emerging market investments may actually lead to a strengthening of the exchange rate. The persistent strength of the Japanese Yen, despite moribund economic growth over the past two decades, is an example of this phenomenon.

Part of the driving force behind developed market currency strength in response to a tightening of global monetary conditions is demographic, a younger working age population borrows more, an ageing populous borrows less.

At the risk of oversimplification, lower bond yields in developing (and even developed) economies accelerate the process of capital repatriation. Japanese pensioners can hardly rely on JGBs to deliver their retirement income when yields are at the zero bound, they must accept higher risk to achieve a living income, but this makes them more likely to drawdown on investments made elsewhere when uncertainty rises. A 2% rise in US interest rates only helps the eponymous Mrs Watanabe if the Yen appreciates by less than 2% in times of stress. Japan’s pensioners face a dilemma, a fall in US rates, in response to weaker global growth, also creates an income shortfall; capital is still repatriated, simply with less vehemence than during an emerging market crisis. As I said, this is an oversimplification of a vastly more complex system, but the importance of capital flows, in a more polarised ‘risk-on, risk-off’ world, is not to be underestimated.

Returning to the BIS working paper, the authors conclude: –

The models highlight a novel inter-temporal trade-off for monetary policy since the level of the ELB is affected by the past monetary stance. Tighter ex-ante monetary conditions tend to lower the ELB and thus create more monetary space to offset possible shocks. This observation has important normative implications since it calls for keeping a somewhat tighter monetary stance when global conditions are supportive to lower the ELB in the future.

Finally, the models have rich implications for the use of alternative policy tools that can be deployed to overcome the ELB and restore monetary transmission. In particular, the presence of the ELB calls for an active use of the central bank’s balance sheet, for example through quantitative easing and foreign exchange intervention. Furthermore, the ELB provides a new rationale for capital controls and macro-prudential policies, as they can be successfully used to relax the tensions between domestic collateral constraints and capital flows. Fiscal policy can also help to overcome the ELB, while forward guidance is ineffective since the ELB increases with the expectation of looser future monetary conditions.

Conclusions and investment opportunities

The concept of the ELB is new, the focus of the BIS working paper is on its impact on emerging markets. I believe the same forces are evident in developed economies too, but the capital flows are reversed. For investors, the greatest risk of emerging market investment is posed by currency, however, each devaluation by an emerging economy inexorably weakens the position of developed economies, since the devaluation makes that country’s exports immediately more competitive.

At present the demographic forces favour repatriation during times of crisis and repatriation, at a slower rate, during times of EM currency appreciation. This is because the ageing economies of the developed world continue to drawdown on their investments. At some point this demographic effect will reverse, however, for Japan and the Eurozone this will not be before 2100. For more on the demographic deficit the 2018 Ageing Report: Europe’s population is getting older – is worth reviewing. Until demographic trends reverse, international demand to borrow in US$, Euros and Yen will remain popular. Emerging market countries will pay the occasional price for borrowing cheaply, in the form of currency depreciations.

For Europe and Japan a reckoning may be nigh, but it seems more likely that their economic importance will gradually diminish as emerging economies, with a younger working age population and higher structural growth rates, eclipse them.

![]()

Macro Letter – No 99 – 22-06-2018

Where in the world? Hunting for value in the bond market

In my last Macro Letter – Italy and the repricing of European government debt – I said: –

I have never been a great advocate of long-term investment in fixed income securities, not in a world of artificially low official inflation indices and fiat currencies. Given the de minimis real rate of return I regard them as trading assets.

Suffice to say, I received a barrage of advice from some of my good friends who have worked in the fixed income markets for the majority of their careers. I felt I had perhaps been flippant in dismissing an entire asset class without so much as a qualm. In this letter I distil an analysis of more than one hundred markets around the world into a short list of markets which may be worthy of further analysis.

To begin with I organised countries by their most recent inflation rate, then I added their short term interest rate and finally, where I was able to find reliable information, a 10 year yield for the government bond of each country. I then calculated the real interest rate, real yield and shape of the yield curve.

At this point I applied three criteria, firstly that the real yield should be greater than 1.5%, second, that the real interest rate should also exceed that level: and finally, that the yield curve should be more than 2% positive. These measures are not entirely arbitrary. A real return of 1.5% is below the long-run average (1.7%) for fixed income securities in the US since 1900, though not by much. For an analysis of the data, this article from Observations and Notes is informative – U.S. 10-Year Treasury Note Real Return History: –

As you might have expected, the real returns earned were consistently below the initial coupon rate. The only exceptions occur around the time of the Great Depression. During this period, because of deflation, the value of some or all of the yearly interest payments was often higher than the original coupon rate, increasing the yield. (For more on this important period see The 1929 Stock Market Crash Revisited)

While the average coupon rate/nominal return was 4.9%, the average real return was only1.7%. Not surprisingly, the 3.2% difference between the two is the average inflation experienced for the century.

As an investor I require a positive expected real return with the minimum of risk, therefore if short term interest rates offer a real return of more than 1.5% I will incline to favour a floating rate rather than a fixed rate investment. Students of von Mises and Rothbard may beg to differ perhaps; for those of you who are unfamiliar with the Austrian view of the shape of the yield curve in an unhampered market, this article by Frank Shostak – How to Interpret the Shape of the Yield Curve provides an excellent primer. Markets are not unhampered and Central Banks, at the behest of their respective governments, have, since the dawn of the modern state, had an incentive to artificially lower short-term interest rates: and, latterly, rates across the entire maturity spectrum. For more on this subject (6,000 words) I refer you to my essay for the Cobden Centre – A History of Fractional Reserve Banking – the link will take you to part one, click here for part two.

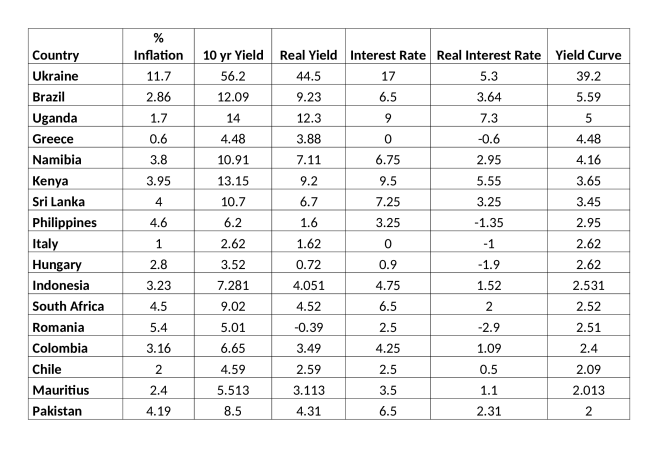

Back to this week’s analysis. I am only interested in buying 10yr government bonds of credit worthy countries, where I can obtain a real yield on 10yr maturity which exceeds 1.5%, but I also require a positive yield curve of 2%. As you may observe in the table below, my original list of 100 countries diminishes rapidly: –

Source: Investing.com, Trading Economics, WorldBondMarkets.com

Five members of this list have negative real interest rates – Italy (the only G7 country) included. Despite the recent prolonged period of negative rates, this situation is not normal. Once rates eventually normalise, either the yield curve will flatten or 10yr yields will rise. Setting aside geopolitical risks, as a non-domicile investor, do I really want to hold the obligations of nations whose short-term real interest rates are less than 1.5%? Probably not.

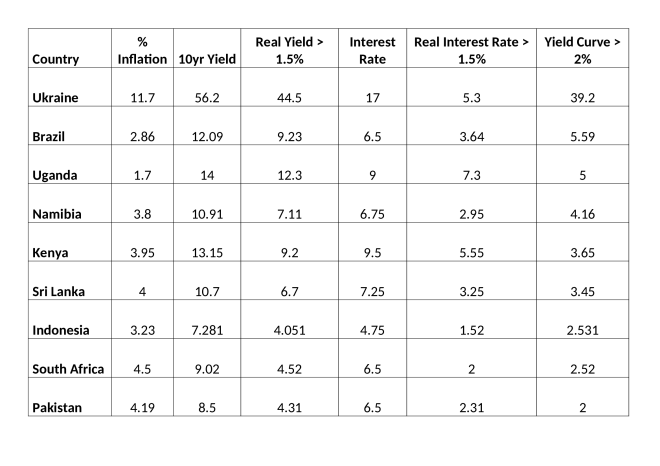

Thus, I arrive at my final cut. Those markets where short-term real interest rates exceed 1.5% and the yield curve is 2% positive. Only nine countries make it onto the table and, perhaps a testament to their governments ability to raise finance, not a single developed economy makes the grade: –

Source: Investing.com, Trading Economics, WorldBondMarkets.com

There are a couple of caveats. The Ukrainian 10yr yield is derived, I therefore doubt its accuracy. 3yr Ukrainian bonds yield 16.83% and the yield curve is mildly inverted relative to official short-term rates. Brazilian bonds might look tempting, but it is important to remember that its currency, the Real, has declined by 14% against the US$ since January. The Indonesian Rupiah has been more stable, losing less than 3% this year, but, seen in the context of the move since 2012, during which time the currency has lost 35% of its purchasing power, Indonesian bonds cannot but considered ‘risk-free’. I could go on – each of these markets has lesser or greater currency risk.

I recant. For the long term investor there are bond markets which are worth consideration, but, setting aside access, liquidity and the uncertainty of exchange controls, they all require active currency management, which will inevitably reduce the expected return, due to factors such as the negative carry entailed in hedging.

Conclusions and investment opportunities

Investing in bond markets should be approached from a fundamental or technical perspective using strategies such as value or momentum. Since February 2012 Greek 10yr yields have fallen from a high of 41.77% to a low of 3.63%, although from the July 2014 low of 5.47% they rose to 19.44% in July 2015, before falling to recent lows in January of this year. For a trend following strategy, this move has presented abundant opportunity – it increases further if the strategy allows the investor to be short as well as long. Compare Greek bonds with Japanese 10yr JGBs which, over the same period, have fallen in yield from 1.02 in January 2012 to a low of -0.29% in July 2016. That is still a clear trend, although the current BoJ policy of yield curve control have created a roughly 10bp straight-jacket beyond which the central bank is committed to intervene. The value investor can still buy at zero and sell at 10bp – if you trust the resolve of the BoJ – it is likely to be profitable.

The idea of buying bonds and holding them to maturity may be profitable on occasion, but active management is the only logical approach in the current global environment, especially if one hopes to achieve acceptable real returns.

![]()

Macro Letter – No 92 – 09-03-2018

Are we nearly there yet? Employment, interest rates and inflation

There are two factors, above all others, which are spooking asset markets at present, inflation and interest rates. The former is impossible to measure with any degree of certainty – for inflation is in the eye of the beholder – and the latter is divergent depending on whether you look at the US or Japan – with Europe caught somewhere between the two extremes. In this Macro Letter I want to investigate the long term, demand-pull, inflation risk and consider what might happen if stocks, bonds and real estate all collapse in tandem.

It is reasonable to assume that US rates will rise this year, that UK rates might follow and that the ECB (probably) and BoJ (almost certainly) will remain on the side-lines. An additional worry for export oriented countries, such as Japan and Germany, is the protectionist agenda of the current US administration. If their exports collapse, GDP growth is likely to slow in its wake. The rhetoric of retaliation will be in the air.

For international asset markets, the prospect of higher US interest rates and protectionism, spells lower growth, weakness in employment and a lowering of demand-pull inflationary pressure. Although protectionism will cause prices of certain goods to rise – use that aluminium foil sparingly, baste instead – the overall effect on employment is likely to be swift.

Near-term impact

Whilst US bond yields rise, European bond yields may fail to follow, or even decline, if export growth collapses. Stocks in the US, by contrast, may be buoyed by tax cuts and the short-term windfall effect of tariff barriers. The high correlation between equity markets and the international nature of multinational corporations, means global stocks may remain levitated a while longer. The momentum of recent economic growth may lead to increased employment and higher wages in the near-term – and this might even spur demand for a while – but the spectre of inflation at the feast, will loom like a hawk.

Longer-term effects

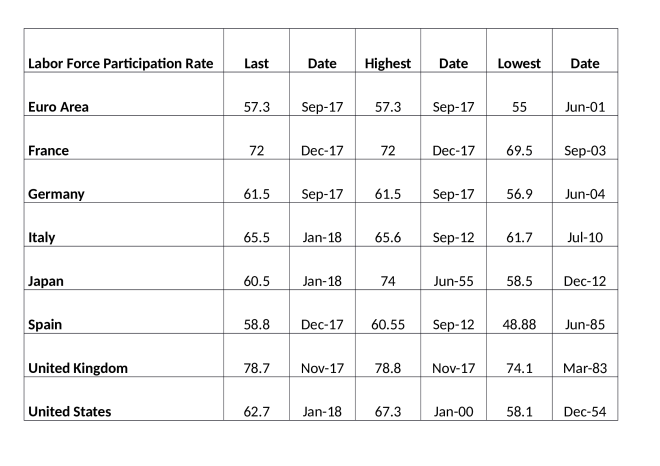

But is inflation really going to be a structural problem? In an attempt to answer this we must delve into the murky waters of the employment data. As a starting point, at what juncture can we be confident that the US and other countries at or near to full-employment? Let us start by looking at the labour force participation rate. It is a difficult measure to interpret. As the table below shows, in the US and Japan the trend has been downward whilst the UK and the EU are hitting record highs:-

Source: Trading Economics

One possible reason for this divergence between the EU and the US/Japan is that the upward trend in European labour participation has been, at least partially, the result of an inexorable reduction in the scope and scale of the social safety net throughout the region.

More generally, since the Great Recession of 2008/2009 a number of employment trends have been evident across most developed countries. Firstly, many people have moved from full-time to part-time employment. Others have switched from employment to self-employment. In both cases these trends have exerted downward pressure on earnings. What little growth in earnings there has been, has mainly emanated from the public sector, but rising government deficits make this source of wage growth unsustainable in the long run.

The Record of Meeting of the CAC and Federal Reserve Board of Governors – published last November, stated the following in relation to US employment:-

The data indicate that despite the drop in unemployment, there has not been an increase in the number of quality jobs—those that pay enough to cover expenses and enable workers to save for the future. The 2017 Scorecard reports that one in four jobs in the U.S. is in a low-wage occupation, which means that at the median salary, these jobs pay below the poverty threshold for a family of four. For the first time, the 2017 Scorecard includes a measure of income volatility that shows that one in five households has significant income fluctuations from month to month. The percentage varies by state, from a low of 14.7 percent of households in Virginia to a stunning 29.8 percent of households in Wyoming. In addition, 40 percent of those experiencing volatility reported struggling to pay their bills at least once in the last year because of these income fluctuations. These two factors contribute significantly to the fact that almost 37 percent of U.S. households, and 51 percent of households of color, live in the financial red zone of “liquid asset poverty.” This means that they do not have enough liquid savings to replace income at the poverty level for three months if their main source of income is disrupted, such as from job loss or illness. This level of financial insecurity has profound implications for the security of households, and for the overall economic growth of the nation.

Another trend that has been evident is the increase in the number of people no longer seeking employment. Setting aside those who, for health related reasons, have exited the employment pool, early retirement has been one of the main factors swelling the ranks of the previously employable. For this growing cohort, inflation never went away. In particular, inflation in healthcare has been one of the main sources of increases in the price level over the past decade.

At the opposite end of the working age spectrum, education is another factor which has reduced the participation rate. It has also exerted downward pressure on wages; as more students enrol in higher education in order to gain, hopefully, better paid employment, the increased supply of graduates insures that the economic value of a degree diminishes. Whilst a number of corporations have begun to offer apprenticeships or in-work degree qualifications, in order to address the skill gap between what is being taught and what these firms require from their employees, the overall impact of increased demand for higher education has been to reduce the participation rate.

For a detailed assessment of the situation in the US, this paper from the Kansas City Federal Reserve – Why Are Prime-Age Men Vanishing from the Labor Force? provides some additional and fascinating insights. Here is the author’s conclusion:-

Over the past two decades, the nonparticipation rate among primeage men rose from 8.2 percent to 11.4 percent. This article shows that the nonparticipation rate increased the most for men in the 25–34 age group and for men with a high school degree, some college, or an associate’s degree. In 1996, the most common situation prime-age men reported during their nonparticipation was a disability or illness, while the least common situation was retirement. While the share of primeage men reporting a disability or illness as their situation during nonparticipation declined by 2016, this share still accounted for nearly half of all nonparticipating prime-age men. This result is in line with Krueger’s (2016) finding, as many of these men with a disability or illness are likely suffering from daily pain and using prescription painkillers.

I argue that a decline in the demand for middle-skill workers accounts for most of the decline in participation among prime-age men. In addition, I find that the decline in participation is unlikely to reverse if current conditions hold. In 2016, the share of nonparticipating prime-age men who stayed out of the labor force in the subsequent month was 83.8 percent. Moreover, less than 15 percent of nonparticipating prime-age men reported that they wanted a job. Together, this evidence suggests nonparticipating prime-age men are less likely to return to the labor force at the moment.

The stark increase in prime-age men’s nonparticipation may be the result of a vicious cycle. Skills demanded in the labor market are rapidly changing, and automation has rendered the skills of many less-educated workers obsolete. This lack of job opportunities, in turn, may lead to depression and illness among displaced workers, and these health conditions may become further barriers to their employment. Ending this vicious cycle—and avoiding further increases in the nonparticipation rate among prime-age men—may require equipping workers with the new skills employers are demanding in the face of rapid technological advancements.

For an even more nuanced interpretation of the disconnect between corporate profits and worker compensation this essay by Jonathan Tepper of Varient Perception – Why American Workers Aren’t Getting A Raise: An Economic Detective Story – is even more compelling:-

Rising industrial concentration is a powerful reason why profits don’t mean revert and a powerful explanation for the imbalance between corporations and workers. Workers in many industries have fewer choices of employer, and when industries are monopolists or oligopolists, they have significant market power versus their employees.

The role of high industrial concentration on inequality is now becoming clear from dozens recent academic studies. Work by The Economist found that over the fifteen-year period from 1997 to 2012 two-thirds of American industries were more concentrated in the hands of a few firms. In 2015, Jonathan Baker and Steven Salop found that “market power contributes to the development and perpetuation of inequality.”

One of the most comprehensive overviews available of increasing industrial concentration shows that we have seen a collapse in the number of publicly listed companies and a shift in power towards big companies. Gustavo Grullon, Yelena Larkin, and Roni Michaely have documented how despite a much larger economy, we have seen the number of listed firms fall by half, and many industries now have only a few big players. There is a strong and direct correlation between how few players there are in an industry and how high corporate profits are.

Tepper goes on to discuss monopolies and monopsonies. At the heart of the issue is the zombie company phenomenon. With interest rates at artificially low levels, companies which should have been liquidated have survived. Others have used their access to finance, gained from many years of negotiation with their bankers, to buy out their competitors. If interest rates were correctly priced this would not have been possible – these zombie corporations would have gone to the wall. I wrote a rather long two part essay on this subject in 2016 for the Cobden Centre – A history of Fractional Reserve Banking – or why interest rates are the most important influence on stock market valuations? This is about the long-run even by my standards but I commend it to those of you with an interest in economic history. Here is a brief quote from part 2:-

…This might seem incendiary but, let us assume that the rate of interest at which the UK government has been able to borrow is a mere 300bp below the rate it should have been for the last 322 years – around 4% rather than 7%. What does this mean for corporate financing?

There are two forces at work: a lower than “natural” risk free rate, which should make it possible for corporates to borrow more cheaply than under unfettered conditions. They can take on new projects which would be unprofitable under normal conditions, artificially prolonging economic booms. The other effect is to allow the government to crowd out private sector borrowing, especially during economic downturns, where government borrowing increases at the same time that corporate profitability suffers. The impact on corporate interest rates of these two effects is, to some extent, self-negating. In the long run, excessive government borrowing permanently reduces the economic capacity of the country, by the degree to which government investment is less economically productive than private investment.

To recap, more people are remaining in education, more people are working freelance or part-time and more people are choosing to retire early. The appreciation of the stock, bond and property markets has certainly helped those who are asset rich, choose to exit the ranks of the employable, but, I suspect, in many cases this is only because asset prices have been rising for the past decade. Pension annuity rates appear to have hit all-time lows, a reckoning for asset markets is overdue.

What happens come the next bust and beyond?

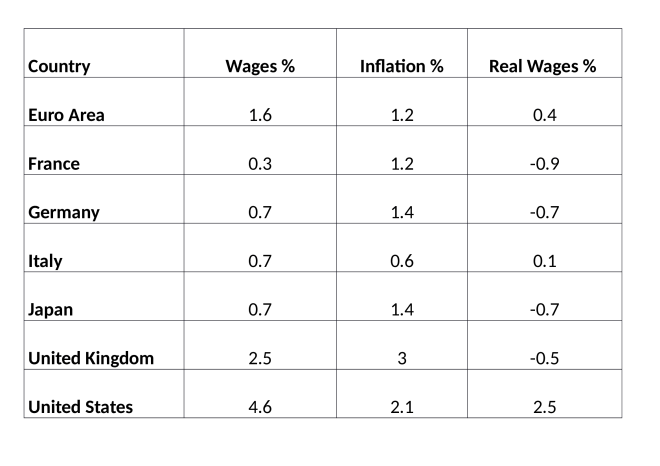

If inflation rises and Central Banks respond by raising interest rates, bond prices will fall and stocks will have difficulty avoiding the force of gravity. Once bond and stock markets fall, property prices are likely to follow, as the cost of financing mortgages increases. With all the major asset classes in decline, economic growth will slow and unemployment will rise. Meanwhile, the need to work, in order to supplement the reduction in income derived from a, no longer appreciating, pool of assets, will increase, putting downward pressure on average earnings. Here is the most recent wage, inflation and real wage data. For France, Germany and the UK, wages continue to lag behind prices. A 2% inflation target is all very well, just so long as wages can keep up:-

Source: Trading Economics

The first place where this trend in lower earnings will become evident is likely to be among freelance and part-time workers – at least they will still have employment. The next casualty will be the fully employed. Corporations will lay-off staff as corporate profit warnings force their hands. Governments will be beseeched to create jobs and, regardless of whether the inflation rate is still rising or not, Central Banks will be implored, cajoled (whatever it takes) to cut interest rates and renew their quest to purchase every asset under the sun.

Wage deflation will, of course, continue, harming those who have no alternative but to work; those who lack sufficient unearned income to survive. Government debt will accelerate, Central Bank balance sheets will balloon and asset prices will eventually recover. Bond yields may even reach new record lows, prompting assets to flow into stocks – the ones Central Banks have not yet purchased as part of their QQE programmes – despite their inflated valuations. Corporate executives will no doubt take the view that interest rates are artificially low and conclude that they can best serve their shareholders by buying back their own stock – accompanied by the occasional special dividend to avoid accusations for impropriety.

As economic growth takes a nose drive, inflation will moderate, providing justification for the pre-emptive rate cutting and balance sheet expanding actions of the Central Banks. Articles will begin to appear, in esteemed journals, talking of a new era of low economic trend growth. Finally, after several years of QE, QQE and whatever the stage beyond that may be – helicopter money anyone? – the world economy will start to grow more rapidly and the labour force participation rate, increase once more. Inflation will start to rise, interest rates will be tightened, bond yields, increase. At this point, stocks will fall and the next downward leg of the economic cycle will have to be averted by renewed QQE and fiscal stimulus. If this is reminiscent of a scene from Groundhog Day, I regret to inform you, it is.

There will be a point at which the financialisation of the global economy and the nationalisation of the stock market can no longer deliver the markets from the deleterious curse of debt, but, sadly, I do not believe that moment has yet arrived. Are we nearly there yet? Not even close.