Macro Letter – No 50 – 26-02-2016

Will Nigeria be forced to devalue the naira?

- The Nigerian government met the World Bank to discuss its deficit – loan pending

- The Bank of Nigeria cut rates in November – bond prices suggest further cuts are imminent

- Foreign Exchange controls tightened further in December

- President Buhari states he won’t “kill the naira”

I last wrote about Nigeria back in early June – Nigeria and South Africa – what are their prospects for growth and investment? My favoured investment was long Nigerian bonds – then trading around 13.7%. They rose above 16% as naira exchange controls tightened. Here is a chart showing what happened next:-

Source: Trading Economics, Central Bank of Nigeria

The catalyst for lower yields was an unexpected interest rate cut by the Central Bank of Nigeria. This is how it was reported by Reuters back on 25th November:-

Nigeria’s central bank cut benchmark interest rate to 11 percent from 13 percent on Tuesday, its first reduction in the cost of borrowing in more than six years.

…The stock market, which has the second-biggest weighting after Kuwait on the MSCI frontier market index , erased seven days of losses to climb to 27,662 points following the rate cut. The index has fallen 20.4 percent so far this year.

“On the back of the reduction in policy rates … investors are reconsidering investment in the equities market to earn higher return,” said Ayodeji Ebo, head of research at Afrinvest. “We anticipate further moderation in bond yields.”

He expected stocks in the industrial sector such as Dangote Cement and Lafarge Africa to gain from the liquidity surge as infrastructure projects boom. Ebo said the rate cut may hurt bank earnings as consumer firms reel from dollar shortages.

Yield on the most liquid 5-year bond fell 264 basis points to a five-year low of 7 percent while the benchmark 20-year bond closed 150 basis points down at 10.8 percent on Wednesday, traders said.

Bond yields had traded above 11 percent across maturities prior to Tuesday’s rate decision, with the 2034 bond trading at 12.30 percent.

The central bank has been injecting cash into the banking system since October in a bid to help the economy. Banking system credit stood at 290 billion naira ($1.5 bln) as of Wednesday, keeping overnight rates as low as 0.5 percent .

…The rate cut also weakened the naira on the unofficial market, which fell 0.8 percent to 242 to the dollar. The currency is pegged at 197 naira on the official market.

Non-deliverable currency forwards, a derivative product used to hedge against future exchange rate moves, indicated markets expected the naira’s exchange rate at 235.56 to the dollar in 12 months’ time – the strongest level in five months – and compared to 245.25 at Tuesday’s close

“Our economists still believe a devaluation will happen in a couple of quarters but I think they have had opportunities,” said Luis Costa, head of CEEMEA debt and FX strategy at Citi.

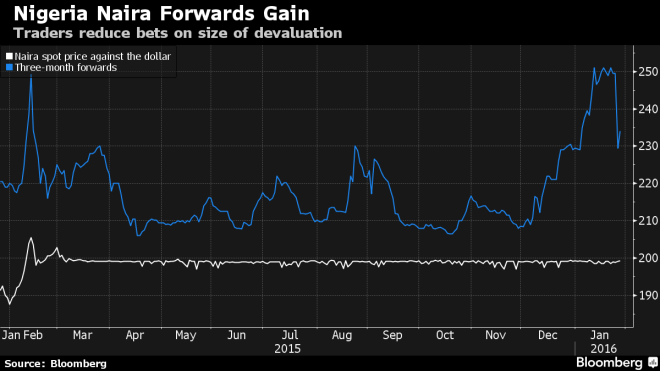

Here is a chart showing the naira spot and three month forward rate – a good surrogate for the differential between the official and black market rate:-

Source: Bloomberg

December saw a further tightening of exchange controls, the FT – Capital controls curtail spending of Nigeria’s jet set elaborates:-

Nigeria’s central bank introduced currency controls last spring as the naira came under pressure after the collapse in the price of oil, the country’s main export and the lifeblood of its economy.

As well as in effect banning imports of goods from rice to steel pipes to protect dwindling foreign exchange reserves, the central bank has also enforced spending limits on foreign currency-denominated Nigerian bank cards, much to the chagrin of Nigeria’s well-heeled travellers. These are needed, it says, to curb black market activity such as “arbitraging”: when a customer turns a quick profit by withdrawing foreign exchange from an overseas ATM to sell on the black market back home.

Another less publicised aim of the controls, according to one senior official, is to limit the flight of billions of dollars suspected to have been fraudulently obtained and then hoarded in cash by business people and officials under the former government of Goodluck Jonathan.

Last month, the central bank extended the policy by banning the use of naira-denominated debit cards altogether for overseas transactions or withdrawals. The central bank has said it will not lift the restrictions until foreign reserves, which have fallen to $29bn from $34.5bn a year ago, are restored.

There is speculation among economists about the true level of foreign exchange reserves – suffice to say $29bln is regarded as an overestimate.

The January Central Bank of Nigeria Communiqué looked back to the rate cut in November but left rates unchanged, here are some of the highlights:-

Output

…Domestic output growth in 2015 remained moderate. According to the National Bureau of Statistics (NBS), real GDP grew by 2.84 per cent in the third quarter of 2015, almost half a percentage point higher than the 2.35 per cent recorded in the second quarter. However, third quarter expansion remained substantially below the 3.96 and 6.23 per cent in the first quarter of 2015 and corresponding period of 2014, respectively. The major impetus to growth continued to come from the non-oil sector which grew by 3.05 per cent compared with the growth of 3.46 per cent posted in the preceding quarter. The major drivers of expansion in the non-oil sector were Services, Agriculture and Trade.

…The economy is expected to continue on its growth path in the first quarter 2016, albeit less robust than in the corresponding period of 2015. This expectation is predicated on the current low global oil price trend which is projected to hold low over the medium-to long term, and with attendant implications for government revenue and foreign exchange earnings. Other downside risks to growth in 2016 include: capital flow reversal, high lending rates, sluggish credit to private sector and bearish trends in the equities market.

Prices

…Core inflation declined for the third consecutive month to 8.70 per cent in November and December from 8.74 per cent in October 2015, while food inflation inched up to 10.32 per cent from 10.13 and 10.2 per cent over the same period.

Monetary, Credit and Financial Markets Developments

Broad money supply (M2) rose by 5.90 per cent in December 2015, over the level at end-December 2014, although below the growth benchmark of 15.24 per cent for 2015. Net domestic credit (NDC) grew by 12.13 per cent in the same period, but remained below the provisional benchmark of 29.30 per cent for 2015. Growth in aggregate credit reflected mainly growth in credit to the Federal Government by 151.56 per cent in December 2015 compared with 145.74 per cent in the corresponding period of 2014. The renewed increase in credit to government may be partly attributable to increased government borrowing to implement the 2015 supplementary budget.

Committee’s Considerations

The Committee observed that the last episode of low oil prices in 2005 lasted for a maximum period of 8 months. However, the current episode of lower oil prices is projected to remain over a very long period.

At the end of January, President Buhari stated that he would not “kill the naira” – this prompted some commentators to question the independence of the central bank. It also suggests that foreign exchange controls will remain in place, despite pressure from the IMF for their removal.

Conclusion and Investment Opportunities

Whilst foreign exchange controls remain in place it is difficult to access the Nigerian markets: stubbornly high inflation remains a concern which these controls will only exacerbate – see chart below:-

Source: Trading Economics, Nigerian Statistics Bureau

In this, high inflation, environment, it is difficult to envisage much further upside for government bonds. If you have been long I would take profit before the currency comes under renewed pressure. On 21st January Nigeria’s finance minister Kemi Adeosun announced that the government would borrow $5bln from international agencies to plug the shortfall in tax receipts, she has since then been in talks with the AfDB and the World Bank – after all, oil represents 95% of exports and more than two thirds of government revenue.

Stocks have fallen by more than 45% since their July 2014 highs, but further devaluation looks likely. The non-oil sector will outperform in the current environment but should the central bank “throw in the towel” it will be the energy sector which benefits in the short-term. According to Knoema, Nigerian oil production offshore is around $30/bbl whilst the smaller on-shore production is nearer $15/bbl. Other estimates suggest that only 16% of Nigerian oil reserves are worth exploiting at prices below $40/bbl. A 20% to 40% decline in the naira will reduce the break-even immediately. I remain side-lined until the valuation of the naira has been resolved.

As for the naira – a prolonged period of low oil prices will see the three month forward rate return towards NGNUSD 250 – a break towards 280 could represent a capitulation point. I believe this offers value, being 40% above the official rate. Will it happen? Yes, I think so.