Macro letter – No 61 – 16-09-2016

Is the “flight to quality” effect breaking down?

- 54% of government bonds offered negative yields at the end of August

- Corporate bond spreads did not widen during last week’s decline in government bonds

- Since July the dividend yield on the S&P500 has been higher than the yield on US 30yr bonds

- In a ZIRP to NIRP world the “capital” risk of government bonds may be under-estimated

Back in 2010 I switched out of fixed income securities. I was much too early! Fortunately I had other investments which allowed me to benefit from the extraordinary rally in government bonds, driven by the central bank quantitative easing (QE) policies.

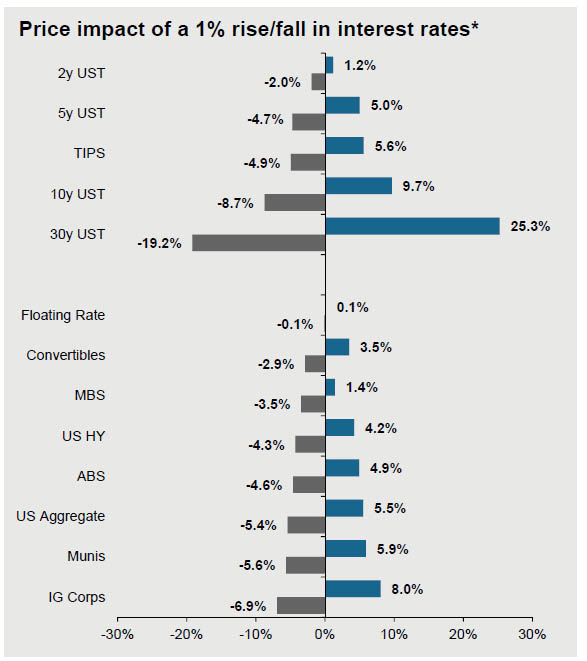

In the aftermath of Brexit the total outstanding amount of bonds with negative yields hit $13trln – that still leaves $32trln which offer a positive return. This is alarming nonetheless, according to this 10th July article from ZeroHedge, a 1% rise in yields would equate to a mark-to-market loss of $2.4trln. The chart below shows the capital impact of a 1% yield change for different categories of bonds:-

Source: ZeroHedge

Looked at another way, the table above suggests that the downside risk of holding US Treasuries, in the event of a 1% rise in yields, is 2.8 times greater than holding Investment Grade corporate bonds.

Corporate bonds, even of investment grade, traditionally exhibit less liquidity and greater credit risk, but, in the current, ultra-low interest rate, environment, the “capital” risk associated with government bonds is substantially higher. It can be argued that the “free-float” of government bonds has been reduced by central bank buying. A paper from the IMF – Government Bonds and Their Investors: What Are the Facts and Do They Matter? provides a fascinating insight into government bond holdings by investor type. The central bank with the largest percentage holding is the Bank of England (BoE) 19.7% followed by the Federal Reserve (Fed) 11.5% and the Bank of Japan (BoJ) 8.3% – although the Japanese Post Office, with 29%, must be taken into account as well. The impact of central bank buying on secondary market liquidity may be greater, however, since the central banks have principally been accumulating “on the run” issues.

Since 2008, financial markets in general, and government bond markets in particular, have been driven by central bank policy. Fear about tightening of monetary conditions, therefore, has more impact than ever before. Traditionally, when the stock market falls suddenly, the price of government bonds rises – this is the “flight to quality” effect. It also leads to a widening of the spread between “risk-free” assets and those carrying greater credit and liquidity risk. As the table above indicates, however, today the “capital” risk associated with holding government securities, relative to higher yielding bonds has increased substantially. This is both as a result of low, or negative, yields and reduced liquidity resulting from central bank asset purchases. These factors are offsetting the traditional “flight to quality” effect.

Last Friday, government bond yields increased around the world amid concerns about Fed tightening later this month – or later this year. The table below shows the change in 10yr to 30yrs Gilt yields together with a selection of Sterling denominated corporate bonds. I have chosen to focus on the UK because the BoE announced on August 4th that they intend to purchase £10bln of Investment Grade corporate bonds as part of their Asset Purchase Programme. Spreads between Corporates and Gilts narrowed since early August, although shorter maturities benefitted most.

| Issuer | Maturity | Yield | Gilt yield | Spread over Gilts | Corporate Change 7th to 12th | Gilts change 7th to 12th |

| Barclays Bank Plc | 2026 | 3.52 | 0.865 | 2.655 | 0.19 | 0.18 |

| A2Dominion | 2026 | 2.938 | 0.865 | 2.073 | 0.03 | 0.18 |

| Sncf | 2027 | 1.652 | 0.865 | 0.787 | 0.18 | 0.18 |

| EDF | 2027 | 1.9 | 0.865 | 1.035 | 0.19 | 0.18 |

| National Grid Co Plc | 2028 | 1.523 | 0.865 | 0.658 | 0.19 | 0.18 |

| Italy (Republic of) | 2028 | 2.891 | 0.865 | 2.026 | 0.17 | 0.18 |

| Kreditanstalt fuer Wiederaufbau | 2028 | 1.187 | 0.865 | 0.322 | 0.18 | 0.18 |

| EIB | 2028 | 1.347 | 0.865 | 0.482 | 0.18 | 0.18 |

| BT | 2028 | 1.976 | 0.865 | 1.111 | 0.2 | 0.18 |

| General Elec Cap Corp | 2028 | 1.674 | 0.865 | 0.809 | 0.2 | 0.18 |

| Severn Trent | 2029 | 1.869 | 1.248 | 0.621 | 0.19 | 0.18 |

| Tesco Plc | 2029 | 4.476 | 1.248 | 3.228 | 0.2 | 0.18 |

| Procter & Gamble Co | 2030 | 1.683 | 1.248 | 0.435 | 0.2 | 0.18 |

| RWE Finance Bv | 2030 | 3.046 | 1.248 | 1.798 | 0.17 | 0.22 |

| Citigroup Inc | 2030 | 2.367 | 1.248 | 1.119 | 0.2 | 0.22 |

| Wal-mart Stores | 2030 | 1.825 | 1.248 | 0.577 | 0.2 | 0.22 |

| EDF | 2031 | 2.459 | 1.248 | 1.211 | 0.22 | 0.22 |

| GE | 2031 | 1.778 | 1.248 | 0.53 | 0.21 | 0.22 |

| Enterprise Inns plc | 2031 | 6.382 | 1.248 | 5.134 | 0.03 | 0.22 |

| Prudential Finance Bv | 2031 | 3.574 | 1.248 | 2.326 | 0.19 | 0.22 |

| EIB | 2032 | 1.407 | 1.248 | 0.159 | 0.2 | 0.22 |

| Kreditanstalt fuer Wiederaufbau | 2032 | 1.311 | 1.248 | 0.063 | 0.19 | 0.22 |

| Vodafone Group PLC | 2032 | 2.887 | 1.248 | 1.639 | 0.24 | 0.22 |

| Tesco Plc | 2033 | 4.824 | 1.248 | 3.576 | 0.21 | 0.22 |

| GE | 2033 | 1.88 | 1.248 | 0.632 | 0.21 | 0.22 |

| Proctor & Gamble | 2033 | 1.786 | 1.248 | 0.538 | 0.2 | 0.22 |

| HSBC Bank Plc | 2033 | 3.485 | 1.248 | 2.237 | 0.21 | 0.22 |

| Wessex Water | 2033 | 2.114 | 1.248 | 0.866 | 0.19 | 0.22 |

| Nestle | 2033 | 0.899 | 1.248 | -0.349 | 0.16 | 0.22 |

| Glaxo | 2033 | 1.927 | 1.248 | 0.679 | 0.2 | 0.22 |

| Segro PLC | 2035 | 2.512 | 1.401 | 1.111 | 0.19 | 0.22 |

| Walmart | 2035 | 2.028 | 1.401 | 0.627 | 0.2 | 0.22 |

| Aviva Plc | 2036 | 3.979 | 1.401 | 2.578 | 0.18 | 0.22 |

| General Electric | 2037 | 2.325 | 1.401 | 0.924 | 0.23 | 0.22 |

| Lcr Financial Plc | 2038 | 1.762 | 1.401 | 0.361 | 0.2 | 0.22 |

| EIB | 2039 | 1.64 | 1.401 | 0.239 | 0.2 | 0.22 |

| Lloyds TSB | 2040 | 2.693 | 1.495 | 1.198 | 0.2 | 0.22 |

| GE | 2040 | 2.114 | 1.495 | 0.619 | 0.2 | 0.22 |

| Direct Line | 2042 | 6.738 | 1.495 | 5.243 | 0.06 | 0.22 |

| Barclays Bank Plc | 2049 | 3.706 | 1.4 | 2.306 | 0.1 | 0.22 |

Source: Fixed Income Investor, Investing.com

The spread between international issuers such as Nestle – which, being Swiss, trades at a discount to Gilts – narrowed, however, higher yielding names, such as Direct Line, did likewise.

For comparison the table below – using the issues in bold from the table above – shows the change between the 22nd and 23rd June – pre and post-Brexit:-

| Maturity | Gilts 22-6 | Corporate 22-6 | Gilts 23-6 | Corporate 23-6 | Issuer | Spread 22-6 | Spread 23-6 | Spread change |

| 10y | 1.314 | 4.18 | 1.396 | 4.68 | Barclays | 2.866 | 3.284 | 0.418 |

| 15y | 1.879 | 3.86 | 1.96 | 3.88 | Vodafone | 1.981 | 1.92 | -0.061 |

| 20y | 2.065 | 4.76 | 2.124 | 4.78 | Aviva | 2.695 | 2.656 | -0.039 |

| 25y | 2.137 | 3.42 | 2.195 | 3.43 | Lloyds | 1.283 | 1.235 | -0.048 |

| 30y | 2.149 | 4.21 | 2.229 | 4.23 | Barclays | 2.061 | 2.001 | -0.06 |

Source: Fixed Income Investor, Investing.com

Apart from a sharp increase in the yield on the 10yr Barclays issue (the 30yr did not react in the same manner) the spread between Gilts and corporates narrowed over the Brexit debacle too. This might be because bid/offer spreads in the corporate market became excessively wide – Gilts would have become the only realistic means of hedging – but the closing prices of the corporate names should have reflected mid-market yields.

If the “safe-haven” of Gilts has lost its lustre where should one invest? With patience and in higher yielding bonds – is one answer. Here is another from Ben Lord of M&G’s Bond Vigilantes – The BoE and ECB render the US bond market the only game in town:-

…The ultra-long conventional gilt has returned a staggering 52% this year. Since the result of the referendum became clear, the bond’s price has increased by 20%, and in the couple of weeks since Mark Carney announced the Bank of England’s stimulus package, the bond’s price has risen by a further 13%.

…the 2068 index-linked gilt, which has seen its price rise by 57% year-to-date, by 35% since the vote to exit Europe, and by 18% since further quantitative easing was announced by the central bank. Interestingly, too, the superior price action of the index-linked bond has occurred not as a result of rising inflation or expectations of inflation; instead it has been in spite of significantly falling inflation expectations so far this year. The driver of the outperformance is solely due to the much longer duration of the linker. Its duration is 19 years longer than the nominal 2068 gilt, by virtue of its much lower coupon!

When you buy a corporate bond you don’t just buy exposure to government bond yields, you also buy exposure to credit risk, reflected in the credit spread. The sterling investment grade sector has a duration of almost 10 years, so you are taking exposure to the 10 year gilt, which has a yield today of circa 0.5%. If we divide the yield by the bond’s duration, we get a breakeven yield number, or the yield rise that an investor can tolerate before they would be better off in cash. At the moment, as set out above, the yield rise that an investor in a 10 year gilt (with 9 year’s duration) can tolerate is around 6 basis points (0.5% / 9 years duration). Given that gilt yields are at all-time lows, so is the yield rise an investor can take before they would be better off in cash.

We can perform the same analysis on credit spreads: if the average credit spread for sterling investment grade credit is 200 basis points and the average duration of the market is 10 years, then an investor can tolerate spread widening of 20 basis points before they would be better off in cash. When we combine both of these breakeven figures, we have the yield rise, in basis points, that an investor in the average corporate bond or index can take before they should have been in cash.

With very low gilt yields and credit spreads that are being supported by coming central bank buying, accommodative policy and low defaults, and a benign consumption environment, it is no surprise that corporate bond yield breakevens are at the lowest level we have gathered data for. It is for these same reasons that the typical in-built hedge characteristic of a corporate bond or fund is at such low levels. Traditionally, if the economy is strong then credit spreads tighten whilst government bond yields sell off, such as in 2006 and 2007. And if the economy enters recession, then credit spreads widen and risk free government bond yields rally, such as seen in 2008 and 2009.

With the Bank of England buying gilts and soon to start buying corporate bonds, with the aim of loosening financial conditions and providing a stimulus to the economy as we work through the uncertain Brexit process and outcome, low corporate bond breakevens are to be expected. But with Treasury yields at extreme high levels out of gilts, and with the Fed not buying government bonds or corporate bonds at the moment, my focus is firmly on the attractive relative valuation of the US corporate bond market.

The table below shows a small subset of liquid US corporate bonds, showing the yield change between the 7th and 12th September:-

| Issuer | Issue | Yield | Maturity | Change 7th to 12th | Spread | Rating |

| Home Depot | HD 2.125 9/15/26 c26 | 2.388 | 10y | 0.17 | 0.72 | A2 |

| Toronto Dominion | TD 3.625 9/15/31 c | 3.605 | 15y | 0.04 | 1.93 | A3 |

| Oracle | ORCL 4.000 7/15/46 c46 | 3.927 | 20y | 0.14 | 1.54 | A1 |

| Microsoft | MSFT 3.700 8/8/46 c46 | 3.712 | 20y | 0.13 | 1.32 | Aaa |

| Southern Company | SO 3.950 10/1/46 c46 | 3.973 | 20y | 0.18 | 1.58 | Baa2 |

| Home Depot | HD 3.500 9/15/56 c56 | 3.705 | 20y | 0.19 | 1.31 | A2 |

| US Treasury | US10yr | 1.67 | 10y | 0.13 | N/A | AAA |

| US Treasury | US30y | 2.39 | 30y | 0.16 | N/A | AAA |

Source: Market Axess, Investing.com

Except for Canadian issuer Toronto Dominion, yields moved broadly in tandem with the T-Bond market. The spread between US corporates and T-Bonds may well narrow once the Fed gains a mandate to buy corporate securities, but, should Fed negotiations with Congress prove protracted, the cost of FX hedging may negate much of the benefit for UK or European investors.

What is apparent, is that the “flight to quality” effect is diminished even in the more liquid and higher yielding US market.

The total market capitalisation of the UK corporate bond market is relatively small at £285bln, the US market is around $4.5trln and Europe is between the two at Eur1.5trln. The European Central Bank (ECB) began its Corporate Sector Purchase Programme (CSPP) earlier this summer but delegated the responsibility to the individual National Banks.

Between 8th June and 15th July Europe’s central banks purchased Eur10.43bln across 458 issues. The average position was Eur22.8mln but details of actual holdings are undisclosed. They bought 12 issues of Deutsche Bahn (DBHN) 11 of Telefonica (TEF) and 10 issues of BMW (BMW) but total exposures are unknown. However, as the Bond Vigilantes -Which corporate bonds has the ECB been buying? point out, around 36% of all bonds eligible for the CSPP were trading with negative yields. This was in mid-July, since then 10y Bunds have fallen from -012% to, a stellar, +0.3%, whilst Europe’s central banks have acquired a further Eur6.71bln of corporates in August, taking the mark-to-market total to Eur19.92bln. The chart below shows the breakdown of purchases by country and industry sector at the 18th July:-

Source: M&G Investments, ECB, Bloomberg

Here is the BIS data for total outstanding financial and non-financial debt as at the end of 2015:-

| Country | US$ Blns |

| France | 2053 |

| Spain | 1822 |

| Netherlands | 1635 |

| Germany | 1541 |

| Italy | 1023 |

| Luxembourg | 858 |

| Denmark | 586 |

Source: BIS

In terms of CSPP holdings, Germany appears over-represented, Spain and the Netherlands under-represented. The “devil”, as they say, is in the “detail” – and a detailed breakdown by issuer, issue and size of holding, has not been published. The limited information is certainly insufficient for traders to draw any clear conclusions about which issues to buy or sell. As Wolfgang Bauer, the author of the M&G article, concludes:-

But as tempting as it may be to draw conclusions regarding over- and underweights and thus to anticipate the ECB’s future buying activity, we have to acknowledge that we are simply lacking data. Trying to “front run” the ECB is therefore a highly difficult, if not impossible task.

Conclusions and investment opportunities

Back in May the Wall Street Journal published the table below, showing the change in the portfolio mix required to maintain a 7.5% return between 1995 and 2015:-

Source: Wall Street Journal, Callan Associates

The risk metric they employ is volatility, which in turn is derived from the daily mark-to-market price. Private Equity and Real-Estate come out well on this measure but are demonstrably less liquid. However, this table also misses the point made at the beginning of this letter – that “risk-free” assets are encumbered with much higher “capital” risk in a ZIRP to NIRP world. The lower level of volatility associated with bond markets disguises an asymmetric downside risk in the event of yield “normalisation”.

Dividends

Corporates with strong cash flows and rising earnings are incentivised to issue debt either for investment or to buy back their own stock; thankfully, not all corporates and leveraging their balance sheets. Dividend yields are around the highest they have been this century:-

Source: Multpl.com

Meanwhile US Treasury Bond yields hit their lowest ever in July. Below is a sample of just a few higher yielding S&P500 stocks:-

| Stock | Ticker | Price | P/E | Beta | EPS | DPS | Payout Ratio | Yield |

| At&t | T | 39.97 | 17.3 | 0.56 | 2.3 | 1.92 | 83 | 4.72 |

| Target | TGT | 68.94 | 12.8 | 0.35 | 5.4 | 2.4 | 44 | 3.46 |

| Coca-cola | KO | 42.28 | 24.3 | 0.73 | 1.7 | 1.4 | 80 | 3.24 |

| Mcdonalds | MCD | 114.73 | 22.1 | 0.61 | 5.2 | 3.56 | 69 | 3.07 |

| Procter & Gamble | PG | 87.05 | 23.6 | 0.66 | 3.7 | 2.68 | 73 | 3.03 |

| Kimberly-clark | KMB | 122.39 | 22.8 | 0.61 | 5.4 | 3.68 | 68 | 2.98 |

| Pepsico | PEP | 104.59 | 29.5 | 0.61 | 3.6 | 3.01 | 85 | 2.84 |

| Wal-mart Stores | WMT | 71.46 | 15.4 | 0.4 | 4.6 | 2 | 43 | 2.78 |

| Johnson & Johnson | JNJ | 117.61 | 22.1 | 0.43 | 5.3 | 3.2 | 60 | 2.69 |

Source: TopYield.nl

The average beta of the names above is 0.55 – given that the S&P500 has an historic volatility of around 15%, this portfolio would have a volatility of 8.25% and an average dividend yield of 3.2%. This is not a recommendation to buy an equally weighted portfolio of these stocks, merely an observation about the attractiveness of returns from dividends.

Government bonds offer little or no return if held to maturity – it is a traders market. For as long as central banks keep buying, bond prices will be supported, but, since the velocity of the circulation of money keeps falling, central banks are likely to adopt more unconventional policies in an attempt to transmit stimulus to the real economy. If the BoJ, BoE and ECB are any guide, this will lead them (Fed included) to increase purchases of corporate bonds and even common stock.

Bond bear-market?

Predicting the end of the bond bull-market is not my intention, but if central banks should fail in their unconventional attempts at stimulus, or if their mandates are withdrawn, what has gone up the most (government bonds) is likely to fall farthest. At some point, the value of owning “risk-free” assets will reassert itself, but I do not think a 1% rise in yields will be sufficient. High yielding stocks from companies with good dividend cover, low betas and solid cash flows, will weather the coming storm. These stocks may suffer substantial corrections, but their businesses will remain intact. When the bond bubble finally bursts “risky” assets may be safer than conventional wisdom suggests. The breakdown in the “flight to quality” effect is just one more indicator that the rules of engagement are changing.