Macro Letter – No 64 – 28-10-2016

Saudi Arabian bonds and stocks – is it time to buy?

- Saudi Arabia issued $17.5bln of US$ denominated sovereign bonds – the largest issue ever

- Saudi Aramco may float 5% of their business in the largest IPO ever

- The TASI stock index is down more than 50% from its 2014 high

- OPEC agreed to cut output by 640,000 to 1,140,000 bpd

The sovereign bond issue

The Saudi Arabia’s first international bond deal raised $17.5bln. They tapped the market across the yield curve issuing 5yr, 10yr and 30yr bonds. The auction was a success – international investors, mostly from the US, placed $67bln of bids. The issues were priced slightly higher than Qatar, which raised $9bln in May, and Abu Dhabi, which issued $2.5bln each of 5yr and 10yr paper in April.

The Saudi issue appears to have been priced to go, as the table below, showing the basis point spread over US Treasuries, indicates. According to the prospectus the Kingdom of Saudi Arabia (KSA) want to tap the US$ sovereign bond market extensively in the future, raising as much as $120bln; attracting investors has therefore been a critical aspect of their recent charm offensive:-

| Issuer | 5yr Spread | 10yr Spread | 30yr Spread | Bid to Cover |

| Saudi Arabia | 135 | 165 | 210 | 3.82 |

| Qatar | 120 | 150 | 210 | 2.56 |

| Abu Dhabi | 85 | 125 | N/A | 3.4 |

Source: Bloomberg

The high bid to cover ratio (3.8 times) enabled the Kingdom to issue $2.5bln more paper than had been originally indicated: and on better terms – 40bp over, higher rated, Qatar rather than 50bp which had been expected prior to the auction.

The bonds immediately rose in secondary market trading and other Gulf Cooperation Council (GCC) issues also caught a bid. The Saudi issue was also unusual in that the largest tranche ($6.5bln) was also the longest maturity (30yr). The high demand is indicative of the global quest for yield among investors. This is the largest ever Emerging Market bond issue, eclipsing Argentina’s $16.5bln offering in April.

The Aramco IPO

Another means by which the Kingdom plans to balance the books is through the Saudi Aramco IPO – part of the Vision 2030 plan – which may float as much as 5% of the company, worth around $100bln, in early 2018. This would be four times larger than the previous record for an IPO set by Alibaba in September 2014.

An interesting, if Machiavellian, view about the motivation behind the Aramco deal is provided by – Robert Boslego – Why Saudi Arabia Will Cut Production To Achieve Vision 2030:-

As part of the implementation of this plan, Saudi Aramco and Shell (NYSE:RDS.A) (NYSE:RDS.B) are dividing up their U.S. joint venture, Motiva, which will result in Saudi’s full ownership of the Port Author refinery. Aramco will fully own Motiva on April 1, 2017, and has been in talks of buying Lyondell’s Houston refinery.

I suspect Motiva may also purchase U.S. oil shale properties (or companies) that are in financial trouble as a result of the drop in prices since 2014. According to restructuring specialists, about 100 North American oil and gas companies have filed for bankruptcy, and there may be another 100 to go. This would enable Aramco to expand market share as well as control how fast production is brought back online if prices rise.

By using its ability to cut production to create additional spare capacity, Aramco can use that spare capacity to control prices as it wishes. It probably does not want prices much above $50/b to keep U.S. shale production to about where it is now, 8.5 mmbd. And it doesn’t want prices below $45/b because of the adverse impact of such low prices on its budget. And so it will likely adjust its production accordingly to keep prices in a $45-$55/b range.

… Conclusions

Although I authored a series of articles stating that OPEC was bluffing (and it was), I now think that Saudi Arabia has formulated a plan and will assume the role of swing producer to satisfy its goals. It can and will cut unilaterally to create excess spare capacity, which it needs to control oil prices.

This will make the company attractive for its IPO. And by selling shares, Aramco can use some of the proceeds to buy U.S. shale reserves “on the cheap,” not unlike John D. Rockefeller, who bankrupted competitors to acquire them.

The Saudi’s long-term plan is to convert Aramco’s assets into a $2 trillion fund, which can safely reside in Swiss banks. And that is a much safer investment than oil reserves in the ground subject to external and internal political threats.

Whatever the motives behind Vision 2030, it is clear that radical action is needed. The Tadawul TASI Stock Index hit its lowest level since 2011 on 3rd October at 5418, down more than 50% from its high of 11,150 in September 2014 – back when oil was around $90/bbl.

As a starting point here is a brief review of the Saudi economy.

The Saudi Economy

The table below compares KSA with its GCC neighbours; Iran and Iraq have been added to broaden the picture of the oil producing states of the Middle East:-

| Country | GDP YoY | Interest rate | Inflation rate | Jobless rate | Gov. Budget | Debt/GDP | C/A | Pop. |

| Saudi Arabia | 1.40% | 2.00% | 3.30% | 5.60% | -15.00% | 5.90% | -8.2 | 31.52 |

| Iran | 0.60% | 20.00% | 9.40% | 11.80% | -2.58% | 16.36% | 0.41 | 78.8 |

| UAE | 3.40% | 1.25% | 0.60% | 4.20% | 5.00% | 15.68% | 5.8 | 9.16 |

| Iraq | 2.40% | 4.00% | 0.20% | 16.40% | -2.69% | 37.02% | -0.8 | 35.87 |

| Qatar | 1.10% | 4.50% | 2.60% | 0.20% | 16.10% | 35.80% | 8.3 | 2.34 |

| Kuwait | 1.80% | 2.25% | 2.90% | 2.20% | 26.59% | 7.10% | 11.5 | 3.89 |

| Oman | -14.10% | 1.00% | 1.30% | 7.20% | -17.10% | 9.20% | -15.4 | 4.15 |

| Bahrain | 2.50% | 0.75% | 2.60% | 3.70% | -5.00% | 42.00% | 3.3 | 1.37 |

Source: Trading Economics

In terms of inflation the KSA is in a better position than Iran and its unemployment rate is well below that of Iran or Iraq, but on several measures it looks weaker than its neighbours.

Moody’s downgraded KSA in May – click here for details – citing concern about their reliance on oil. They pointed to a 13.5% decline in nominal GDP during 2015 and forecast a further fall this year. This concurs with the IMF forecast of 1.2% in 2016 versus 3.5% GDP growth in 2015. It looks likely to be the weakest economic growth since 2009.

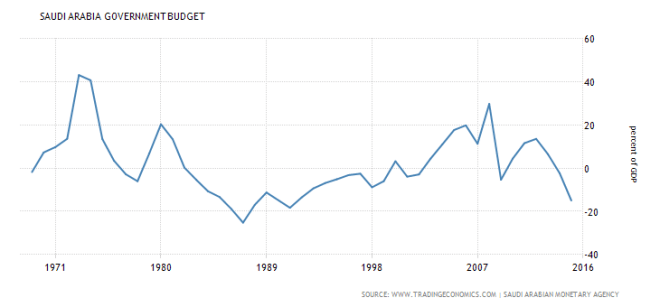

The government’s fiscal position has deteriorated in line with the oil price. In 2014 the deficit was 2.3%, by 2015 it was 15%:-

Source: Trading Economics, SAMA

Despite austerity measures, including proposals to introduce a value added tax, the deficit is unlikely to improve beyond -13.5% in 2016. It is estimated that to balance the Saudi budget the oil price would need to be above $79/bbl.

At $98bln, the 2015 government deficit was the largest of the G20, of which Saudi Arabia is a member. According to the prospectus of the new bond issue Saudi debt increased from $37.9bln in December 2015 to $72.9bln in August 2016. Between now and 2020 Moody’s estimate the Kingdom will have a cumulative financing requirement of US$324bln. More than half the needs of the GCC states combined. Despite the recent deterioration, Government debt to GDP was only 5.8% in 2015:-

Source: Trading Economics, SAMA

They have temporary room for manoeuvre, but Moody’s forecast this ratio rising beyond 35% by 2018 – which is inconsistent with an Aa3 rating. Even the Saudi government see it rising to 30% by 2030.

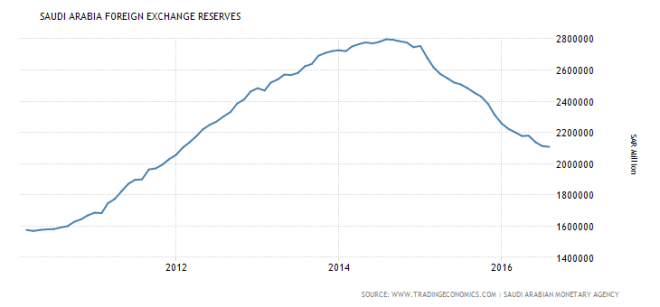

The fiscal drag has also impacted foreign exchange reserves. From a peak of US$731bln in August 2014 they have fallen by 23% to US$562bln in August 2016:-

Source: Trading Economics, SAMA

Reserves will continue to decline, but it will be some time before the Kingdom loses its fourth ranked position by FX reserves globally. Total private and public sector external debt to GDP was only 15% in 2015 up from 12.3% in 2014 and 11.6% in 2013. There is room for this to grow without undermining the Riyal peg to the US$, which has been at 3.75 since January 2003. A rise in the ratio to above 50% could undermine confidence but otherwise the external debt outlook appears stable.

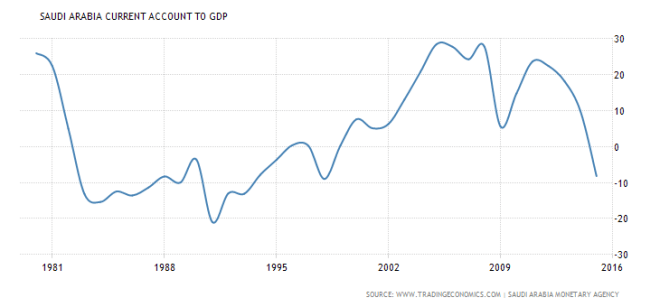

The fall in the oil price has also led to a dramatic reversal in the current account, from a surplus of 9.8% in 2014 to a deficit of 8.2% last year. In 2016 the deficit may reach 12% or more. It has been worse, as the chart below shows, but not since the 1980’s and the speed of deterioration, when there is no global recession to blame for the fall from grace, is alarming:-

Source: Trading Economics, SAMA

The National Vision 2030 reform plan has been launched, ostensibly, to wean the Kingdom away from its reliance on oil – which represents 85% of exports and 90% of fiscal revenues. In many ways this is an austerity plan but, if fully implemented, it could substantially improve the economic position of Saudi Arabia. There are, however, significant social challenges which may hamper its delivery.

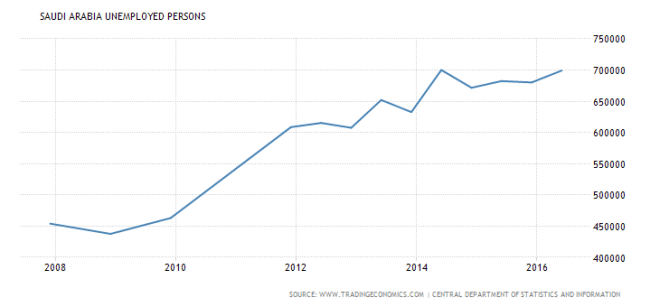

Perhaps the greatest challenge domestically is youth unemployment. More than two thirds of Saudi Arabia’s population (31mln) is under 30 years of age. A demographic blessing and a curse. Official unemployment is 5.8% but for Saudis aged 15 to 24 it is nearer to 30%. A paper, from 2011, by The Woodrow Wilson International Center – Saudi Arabia’s Youth and the Kingdom’s Future – estimated that 37% of all Saudis were 14 years or younger. That means the KSA needs to create 3mln jobs by 2020. The table below shows the rising number unemployed:-

Source: Trading Economics, Central Department of Statistics and Economics

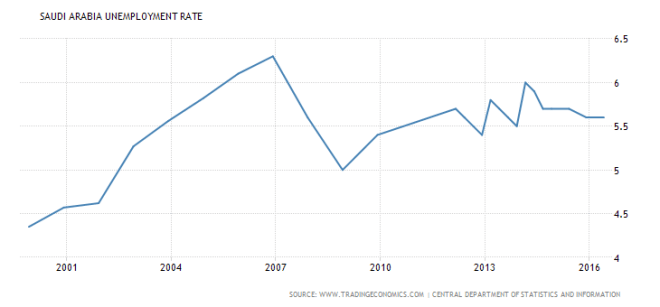

If you compare the chart above with the unemployment percentage shown below you would be forgiven for describing the government’s work creation endeavours as Sisyphean:-

Source: Trading Economics, Central Department of Statistics and Economics

Another and more immediate issue is the cost of hostilities with Yemen – and elsewhere. Exiting these conflicts could improve the government’s fiscal position swiftly. More than 25% ($56.8bln) of the 2016 budget has been allocated to military and security expenditure. It has been rising by 19% per annum since the Arab spring of 2011 and, according to IHS estimates, will reach $62bln by 2020.

The OPEC deal and tightness in the supply of oil

After meeting in Algiers at the end of September, OPEC members agreed, in principle, to reduce production to between 32.5 and 33mln bpd. A further meeting next month, in Vienna, should see a more concrete commitment. This is, after all, the first OPEC production agreement in eight years, and, despite continuing animosity between the KSA and Iran, the Saudi Energy Minister, Khalid al-Falih, made a dramatic concession, stating that Iran, Nigeria and Libya would be allowed to produce:-

…at maximum levels that make sense as part of any output limits.

Iranian production reached 3.65mln bpd in August – the highest since 2013 and 10.85% of the OPEC total. Nigeria pumped 1.39mln bpd (4.1%) and although Libya produced only 363,000 bpd, in line with its negligible output since 2013, it is important to remember they used to produce around 1.4mln bpd. Nigeria likewise has seen production fall from 2.6mln bpd in 2012. Putting this in perspective, total OPEC production reached a new high of 33.64mln bpd in September.

The oil price responded to the “good news from Algiers” moving swiftly higher. Russia has also been in tentative discussions with OPEC since the early summer. President Putin followed the OPEC communique by announcing that Russia will also freeze production. Russian production of 11.11mln bpd in September, is the highest since its peak in 1988. Other non-OPEC nations are rumoured to be considering joining the concert party.

Saudi Arabia is currently the largest producer of oil globally, followed by the USA. In August Saudi production fell from 10.67mln bpd to 10.63mln bpd. It rebounded slightly to 10.65mln bpd in September – this represents 32% of OPEC output.

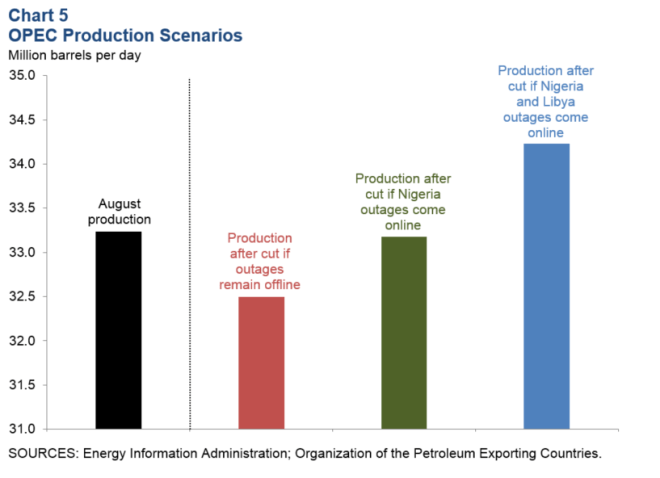

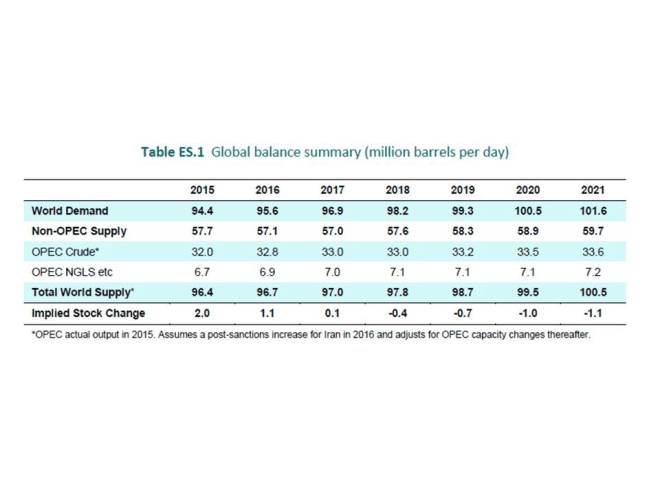

There are a range of possible outcomes, assuming the OPEC deal goes ahead. Under the proposed terms of the agreement, production is to be reduced by between 1.14mln and 640,000 bpd. Saudi Arabia, as the swing producer, is obliged to foot the bill for an Iranian production freeze and adjust for any change in Nigerian and Libyan output. The chart below, which is taken from the Federal Reserve Bank of Dallas – Signs of Recovery Emerge in the U.S. Oil Market – Third Quarter 2016 make no assumptions about Saudi Arabia taking up the slack but it provides a useful visual aid:-

Source: EIA, OPEC, Dallas Fed

They go on to state in relation to US production:-

While drilling activity has edged up, industry participants believe it will be awhile before activity significantly increases. When queried in the third quarter 2016 Dallas Fed Energy Survey, most respondents said prices need to exceed $55 per barrel for solid gains to occur, with a ramp-up unlikely until at least second quarter 2017.

Assuming the minimum reduction in output to 33mln bpd and Iran, Nigeria and Libya maintaining production at current levels, Saudi Arabian must reduce its output by 300,000 bpd. If the output cut is the maximum, Iran freezes at current levels but Nigeria and Libya return to the production levels of 2012, Saudi Arabia will need to reduce its output by 623,000 bpd. The indications are that Nigeria and Libya will only be able to raise output by, at most, 500,000 bpd each, so a 623,000 bpd cut by Saudi Arabia is unlikely to be needed, but even in the worst case scenario, if the oil price can be raised by $3.11/bbl the Saudi production cut would be self-financing. My “Median” forecast below assumes Nigeria and Libya increase output by 1mln bpd in total:-

| OPEC Cut ‘000s bpd | KSA Cut ‘000s bpd | KSA % of total OPEC Cut | Oil Price B/E for KSA/bbl | |

| Max | 1,140 | 623 | 54.68% | +$3.11 |

| Median | 890 | 422 | 47.41% | +$2.06 |

| Minimum | 640 | 300 | 47.07% | +$1.45 |

Source: OPEC

Many commentators are predicting lower oil prices for longer; they believe OPEC no longer has the power to influence the global oil price. This article by David Yager for Oil Price – Why Oil Prices Will Rise More And Sooner Than Most Believe – takes a different view. His argument revolves around the amount of spare capacity globally. The author thinks OPEC is near to full production, but it is his analysis of non-OPEC capacity which is sobering:-

…RBC Capital Markets was of the view oil prices would indeed rise but not until 2019. RBC says 2.2 million b/d of new non-OPEC production will enter the markets this year, 1.3 million b/d next year and 1.6 million b/d in 2018. Somehow U.S. production will rise by 900,000 b/d from 2017 and 2019 despite falling by 1.1 million b/d in the past 15 months and with rigs count at historic lows. At the same time RBC reported the 124 E&P companies it follows will cut spending another 32 percent in 2016 from 2015, a $US106 billion reduction.

…The Telegraph ran it under the title, “When oil turns it will be with such lightning speed that it could upend the market again”. Citing the lowest levels of oil discoveries since 1952, annual investment in new supplies down 42 percent in the past two years and how the International Energy Agency (IEA) estimates 9 percent average annual global reservoir depletion, the article stated, “…the global economy is becoming dangerously reliant on crude supply from political hotspots”. “Drillers are not finding enough oil to replace these (depletion) barrels, preparing the ground for an oil price spike and raising serious questions about energy security”.

Depletion of 9 percent per year is about 8.6 million b/d. Add demand growth and you’re approaching 10 million b/d. How do the crystal ball polishers of the world who see flat oil prices for the foreseeable future figure producers can replace this output when others report $US1 trillion in capital projects have been cancelled or delayed over the rest of the decade?

The last ingredient in the oil price confusion in inventory levels. OECD countries currently hold 3.1 billion barrels of oil inventory. That sounds like lot. But what nobody reports is the five-year average is about 2.7 billion barrels. Refinery storage tanks. Pipelines. Field locations. Tankers in transit. It’s huge. The current overhang is about 6 days of production higher than it has been for years, about 60 days. So inventories are up roughly 10 percent from where they have been.

Obviously this is going to take a change in the global supply/demand balance to return to historic levels and will dampen prices until it does. But don’t believe OECD inventories must go to zero.

…The current production overhang suppressing markets is only about 1 million b/d or less depending upon which forecast you’re looking at. Both the IEA (Paris) and the EIA (Washington) see the curves very close if they haven’t crossed already. Neither agency sees any overhang by the end of the next year.

…OPEC has no meaningful excess capacity. Non-OPEC production is flat out and, in the face of massive spending cuts, is more likely to fall than rise because production increases will be more than offset by natural reservoir depletion.

Since this article was published OECD inventories have declined a fraction. Here is the latest EIA data:-

| 2014 | 2015 | 2016 | 2017 | |

| Non-OPEC Production | 55.9 | 57.49 | 56.84 | 56.94 |

| OPEC Production | 37.45 | 38.32 | 39.2 | 40.07 |

| OPEC Crude Oil Portion | 30.99 | 31.76 | 32.45 | 33.03 |

| Total World Production | 93.35 | 95.81 | 96.04 | 97.01 |

| OECD Commercial Inventory (end-of-year) | 2688 | 2967 | 3049 | 3073 |

| Total OPEC surplus crude oil production capacity | 2.08 | 1.6 | 1.34 | 1.21 |

| OECD Consumption | 45.86 | 46.41 | 46.53 | 46.6 |

| Non-OECD Consumption | 46.69 | 47.63 | 48.8 | 50.07 |

| Total World Consumption | 92.55 | 94.04 | 95.33 | 96.67 |

Source: EIA

Whether or not David Yager is correct about supply, the direct cost to Saudi Arabia, of a 623,000 bpd reduction in output, pales into insignificance beside the cost of domestic oil and gas subsidies – around $61bln last year. Subsidies on electricity and water add another $10bln to the annual bill. These subsidies are being reduced as part of the Vison 2030 austerity plan. The government claim they can save $100bln by 2020, but given the impact of removing subsidies on domestic growth, I remain sceptical.

The Kingdom’s domestic demand for crude oil continues to grow. Brookings – Saudi Arabia’s economic time bomb – forecast that it will reach 8.2mln bpd by 2030. By some estimates they may become a net importer of oil by their centenary in 2032. Saudi oil reserves are estimated at 268bln bbl. Her gas reserves are estimated to be 8.6trln M3 (2014) but exploration may yield considerable increases in these figures.

The Kingdom is also planning to build 16 nuclear power stations over the next 20 years, along with extensive expansion of solar power generating capacity. Improvements in technology mean that solar power stations will, given the right weather conditions, produce cheaper electricity than gas powered generation by the end of this year. This article from the Guardian – Solar and wind ‘cheaper than new nuclear’ by the time Hinkley is built – looks longer term.

According to EIA data US production in July totalled 8.69mln bpd down from 9.62mln bpd in March 2015. A further 200,000 bpd reduction is forecast for next year.

The table below, which is taken from the IEA – Medium Term Oil Market Report – 2016 – suggests this tightness in supply may last well beyond 2018:-

Source: IEA – MTOMR 2016

According to Baker Hughes data, US rig count has rebounded to 443 since the low of 316 at the end of May, but this is still 72% below its October 2014 peak of 1609. This March 2016 article from Futures Magazine – How quickly will U.S. energy producers respond to rising prices? Explains the dynamics of the US oil industry:-

Crude oil produced by shale made up 48% of total U.S. crude oil production in 2015, up from 22% in 2007 according to the Energy Information Administration (EIA), which warns that the horizontal wells drilled into tight formations tend to have very high initial production rates–but they also have steep initial decline rates. Some wells lose as much as 70% of their initial production the first year. With steep decline rates, constant drilling and development of new wells is necessary to maintain or increase production levels. The problem is that many of these smaller shale companies do not have the capital nor the manpower to keep drilling and keep production going.

This is one of the reasons that the EIA is predicting that U.S. oil production will fall by 7.4%, or roughly 700,000 barrels a day. That may be a modest assessment as we are hearing of more stress and bankruptcies in the space. The EIA warns that with the U.S. oil rig count down 76% since the fall of 2014, that unless capital spending picks up, the EIA says that U.S. oil production will keep falling in 2017, ending up 1.2 million barrels a day lower than the 2015 average at 8.2 million barrels a day.

The bearish argument that shale will save the day and keep prices under control does not fit with the longer term reality. When more traditional energy projects with much slower decline rates get shelved, there is the thought that the cash strapped shale producers can just drill, drill. Drill to make up that difference is a fantasy. The problem is that while shale may replace that oil for a while, in the long run it can never make up for the loss of projects that are more sustainable.

OPEC might just have the whip hand for the first time in several years.

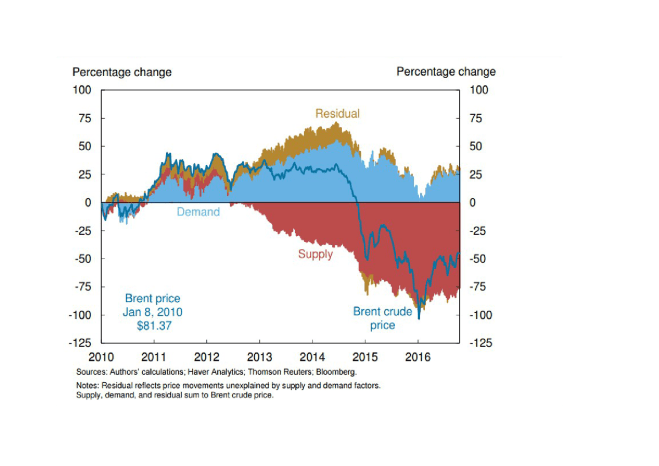

The chart below, taken from the New York Federal Reserve – Oil Price Dynamics Report – 24th October 2016 – shows how increased supply since 2012 has pushed oil prices lower. Now oversupply appears to be abating once more; combine this with the inability of the fracking industry to “just drill” and the reduction in inventories and conditions may be ripe for an aggressive short squeeze:-

Source: NY Federal Reserve, Haver Analytics, Reuters, Bloomberg

But, how sustainable is any oil price increase?

Longer term prospects for oil demand

Source: Trading Economics

In the short term there are, as always, a plethora of conflicting opinions about the direction of the price of oil. Longer term, advances in drilling techniques and other technologies – especially those relating to fracking – will exert a downward pressure on prices, especially as these methods are adopted more widely across the globe. Recent evidence supports the view that tight-oil extraction is economic at between $40 and $60 per bbl, although the Manhattan Institute – Shale 2:0 – May 2015 – suggests:-

In recent years, the technology deployed in America’s shale fields has advanced more rapidly than in any other segment of the energy industry. Shale 2.0 promises to ultimately yield break-even costs of $5–$20 per barrel—in the same range as Saudi Arabia’s vaunted low-cost fields.

These reductions in extraction costs, combined with improvements in fuel efficiency and the falling cost of alternative energy, such as solar power, will constrain prices from rising for any length of time.

Published earlier this month, the World Energy Council – World Energy Scenarios 2016 – The Grand Transition – propose three, very different, global outlooks, with rather memorable names:-

- Modern Jazz – digital disruption, innovation and market based reform

- Unfinished Symphony – intelligent and sustainable economic growth with low carbon

- Hard Rock – fragmented, weaker, inward-looking and unsustainable growth

They go on to point out that, despite economic growth – especially in countries like China and India – global reliance on fossil fuels has fallen from 86% in 1970 to 81% in 2014 – although in transportation reliance remains a spectacular 92%. The table below shows rising energy consumption under all three scenarios, but an astonishing divergence in its rise and source of supply, under the different regimes:-

| Scenario – 2060 | % increase in energy consumption | % reliance on oil | Transport % reliance on oil |

| Modern Jazz | 22 | 50 | 67 |

| Unfinished Symphony | 38 | 63 | 60 |

| Hard Rock | 46 | 70 | 78 |

Source: World Energy Council

The authors expect demand for electricity to double by 2060 requiring $35trln to $43trln of infrastructure investment. Solar and Wind power are expected to increase their share of supply from 4% in 2014 to between 20% and 39% dependent upon the scenario.

As to the outlook for fossil fuels, global demand for coal is expected to peak between 2020 and 2040 and for oil, between 2030 and 2040.

…peaks for coal and oil have the potential to take the world from stranded assets predominantly in the private sector to state-owned stranded resources and could cause significant stress to the current global economic equilibrium with unforeseen consequences on geopolitical agendas. Carefully weighed exit strategies spanning several decades need to come to the top of the political agenda, or the destruction of vast amounts of public and private shareholder value is unavoidable. Economic diversification and employment strategies for growing populations will be a critical element of navigating the challenges of peak demand.

The economic diversification, to which the World Energy Council refer, is a global phenomenon but the impact on nations which are dependent on oil exports, such as Saudi Arabia, will be even more pronounced.

Conclusion and investment opportunities

As part of Vision 2030 – which was launched in the spring by the King Salman’s second son, Prince Mohammed bin Salman – the Saudi government introduced some new measures last month. They cancelled bonus payments to state employees and cut ministers’ salaries by 20%. Ministers’ perks – including the provision of cars and mobile phones – will also be withdrawn. In addition, legislative advisors to the monarchy have been subjected to a 15% pay cut.

These measures are scheduled to take effect this month. They are largely cosmetic, but the longer term aim of the plan is to reduce the public-sector wage bill by 5% – bringing it down to 40% of spending by 2020. Government jobs pay much better than the private sector and the 90/90 rule applies –that is 90% of Saudi Arabians work for the government and the 10% of workers in the private sector are 90% non-Saudi in origin. The proposed pay cuts will be deeply unpopular. Finally, unofficial sources claim, the government has begun cancelling $20bln of the $69bln of investment projects it had previously approved. All this austerity will be a drag on economic growth – it begins to sound more like Division 2030, I anticipate social unrest.

The impact of last month’s announcement on the stock market was unsurprisingly negative – the TASI Index fell 4% – largely negating the SAR20bln ($5.3bln) capital injection by the Saudi Arabian Monetary Agency (SAMA) from the previous day.

Saudi Bonds

Considering the geo-political uncertainty surrounding the KSA, is the spread over US Treasuries sufficient? In the short term – two to five years – I think it is, but from a longer term perspective this should be regarded as a trading asset. If US bond yield return to a more normal level – they have averaged 6.5% since 1974 – the credit spread is likely to widen. Its current level is a function of the lack of alternative assets offering an acceptable yield, pushing investors towards markets with which many are unfamiliar. KSA bonds do have advantages over some other emerging markets, their currency is pegged to the US$ and their foreign exchange reserves remain substantial, nonetheless, they will also be sensitive to the price of oil.

Saudi stocks

For foreign investors ETFs are still the only way to access the Saudi stock market, unless you already have $5bln of AUM – then you are limited to 5% of any company and a number of the 170 listed stocks remain restricted. For those not deterred, the iShares MSCI Saudi Arabia Capped ETF (KSA) is an example of a way to gain access.

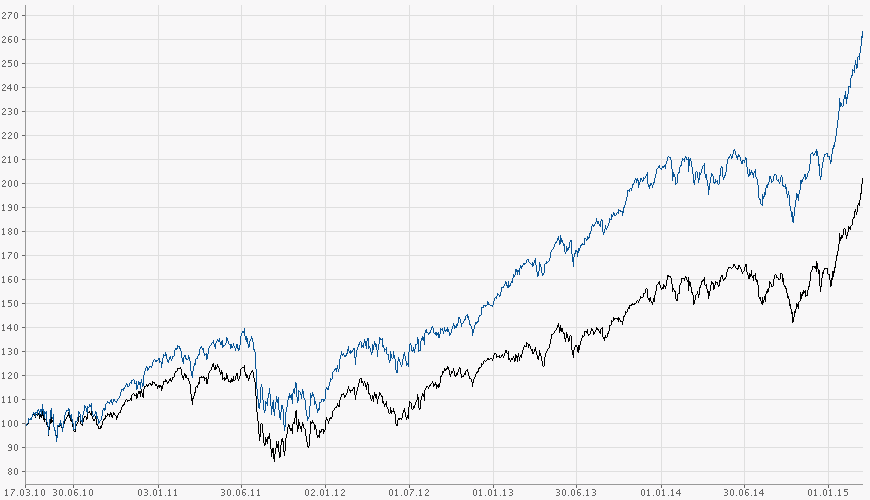

Given how much of the economy of KSA relies on oil revenues, it is not surprising that the TASI Index correlates with the price of oil. It makes the Saudi stock exchange a traders market with energy prices dominating direction. Several emerging stock markets have rallied dramatically this year, as the chart below illustrates, the TASI has not been among their number:-

Source: Saudi Stock Exchange, Trading Economics

Oil

Tightness in supply makes it likely that oil will find a higher trading range, but previous OPEC deals have been wrecked by cheating on quotas. Longer term, improvements in technology will reduce the cost of extraction, increase the amount of recoverable reserves and diminish our dependence on fossil fuels by improving energy efficiency and developing, affordable, renewable, alternative sources of energy. By all means trade the range but remember commodities have always had a negative real expected return in the long run.