![]()

Macro Letter – No 99 – 22-06-2018

Where in the world? Hunting for value in the bond market

- Few government bond markets offer a positive real return

- Those that do tend to have high associated currency risk

- Active management of fixed income portfolios is the only real solution

- Italy is the only G7 country offering a real-yield greater than 1.5%

In my last Macro Letter – Italy and the repricing of European government debt – I said: –

I have never been a great advocate of long-term investment in fixed income securities, not in a world of artificially low official inflation indices and fiat currencies. Given the de minimis real rate of return I regard them as trading assets.

Suffice to say, I received a barrage of advice from some of my good friends who have worked in the fixed income markets for the majority of their careers. I felt I had perhaps been flippant in dismissing an entire asset class without so much as a qualm. In this letter I distil an analysis of more than one hundred markets around the world into a short list of markets which may be worthy of further analysis.

To begin with I organised countries by their most recent inflation rate, then I added their short term interest rate and finally, where I was able to find reliable information, a 10 year yield for the government bond of each country. I then calculated the real interest rate, real yield and shape of the yield curve.

At this point I applied three criteria, firstly that the real yield should be greater than 1.5%, second, that the real interest rate should also exceed that level: and finally, that the yield curve should be more than 2% positive. These measures are not entirely arbitrary. A real return of 1.5% is below the long-run average (1.7%) for fixed income securities in the US since 1900, though not by much. For an analysis of the data, this article from Observations and Notes is informative – U.S. 10-Year Treasury Note Real Return History: –

As you might have expected, the real returns earned were consistently below the initial coupon rate. The only exceptions occur around the time of the Great Depression. During this period, because of deflation, the value of some or all of the yearly interest payments was often higher than the original coupon rate, increasing the yield. (For more on this important period see The 1929 Stock Market Crash Revisited)

While the average coupon rate/nominal return was 4.9%, the average real return was only1.7%. Not surprisingly, the 3.2% difference between the two is the average inflation experienced for the century.

As an investor I require a positive expected real return with the minimum of risk, therefore if short term interest rates offer a real return of more than 1.5% I will incline to favour a floating rate rather than a fixed rate investment. Students of von Mises and Rothbard may beg to differ perhaps; for those of you who are unfamiliar with the Austrian view of the shape of the yield curve in an unhampered market, this article by Frank Shostak – How to Interpret the Shape of the Yield Curve provides an excellent primer. Markets are not unhampered and Central Banks, at the behest of their respective governments, have, since the dawn of the modern state, had an incentive to artificially lower short-term interest rates: and, latterly, rates across the entire maturity spectrum. For more on this subject (6,000 words) I refer you to my essay for the Cobden Centre – A History of Fractional Reserve Banking – the link will take you to part one, click here for part two.

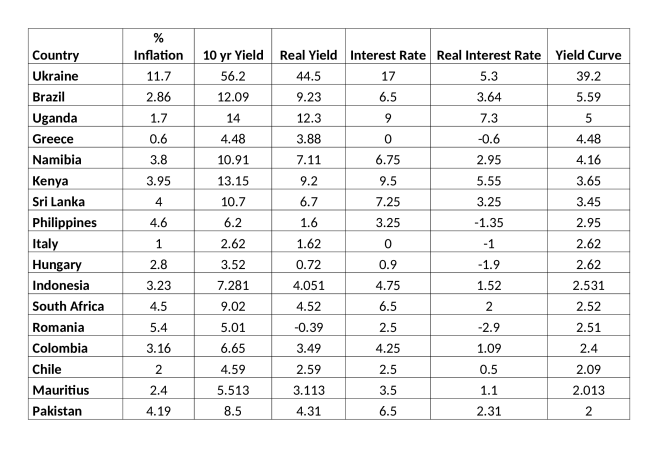

Back to this week’s analysis. I am only interested in buying 10yr government bonds of credit worthy countries, where I can obtain a real yield on 10yr maturity which exceeds 1.5%, but I also require a positive yield curve of 2%. As you may observe in the table below, my original list of 100 countries diminishes rapidly: –

Source: Investing.com, Trading Economics, WorldBondMarkets.com

Five members of this list have negative real interest rates – Italy (the only G7 country) included. Despite the recent prolonged period of negative rates, this situation is not normal. Once rates eventually normalise, either the yield curve will flatten or 10yr yields will rise. Setting aside geopolitical risks, as a non-domicile investor, do I really want to hold the obligations of nations whose short-term real interest rates are less than 1.5%? Probably not.

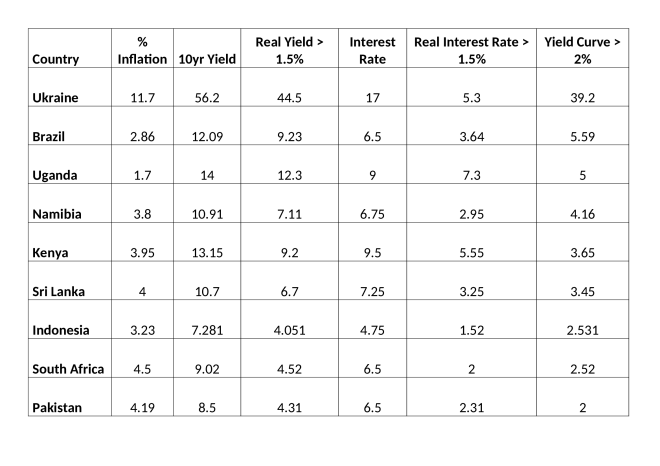

Thus, I arrive at my final cut. Those markets where short-term real interest rates exceed 1.5% and the yield curve is 2% positive. Only nine countries make it onto the table and, perhaps a testament to their governments ability to raise finance, not a single developed economy makes the grade: –

Source: Investing.com, Trading Economics, WorldBondMarkets.com

There are a couple of caveats. The Ukrainian 10yr yield is derived, I therefore doubt its accuracy. 3yr Ukrainian bonds yield 16.83% and the yield curve is mildly inverted relative to official short-term rates. Brazilian bonds might look tempting, but it is important to remember that its currency, the Real, has declined by 14% against the US$ since January. The Indonesian Rupiah has been more stable, losing less than 3% this year, but, seen in the context of the move since 2012, during which time the currency has lost 35% of its purchasing power, Indonesian bonds cannot but considered ‘risk-free’. I could go on – each of these markets has lesser or greater currency risk.

I recant. For the long term investor there are bond markets which are worth consideration, but, setting aside access, liquidity and the uncertainty of exchange controls, they all require active currency management, which will inevitably reduce the expected return, due to factors such as the negative carry entailed in hedging.

Conclusions and investment opportunities

Investing in bond markets should be approached from a fundamental or technical perspective using strategies such as value or momentum. Since February 2012 Greek 10yr yields have fallen from a high of 41.77% to a low of 3.63%, although from the July 2014 low of 5.47% they rose to 19.44% in July 2015, before falling to recent lows in January of this year. For a trend following strategy, this move has presented abundant opportunity – it increases further if the strategy allows the investor to be short as well as long. Compare Greek bonds with Japanese 10yr JGBs which, over the same period, have fallen in yield from 1.02 in January 2012 to a low of -0.29% in July 2016. That is still a clear trend, although the current BoJ policy of yield curve control have created a roughly 10bp straight-jacket beyond which the central bank is committed to intervene. The value investor can still buy at zero and sell at 10bp – if you trust the resolve of the BoJ – it is likely to be profitable.

The idea of buying bonds and holding them to maturity may be profitable on occasion, but active management is the only logical approach in the current global environment, especially if one hopes to achieve acceptable real returns.