With another $1.9trln of US fiscal relief set to be voted through, attention is likely to switch back to Europe. This article from August 2020 seems relevant to the debate.

Eurozone

Brexit, Grexit and the rise and fall and rise again of the Euro

Macro Letter – No 54 – 06-05-2016

Brexit, Grexit and the rise and fall and rise again of the Euro

- Should the UK leave the EU, Euro volatility will follow

- If the UK remains, the Euro experiment might still be scuppered

- The problems of the EU periphery are not solved by the UK remaining

Whilst the majority of articles between now and the 23rd June will focus on whether the UK will leave or remain in the EU and what this might mean, I want to consider the impact Brexit is likely to have on the long-run fortunes of the Euro.

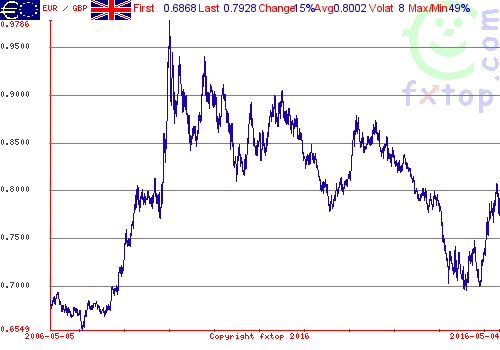

Since December 2008 the EURGBP has fallen from 0.979 to a low of 0.694 in July 2015. Since the end of last year concern, about the outcome of a UK referendum on whether to remain or leave the EU, has seen the EUR strengthen to 0.810 – just over a 38.2% retracement. The UK economy has already begun to show signs of economic slowdown due to uncertainty. A vote to leave is likely to have a negative impact on the GBP, initially, if for no other reason than the continuation of uncertainty; neither the government nor the opposition has presented a road map for exit should the electorate decide to leave. In the event of a UK departure I could envisage a move back to 0.865 or even 0.971:-

Source: fxtop.com

I believe the impact on the UK economy of Brexit would therefore be a substantial weakening of the GBP, a rise in UK inflation and an initial slowing of economic growth. Our exports would rise and our imports would decline, improving our trade balance. Those European countries for whom the UK is their largest export market would suffer.

The cost of the UK leaving the EU would not stop there. The UK is the second largest member of the union. In terms of the economic and political strength of the EU, Britain’s inclusion is significant. By leaving the Schengen Agreement area we would impose higher costs on the remaining members, potentially hastening its interruption or demise. The ECIPE Five Freedom Project – The Cost of Non-Schengen for the Single Market published this week, provides an alarming vision of what that cost to EU growth might be:-

If Schengen would be suspended for the two-year period or even in full, trade and economic growth in the EU could be severely damaged. The Schengen Agreement is not just a symbol of European integration, it creates real economic value by facilitating cross-border exchange. Obviously, the Schengen Agreement promotes the free movement of people, but that is not all. It also boosts the flow of goods, services and capital across borders.

…In 2015 intra-EU trade in goods made up for approximately 60% of the EU’s overall trade.

…The Bertelsmann Stiftung estimated the impact of reintroduced border controls on the EU’s gross domestic product (GDP). Border checks which stop and control trucks cause time delays which increase transport costs and lead to higher product prices. According to their results these higher product prices can cause a yearly reduction in GDP growth of 0.04 percentage points compared to intra-EU trade with open borders. Furthermore, the study argues that the time delays at the border would make just-in-time production and decentralized production more difficult for European firms. As a result, production costs for intra-European value chains would increase and the price competitiveness of European producers would decrease. This could affect location and investment decisions by foreign firms.

A recent Ifo study finds that for EU member states the removal of border controls leads to an increase of 3.8% in goods trade or a cost saving equivalent to a tariff reduction of 0.7 percentage points for every internal border which a good needs to cross. As a result, countries which are at the periphery of the Schengen Area benefit more from the Agreement because their costs savings are greater if goods have to cross several borders until they reach their markets.

Such an integral pillar of EU membership as the Schengen Agreement may not be suspended, but concerns about the indebtedness of some of the more profligate peripheral countries is likely to return to the fore by the summer. As reported earlier this week by Reuters – Greek bank stocks could rise 90 percent on bailout cash deal: Morgan Stanley:-

…upgraded Greek banks to “overweight” saying current valuations did not reflect the compression in bond yield spreads that would follow a deal with Athens’ lenders and took an overly pessimistic view on the banks’ return on equity targets.

The Economist – The threat of Grexit never really went away sees it rather differently: –

Greece badly needs the next dollop of the €86 billion ($99 billion) bail-out creditors promised it last summer, in exchange for promises of austerity and reform. But it will not get the money until the creditors complete a review of its progress, which has been dragging on since November. The government has scraped together enough cash (by raiding independent public agencies) to pay salaries and pensions in May, perhaps even in June. But by July 20th, when a bond worth more than €2 billion matures, the country once again faces default and perhaps a forced exit from the euro zone. The threat of Grexit is not exactly back; it never really went away.

Meanwhile the creation of the “Atlas Fund” which will purchase non-performing loans of Italian banks which are in distress, appears to have averted the, potentially fatal, run on the Italian banking system which was developing earlier this year. Bruegel – Italy’s Atlas bank bailout fund: the shareholder of last resort takes up the story:-

Italy’s new bank fund Atlas might be what is needed in the short run, but in the longer term the fund will increase systemic risk. What ultimately matters is how this initiative will affect the quality of bank governance, a key issue for the future resilience of the system.

…The Atlas fund has a heavy task, although probably not as heavy as that of its mythological namesake. In the short run, it might be what most commentators have described: an imperfect but needed second-best way to avoid bail-in and resolution, matching repeated calls from the Bank of Italy for a revision of the Bank Recovery and Resolution Directive (BRRD) framework after Italy negotiated and approved it.

However, by acting as a bank shareholder of last resort the fund increases systemic risk in the longer term, weakening the stronger banks and involving a publicly controlled institution whose main source of funding is postal savings into a rather risky venture.

While it’s unclear whether the aim is to keep foreign capital out of the Italian banking system, what ultimately matters is how this initiative will affect (or avoid affecting) the quality of bank governance, a key issue for the future resilience of the system. Regardless of whether we think that keeping weak banks alive at all costs is a good idea, the idea of such a shareholder of last resort appears at odds with the aim of making progress towards a solid European Banking Union.

Conclusion

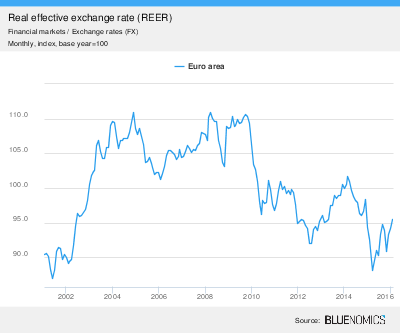

The implications of a UK exit from the EU would, initially, lead to a strengthening EURGBP, although not necessarily EURUSD. This will be followed by a period of increased uncertainty about the survival of the Eurozone (EZ) during which the EUR will decline against its main trading partners. The chart below shows the Euro effective Exchange rate over the last 15 years:-

Source: Bluenomics, Eurostat

Once the first country leaves the EZ, sentiment will change once more. Investors will realise that the departure of the periphery strengthens the prospects of the currency union for those countries which remain; the EUR will begin to look less like a Drachma and more like a Deutschemark. The 2009 highs on the chart above will be within reach and a long-term trajectory similar to, though less steep than, the path of the CHF could become the norm.

For those who thrive on market volatility, over the next few years, opportunities to trade the EUR will be golden.

Quantitative to qualitative – is unelected nationalisation next?

Macro Letter – No 52 – 08-04-2016

Quantitative to qualitative – is unelected nationalisation next?

- Negative interest rates are reducing the velocity of circulation

- Qualitative easing is on the rise

- Liquidity in government bond markets continues to decline

- A lack of liquidity in equity markets will be next

Last year, in a paper entitled The Stock Market Crash Really Did Cause the Great Recession – Roger Farmer of UCLA argued that the collapse in the stock market was the cause of the Great Recession:-

In November of 2008 the Federal Reserve more than doubled the monetary base from eight hundred billion dollars in October to more than two trillion dollars in December: And over the course of 2009 the Fed purchased eight hundred billion dollars worth of mortgage backed securities. According to the animal spirits explanation of the recession (Farmer, 2010a, 2012a,b, 2013a), these Federal Reserve interventions in the asset markets were a significant factor in engineering the stock market recovery.

The animal spirits theory provides a causal chain that connects movements in the stock market with subsequent changes in the unemployment rate. If this theory is correct, the path of unemployment depicted in Figure 8 is an accurate forecast of what would have occurred in the absence of Federal Reserve intervention. These results support the claim, in the title of this paper, that the stock market crash of 2008 really did cause the Great Recession.

Central banks (CBs) around the globe appear to concur with his view. Their response to the Great Recession has been the provision of abundant liquidity – via quantitative easing – at ever lower rates of interest. They appear to believe that the recovery has been muted due to the inadequate quantity of accommodation and, as rates drift below zero, its targeting.

The Federal Reserve (Fed) was the first to recognise this problem, buying mortgages as well as Treasuries, perhaps guided by the US Treasury’s implementation of TARP in October 2008. The Fed was fortunate in being unencumbered by the political grid-lock which faced the European Central Bank (ECB). They acted, aggressively and rapidly, hoping to avoid the policy mistakes of the Bank of Japan (BoJ). The US has managed to put the great recession behind it. But at what cost? Only time will tell.

Other major CBs were not so decisive or lucky. In the immediate aftermath of the sub-prime crisis the Swiss Franc (CHF) rose – a typical “safe-haven” reaction. The SNB hung on grimly as the CHF appreciated, especially against the EUR, but eventually succumbed to “the peg” in September 2011 after the Eurozone (EZ) suffered its first summer of discontent. It was almost a year later before ECB President Draghi uttered his famous “Whatever it takes” speech on 26th July 2012.

Since 2012 government bond yields in the EZ, Switzerland, Japan and the UK have fallen further. In the US yields recovered until the end of 2013 but have fallen once more as international institutions seek yield wherever they can.

By 2013 CBs had begun to buy assets other than government bonds as a monetary exercise, in the hope of simulating economic growth. Even common stock became a target, since they were faced with the same dilemma as other investors – the need for yield.

In late April 2013 Bloomberg – Central Banks Load Up on Equities observed:-

Central banks, guardians of the world’s $11 trillion in foreign-exchange reserves, are buying stocks in record amounts as falling bond yields push even risk-averse investors toward equities.

In a survey of 60 central bankers…23 percent said they own shares or plan to buy them. The Bank of Japan, holder of the second-biggest reserves, said April 4 it will more than double investments in equity exchange-traded funds to 3.5 trillion yen ($35.2 billion) by 2014. The Bank of Israel bought stocks for the first time last year while the Swiss National Bank and the Czech National Bank have boosted their holdings to at least 10 percent of reserves.

…The SNB allocated 82 percent of its 438 billion Swiss francs ($463 billion) in reserves to government bonds in the fourth quarter, according to data on its website. Of those securities, 78 percent had the top, AAA credit grade and 17 percent were rated AA.

…The survey of 60 central bankers, overseeing a combined $6.7 trillion, found that low bond returns had prompted almost half to take on more risk. Fourteen said they had already invested in equities or would do so within five years.

…Even so, 70 percent of the central bankers in the survey indicated that equities are “beyond the pale.”

…the SNB has allocated about 12 percent of assets to passive funds tracking equity indexes. The Bank of Israel has spent about 3 percent of its $77 billion reserves on U.S. stocks.

…the BOJ announced plans to put more of its $1.2 trillion of reserves into exchange-traded funds this month as it doubled its stimulus program to help reflate the economy. The Bank of Korea began buying Chinese shares last year, increasing its equity investments to about $18.6 billion, or 5.7 percent of the total, up from 5.4 percent in 2011. China’s foreign-exchange regulator said in January it has sought “innovative use” of its $3.4 trillion in assets, the world’s biggest reserves, without specifying a strategy for investing in shares.

Reserves have increased at a slower pace since 2012, but the top 50 countries still accounted for $11.4trln, according to the latest CIA Factbook estimates. The real growth has been in emerging and developing countries – according to IMF data, since 2000, in the wake of the Asian crisis, their reserves grew from $700bln to above $8trln.

By June 2014 the Financial Times – Beware central banks’ share-buying sprees was sounding the alarm:-

An eye-catching report this week said that “a cluster of central banking investors has become major players on world equity markets”. An important driver was revenues foregone on bond portfolios.

Put together by the Official Monetary and Financial Institutions Forum, which brings together secretive and normally conservative central bankers, the report’s conclusions have authority. Some equity buying was in central banks’ capacity as, in effect, sovereign wealth fund managers. China’s State Administration of Foreign Exchange, which has $3.9tn under management, has become the world’s largest public sector holder of equities.

The boundary, however, with monetary policy making is not always clear. According to the Omfif report, China’s central bank itself “has been buying minority equity stakes in important European companies”.

…Central bank purchases of shares are not new. The Dutch central bank has invested in equities for decades. The benchmark for its €1.4bn portfolio is the MSCI global developed markets index.

The Italian, Swiss and Danish central banks also own equities. Across Europe, central banks face pressures from cash-strapped governments to boost income. As presumably cautious and wise investors, they have also been put in charge of managing sovereign wealth funds – Norway’s, for instance.

…the Hong Kong Monetary Authority launched a large-scale stock market intervention in 1998, splashing out about $15bn – and ended up making a profit. Since the Asian financial crisis of that year, official reserves have expanded massively – far beyond what might be needed in future financial crises or justified by trade flows.

The article goes on to state that CB transparency is needed and that it should be made clear whether the actions are monetary policy or investment activity. Equities are generally more volatile than bonds – losses could lead to political backlash, or worse still, undermine the prudent reputation of the CB itself.

Here is an example of just such an event, from July last year, as described by Zero Hedge – The Swiss National Bank Is Long $94 Billion In Stocks, Reports Record Loss Equal To 7% Of Swiss GDP:-

…17%, or CHF91 ($94 billion) of the foreign currency investments and CHF bond investments assets held on the SNB’s balance sheet are foreign stocks…

…In other words, the SNB holds 15% of Switzerland’s GDP in equities!

Zero Hedge goes on to remonstrate against the lack of transparency of other CBs equity investment balances – in particular the Fed.

The ECB, perhaps due to its multitude of masters, appears reluctant to follow the lead of the SNB. In March 2015 it achieved some success by announcing that it would buy Belgian, French, Italian and Spanish bonds, under its QE plan, in addition to those of, higher rated, Finland, Germany, Luxembourg and the Netherlands. EZ Yield compression followed with Italy and Spain benefitting most.

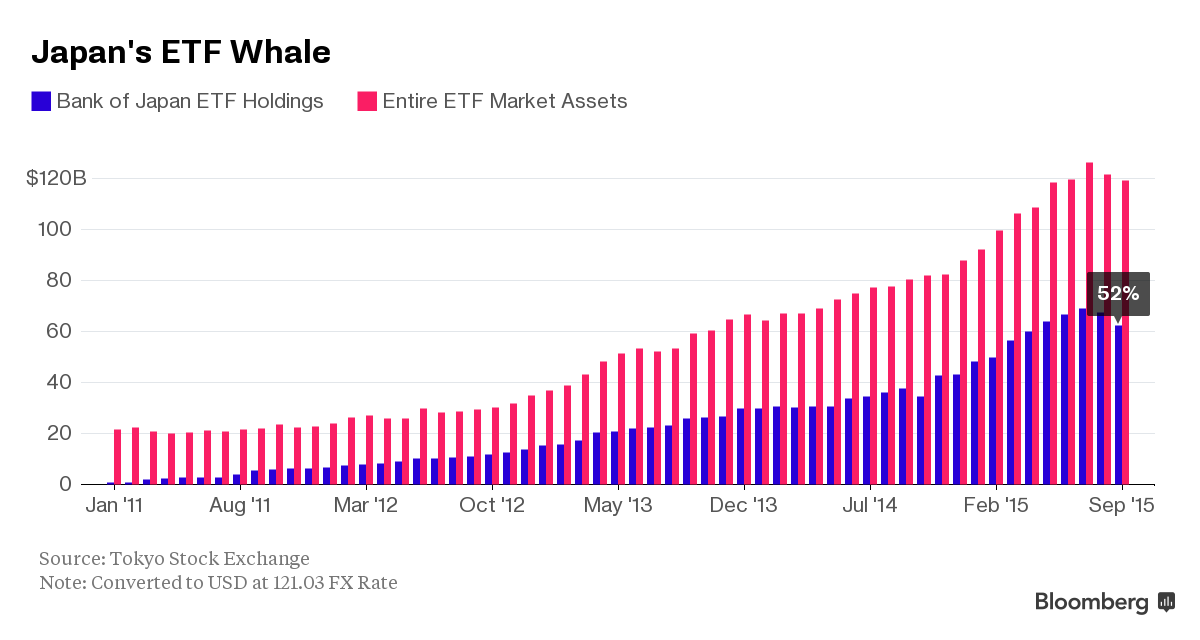

The leading exponent of this “new monetary alchemy” is the BoJ. In an October 2015 report from Bloomberg – Owning Half of Japan’s ETF Market Might Not Be Enough for Kuroda the author states:-

With 3 trillion yen ($25 billion) a year in existing firepower, the BOJ has accumulated an ETF stash that accounted for 52 percent of the entire market at the end of September, figures from Tokyo’s stock exchange show.

…Japan’s central bank began buying ETFs in 2010 to spur more trading and promote “more risk-taking activity in the overall economy.” Governor Haruhiko Kuroda expanded the program in April 2013 and again last October.

Source: Bloomberg, TSE

More ETFs can be created to redress the balance, or the BoJ may embark on the purchase of individual stocks. They announced a small increase in ETF purchases in December, focused on physical and human capital firms – also advising that shares they bought from distressed financial institutions in 2002 will be sold (very gradually) at the rate of JPY 300bln per annum over the next decade. At the end of January the BoJ decided to adopt negative interest rate policy (NIRP) rather than expand ETF and bond purchases – this saw the Nikkei hit its lowest level since October 2014 whilst the JYP shed more than 8% against the US$. I anticipate that they will soon increase their purchases of ETFs or stocks once more. The NIRP decision was half-hearted and BoJ concerns, about corporates and individuals resorting to cash stashed in safes, may prove well founded – So it begins…Negative Interest rates Trickle Down in Japan – Mises.org discusses this matter in greater detail.

In early March the ECB acted with intent, CNBC – ECB pulls out all the stops, cuts rates and expands QE takes up the story:-

…the ECB announced on Thursday that it had cut its main refinancing rate to 0.0 percent and its deposit rate to minus-0.4 percent.

“While very low or even negative inflation rates are unavoidable over the next few months as a result of movement in oil prices, it is crucial to avoid second-round effects,” Draghi said in his regular media conference after the ECB statement.

…The bank also extended its monthly asset purchases to 80 billion euros ($87 billion), to take effect in April.

…the ECB will add corporate bonds to the assets it can buy — specifically, investment grade euro-denominated bonds issued by non-bank corporations. These purchases will start towards end of the first half of 2016.

…the bank will launch a new series of four targeted longer-term refinancing operations (TLTROs) with maturities of four years, starting in June.

The Communique from the G20 meeting in Shanghai alluded to the need for increased international cooperation, but it appears that a sub-rosa agreement may have been reached to insure the Chinese did not devalue the RMB – in return for a cessation of monetary tightening by the Fed.

In an unusually transparent move, a report appeared on March 31st on Reuters – China forex regulator buys $4.2 bln in stocks via new platform:-

Buttonwood Investment Platform Ltd, 100 percent owned by the State Administration of Foreign Exchange (SAFE), and Buttonwood’s two fully-owned subsidiaries, have bought shares in a total of 13 listed companies, the newspaper reported, citing top 10 shareholder lists in the companies latest earnings reports.

Shanghai Securities News said the investments are part of SAFE’s strategy to diversify investment channels for the country’s massive foreign exchange reserves.

Recent earnings filings show Buttonwood is among the top 10 shareholders of Bank of China, Bank of Communications , Shanghai Pudong Development Bank , Everbright Securities and Industrial and Commercial Bank of China.

Conclusions and investment opportunities

The major CBs are beginning to embrace the idea of providing capital to corporates via bond or stock purchases. With next to no yield available from government bonds, corporate securities appear attractive, especially when one has the ability to expand ones balance sheet, seemingly, without limit.

The CBs are unlikely to buy when the market is strong but will provide liquidity in distressed markets. Once they have purchased securities the “free-float” will be almost permanently reduced. The lack of, what might be termed, “trading liquidity”, which has been evident in government bond markets, is likely to spill over into those corporate bonds and ETFs where the CBs hold a significant percentage. In the UK, under our takeover code, a 30% holding in a stock would obligate the holder to make an offer for the company – the 52% of outstanding ETFs held by the BoJ already seems excessive.

The ECB has plenty of government, agency and corporate bonds to purchase, before it moves on to provide permanent equity capital. The BoE and the Fed are subject to less deflationary forces; they will be the last guests to arrive at the “closet nationalisation” party. The party, nonetheless, is getting underway. Larger companies will benefit to a much greater extent than smaller listed or unlisted corporations because the CBs want to appear to be “indiscriminate” buyers of stock.

As the pool of available bonds and stocks starts to dry up, trading liquidity will decline – markets will become more erratic and volatile. Of greater concern in economic terms, malinvestment will increase; interest rates no longer provide signals about the value of projects.

For stocks, higher earning multiples are achievable due to the rising demand for equities from desperate investors with no viable “yield” alternative. CBs are unelected stewards on whom elected governments rely with increasing ease. For notionally independent CBs to purchase common stock is de facto nationalisation. The economic cost of an artificially inflated stock market is difficult to measure in conventional terms, but its promotion of wealth inequality through the sustaining of asset bubbles will do further damage to the fabric of society.

The Scotian experiment and European fragmentation

Macro Letter – No 21 – 10-10-2014

The Scotian experiment and European fragmentation

- Scotland voted to remain part of the Union but the devolution debate doesn’t end there

- Further European integration risks breaking the European Union

- Economic growth in the UK and Eurozone will be damaged by long-term uncertainty

The Scottish decision to remain part of the Union, by such a slim margin – 55% to 45% on an 85% turnout – caught me by surprise. On reflection it should not have been unexpected – it was as much about the “hearts” as the “minds” of the Scottish electorate. Now that the dust has settled, I wonder what this vote means for the United Kingdom and for other regions of Europe.

In this month’s issue of The World Today, Chatham House – A result that resolves little Malcolm Chambers – Research Director at the Royal United Services Institute (RUSI) made the following observations: –

The Scottish referendum was supposed to settle the UK’s constitutional uncertainties, but the result has raised more questions than it answers. How Britain addresses the devolution issue and the question mark over its commitment to Europe will shape perceptions of its ability to wield influence and hard power abroad for years to come.

Britain’s 2010 National Security Strategy, published shortly after the coalition government took office, was entitled ‘A Strong Britain in an Age of Uncertainty’. It made no mention of the two existential challenges – the possible secession of Scotland from the United Kingdom, and the risk of a British withdrawal from the European Union. Yet either event would be a fundamental transformation in the very nature of the British state, with profound impact on its foreign and security policy.

The article goes on to discuss the promises made to Scotland by Westminster’s political elite, from all the main parties, which may now create the conditions for eventual independence: –

Devolution max could have a similar effect, making the final step from ‘devo-max’ to ‘indy-light’ appear less traumatic, even as it still allows Westminster to be blamed for any ills that remain. If a further referendum is to be avoided five or ten years from now, it will not be enough to make constitutional changes.

Prime Minister Cameron took the opportunity to raise the issue of Scottish MPs voting on English issues; whilst this was politically expedient, it sows the seeds for regional calls for devolution of power to the poorer areas of Britain: –

Yet growing awareness of the constitutional imbalances created by devolution to Scotland – and, to a lesser extent, to Wales and Northern Ireland – is creating a series of shockwaves that will not dissipate easily. The UK, as a result, could now see a long period of constitutional experimentation and controversy, with profound effects on the governance of the country as a whole.

Chambers then turns to investigate the “European Question”. Here he sees a parallel between the UKs relationship with the EU and the Scottish desire for independence: –

Britain’s relationship with the European Union is similar, in important respects, to Scotland’s position in the United Kingdom. It has a special financial arrangement, involving a rebate of most of its net contribution, that is not available to other member states. It retains its own currency and border controls, and has a permanent exemption from the common currency and passport-free travel to which other states have agreed. As in Scotland, there is strong political pressure for the UK to be allowed special treatment in further areas, such as immigration controls. In both cases, attempts to construct ‘variable geometry’ governance frameworks are made more difficult by the asymmetry in size between the opting-out nation and the political union as a whole.

From the Brussels’ perspective the issue of devolution is not just restricted to the “Sceptred Isle”: –

While the nature of the Britain’s constitutional crises is unique, they are part of a wider crisis of European politics. Over the past five years, the eurozone has faced successive crises as it has sought to find a way to reconcile vast differences in economic interest and viewpoint between its member states. Relations between Germany and the southern states have worsened as the former takes on a more openly hegemonic role.

Without further significant sharing of political sovereignty – for example through a banking union – the risk that one or more member states could leave the eurozone will remain very substantial. Yet further political integration could bring its own challenges, with powerful nationalistic parties in northern Europe already pushing against those who argue that all the answers must come from Brussels. One of the reasons that Britain’s European allies were so worried about the Scotland vote was precisely their concern as to the example that a Yes vote could have sent to separatist movements in Spain, Belgium, Italy or Bosnia. This concern will not have been entirely dissipated, both because of the precedent set by London’s willingness to hold the vote, and by the closeness of the margin.

In conclusion Chambers states: –

It is still far from likely that the United Kingdom will perish, or that it will abandon its commitment to the European Union. But the possibility of one or both of these separations taking place seems set to be a central part of British politics for a decade or more.

The impact on Sterling

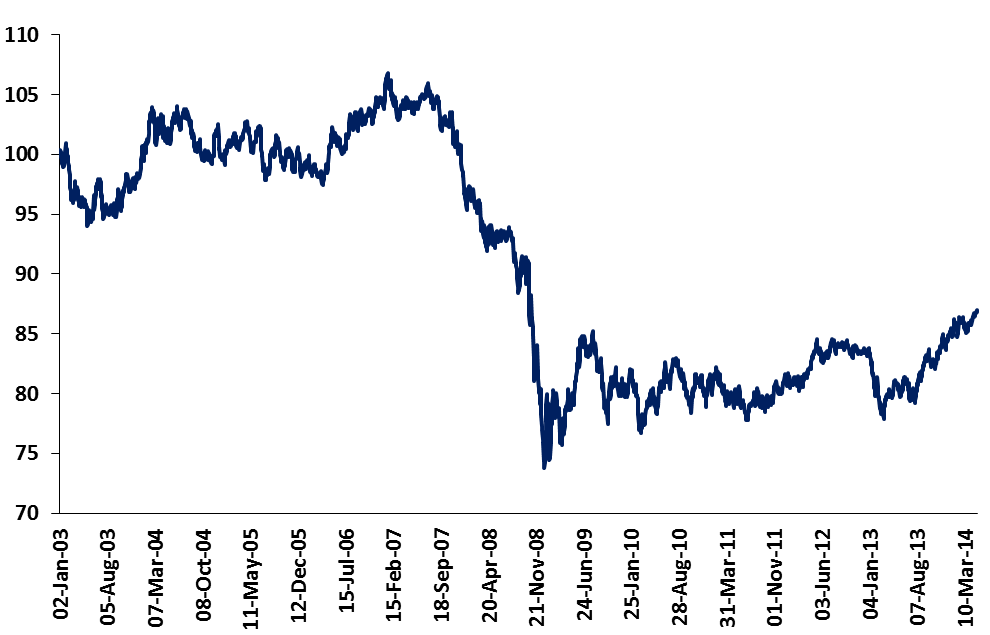

Sterling is still some way below its longer-term average on a trade weighted basis as this chart of the Sterling Effective Exchange Rate (ERI) Index shows, however, it’s worth noting that the average between 1994 and 2013 is around 90: –

Source: Bank of England

Uncertainty always undermines the stability of ones currency and the Scottish referendum was no different, although its impact proved relatively minor. In a recent speech, Bank of England – The economic impact of sterling’s recent moves: more than a midsummer night’s dream – Kristin Forbes – MPC member, downplayed what could have been a dramatic decline in the value of the GBP:-

There has been some volatility in sterling recently, especially around the time of the Scottish referendum, but sterling is currently only 1% weaker than its recent peak in July 2014.

In her conclusion she points to the appreciation of the GBP since the Great Recession and cautions those who fail to anticipate the negative inflationary consequences of a weaker exchange rate: –

Where sterling’s recent moves may have had the greatest economic impact is on prices and inflation. A “top down” analysis estimating the pass-through from exchange rate movements to prices suggests that the lagged effect of sterling’s appreciation during 2013 and early 2014 may have acted as a powerful dampening effect on inflation. Although model simulations may be overestimating the magnitude of the effect, sterling’s past moves have reduced the risk of inflation increasing sharply, despite the strong growth in employment and the overall economy.

This dampening effect of sterling’s past appreciation, however, will peak at the end of 2014 and then begin to fade. As a result, it is becoming increasingly important to monitor trends in domestically-generated inflation – and especially unit labour costs – so that monetary policy can be adjusted appropriately and also be allowed to work through the economy with its own set of lags. Unfortunately, understanding recent trends in the domestic component of inflation – especially the slow growth in wages – has been challenging. A “bottom up” analysis of inflation that focuses on current measures of domestically-generated inflation (which attempt to minimize the dampening effect of sterling’s moves) show price pressures that are well contained and little evidence of imminent inflationary risks.

These “bottom up” indicators present a very different story then the “top down” estimates of inflation after adjusting for sterling’s recent appreciation. Has sterling’s appreciation had less of a dampening effect on prices than has traditionally occurred – perhaps due to structural changes in the UK or global economy? Or are the measures of domestic inflation understating current inflationary risks – perhaps due to the long lags before timely data is available? To answer these questions, it is critically important to monitor measures of prospective inflation to determine the appropriate path for monetary policy.

If concern about political devolution of power to the regions, at the expense of the power-house of the UK’s South East, and expectation of rising Euro-scepticism, are destined to be the pre-eminent political issues for the next decade, then an appreciation in the value of Sterling is likely to be tempered. Since the UK economy is closely integrated to Europe this persistent undervaluation will be less obvious in the GBP/EUR exchange rate but hopes of the trade weighted value of GBP rising like the USD due to structurally stronger growth will be muted.

In the aftermath of the referendum RUSI – Never the Same Again – What the Referendum Means for the UK and the World – observed:-

Having, for the first time, looked at what a ‘yes’ vote might mean for them, private investors and businesses are now more sensitised than ever before to the risks that a further referendum could pose. If some of them were to begin to hedge their bets accordingly, there could be a risk of an extended period of underinvestment in Scotland, with serious consequences for its prosperity.

Better together?

The campaign slogan of the Westminster elite was “Better Together” but, setting aside the rhetoric of power hungry politicians, what are the pros and cons of devolution versus Union? Writing ahead of the referendum Adam Posen of the Peterson Institute – The Huge Costs of Scotland Getting Small made a valiant case for continued integration: –

When is it ever a good idea for a small nation to set up on its own? Leaving aside cases of colonization and outright oppression, there is little good reason ever to shrink on the world scene by leaving a larger unit. The internal politics of democracies always get better deals for regions within them than small sovereigns can elicit from identity-ignoring market forces. The few small nations that did gain in welfare by seceding from transnational entities are those that escaped failed autocratic systems. The Baltic countries escaping the former Soviet Union’s dominance can be seen in this light. But setting out on your own is only beneficial when the system left behind has directly constrained your nation’s human potential. Whatever else, that cannot be said of the current Scottish situation in the United Kingdom.

It is a fact of life in today’s world that a small economy on its own is always buffeted by the forces of the global economy more than a region within a larger union. Even well-run small states like Singapore and Estonia are subject to huge swings in their economy resulting from capricious capital flows in and out. These swings disrupt employment, investment, and competitiveness via real exchange rate fluctuations. More important, small economies are fundamentally undiversified because of their small scale, and they risk their specializations falling out of favor in world markets. Events beyond their control can overwhelm the small nation’s high value-added industries, no matter how good it is at those things, be they oil extraction or banking or whisky distilling. Scottish independence in form will instead mean increased vulnerability in fact, because, inherently, smaller means more exposure when the markets turn—and turn they will.

…The economic debate over independence has tended to focus on the one-time transfer costs: setting up a new government administration, apportioning the accumulated public debt, grabbing as much oil as possible. But these issues are of minimal importance, however one chooses to measure them, compared to the ongoing costs of permanently greater insecurity to households and businesses. Even if an independent Scotland were to start out with the Scottish National Party (SNP) fantasy of relatively low public debt and a relatively high share of remaining oil revenues, it would have to save more, pay higher interest rates, and keep more space in its budget for self-insurance, hampered by a narrow tax base, in order to cope with the vicissitudes of the global economy on its own.

When one looks at the economic austerity foisted on the population of Greece and at the hopeless prospects much of the unemployed youth of Europe I wonder whether there is an alternative to the “integrationist” approach.

Looking for an answer I went back to the forging of the United Kingdom. This is how John Lancaster describes the events which led to the Act of Union in 1707:-

During the 17th century, Scottish investors had noticed with envy the gigantic profits being made in trade with Asia and Africa by the English charter companies, especially the East India Company. They decided that they wanted a piece of the action and in 1694 set up the Company of Scotland, which in 1695 was granted a monopoly of Scottish trade with Africa, Asia and the Americas. The Company then bet its shirt on a new colony in Darien – that’s Panama to us – and lost. The resulting crash is estimated to have wiped out a quarter of the liquid assets in the country, and was a powerful force in impelling Scotland towards the 1707 Act of Union with its larger and better capitalised neighbour to the south. The Act of Union offered compensation to shareholders who had been cleaned out by the collapse of the Company; a body called the Equivalent Society was set up to look after their interests. It was the Equivalent Society, renamed the Equivalent Company, which a couple of decades later decided to move into banking, and was incorporated as the Royal Bank of Scotland. In other words, RBS had its origins in a failed speculation, a bail-out, and a financial crash so big it helped destroy Scotland’s status as a separate nation.”

The above passage, taken from Lancaster’s 2009 book It’s Finished, is quoted near the opening of a recent article by Tim Price – Let’s Stick Together in which he refers to Leopold Kohr – The Breakdown of Nations. The forward by Kirkpatrick Sale describes the problem of size when nation building: –

What matters in the affairs of a nation, just as in the affairs of a building, say, is the size of the unit. A building is too big when it can no longer provide its dwellers with the services they expect – running water, waste disposal, heat, electricity, elevators and the like – without these taking up so much room that there is not enough left over for living space, a phenomenon that actually begins to happen in a building over about ninety or a hundred floors. A nation becomes too big when it can no longer provide its citizens with the services they expect – defence, roads, post, health, coins, courts and the like – without amassing such complex institutions and bureaucracies that they actually end up preventing the very ends they are intending to achieve, a phenomenon that is now commonplace in the modern industrialized world. It is not the character of the building or the nation that matters, nor is it the virtue of the agents or leaders that matters, but rather the size of the unit: even saints asked to administer a building of 400 floors or a nation of 200 million people would find the job impossible.

Kohr grew up in a small village which may have helped him to recognise one of the intrinsic weaknesses of democracy: that it works best on a small scale.

Taking this theme further and applying it to an independent Scotland, John Butler – From bravery to prosperity: A six-year plan to make Scotland the wealthiest Anglosphere region of all makes the case for a smaller more flexible approach. Here is an abbreviated version of his six point plan:-

Debt Repayment

The Scots’ legendary bravery is equalled by legendary parsimony, the first essential element of success. There is no growth without investment and no sustainable investment without savings. It stands to reason that you aren’t a parsimonious society if you carry around a massive, accumulating national debt. Debt service is also a drag on future growth. Thus if the Scots want to prosper long-term, they are going to need to pay down their share of the UK national debt.

Tax Reduction

There are several policies that would quickly create an investment boom. Most important, Scotland should do better than celtic rival Ireland, with a low corporate tax rate, and abolish the corporate income tax altogether. Yes, you read that right: The effective corporate income tax in many countries now approaches zero anyway, due to all manner of creative cross-border accounting.

Human Capital

Developing human capital, at which the Scots excelled in the 19th century, is the third element. Consider which industries are most likely to relocate to Scotland: Those requiring neither natural resources nor extensive industrial infrastructure, that is, those comprised primarily of human capital. Although financial services comes to mind, there is tremendous overcapacity in this area in England and Ireland, including in unproductive yet risky activities, so that is better left to the English and Irish for now. Better would be to concentrate on health care, for example, an industry faced with soaring costs and stifling regulation in much of the world.

Scotland could, inside of six years, become the world’s premier desination for so-called ‘healthcare tourism’. Scotland lies directly under some of the world’s busiest airline routes, an ideal location.

Sound Banking

A fourth essential element to success is to implement Scottish Enlightenment principles for sound banking. This is of utmost importance due to the potential monetary and financial instability of the UK and much of the broader Anglosphere.

As a first step, Scotland should forbid any bank from conducting business in Scotland if they receive any direct financial assistance from the Bank of England or from the UK government. In turn, Scotland should make clear to Westminster that Scottish residents will not contribute to any taxpayer bail out of any UK financial institution. No ‘lender of last resort’ function will exist for financial activities in Scotland, unless such action, if formally requested by a bank, is approved by the Scots in a referendum. (Taxpayers are always on the hook for bailouts one way or the other; why not make this explicit?)

Self-Reliance

The fifth element reaches particularly deep into Scottish history: Self-Reliance. Peoples that inhabit relatively inhospitable or infertile lands tend to establish cultures with self-reliance at the core. No, this does not make them culturally backward, but it does tend to contribute to a distrust of foreign or central authority. The Scots, while brave, were frequently disunited in their opposition to English rule, something that had unfortunate consequences for many, not just William Wallace.

Scottish Presbyterianism

Finally, there is the sixth element: the collective cultural traditions of Scottish Presbyterianism. There are few religions in the world that hold not only faith, but hard work, thrift and charity in such high regard as that of traditional Presbyterianism. Yes, as with most all Europeans, the Scots have become more secular in recent decades. But the same could be said of the Germans, who nevertheless cling to their own, solid Protestant work ethic and associated legal and moral anti-corruption traditions.

To be fair to Adam Posen of the Peterson Institute, none of the arguments for a non-integrated Scotland solve the problems of vulnerability to external shocks. The crux of the issue is whether a larger, more integrated unit, is more effective than a smaller more flexible one.

The Politics of Empires

“Power tends to corrupt, and absolute power corrupts absolutely. Great men are almost always bad men.” Lord Acton – 1834-1902.

Throughout history successful nations have grown through expansion and integration. The process is cyclical, however, and success sows the seeds of its own demise. Europe emerged from the dark ages to conquer much of the known world. Since then it has imploded during two world wars and may now be embarking on a further wave of integration. Or, perhaps, this is the last attempt to assimilate a multitude of disparate cultures before the “long withdrawing breath” into smaller, more dynamic, self-reliant units.

In the opening chapter of Edward Gibbon’s “Decline and Fall of the Roman Empire” he says:-

…but it was reserved for Augustus (who became Caesar in BC 44) to relinquish the ambitious design of subduing the whole earth and to introduce a spirit of moderation into the public councils.

However, I believe the seeds of destruction, which eventually created the conditions for the establishment of A NEW Europe, stem from Diocletian’s introduction of the Tetrarchy in AD 284. It divided the Roman Empire in four regions.

Diocletian’s son, Constantine attempted to slow this fragmentation by adopting Christianity as the official religion of the empire, however, his decision to move the seat of government from Rome to Byzantium in AD 324 set the stage for the final schism into the Eastern and Western Empires which occurred in AD395 on the demise of Theodosius.

The Western Empire sustained continuous assaults from Vandals, Alans, Suebis and Visigoths leading to the second sack of Rome in AD 410 by Alaric. The Western Empire finally collapsed in AD 476 when the Germanic Roman general Odoacer deposed the last emperor, Romulus . Europe had descended into a “dark age” of constant wars between rival tribes. The sole pan-European administrative organization after the fall of the Western Empire was the Catholic Church, which adopted the remnants of its infrastructure.

The creation of the Europe we recognise today began with the conversion to Christianity of Clovis – King of the Franks – in AD 498, but it was not until the re-uniting of the Frankish kingdoms in AD 751 under Pepin The Short and the subsequent appointment of his son Charlemagne as Holy Roman Emperor in AD 800 that the idea of a Christian “Western Europe” began to emerge. When viewed from this long historical perspective the current development of the EU is still in its infancy.

In the East, Constantinople remained the administrative center of the Byzantine Empire. Under Emperor Justinian in AD 526 the Empire expanded. Challenges from the Lombards in AD 568 saw the loss of Northern Italy, but the rise of Islam after AD 623 proved a more terminal event. Although Byzantium went into decline, due to many assailants – not least the Western Empire – it limped on until 1453 when it to finally succumbed to the Ottoman Turks.

Why the history lesson? The spark of the industrial revolution was kindled in Europe. It developed out of the chaotic collapse of the Western Roman Empire, the warring between a plethora of tribes and the rise of independent city states. It was built on the fragmented polity of petty fiefdoms and the desire to trade despite national borders and political restrictions on the movement of labour and goods. The renaissance began in Italy where the competition between small city states stimulated “animal spirits”. The flowering of art and culture that this democratisation of prosperity set in motion goes some way to support the idea that “small is beautiful”.

During the dark ages the concept of “Nationhood” was fluid, as exemplified by the Dukes of Normandy’s fealty after 1066 to the King of France, but only in respect of their French domains. As nation states began to coalesce international trade developed further. Nations waxed and waned, alliances were made and broken but no single nation succeeded in dominating the whole region. Demographic growth encouraged voyages of discovery. Colonisation followed, and finally the conditions were propitious for the birth of the industrial revolution from which we continue to benefit today.

These processes were gradual, running their course over many generations. I believe Europe is now fragmenting once more; painful for our own time but filled with promise for future generations. Calls for self-government from many regions within the EU will increase. The more Brussels attempts to make its citizens feel European the more its citizens will yearn for self-determination.

This trend will be driven by a number of factors aside from the declining effectiveness of central government. Bruegal – The Economics of big cities articulates one of these economic paradoxes, how globalisation has made the world more local: –

Local economies in the age of globalization

Enrico Moretti writes that the growing divergence between cities with a well-educated labor force and innovative employers and the rest of world points to one of the most intriguing paradoxes of our age: our global economy is becoming increasingly local. At the same time that goods and information travel at faster and faster speeds to all corners of the globe, we are witnessing an inverse gravitational pull toward certain key urban centers. We live in a world where economic success depends more than ever on location. Despite all the hype about exploding connectivity and the death of distance, economic research shows that cities are not just a collection of individuals but are complex, interrelated environments that foster the generation of new ideas and new ways of doing business.

Enrico Moretti writes that, historically, there have always been prosperous communities and struggling communities. But the difference was small until the 1980’s. The sheer size of the geographical differences within a country is now staggering, often exceeding the differences between countries. The mounting economic divide between American communities – arguably one of the most important developments in the history of the United States of the past half a century – is not an accident, but reflects a structural change in the American economy. Sixty years ago, the best predictor of a community’s economic success was physical capital. With the shift from traditional manufacturing to innovation and knowledge, the best predictor of a community’s economic success is human capital.

Human Capital may be defined as “the skills, knowledge, and experience possessed by an individual or population”. In the internet age this resource can be located almost anywhere and need not be isolated due to email, telephone or video conference technology, however, the advantages of physical proximity and social interaction favour cities.

Another, and related, issue is the increasingly disruptive effect of technology on employment. Bruegal – 54% of EU jobs at risk of computerisation – highlights one of the greatest economic challenges to the social fabric of the EU, but this is a global phenomenon: –

Based on a European application of Frey & Osborne (2013)’s data on the probability of job automation across occupations, the proportion of the EU work force predicted to be impacted significantly by advances in technology over the coming decades ranges from the mid-40% range (similar to the US) up to well over 60%.

Those authors expect that key technological advances – particular in machine learning, artificial intelligence, and mobile robotics – will impact primarily upon low-wage, low-skill sectors traditionally immune from automation. As such, based on our application it is unsurprising that wealthy, northern EU countries are projected to be less affected than their peripheral neighbours.

European governments are caught between the competing needs of an aging population and a younger generation who have little prospect of finding gainful full-time employment. Meanwhile city workers are paying for the regions where unemployment is highest. The tension between “wealth makers” and “wealth takers” are destined to increase.

Conclusion

Scotland voted to remain part of the Union. The Independence campaign was ill prepared failing to consider such issues as what currency they would use or how they would avoid a run on their banking system. The next time the Scots vote – and there will be a next time – I believe they will leave the Union because these questions will have been addressed. Other regions around the UK and Europe have taken note – the spirit of devolution is abroad. Prosperous regions, such as Catalunya and Northern Italy – Padania as it is sometimes called – crave independence from their poorer neighbours. Poorer regions resent the straight jacket of a single currency – be it the GBP for regions like the North East of England or the EUR for Greece and Portugal. To the poorer regions, the flexibility of a floating exchange rate is beguiling; as the EU stumbles through an era of debt laden low growth devolution pressures will increase.

For the GBP and EUR the Scottish “No” vote will fail to diminish the potential for social and political tension. The value of these currencies will reflect that uncertainty. Longer-term foreign direct investment will be lower. This will place an additional burden on EU budgets. A larger percentage of central government spending will be directed to regions where calls for devolution are highest rather than to economically productive projects in more prosperous areas.

European and UK equities are likely to under-perform in this environment whilst the increased indebtedness of EU governments is likely to increase their real borrowing costs.

Will this happen soon and will it be possible to measure? I think it is already happening but, given the very long-term nature of the fragmentation of nations, it will be difficult to measure except during constitutional crises. The shorter-term business cycles will still exist. Trading and investment opportunities will continue to arise. For the investor, however, it is essential to be aware of the risks and rewards which this fragmentation process will present.

A very French revolt

Macro Letter – No 13 – 06-06-2014

A very French revolt

Sur le Pont d’Avignon

L‘on y danse, l’on y danse

Sur le Pont d’Avignon

L’on y danse tous en rond

Last month I spent a few days helping a friend with his business in Avignon. This was a brilliant opportunity to canvass the views of the non-metropolitan French in respect of the current government and the state of the French economy. During my career I have worked closely with Parisian bankers and asset managers. Somewhat like London, Paris is “another country” which happens to be situated in the middle of France. In the provinces they believe in “rendre la vie plus simple”– life rendered easier.

The city of Avignon is close to the tourist heartland of Provence but it is also very much a commercial centre for a wider agricultural region. The above picture is of the famous Pont Saint-Benezet bridge across the Rhone; the bridge collapsed in 1644 and is now a tourist attraction. It is better suited to dancing today than it was at the time of the 15th century childrens’ song, but, as the home of the Pope from 1309 until 1377, the city has a long history as a tourist attraction.

Old Avignon is a beautiful city and a world heritage site. As one wanders around the walled centre,interieur du murs, filled with shops, cafes and restaurants, one is reminded of the French esteem for “La Bonne Vie”. Exterior du murs it is a different story. Large housing projects and, often, poorly maintained properties, bare witness to the, predominantly North African, diaspora who work in agriculture or the service industries, or, in many instances, do not work at all. Avignon is a city of contrasts but it offers a unique window into “real France”. During my visit I spoke to four of the city’s residents:-

- a French engineer who works for a large utility company.

- a French economist working for local government helping immigrant workers find local jobs

- an ex-pat American carpenter who has lived and worked in the region since the 1960’s

- a French national who works in the real-estate and tourist industry

None of them were overwhelmed by the performance of Francois Hollande’s PS (socialist party) government, but, to my surprise, none were surprised by his “about-turn” on economic policy.

Francois Hollande was elected in 2012 on a mandate to “tax and spend” but soon achieved a volte-face. The current policy calls for Eur 50bln of spending cuts over the next three years. These cuts will be concentrated on health and welfare. Public sector wages are to be frozen – though I have no doubt many public sector workers will be promoted to higher pay grades. The headline figure is somewhat misleading since the policy package also incorporates reductions in taxes for employers amounting to some Eur 30bln. Nonetheless, it is unlikely that any other French political party could have achieved as much austerity.

The French electorate seem unimpressed by these policies as witnessed by the rising fortunes of the Front National in the European Elections last month. The rightward swing has been widely reported but I doubt the “protest vote” – which has been seen across the EU – will have much impact except to slow the process of federalisation. Steen Jakobsen – Saxo bank had this to say following the outcome of the vote:-

Across Europe, EU-sceptic voters gained ground, but it could be in vain as the overall majority of the old guard: Conservative, Liberals, Greens and Social Democrat’s still carry 70 percent of the mandates.

…The 751 members of the EU Parliament operate through coalitions of interest across countries and sometimes political standpoint. The final date for submitting a coalition is June 23, and a “coalition” has to be at least 25 members from seven different nations. Here the protest votes can play vital role. The Europe-sceptic vote is divided. The risk is that, similar to the Occupy movement in the US, all lack of common goal, except those of a negative nature, allows the majority get away with ignoring what clearly is a call from the voters to the politicians that Europe is too far away from the daily life of its 500 million citizens.

…The EU “economic police” will be tested. France and Spain is already in violation of budget deficits for 2014 and 2015. The so called “recovery” is actually a stabilisation, not recovery. In history, unions, even primitive ones, fail when economic times turns negative.

The condition of French government finances is not rosy: public debt to GDP is running at 57%. Tax to GDP, at 57%, is the highest in Europe. Meanwhile unemployment is stuck in double digits. The economy has stalled; Q1 GDP was zero and the IMF revised forecast for 2014 is down to 1%. Unsurprisingly, foreign investment into France declined -0.9% during the first quarter.

Employment

Returning to Avignon the issues which most concerned all the “locals” I interviewed were immigration and the standard of living: or perhaps I should say “Quality of Life”. As in many developed countries, immigrants will accept lower pay and take on more menial tasks than the indigenous population. As long as there are higher paid, higher skilled employment opportunities this process frees up scare resources to be employed in productivity enhancing roles. When those opportunities do not exist a country’s standard of living suffers: younger and older workers bare the brunt. In France this effect has been softened by encouraging younger people to study longer, often at the tax payers’ expense. Older workers have been encouraged to retire earlier, again, at the tax payers’ expense.

A recent post from Scott Sumner – How to think about Francemakes some economic comparisons with the USA: –

…So, here are some [2008] ratios of France to the United State:-

GDP per capita: 0.731

GDP per hour worked: 0.988

Employment as a share of population: 0.837

Hours per worker: 0.884

So French workers are roughly as productive as US workers. But fewer Frenchmen and women are working, and when they work, they work fewer hours.

…The bottom line is that France is a society with the same level of technology and productivity as the US, but one that has made different choices about retirement and leisure. Vive la difference!

Professor Sumner observes what von Mises called “Human Action”. He goes on to make some observations about employment protection: –

France has a wide range of policies that reduce aggregate supply:

1. High taxes and benefits, which create high MTRs.

2. High minimum wages and restrictions on firing workers.

What should we expect from these “bad” supply-side policies? I’d say we should expect less work effort at almost every single margin. Earlier retirements, more students staying longer in college, longer vacations, and a higher unemployment rate.

France has always had a reputation for employment protection but overall it is not dramatically different from its larger European neighbour as the OECD – Employment Outlook 2013 reveals in their latest employment protection rankings. Whilst France is above the OECD average (Page 78 – Figure 2.1) it is not that far above Germany.

TheInternational Labour Office –An anatomy of the French labour market – January 2013gives a detailed account employment trends. The rise of temporary labour has been as prevalent in France as in many other countries despite, or perhaps as a result of, its rigid employment laws. The ILO describes this as a Two-tier system which creates a more stringent protective framework for workers on long-term contracts and very limited protection for workers on short-term contracts. According to their report the legislative policies in countries such as France and Spain has led to higher job turnover. Since the 1990’s France has seen a 70% to 90% increase in short-term employment. This trend has accelerated since the Great Recession.

As French government spending falls, the opportunities for longer-term employment, especially for the young and older worker, will be reduced. The ILO continue: –

The share of temporary jobs in the private sector is far higher among young workers aged between 15 and 24 years old than among prime-age workers (25-50) and senior workers (over 50): 39.9 per cent vs. 10.7 per cent and 7.0 per cent in 2010. It is also higher for women (15.2 per cent) than for men (9.1 per cent).

When viewed through the lens of “employment opportunity” the French protest vote at the European Elections is not that surprising. The table below shows the wage inequality between permanent and temporary contracts across Europe, France comes third, behind the Netherlands and Sweden on this measure: –

| Wage premium for permanent contracts for 15 European countries. | |

| Sweden | 44.7 |

| Netherlands | 35.4 |

| France | 28.9 |

| Luxembourg | 27.6 |

| Germany | 26.6 |

| Italy | 24.1 |

| Greece | 20.2 |

| Austria | 20.1 |

| Finland | 19 |

| Ireland | 17.8 |

| Denmark | 17.7 |

| Spain | 16.9 |

| Portugal | 15.8 |

| Belgium | 13.9 |

| United Kingdom | 6.5 |

Source: Boeri (2011)

Impact on the financial markets

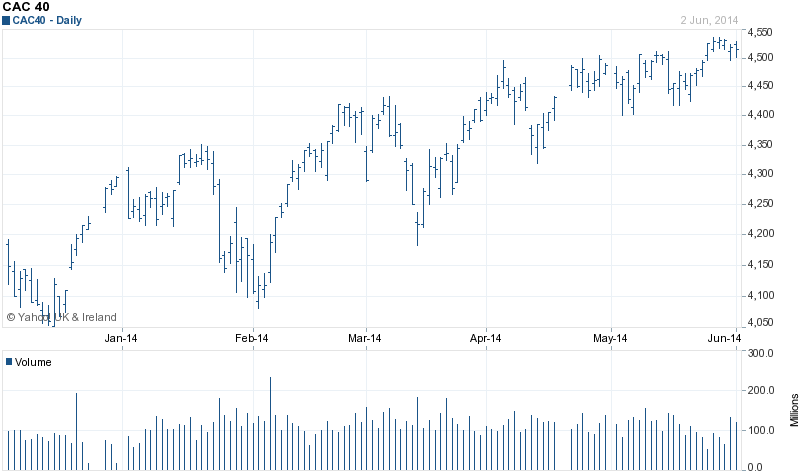

But what does all this mean for the French financial markets? To judge by the recent performance of the CAC40 and 10yr OATs, not much.

Source: Yahoo finance

The new highs have been achieved on low volume which may indicate a lack of conviction. What is clear is that the EU election results were anticipated. What is less clear is whether the market reaction is a sign of approval at the “protest” or apathy. It is clear that the financial markets are more concerned about ECB policy. May 2014 EU inflation was +0.5% vs an ECB target of +2%. The small cut in the refinance rate this week and the introduction of negative interest rates on deposits held at the ECB are hardly sufficient to offset the disinflationary forces of the EZ rebalancing which has been on-going since the great recession. The end of “monetary sterilisation” and new targeted LTROs, together with the proposal for the ECB to purchase certain ABS, however, looks like the beginning of something more substantial. OMT is still in the arsenal but has yet to be deployed.

10 yr OATs reflect a similar story: –

Source: Investing.com

The all-time low yield was set in April 2013 at 1.64% but, with French growth apparently slowing, yields remain wedded to those of German Bunds. The 10 year spread has continued to converge this year from 65bp on 15th January to around 40 bp today.

French Real-Estate may also be influencing other asset classes. According to a recent OECD report French residential property is still overvalued despite the declines of the past couple of years. On a Price to Rent measure the OECD estimate values to be 35% higher than the long run average. On a Price to Income basis the overvaluation is only 32%. It is worth noting that interest rates are at historically low levels so these overvaluations are not entirely surprising. France is not alone in its overvaluation as the table from Deutsche Bank (using earlier OECD data) shows: –

Source: Deutsche Bank and OECD

In their March 2014 Global House Price Index report, Frank Knight commented that residential property in France and Spain was still languishing. However, in comparison with March 2012 prices were down only 1.4% in France compared to 4% in Spain and 9.3% in Greece.

If historically low interest rates cannot stimulate demand for Real-Estate then asset managers would do well to allocate to a more attractive asset class. With OAT yields nearing historic lows the CAC40 appears to be benefitting by default; it trades on a P/E of 26 times. The UK, with the strongest growth forecast in Europe, is trading at 33 times (FTSE) whilst the DAX trades on a P/E of 22.

Conclusion

The French Revolt at the EU elections is principally a protest against the immigration policies of the French administration. The main concern of the average French voter is long-term employment and quality of life. The policies of Brussels, which reinforce those of the French administration, are seen as contrary to the interests of the French people in respect of immigration but this does not mean that the French people are anti-EU.

French financial markets have paid little heed to the EU election results. The actions of the ECB are of much greater importance in the near-term. The longer-term implications of the gains for the Front National will be tested at the Senate Elections in September this year, but, given the large socialist majority last time, any swing to the Front National will be a further “protest”. The real test will be at the presidential elections – scheduled for 2017.

Low interest rates from the ECB look set to continue. The central bank has now begun to utilise some of the unconventional tools at their disposal to transmit longer-term liquidity to the non-financial economy. OAT yields should remain low in expectation of the implementation of these more aggressive policies. They will also be supported internally if Hollande succeeds with his austerity package. French property prices are likely to remain subdued and may weaken further if the economy continues to stall. French stocks will therefore continue to benefit, both from international and domestic capital flows, but, at their current valuations, they will reflect the direction of international markets led by the US and, within Europe, by the UK and Germany.

The limits of convergence – Eurozone bond yield compression cracks

Macro Letter – No 10 – 25-04–2014

The limits of convergence – Eurozone bond yield compression cracks

- European bond yields have been converging since 2012 – but for how much longer?

- There are three scenarios – a federal system, a semi-federal system, or a devolved Europe

- Are yields converged under the different scenarios or has it further to go?

Compression cracks, in the geological sense, are a form of brittle deformation. This might be a good way to describe the political process that has driven European government bond yields since the Euro crisis of 2012.

Since the beginning of 2014 the “Convergence Trade” – buying higher yielding Eurozone government bonds and selling German Bunds – has continued to be one of the most profitable fixed income opportunities, as the table below illustrates:-

Country 15/01/2014 16/04/2014 Change

Yield Spread Yield Spread

Germany 1.82% N/A 1.50% N/A N/A

Netherlands 2.13% 0.31% 1.83% 0.33% +0.02%

France 2.47% 0.65% 1.97% 0.47% -0.18%

Ireland 3.27% 1.45% 2.87% 1.37% -0.08%

Spain 3.82% 2.00% 3.09% 1.59% -0.41%

Italy 3.88% 2.06% 3.11% 1.61% -0.45%

Portugal 5.25% 3.43% 3.80% 2.30% -1.13%

Greece 7.93% 6.91% 6.46% 4.96% -1.15%

Source: Bloomberg

The two charts below show this process over a longer time horizon. The first, from True Economics, looks back to the period of convergence prior to the introduction of the Euro. It shows the extraordinary stability, both in terms of absolute yield and spread differentials, for the period from 1999 until the Lehman default in 2008. The subsequent divergence is more clearly captured by the second chart which also shows Gilt yields; they might be regarded as a surrogate for the global bond market’s reaction to the financial crisis and subsequent Euro crisis.

Source: Trueeconomics.com

Source: Bloomberg

What is clear from both charts is the bond market’s sudden realisation, after 2008, that the ECB and the EU Commission might not be in a sufficiently strong position economically and, more importantly, politically, to avert a break-up of the Euro.

Whilst Irish Gilt yields had already begun to decline in 2011, due to their adoption of radical measures in response to economic depression, the turning point, from divergence to convergence, for the rest of the EZ, commenced after Mario Draghi’s speech on 26th July 2012 in which he said “Within our mandate, the ECB is ready to do whatever it takes to preserve the euro. And believe me, it will be enough.”

The European Commission had been analysing EZ bond spreads for some time before the 2011 Euro crisis as this paper from November 2009 shows – Determinates of intra-euro area government bond spreads during the financial crisis. The paper noted that the average spread over German Bunds between 1999 and mid-2007 had been 18bp. They concluded: –

Although conditions on government bond markets have been easing considerably since spring 2009, it seems unlikely that spreads will revert to pre-crisis levels in the near future. A number of elements suggest this. First, the strong rise in financing costs by sovereign issuers since September 2008 may, to a certain extent, be explained by the correction of abnormally narrow spreads in the pre-crisis period, when domestic risk factors resulted in small yield differentials. Second, it can be expected that government bond yield spreads will remain elevated compared to the pre-crisis period as debt levels have increased significantly in a number of countries (relative to the German benchmark) and the contingent liabilities assumed by the public sector in rescuing the financial sector will continue to weigh on the outlook for public finances.

Looking further ahead, greater market discrimination across countries may provide higher incentives for governments to attain and maintain sustainable public finances. Since even small changes in bond yields have a noticeable impact on government outlays, market discipline may act as an important deterrent against deteriorating public finances.

Three scenarios for Eurozone bonds

I believe we should consider three possible scenarios with very different outcomes for yield differentials.

1. Full Banking Union and further Federalization of Europe

Under this scenario the ECB becomes the “back-stop” to all members of the Eurozone. The European Parliament wrests partial control of spending from the individual state governments, but, in the process, becomes an unofficial guarantor of the obligations of EZ member states.

In this environment yield spreads will reflect a possible default risk and a liquidity risk. I see a parallel with the US Treasury market yield differential for On-the-run and Off-the-run issues but with an additional small default premium – unless the EU guarantee becomes de juro.

A fascinating study of this phenomenon is Liquidity ‘life cycle’ in US Treasury bondswhich was published in January 2012 by the European Financial Management Association – the table on page 26 analyses the period 1996-2006. For 30 year bonds the mean yield differential is 13 bp with a range of -34 to +93 dependent upon the issue.

A prior paper on this subject was published in the January 2009 by the Journal of Financial Economics – The on-the-run liquidity phenomenon. This proposes an interesting model for measuring and forecasting the phenomenon. They conclude: –

Our evidence indicates that (i) the resulting off/on-the- run liquidity differentials are large, even after controlling for several differences in their intrinsic characteristics (such as duration, convexity, repo rates, or term premiums), and (ii) an economically meaningful portion of those liquidity differentials is linked to strategic trading activity in both security types. The nature of this linkage is sensitive to the uncertainty surrounding auction shocks and the economy, the intensity of investors’ dispersion of beliefs, and the noise of the public announcement. In particular, and consistent with our model, off/on-the-run liquidity differentials are smaller immediately following bond auction dates and in the presence of (high-quality) macroeconomic announcements, and larger when the dispersion of auction bids is higher, when fundamental uncertainty is greater, and when the beliefs of sophisticated traders are more heterogeneous.

These findings suggest that liquidity differentials between on-the-run and off-the-run securities depend crucially on endowment uncertainty in the former and the informational role of strategic trading in both.

2. Full Banking Union but limitation of Federalization

Persuading German voters to bail-out the “profligate sons” of Europe is a tall order; however, a collapse an subsequent exit of the countries of the periphery would cause catastrophic damage to the German banking system. A constructive compromise would be to allow limited outright monetary purchases (OMT) together with limited issuance of “Euro Bonds”. This is a slippery slope but, in the consensual world of European politics, I think it is the most likely outcome. After all, the European Financial Stability Fundhas already helped to bail-out Greece, Ireland and Portugal and the European Stability Mechanismcontinued its bail-out of Cyprus this month bringing the total support for Cyprus to Eur 4.5bln.Here is the latest statement from Klaus Regling – MD of the EMS.

The idea that government bonds of individual states are not underwritten bears some similarity to US state issuance in the municipal bond market. Muni bonds have certain tax advantages which makes absolute yield comparison with US Treasuries difficult but their lack of a federal guarantee makes them a useful comparator.

With the exception of Puerto Rico (BB+) all US state Muni bonds are currently rated from AAA to A-. On 10th April 2014 the generic yield on 10 yr Muni Bonds was as follows: –

Rating Yield Spread

AAA 2.37% N/A

AA 2.57% 0.20%

A 3.06% 0.69%

Source: Morgan Stanley

During the depths of the post Lehman crisis in 2008 the spread between AAA and A widened to 160bp. Anecdotally, the last time I looked at Muni Bond spreads as a surrogate for European bonds was in 1998 – the differential between highest and lowest rated state was 109bp. At that time I felt European yields had already converged too much and advocated the “Divergence Trade”, but, as JM Keynes once remarked “The markets can remain irrational longer than I can remain solvent.” I’m glad I didn’t bet the ranch!

3. Eurozone break-up

I don’t think this scenario is likely because too much political investment has been made in the “European Project”; they will do “whatever it takes”. However, for the purposes of comparison, it is useful to consider where yield differentials might be for European governments once they have been relieved of their Euro straightjackets.

Here is a table of some European 10 year bond yields for non-EZ countries, together with their spread over German Bunds, taken on 16th April 2014, I’ve also added their World Bank GDP ranking: –

Country Yield Spread GDP

Switzerland 0.87% (0.63%) 20

Denmak 1.52% 0.02% 33

Czech Rep 1.99% 0.49% 51

Sweden 2.00% 0.50% 22

UK 2.65% 1.15% 6

Norway 2.86% 1.36% 23

Latvia 3.00% 1.50% 93

Lithuania 3.30% 1.80% 83

Bulgaria 3.30% 1.80% 75

Slovenia 3.63% 2.13% 79

Poland 4.14% 2.64% 24

Croatia 4.87% 3.37% 70

Romania 5.24% 3.74% 56

Hungary 5.74% 4.24% 58

Iceland 6.71% 5.21% 121

Turkey 9.95% 8.45% 17

Source: Bloomberg

The yield differentials of these countries reflect several factors including inflation, debt levels and growth expectations, however there are some useful observations.

Firstly the Swiss National Bank has been intervening to halt further appreciation in the CHF exchange rate. They have also been combating deflationary forces for an extended period.

The UK economy has been exhibiting some of the strongest growth in Europe this year but has also been beset by above target inflation for a protracted period until very recently.

Turkey, whilst it is the second largest economy in the table, is less “European” in structure; it may remain interested in joining the EU but it is culturally and politically “another country”.

Iceland is the smallest economy in the table but it is also a “post-crisis” country and therefore reflects lenders perceptions of a country’s credit worthiness, post-default.

Yield spreads – where are they now and where will they go?

Returning to the EZ countries, I want to narrow my analysis to Spain, Italy, Portugal and Greece. These are the countries with reasonably liquid government bond markets which are also benefitting most clearly from the brittle yield compression of the EZ. Where are their yields today and where might be fair-value under the three scenarios outlined above.

Country Yield Spread GDP

Spain 3.09% 1.59% 13

Italy 3.11% 1.61% 9

Portugal 3.80% 2.30% 46

Greece 6.46% 4.96% 42

Source: Bloomberg

Firstly, a leptokurtic excuse – in my estimates below I am ignoring times of economic crisis since these are “Black Swan” events with highly unpredictable outcomes.

Scenario 1. 100bp

Where individual EZ states receive a tacit guarantee from Brussels; I would expect a maximum spread of 100bp. This makes all the above issuers still look attractive from a yield enhancement perspective.

Scenario 2. 200bp

Where individual EZ states are not guaranteed: and therefore subject to the discipline of the market; I would expect the maximum spread to reach 200bp. This still makes Portugal and Greece look relatively cheap. Italy and Spain may head towards the levels of France (49bp) but this is unlikely to be sustainable unless they radically change their attitude towards deficit spending. Alternatively, French yield premiums may rise up to meet them.