During the last three months inflation has become a much debated topic. This article, which was published in March, may still add something to the increasingly heated debate: –

Inflationary Inflection Point or Temporary Blip?

During the last three months inflation has become a much debated topic. This article, which was published in March, may still add something to the increasingly heated debate: –

Inflationary Inflection Point or Temporary Blip?

Macro Letter – No 134 – 27-11-2020

Relax, Rotate, Reflate

November has been an interesting month for financial markets around the world. The US Presidential election came and went and with its passing financial market uncertainty diminished. This change of administration is undeniably important, but its effect was overshadowed by the arrival of three vaccines for Covid-19. As I write (Thursday 26th) the S&P 500 Index is within 30 points of its all-time high, amid a chemical haze of pharmaceutical hope, whilst the VIX Index has tested its lowest level since February (20.8%). The Nasdaq Composite is also near to its peak and the Russell 2000 Index (an index of smaller capitalisation stocks) burst through its highs from February 2020 taking out its previous record set in September 2018. The chart below shows the one year performance of the Russell 2000 versus the S&P500 Index: –

Source: Yahoo Finance, S&P, Russell

It is worth remembering that over the very long term Small Caps have outperformed Large Caps, however, during the last decade the rapid growth of index tracking investments such as ETFs has undermined this dynamic, investment flows are a powerful force. I wrote about this topic in June in – A Brave New World for Value Investing – in which I concluded: –

Stock and corporate bond markets have regained much of their composure since late March. Central banks and governments have acted to ameliorate the effects of the global economic slowdown. As the dust begins to settle, the financial markets will adjust to a new environment, one in which value-based stock and bond market analysis will provide an essential aid to navigation.

The geopolitics of trade policy, already a source of tension before the pandemic struck, has been turbo-charged by the simultaneous supply and demand shocks and their impact on global supply chains. Supply chains will shorten and diversify. Robustness rather than efficiency will be the watch-word in the months and years ahead. This sea-change in the functioning of the world economy will not be without cost. It will appear in increased prices or reduced corporate profits. Value-based investment analysis will be the best guide in this brave new world.

To date, evidence of a return to Value Investing seems premature, Growth still dominates and the structural acceleration of technology trends seems set to continue – one might say, ‘there is Value in that.’

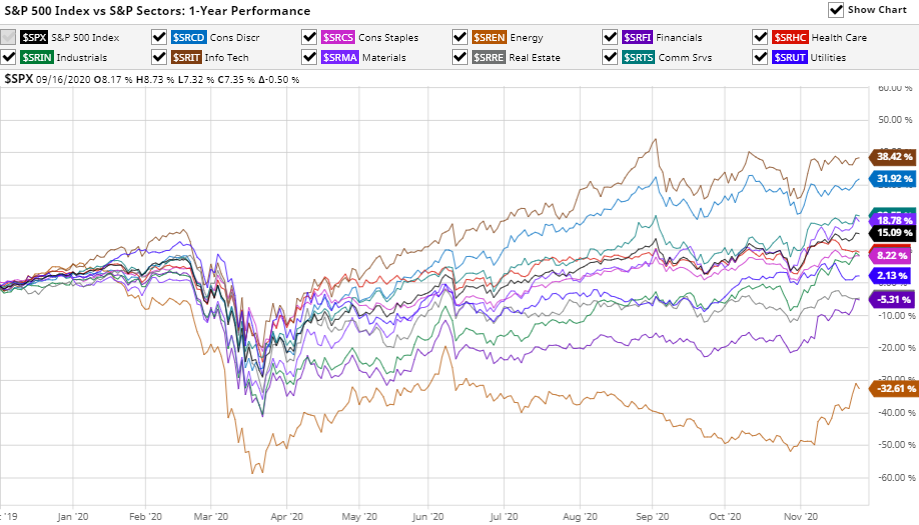

The vaccine news led to a rotation out of technology stocks but this was more to do with profit taking, new ‘Tech’ buyers quickly emerged. The rotation into Small Caps was also echoed among a number of out of favour sectors such as Airlines and Energy. It was enough to prompt the creation of a new acronym – BEACHs – Booking, Entertainment, Airlines, Cruises and Hotels.

Source: Barchart.com, S&P

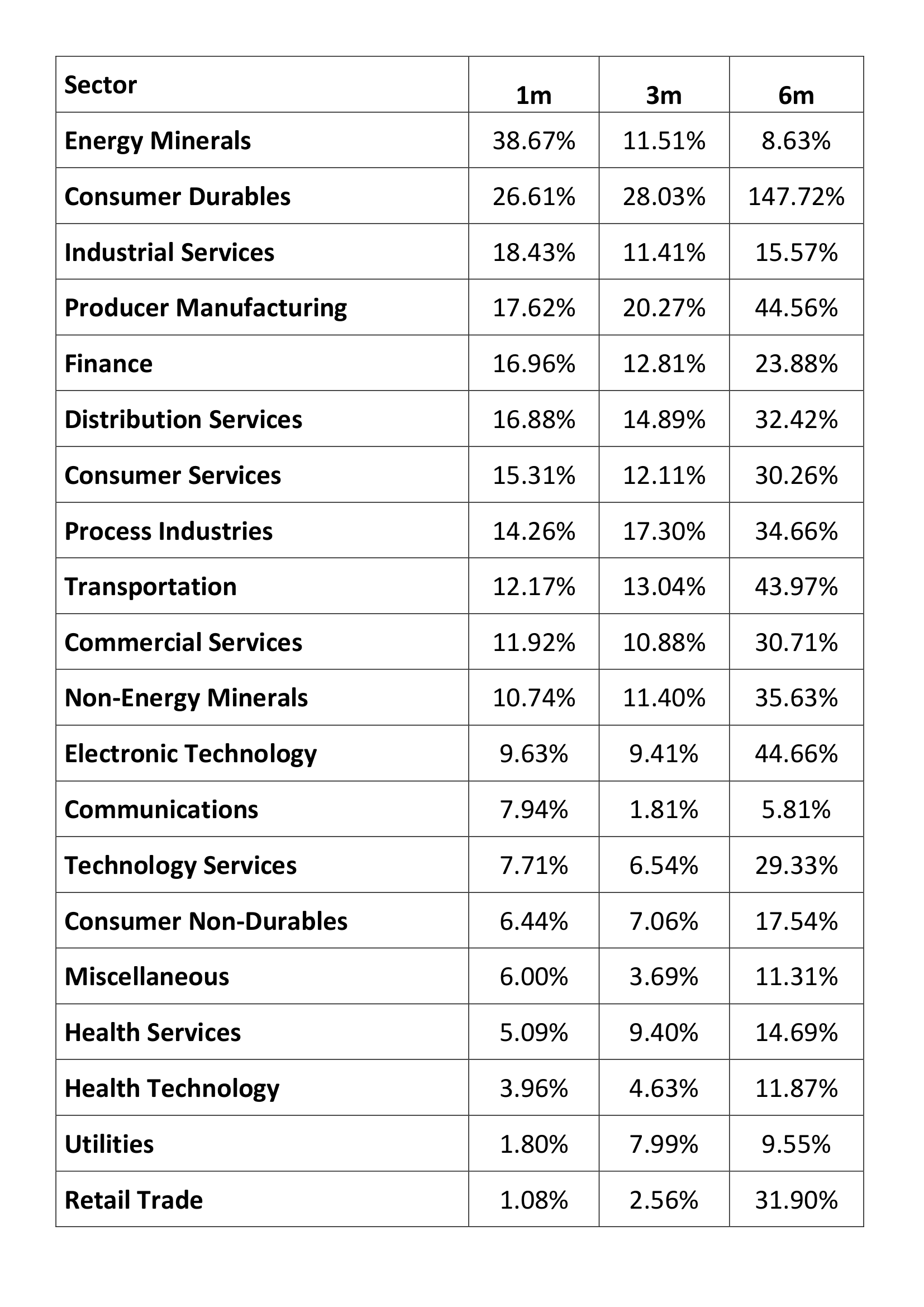

Above is the one year performance of the 11 S&P 500 industry sectors. Information Technology remains the leader (+38%) with Energy bringing up the rear (-32%) however the level of dispersion of returns is unusually which has presented an abundance of trading opportunities. The table below shows the one, three and six month performance for an expanded selection of these sectors: –

Source: Tradingview

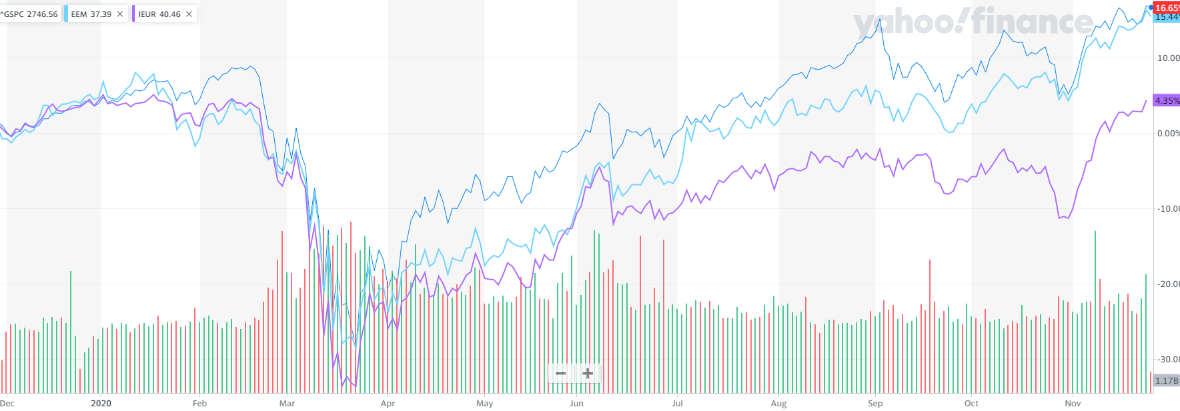

Beyond the US, news of the vaccines encouraged both European and emerging markets, but the latter (EEM), helped by the strong performance of Chinese stocks, have tracked the US quite closely throughout the year, it is Europe (IEUR) which has staged the stronger recovery of late, although it has yet to retest its February highs: –

Source: Yahoo Finance, S&P, MSCI

In the aftermath of the US election, US bond yields have inched higher. From an all-time low of 32bp in March, 10yr yields tripled, testing 97bp in the wake of the Democrat win. Putting this in perspective, the pre-Covid low was seen at 1.32% in July 2016. The current concern is partly about the ‘socialist’ credentials of President-elect, Biden, but the vaccine announcement, together with the prospect of a return to some semblance of normality, has also raised the spectre of a less accommodative stance from the Fed. There was initial fear they might ‘take away the punch-bowl’ before the global economy gets back on its knees, let alone its feet. Governor Powell, quickly dispelled bond market fears and yields have since stabilised.

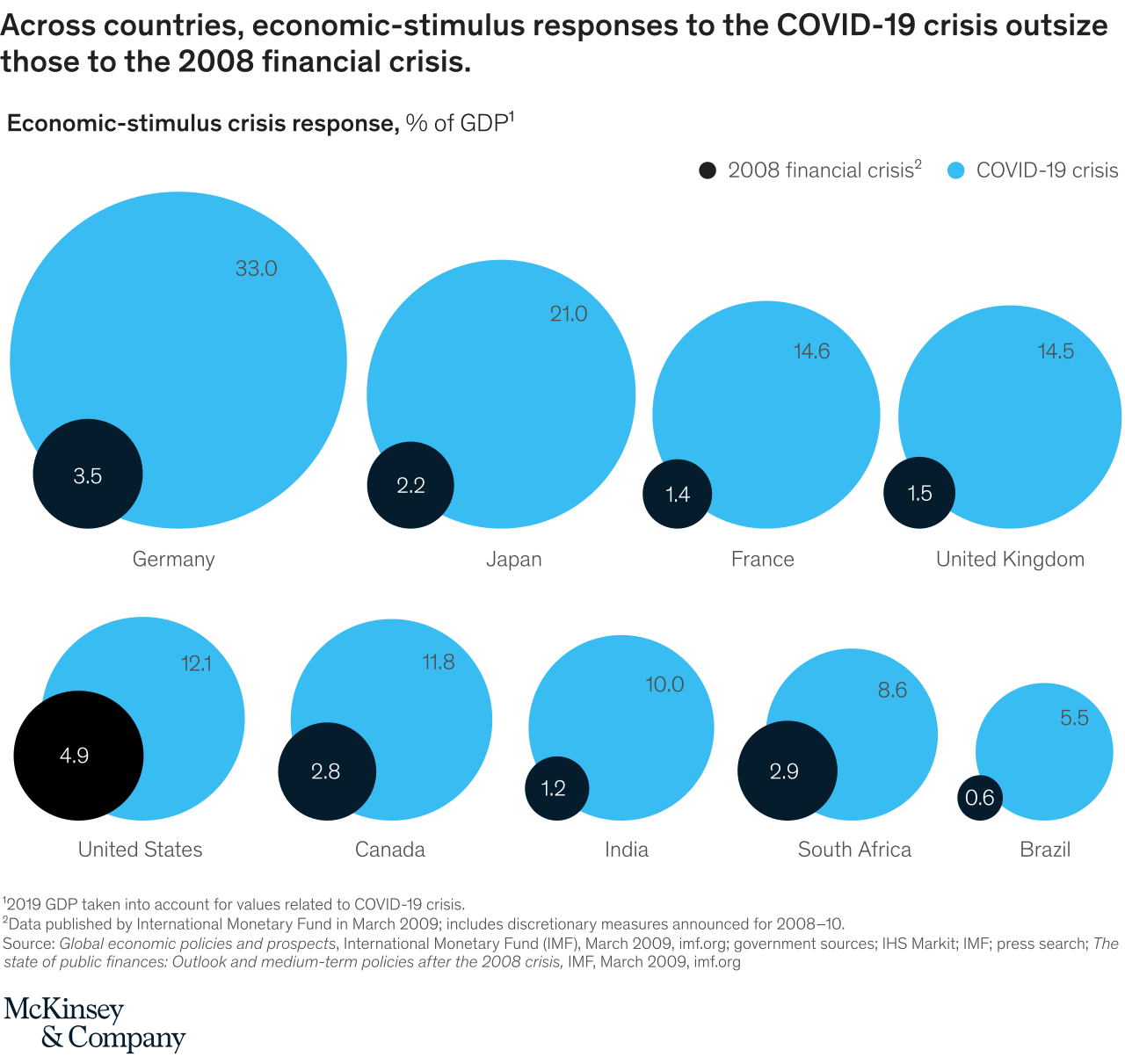

Longer-term, these bond market concerns may be justified, as this infographic from the McKinsey Institute reveals, combined central bank and government fiscal stimulus in 2020 has utterly eclipsed the largesse witnessed in the wake of the 2008 crisis: –

Source: McKinsey

Bond watchers can probably rest easy, however, should the global economy stage the much vaunted ‘V’ shaped recovery economists predicted back in the spring, only a fraction of the fiscal stimulus will actually materialise. Nonetheless, prospects for mass-vaccination, even in developed countries, remains some months away, both monetary and fiscal spigots will continue to spew for the present.

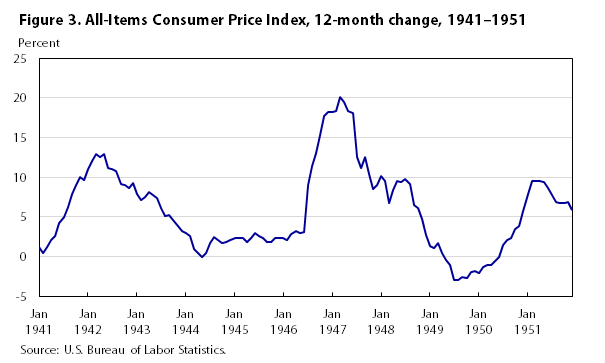

On the topic of monetary policy it is worth noting that the Federal Reserve previously employed ‘yield curve control,’ though it was not called by that name, back in April 1942, five months after the attack on Pearl Harbor. Under this arrangement the Fed committed to peg T-Bills at 3/8th and implicitly cap long-dated T-Bonds at 2.5%. The aim was to stabilize the securities market and allow the government to engage in cheaper debt financing during the course of WWII. This arrangement only ended with the Treasury – Fed Accord of 1951 in response to a sharp peace-time resurgence in inflation. This chart shows the period from 1941 (when the US entered WWII) up to the middle of the Korean War: –

Source: US BLS

I believe we will need to see several years of above target inflation before the Fed to feel confident in raising rates aggressively. The experience of Japan, where deflation has been lurking in the wings for decades, will inform Fed decision making for the foreseeable future.

Returning to the present environment; away from the stock and bond markets, oil prices also basked in the reflected light shining from the end of the pandemic tunnel. West Texas Intermediate, which tested $33.64/bbl on 2nd, reached $46.26/bbl on 25th. The energy sector remains cautious, nonetheless, even the recent resurgence leaves oil prices more than $15/bbl lower than they were at the start of the year.

Looking ahead, the stock market may take a breather over the next few weeks. A vaccine is coming, but not immediately. US politics also remains in the spotlight, the Republicans currently hold 50 Senate seats to the Democrats 48. If Democrats secure the two seats in Georgia, in the runoff election on 5th January, VP Elect, Harris, will be able to use her ‘tie-break’ vote to carry motions, lending the Biden Presidency teeth and hastening the expansion of US fiscal policy.

The stock market has yet to make up its mind about whether Biden’s ‘New New Dealers’ are a positive or a negative. Unemployment and under-employment numbers remain elevated as a result of the pandemic: and, whilst bankruptcies are lower than at this time last year, the ending of the myriad schemes to prolong the existence of businesses will inevitably see those numbers rise sharply. Does the stock market benefit more from the fiscal spigot than the tax increase? This is a question which will be mulled, chewed and worried until long after Biden’s inauguration on January 20th.

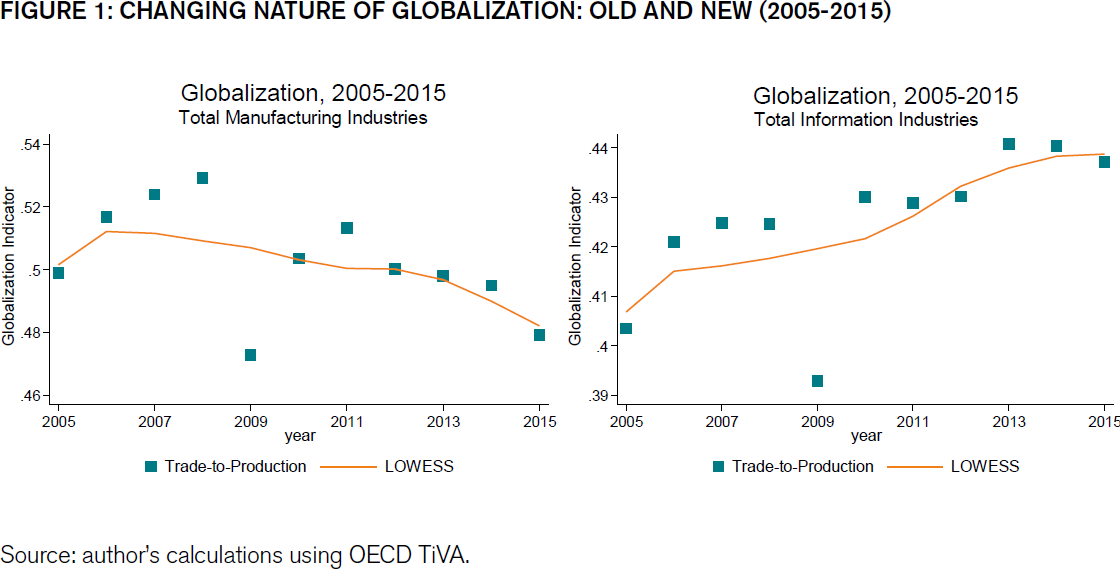

Meanwhile the trend accelerations in technology which I discussed in – The prospects for Emerging and Frontier Markets in the post-Covid environment – earlier this month, continue. The chart below shows how information industries have been transforming the makeup of global trade ever since the great financial crisis: –

Source: ECIPE, OECD, TiVA, van der Marel

Manufacturing trade is in retreat, trade in digital services is accelerating. The chart above stops at 2015, when we have the data to incorporate the period of the current pandemic, I expect the pace of growth in information industries to have gain even greater momentum.

Back in 1987, MIT economist and Nobel Laureate, Robert Solow, observed that the computer age was everywhere except for the productivity statistics. During the 1990’s technology productivity growth was finally observed, but the past decade has seen a string of disappointing productivity growth statistics, yet they have coincided with digitisation transforming vast swathes of the global economy, perhaps the next decade will see the fruit of these labours. I believe we can look forward to significant productivity improvements in the coming years. Stock prices, however, are forward looking, their valuations may seem extended but this may be entirely justified if technology ushers in a new golden age.

![]()

Macro Letter – No 114 – 10-05-2019

Debasing the Baseless – Modern Monetary Theory

A recent post from the Peterson Institute – Further Thinking on the Costs and Benefits of Deficits – follows on from the Presidential Lecture given by Olivier Blanchard at the annual gathering of the American Economic Association (AEA) Public Debt and Low Interest Rates . The article discusses a number of issues which are linked to Blanchard’s speech: –

Is the political system so biased towards deficit increases that economists have a responsibility to overemphasize the cost of deficits?

Do the changing economics of deficits mean that anything goes and we do not need to pay attention to fiscal constraints, as some have inferred from modern monetary theory (MMT)?

You advocate doing no harm, but is that enough to stabilize the debt at a reasonable level?

Isn’t action on the deficit urgent in order to reduce the risk of a fiscal crisis?

Do you think anything about fiscal policy is urgent?

Their answers are 1. Sometimes, although they question whether it is the role of economists to lean against the political wind. 2. No, which is a relief to those of a more puritanical disposition towards debt. The authors’ argument, however, omits any discussion of the function of interest rates in an unfettered market, to act as a signal about the merit of an investment. When interest rates are manipulated, malinvestment flourishes. They propose: –

…that the political system should adopt a “do no harm” approach, paying for new proposals but not necessarily making it an urgent priority to do any more than that. Adopting this principle would have the benefit of requiring policymakers to think harder about whether to adopt the next seemingly popular tax credit or spending program. Many ideas that seem appealing judged against an unspecified future cost are less appealing when you make their costs explicit today.

A prelude to MMT

The reason for highlighting recent Peterson commentary is because it represents the acceptable face of a more dubious set of proposals, known collectively as MMT. These ideas are not particularly modern, beginning with the Chartalist tenet that countries which issue their own fiat currencies can never “run out of money.” For a measured introduction to this topic, Dylan Matthews has published a brilliant essay for Vox – Modern Monetary Theory, explained. Here are some of the highlights: –

[The starting point is]…endogenous money theory, that rejects the idea that there’s a supply of loanable funds out there that private businesses and governments compete over. Instead, they believe that loans by banks themselves create money in accordance with market demands for money, meaning there isn’t a firm trade-off between loaning to governments and loaning to businesses of a kind that forces interest rates to rise when governments borrow too much.

MMTers go beyond endogenous money theory, however, and argue that government should never have to default so long as it’s sovereign in its currency: that is, so long as it issues and controls the kind of money it taxes and spends. The US government, for instance, can’t go bankrupt because that would mean it ran out of dollars to pay creditors; but it can’t run out of dollars, because it is the only agency allowed to create dollars. It would be like a bowling alley running out of points to give players.

A consequence of this view, and of MMTers’ understanding of how the mechanics of government taxing and spending work, is that taxes and bonds do not and indeed cannot directly pay for spending. Instead, the government creates money whenever it spends…

And why does the government issue bonds? According to MMT, government-issued bonds aren’t strictly necessary. The US government could, instead of issuing $1 in Treasury bonds for every $1 in deficit spending, just create the money directly without issuing bonds.

The Mitchell/Wray/Watts MMT textbook argues that the purpose of these bond issuances is to prevent interest rates in the private economy from falling too low. When the government spends, they argue, that adds more money to private bank accounts and increases the amount of “reserves” (cash the bank has stocked away, not lent out) in the banking system. The reserves earn a very low interest rate, pushing down interest rates overall. If the Fed wants higher interest rates, it will sell Treasury bonds to banks. Those Treasury bonds earn higher interest than the reserves, pushing overall interest rates higher…

“In the long term,” they conclude, “the only sustainable position is for the private domestic sector to be in surplus.” As long as the US runs a current account deficit with other countries, that means the government budget has to be in deficit. It isn’t “crowding out” investment in the private sector, but enabling it.

The second (and more profound) aspect of MMT is that it proposes to reverse the roles of fiscal and monetary policy. Taxation is used to control aggregate demand (and thus inflation) whilst government spending (printing money) is used to prevent deflation and to stimulate consumption and employment. Since MMT advocates believe there is no need for bond issuance and that interest rates should reside, permanently, at zero, monetary policy can be controlled entirely by the treasury, making central banks superfluous.

At the heart of MMT is an accounting tautology, that: –

G − T = S – I

Where G = Government spending, T = Taxation, S = Savings and I = Investment

In other words…

Government Budget Deficit = Net Private Saving

You may be getting the feeling that something does not quite tally. Robert Murphy of the Mises Institute – The Upside-Down World of MMT explains it like this (the emphasis is mine): –

When I first encountered such a claim — that the government budget deficit was necessary to allow for even the mathematical possibility of net private-sector saving — I knew something was fishy. For example, in my introductory textbook I devote Chapter 4 to “Robinson Crusoe” economics.

To explain the importance of saving and investment in a barter economy, I walk through a simple numerical example where Crusoe can gather ten coconuts per day with his bare hands. This is his “real income.” But to get ahead in life, Crusoe needs to save — to live below his means. Thus, for 25 days in a row, Crusoe gathers his ten coconuts per day as usual, but only eats eight of them. This allows him to accumulate a stockpile of 50 coconuts, which can serve as a ten-day buffer (on half-rations) should Crusoe become sick or injured.

Crusoe can do even better. He takes two days off from climbing trees and gathering coconuts (with his bare hands), in order to collect sticks and vines. Then he uses these natural resources to create a long pole that will greatly augment his labor in the future in terms of coconuts gathered per hour. This investment in the capital good was only possible because of Crusoe’s prior saving; he wouldn’t have been able to last two days without eating had he not been able to draw down on his stockpile of 50 coconuts.

This is an admittedly simple story, but it gets across the basic concepts of income, consumption, saving, investment, and economic growth. Now in this tale, I never had to posit a government running a budget deficit to make the story “work.” Crusoe is able to truly live below his means — to consume less than his income — and thereby channel resources into the production of more capital goods. This augments his future productivity, leading to a higher income (and hence consumption) in the future. There is no trick here, and Crusoe’s saving is indeed “net” in the sense that it is not counterbalanced by a consumption loan taken out by his neighbor Friday…

When MMTers speak of “net saving,” they don’t mean that people collectively save more than people collectively borrow. No, they mean people collectively save more than people collectively invest.

MMT goes on to solve the problem of achieving full employment by introducing a job guarantee and wage controls.

If, by this stage, you feel the need for an antidote to MMT, look no further than, Forty Centuries of Wage and Price Controls: How Not to Fight Inflation by Dr Eamon Butler of the ASI. Published in 1978, it documents the success of these types of policy during the past four thousand years.

Conclusion and Investment Opportunities

The radical ideas contained in MMT are unlikely to be adopted in full, but the idea that fiscal expansion is non-inflationary provides succour to profligate politicians of all stripes. Come the next hint of recession, central banks will embark on even more pronounced quantitative and qualitative easing, safe in the knowledge that, should they fail to reignite their economies, government mandated fiscal expansion will come to their aid. Long-term bond yields will head towards the zero-bound – some are there already. Debt to GDP ratios will no longer trouble finance ministers. If stocks decline, central banks will acquire them: and, in the process, the means of production. This will be justified as the provision of permanent capital. Bonds will rise, stocks will rise, real estate will rise. There will be no inflation, except in the price of assets.

John Mauldin describes the end-game of the debt-explosion as the Great Reset, but if government borrowing costs are zero (or lower) the Great Reset can be postponed, but the economy will suffer from low productivity growth due to malinvestment.