Macro Letter – No 32 – 20-03-2015

German resurgence – Which asset? Stocks, Bunds or Real Estate

- German domestic consumption is driving GDP growth as wages rise

- The effect of a weaker Euro has yet to be seen in exports

- Lower energy prices are beginning to boost corporate margins

- Bund yields are now negative out to seven years

Last month Eurostat released German GDP data for Q 2014 at +0.7%, this was well above consensus forecasts of +0.3% and heralded a surge in the DAX stock index. For the year German growth was +1.6% this compares favourably to France which managed an anaemic +0.4% for the same period. German growth forecasts are being, feverishly, revised higher. Here is the latest data as polled by the BDA – revisions are highlighted in bold:-

| Institution | Survey Date | 2015 Previous | 2015 | 2016 |

| ifo ifo Institute (Munich) | Dec-14 | N/A | 1.5 | |

| IfW Kiel Institute | Mar-15 | 1.7 | 1.8 | 2 |

| HWWI Hamburg Institute | Mar-15 | 1.3 | 1.9 | 1.7 |

| RWI Rheinisch-Westf. Institute (Essen) | Dec-14 | N/A | 1.5 | |

| IWH Institute (Halle) | Dec-14 | N/A | 1.3 | 1.6 |

| DIW German Institute (Berlin) | Dec-14 | N/A | 1.4 | 1.7 |

| IMK Macroeconomic Policy Institute (Düsseldorf) | Dec-14 | N/A | 1.6 | |

| Research Institutes Joint Economic Forecast Autumn 2014 | Oct-14 | N/A | 1.2 | |

| Council of experts Annual Report 2014/2015 | Nov-14 | N/A | 1 | |

| Federal Government Annual Economic Report 2015 | Jan-15 | 1.3 | 1.5 | |

| Bundesbank Forecast (Frankfurt) | Dec-14 | N/A | 1 | 1.6 |

| IW Köln IW Forecast | Sep-14 | N/A | 1.5 | |

| DIHK German Chambers of Industry and Commerce (Berlin) | Feb-15 | N/A | 0.8 | 1.3 |

| OECD | Nov-14 | N/A | 1.1 | 1.8 |

| EU Commission | Feb-15 | 1.1 | 1.5 | 2 |

| IMF | Oct-14 | N/A | 1.5 | 1.8 |

Source: Confederation of German Employers’ Associations (BDA), Survey Date: March 13, 2015

The improvement in German growth has been principally due to increases in construction spending, machinery orders and, more significantly, domestic consumption, which rose 0.8% for the second successive quarter. This, rather than a resurgence in export growth, due to the decline in the Euro, appears to be the essence of the recovery. That the Euro has continued to fall, thanks to ECB QE and political uncertainty surrounding Greece, has yet to show up in the export data:-

Source: Trading Economics

German imports have also remained stable:-

Source: Trading Economics

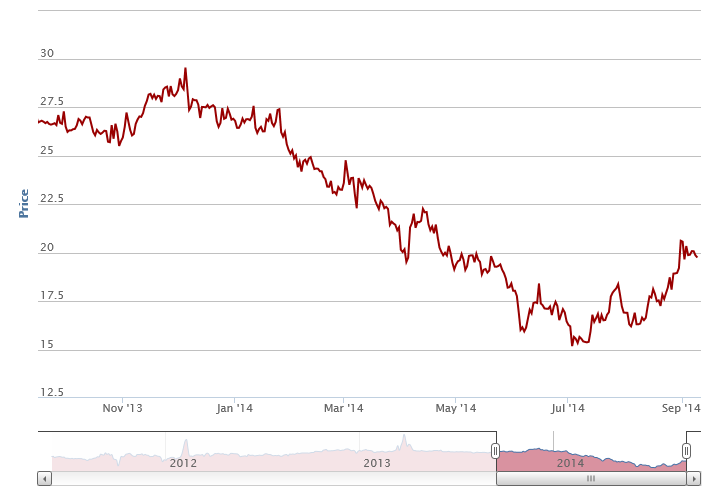

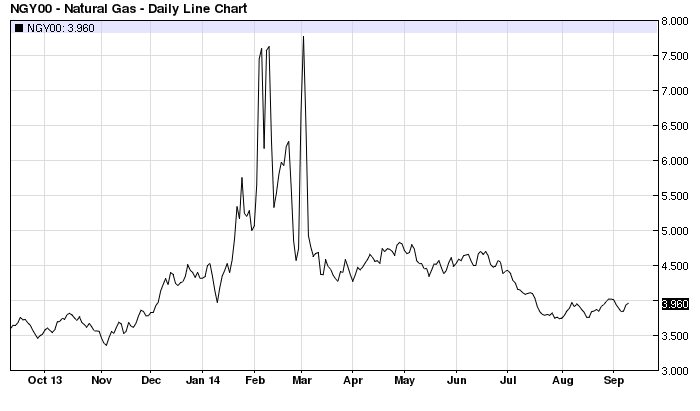

This may seem surprising given the extent of the fall in the price of crude oil – it made new lows this week. German Natural Gas prices, which had been moderately elevated to around $10.4/btu during the autumn have fallen to $9.29/btu, a level last seen in early 2011. That the improved energy input has not shown up in the terms of trade data may be explained by the fact that crude oil and natural gas imports account for only 10% of total German imports. Nonetheless, I suspect the benevolent impact of lower energy prices is being delayed by the effects of long-term energy contracts running off. Watch for the February PPI data due out this morning (forecast -1.9% y/y).

The ZEW Institute – Indicator of Economic Sentiment – released on Tuesday, showed a fifth consecutive increase, hitting the highest level since February 2014 at 54.8 – the forecast, however, was a somewhat higher 58.2. This is an extract from their press release:-

“Economic sentiment in Germany remains at a high level. In particular, the continuing positive development of the domestic economy confirms the expectations of the experts. At the same time, limited progress is being made with regard to solving the Ukraine conflict and the sovereign debt crisis in Greece. This has a dampening effect on sentiment,” says ZEW President Professor Clemens Fuest. The assessment of the current situation in Germany has improved notably. Increasing by 9.6 points, the index now stands at 55.1 points.

The good news is not entirely unalloyed (pardon the pun) IG Metall – the German metal workers union which sets the benchmark for other union negotiations – achieved a +3.4% wage increase for their 800,000 members in Baden Württemberg, starting next month. Meanwhile, German CPI came in at 0.09% in February after falling -0.4% in January. This real-wage increase is an indication of the tightness of the broader labour market. Nationally wages are rising at a more modest 1.3%, this is, however, the highest in 20 years. German unemployment fell to 4.8% in January, the lowest in 33years, despite the introduction of a minimum wage of Eur8.50/hour, for the first time, on 1st January.

One of my other concerns for Germany is the declining trend of productivity growth. Whilst employment has been growing, the pace of productivity growth has not. This 2013 paper from Allianz – Low Productivity Growth in Germany examines the issue in detail, here is the abstract:-

Since the labor market reforms implemented in the first half of the last decade, Germany’s labor market has been on a marked upward trend. In 2012, there were 2.6 million (+6.8%) more people in work than in 2005 and the volume of labor was up by 2.4 million hours (+4.3%) on 2005. But the focus on this economic success, which has also earned Germany a great deal of recognition on the international stage, makes it easy to overlook the fact that productivity growth in the German economy has continued to slacken. Whereas the increase in labor productivity per person in work was still averaging 1.0% a year between 1995 and 2005, the average annual increase in the period between 2005 and 2012 was only 0.5%. The slowdown in the pace of labor productivity growth, measured per hour worked, is even more pronounced. The average growth rate of 1.6% between 1995 and 2005 had slipped back to 0.9% between 2005 and 2012.

Allianz go on to make an important observation about the importance of capital investment:-

…the capital factor is now making much less of a contribution to economic growth in Germany than in the past, thus also putting a damper on labor productivity growth.

… Since the bulk of the labor market reforms came into force – in 2005 – the German economy has been growing at an average rate of 1.5% a year. Based on the growth accounting process, the capital stock delivered a growth contribution of 0.4 percentage points, with the volume of labor also contributing 0.4 percentage points. This means that total factor productivity contribute 0.7 percentage points to growth. So if the volume of labor and capital stock were to stagnate, Germany could only expect to achieve economic growth to the tune of 0.7% a year.

… Although gross domestic product also grew by 1.5% on average during that period, labor productivity growth came in at 2.0%, more than twice as high as the growth rate for the 2005 – 2012 period. Between 1992 and 2001, the contribution to growth made by the capital stock, namely 0.9 percentage points, was much greater than that made in the period from 2005 to 2012; by contrast, the growth contribution delivered by the volume of labor was actually negative in the former period, at -0.4 percentage points, and 0.8 percentage points lower than between 2005 and 2012. This could allow us to draw the conclusion that the labor market reforms boosted economic growth by 0.8 percentage points a year. Although there is no doubt that this conclusion is something of a simplification, the sheer extent of the difference supports the theory that the labor market reforms had a marked positive impact on growth. In the period between 1992 and 2001, total factor productivity contributed 1.0 percentage points to growth, 0.3 percentage points more than between 2005 and 2012. This tends to suggest that the growth contribution delivered by technical progress is slightly on the wane.

… The finding that the weaker productivity growth in Germany is due, to a considerable extent, to the insufficient expansion of the capital stock and, consequently, to excessive restraint in terms of investment activity, suggests that there is a widespread cause, and one that is not specific to Germany, that is putting a stranglehold on the German productivity trend.

… The hope remains, however, that especially Germany – a country that has managed to get to grips with the crisis fairly well in an international comparison – will be able to return to more dynamic investment activity as soon as possible.

The issue of under-investment is not unique to Germany and is, I believe, a by-product of quantitative easing. Interest rates are at negative real levels in a number of countries. This encourages equity investment but, simultaneously, discourages companies from investing for fear that demand for their products will decline once interest rates normalise. Instead, corporates increase dividends and buy back their own stock. European dividends grew 12.3% in 2014 although German dividend growth slowed – perhaps another sign of a return to capital investment.

German Bunds

Bunds made new highs again last week. The 10 year yield reached 19 bp. Currently, Bunds up to seven years to maturity are trading at negative yields. These were the prices on Wednesday after then 10 year Bund auction:-

| Maturity | Yield |

| 1-Year | -0.18 |

| 2-Year | -0.225 |

| 3-Year | -0.202 |

| 4-Year | -0.173 |

| 5-Year | -0.099 |

| 6-Year | -0.065 |

| 7-Year | -0.025 |

| 8-Year | 0.053 |

| 9-Year | 0.127 |

| 10Y | 0.212 |

| 15-Year | 0.38 |

| 20-Year | 0.519 |

| 30-Year | 0.626 |

Source: Investing.com

Wednesday’s 10 year auction came in at 0.25% with a cover ratio of 2.4 times, demand is still strong. The five year Bobl auction, held on 25th February, came with a negative 0.08% yield for the first time. Negative yields are becoming common-place but their implications are not clearly understood as this article from Bruegal – The below-zero lower bound explains – the emphasis is mine):-

The negative yields observed on some government and corporate bonds, as well as the recent move into further negative territory of monetary policy rates, are shaking our understanding of the ZLB constraint.

… Matthew Yglesias writes… Interest rates on a range of debt — mostly government bonds from countries like Denmark, Switzerland, and Germany but also corporate bonds from Nestlé and, briefly, Shell — have gone negative.

…Evan Soltas writes… economists had believed that it was effectively impossible for nominal interest rates to fall below zero. Hence the idea of the “zero lower bound.” Well, so much for that theory. Interest rates are going negative all around the world. And not by small amounts, either. $1.9 trillion dollars of European debt now carries negative nominal yields,

…Gavyn Davies writes… the Swiss and Danish central banks are testing where the effective lower bound on interest rates really lies. Denmark and Switzerland are clearly both special cases, because they have been subject to enormous upward pressure on their exchange rates. However, if they prove that central banks can force short term interest rates deep into negative territory, this would challenge the almost universal belief among economists that interest rates are subject to a ZLB.

…JP Koning writes that there are a number of carrying costs on cash holdings, including storage fees, insurance, handling, and transportation costs. This means that a central bank can safely reduce interest rates a few dozen basis points below zero before flight into cash begins. The lower bound isn’t a zero bound, but a -0.5% bound (or thereabouts).

…Evan Soltas writes that if people aren’t converting deposits to currency, one explanation is that it’s just expensive to carry or to store any significant amount of it… How much is that convenience worth? It seems like a hard question, but we have a decent proxy for that: credit card fees, counting both those to merchants and to cardholders… The data here suggest a conservative estimate is 2 percent annually.

…Barclays writes… Coincidentally, the ECB has calculated that the social welfare value of transactions is 2.3%.

…Brad Delong writes…In the late 19th century, the German economist Silvio Gesell argued for a tax on holding money. He was concerned that during times of financial stress, people hoard money rather than lend it.

Whilst none of these authors definitively tell us how negative is too negative, it is clear that negative rates may have substantially further to go. The only real deterrent is the negative cost of carry, which is likely to make price fluctuations more volatile.

German Stocks

Traditionally Germany was the preserve of the bond investor. Stocks have become increasingly popular with younger investors and those who need yield. Corporate bonds used to be an alternative but even these issues are heading towards a zero yield. I have argued for many years that a well-run company, whilst limited by liability, may be less likely to default or reschedule their debt than a profligate government. Even today, corporates offer a higher yield – the only major concern for an investor is the liquidity of the secondary market.

Nonetheless, with corporate yields fast converging on government bonds, stocks become the “least worst” liquid investment, since they should be supported at the zero-bound – I assume companies will not start charging investors to hold their shares. Putting it in finance terms; whereas we have been inclined to think of stocks as “growth” perpetuities, at the “less-than-zero-bound”, even a “non-growth” perpetuity looks good when compared to the negative yield on dated debt. We certainly live in interesting, or perhaps I should say “uninteresting” times.

A different case for investing in stocks is the potential restructuring risk inherent throughout the Eurozone (EZ). Michael Pettis – When do we decide that Europe must restructure much of its debt? Is illuminating on this issue:-

It is hard to watch the Greek drama unfold without a sense of foreboding. If it is possible for the Greek economy partially to revive in spite of its tremendous debt burden, with a lot of hard work and even more good luck we can posit scenarios that don’t involve a painful social and political breakdown, but I am pretty convinced that the Greek balance sheet itself makes growth all but impossible for many more years.

… while German institutions and policymakers are as responsible as those in peripheral Europe for the debt crisis, in fact it was German and peripheral European workers who ultimately bear the cost of the distortions, and it will be German households who will pay to clean up German banks as, one after another, the debts of peripheral European countries are explicitly or implicitly written down.

… In many countries in Europe there is tremendous uncertainty about how debt is going to be resolved. This uncertainty has an economic cost, and the cost only grows over time. But because most policymakers stubbornly refuse to consider what seems to have become obvious to most Europeans, there is a very good chance that Europe is going to repeat the history of most debt crises.

… For now I would argue that the biggest constraint to the EU’s survival is debt. Economists are notoriously inept at understanding how balance sheets function in a dynamic system, and it is precisely for this reason that we haven’t put the resolution of the European debt crisis at the center of the debate. But Europe will not grow, the reforms will not “work”, and unemployment will not drop until the costs of the excessive debt burdens are addressed.

If Pettis is even half-right, the restructuring of non-performing EZ debt will be a dislocating process during which EZ government bond yields will vacillate wildly. If the German government ends up footing the bill for the lion’s share of Greek debt, rather than letting its banking system default, then stocks might become an accidental “safe-haven” but I think it more likely that rising Bund yields will precipitate a decline in German stocks.

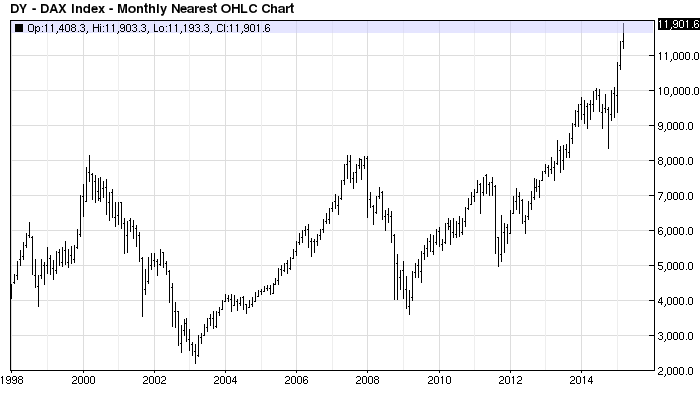

Here is how the DAX Index has reacted to the heady cocktail of ECB QE, a falling Euro and a deferral of the Greek dilemma:-

Source: Barchart.com

The DAX has more than doubled since the dark days of 2011 when the ECB saved the day with rhetoric rather than real accommodation. From a technical perspective we might have another 1,500 points to climb even from these ethereal heights – I am taking the double top of 2000 and 2007 together with the 2003 low and extrapolating a similar width of channel to the upside – around 13,500. The speed of the rally is cause for concern, however, since earnings have yet to catch up with expectations, but, as I pointed out earlier, there are non-standard reasons why the market may be inhaling ether. The current PE Ratio is 21.5 times and the recent rally has made the market look expensive relative to forward earning. At 13,500 the PE will be close to 24.5 times. This chart book from Dr Ed Yardeni makes an excellent case for caution. This is a subscriber service if you wish to sign up for a free trial.

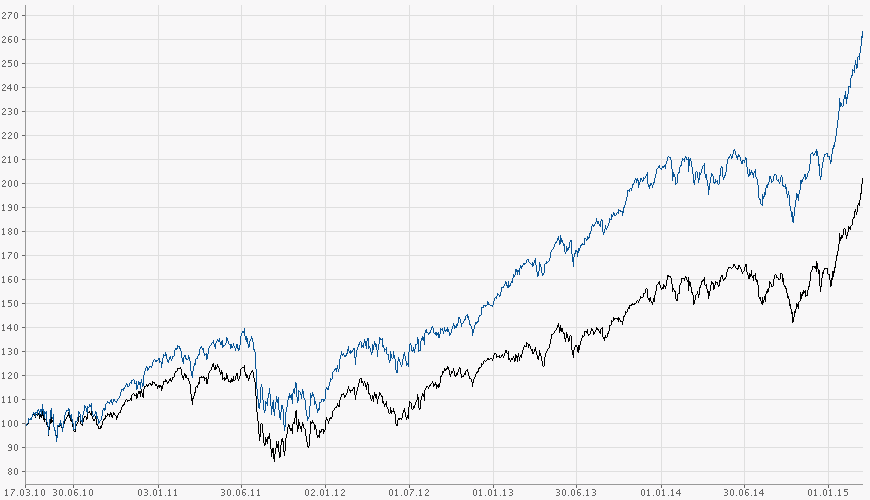

The domestic nature of the economic resurgence is exemplified most clearly by the chart below which shows the five year performance of the DAX Index versus the mid-cap MDAX Index, I believe it is time for the large cap stocks to benefit from the external windfalls of a weaker Euro and lower energy prices:-

Source: Finanzen.net

Real Estate

In Germany, Real Estate investment is different. Government policy has been to keep housing affordable and supply is therefore plentiful. This article from Inside Housing – German Lessons elaborates:-

Do you fancy a one-bed apartment in Berlin for £35,000 or a four- bed detached house in the Rhineland for £51,000?

In many parts of Germany house prices are a fraction of their UK equivalents – in fact, German house prices have decreased in real terms by 10 percent over the past thirty years, whereas UK house prices have increased by a staggering 233 percent in real terms over the same period. Yet German salaries are equal to or higher than ours. As a consequence Germans have more cash to spend on consumer goods and a higher standard of living, and they save twice as much as us, which means more capital for industry and commerce. Is it any surprise that the German economy is consistently out-performing ours?

There are a number of reasons for the disparity between the German and UK housing markets. Firstly, German home ownership is just over 40 percent compared to our 65 percent (there are stark regional variations – in Berlin 90 percent of all homes are privately rented) and the Germans do not worship ownership in the way we do. Not only is it more difficult to get mortgage finance (20 percent deposits are a typical requirement) but the private rented sector offers high quality, secure, affordable and plentiful accommodation so there are fewer incentives to buy. You can rent an 85 square metre property for less than £500 per month in Berlin or for around £360 per month in Leipzig. There is also tight rent control and unlimited contracts are common, so that tenants, if they give notice, can stay put for the long-term. Deposits must be repaid with interest on moving out.

In addition, Germany’s tax regime is not very favourable for property owners. There is a property transfer tax and an annual land tax. But the German housebuilding industry is also more diverse than ours with more prefabraction and more self-builders. The German constitution includes an explicit “right-to-build’’ clause, so that owners can build on their property or land without permission so long as it conforms with local codes.

But the biggest advantage of the German system is that they actively encourage new housing supply and release about twice as much land for housing as we do. German local authorities receive grants based on an accurate assessment of residents, so there is an incentive to develop new homes. The Cologne Institute for Economic Research calculated that in 2010 there were 50 hectares of new housing development land per 100,000 population in Germany but only 15 hectares in the UK. That means the Germans are building three times as many new homes as us pro-rata even though our population growth is greater than theirs. This means that German housing supply is elastic and can respond quickly to rising demand…

German rental protection laws – for the renter – are stronger than in other countries – this encourages renting rather than buying. From an investment perspective this makes owning German Real Estate a much more “bond like” proposition. With wages finally rising and economic prospects brightening, Real Estate is a viable alternative to fixed income. The table below was last updated in May 2014, at that time 10 yr Bunds were yielding around 1.5%:-

Source: Global Property Guide Definitions: Data FAQ |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

For comparison, commercial office space in these three locations also offers a viable yield: –

| Office Location | Yield | ||

| 2013 | 2012 | 2011 | |

| Berlin | 4.7 | 4.8 | 4.95 |

| Frankfurt | 4.65 | 4.75 | 4.9 |

| Munich | 4.4 | 4.6 | 4.75 |

Source: BNP Paribas

I believe longer term investors are fairly compensated for the relative illiquidity of German Real Estate.

The Euro

For the international investor, buying Euro denominated assets exposes one to the risk of a continued decline in the value of the currency. The Euro Effective Exchange Rate is still near the middle of its long-term range, as the chart below illustrates, though since this chart ends in Q4 2014 the Euro has weakened to around 90:-

Source: ECB

Investors must expect further Euro weakness whilst markets obsess about the departure of Greece from the EZ, however, a “Grexit” or a resolution (aka restructuring/forgiveness) of Greek debt will allow the markets to clear.

Conclusion and Investment Opportunities

German Bunds continue to be the safe-haven asset of choice for the EZ, however, for the longer term investor they offer negligible or negative returns. German Real Estate, both residential and commercial, looks attractive from a yield perspective, but take care to factor in the useful life of buildings, since capital gains are unlikely.

This leaves German equities. A secular shift from bond to equity investment has been occurring due to the low level of interest rates, this has, to some extent, countered the demographic forces of an aging German population. Nonetheless, on a P/E ratio of 21.5 times, the DAX Index is becoming expensive – the S&P 500 Index is trading around 20 times.

At the current level I feel it is late to “arrive at the party” but on a correction to test the break-out around 10,000 the DAX looks attractive, I expect upward revisions to earnings forecasts to reflect the weakness of the Euro and the lower price of energy.