Macro Letter – No 41 – 11-09-2015

What are the bond markets telling us about inflation, recession and the path of central bank policy?

- Since January US Government bond yields have risen across the yield curve

- Corporate bond yields have risen more rapidly as stock markets have retreated

- China, Canada and Mexico have seen their currencies weaken against the US$

For several years some commentators have been concerned that the Federal Reserve is behind the curve and needs to tighten interest rates before inflation returns. To date, inflation – by which I refer narrowly to CPI – has remained subdued. The recent recovery in the US economy and improvement in the condition of the labour market has seen expectations of rate increases grow and bond market yields have risen in response. In this letter I want to examine whether the rise in yields is in expectation of a Fed rate increase, fears about the return of inflation or the potential onset of a recession for which the Federal Reserve and its acolytes around the globe are ill-equipped to manage.

Below is a table showing the change in yields since the beginning of February. Moody Baa rating is the lowest investment grade bond. Whilst the widening of spreads is consistent with the general increase in T-Bond yields, the yield on Baa bonds has risen by 30bp more than Moody BB – High Yield, sub-investment grade. This could be the beginning of an institutional reallocation of risk away from the corporate sector.

| Bond | Spread over T-Bonds | |||||

| 08-Sep | 02-Feb | Change | 08-Sep | 02-Feb | Change | |

| 10yr US T-Bond | 2.19 | 1.65 | 0.54 | N/A | N/A | N/A |

| Baa Corporate | 5.28 | 4.29 | 0.99 | 3.09 | 2.64 | 0.45 |

| BB Corporate | 5.55 | 4.86 | 0.69 | 3.36 | 3.21 | 0.15 |

Source: Ycharts and Investing.com

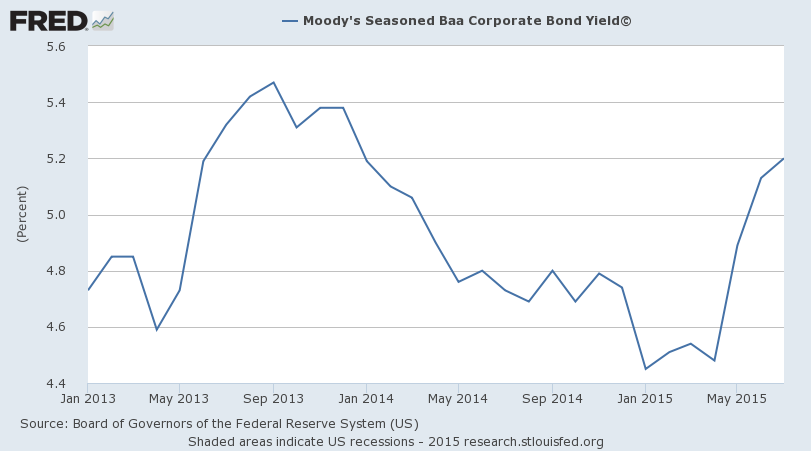

The chart below shows the evolution of Baa bond yields over the last two years:-

Source: St Louis Federal Reserve

The increase in the cost of financing for the corporate sector is slight but the trend, especially since May, is clear.

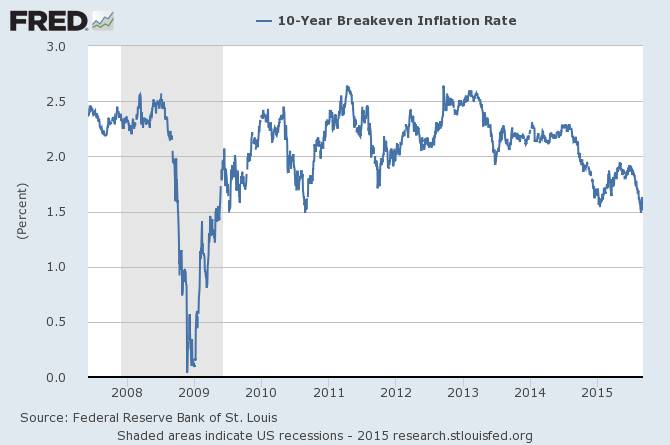

Another measure of the state of the economy is the breakeven expected inflation rate. This metric is derived from the differential between 10-Year Treasury Constant Maturity Securities and 10-Year Treasury Inflation-Indexed Constant Maturity Securities:-

Source: St Louis Federal Reserve

By this measure inflation expectations are near their lowest levels since 2010. It looks as if the bond markets are doing the Federal Reserve’s work for it. Added to which the July minutes of the FOMC stated:-

The risks to the forecast for real GDP and inflation were seen as tilted to the downside, reflecting the staff’s assessment that neither monetary nor fiscal policy was well positioned to help the economy withstand substantial adverse shocks.

This is hardly hiking rhetoric.

The International perspective

The table below looks at the largest importers into the US and their contribution to the US trade deficit as at December 2014:-

| Country/Region | Imports | Deficit |

| China | $467bln | $343bln |

| EU | $418bln | $142bln |

| Canada | $348bln | $35bln |

| Mexico | $294bln | $54bln |

| Japan | $134bln | $68bln |

Source: US Census Bureau

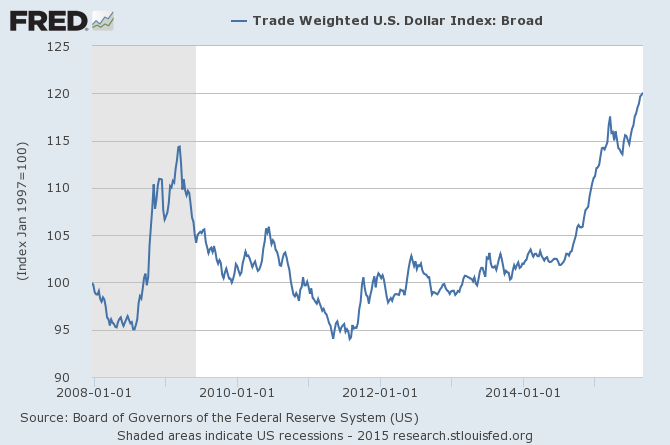

The TWI US$ Index shows a rather different picture to the US$ Index chart I posted last month, it has strengthened against its major trading partners steadily since it lows in July 2011; after a brief correction, during the first half of 2015, the trend has been re-established and shows no signs of abating:-

Source: St Louis Federal Reserve

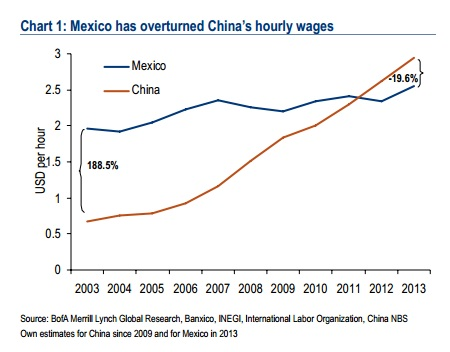

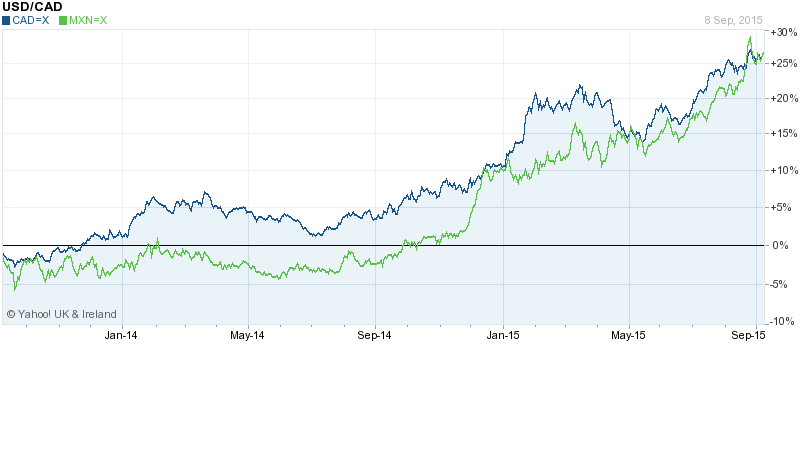

A closer inspection of the performance of the Loonie (CAD) and Peso (MXN) reveals an additional source of disinflation:-

Source: Yahoo Finance

Focus Economics – After dismal performance in May, exports and imports increase in June – investigates the bifurcated impact of lower oil prices and a weaker currency on the prospects for the Mexican economy:-

Looking at the headline numbers, exports increased 1.2% year-on-year in June, which pushed overseas sales to USD 33.8 billion. The monthly expansion contrasted the dismal 8.8% contraction registered in May. June’s expansion stemmed mainly from a solid increase in non-oil exports (+6.8% yoy). Conversely, oil exports registered another bleak plunge (-41.0% yoy).

… Should the U.S. economy continue to recover and the Mexican peso weaken, growth in Mexico’s overseas sales is likely to continue improving in the coming months.

Mexico’s gains have to some extent been at the expense of Canada as this August 2015 article from the Fraser Institute – Canada faces increased competition in U.S. market – explains:-

There are several possible explanations of the cessation of real export growth to the U.S. One is the slow growth of the U.S. economy over much of the period from 2000-2014, particularly during and following the Great Recession of 2008. Slower real growth of U.S. incomes can be expected to reduce the growth of demand for all types of goods including imports from Canada.

A second possible explanation is the appreciation of the Canadian dollar over much of the time period. For example, the Canadian dollar increased from an all-time low value of US$.6179 on Jan. 21, 2002 to an all-time high value of US$1.1030 on Nov. 7, 2007. It then depreciated modestly to a value of US$.9414 by Jan. 1, 2014.

A third possible explanation is the higher costs to shippers (and ultimately to U.S. importers) associated with tighter border security procedures implemented by U.S. authorities after 9/11.

Perhaps a more troubling and longer-lasting explanation is Canada’s loss of U.S. market share to rival exporters. For example, Canada’s share of total U.S. imports of motor vehicles and parts decreased by almost 12 percentage points from 2000 through 2013, while Mexico’s share increased by eight percentage points. Canada lost market share (particularly to China) in electrical machinery and even in its traditionally strong wood and paper products sectors.

There is fundamentally only one robust way for Canadian exporters to reverse the recent trend of market share loss to rivals. Namely, Canadian manufacturers must improve upon their very disappointing productivity performance over the past few decades—both absolutely and relatively to producers in other countries. Labour productivity in Canada grew by only 1.4 per cent annually over the period 1980-2011. By contrast, it grew at a 2.2 per cent annual rate in the U.S. Even worse, multifactor productivity—basically a measure of technological change in an economy—did not grow at all over that period in Canada.

With an election due on 19th October, the Canadian election campaign is focused on the weakness of the domestic economy and measures to stimulate growth. While energy prices struggle to rise, non-energy exports are likely to be a policy priority. After rate cuts in January and July, the Bank of Canada left rates unchanged this week, but with an election looming this is hardly a surprise.

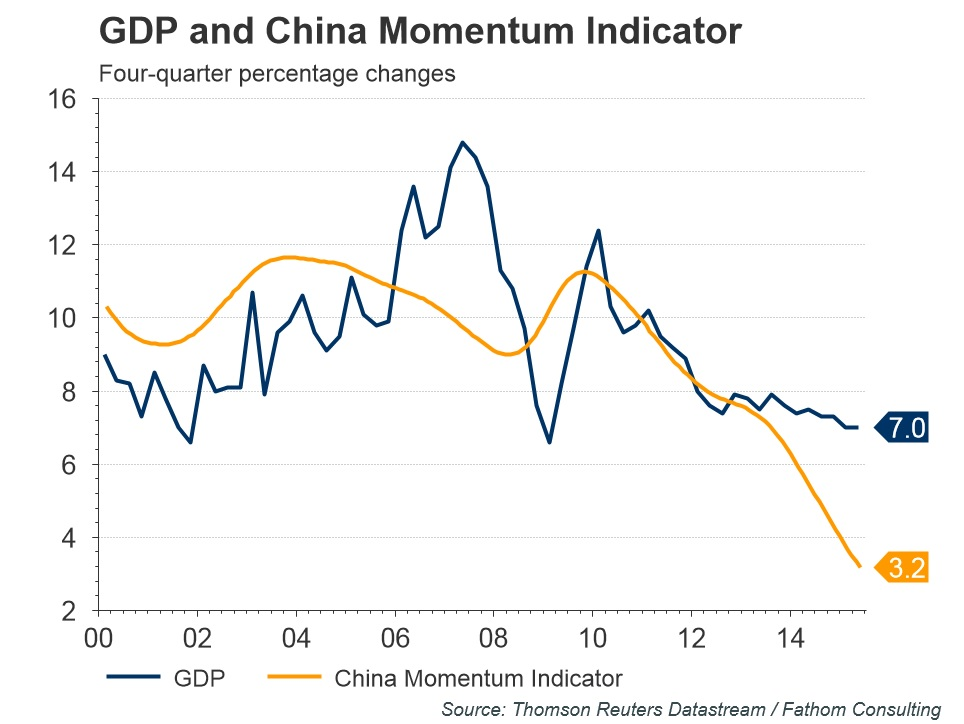

China, as I mentioned in my last post here, unpegged its currency last month. Official economic forecasts remain robust but, as economic consultants Fathom Consulting pointed out in this July article for Thomson Reuters – Alpha Now – China a tale of two economies – there are many signs of a slowing of economic activity, except in the data:-

With its usual efficiency, China’s National Bureau of Statistics released its 2015 Q2 growth estimate earlier this week. Reportedly, GDP rose by 7.0% in the four quarters to Q2. We remain sceptical about the accuracy of China’s GDP data, and the speed with which they are compiled. Our own measure of economic activity — the China Momentum Indicator — suggests the current pace of growth is nearer 3.0%.

…although policymakers are reluctant to admit that China has slowed dramatically, the recent onslaught of measures aimed at stimulating the economy surely hints at their discomfort. While these measures may temporarily alleviate the downward pressure, they do very little to resolve China’s long standing problems of excess capacity, non-performing loans and perennially weak household consumption.

Accordingly, as China tries out the full range of its policy levers, we believe that eventually it will resort to exchange rate depreciation. Its recent heavy-handed intervention in the domestic stock market has demonstrated afresh its disregard for financial reform.

The chart below is the Fathom Consulting – China Momentum Indicator – note the increasing divergence with official GDP data:-

Source: Fathom Consulting/Thomson Reuters

A comparison between international government bonds also provides support for those who argue Fed policy should remain on hold:-

| Government Bonds | 2yr | 2yr | Change | 5yr | 5yr | Change | 10yr | 10yr | Change | 30yr | 30yr | Change |

| 08-Sep | 02-Feb | 08-Sep | 02-Feb | 08-Sep | 02-Feb | 08-Sep | 02-Feb | |||||

| US | 0.74 | 0.47 | 0.27 | 1.52 | 1.17 | 0.35 | 2.19 | 1.65 | 0.54 | 2.96 | 2.23 | 0.73 |

| Canada | 0.45 | 0.39 | 0.06 | 0.79 | 0.61 | 0.18 | 1.48 | 1.25 | 0.23 | 2.24 | 1.83 | 0.41 |

| Mexico | 5.01* | 4.13* | 0.88 | 5.29 | 4.89 | 0.4 | 6.15 | 5.41 | 0.74 | 6.81 | 6.1 | 0.71 |

| Germany | -0.22 | -0.19 | -0.03 | 0.05 | -0.04 | 0.09 | 0.68 | 0.32 | 0.36 | 1.44 | 0.9 | 0.54 |

| Japan | 0.02 | 0.04 | -0.02 | 0.07 | 0.09 | -0.02 | 0.37 | 0.34 | 0.03 | 1.41 | 1.31 | 0.1 |

| China | 2.59 | 3.22 | -0.63 | 3.2 | 3.45 | -0.25 | 3.37 | 3.53 | -0.16 | 3.88 | 4.04 | -0.16 |

*Mexico 3yr Bonds

Source: Investing.com

Canada and Mexico have both witnessed rising yields as their currencies declined, whilst Germany (a surrogate for the EU) and Japan have seen a marginal fall in shorter maturities but an increase for maturities of 10 years or more. China, with a still slowing economy and aided by PBoC policy, has lower yields across all maturities. Mexican inflation – the highest of these trading partners – was last recorded at 2.59% whilst core inflation was 2.31%. The 2yr/10yr curve for both Mexico and Canada, at just over 100bps, is flatter than the US at 145bp. The Chinese curve is flatter still.

A final, if somewhat tangential, article which provides evidence of a lack of inflationary pressure comes from this fascinating post by Stephen Duneier of Bija Advisors – Doctoring Deflation – in which he looks at the crisis in healthcare and predicts that computer power will radically reduce costs globally:-

The future of medical diagnosis is about to experience a radical shift. The same pocket sized computer which now holds the power to beat any human being at the game of chess, will soon be used to diagnose medical ailments and prescribe actions to follow, far more cheaply and with a whole lot more accuracy.

Conclusions and investment opportunities

The bond yield curves of America’s main import partners have steepened in train with the US – Canada being an exception – whilst stock markets are unchanged or lower over the same period – February to September. Corporate bond spreads have widened, especially the bottom of the investment grade category. Corporate earnings have exceeded expectations, as they so often do – see this paper by Jim Liew et al of John Hopkins for more on this topic – but by a negligible margin.

The FOMC has already expressed concern about the momentum of GDP growth, commodity prices remain under pressure, China has unpegged and the US$ TWI has reached new highs. This suggests to me, that inflation is not a risk, disinflationary forces are growing – especially driven by the commodity sector. Major central banks are unlikely to tighten but corporate bond yields may rise further.

Currencies

Remain long US$ especially against resource based currencies, but be careful of current account surplus countries which may see flight to quality flows in the event of “risk off” panic.

Stocks

At the risk of stating what any “value” investor should always look for, seek out firms with strong cash-flow, low leverage, earnings growth and comfortable dividend cover. In addition, in the current environment, avoid commodity sensitive stocks, especially in oil, coal, iron and steel.

Bonds

US T-Bonds will benefit from a strengthening US$, if the FOMC delay tightening this will favour shorter maturities. An early FOMC tightening, after initial weakness, will be a catalyst for capital repatriation – US T-Bonds will fare better in this scenario too. Bunds and JGBs are likely to witness similar reactions but, longer term, both their currencies and yields are less attractive.