Macro Letter – No 60 – 02-09-2016

Drowning in debt

- Central Banks are moving from quantitative to qualitative easing

- The spread between Investment Grade and Government bond yields is narrowing

- Issuing corporate debt rather than equity has never been so attractive

- Corporate leverage is rising, share buy-backs continue but investment remains weak

I was always

Far out at sea

And not waving

But drowning

Stevie Smith

During August the financial markets have been relatively quiet, however, the Bank of England (BoE) cut interest rates on 4th and added Investment Grade Corporate bonds to their Asset Purchase Programme. The following day Vodafone (VOD) issued a 40yr bond yielding 3% – a week earlier they had issued a 33yr bond yielding 3.4%.

Meanwhile, at Jackson Hole the Kansas City Federal Reserve Symposium discussed a paper by Professor Jeremy Stein – a member Federal Reserve board member between 2012 and 2014 – and two other Harvard professors entitled The Federal Reserve Balance Sheet as a Financial Stability Tool – in which the authors argue that the Fed should maintain its balance sheet at around $4.5trln but that it “should use its balance sheet to lean against private-sector maturity transformation.” In layman’s terms this is a “call to arms” encouraging the Fed to seek approval from the US government to allow the purchase a much wider range of corporate securities. It would appear that the limits of central bank omnipotence have yet to be reached. The Bank of Japan has already begun to discover the unforeseen effect that negative interest rate policy has on the velocity of the circulation of money – it collapses. Now central bankers, who’s credibility has begun to be questioned in some quarters of late, are considering the wider use of “qualitative” measures.

As Bastiat has taught us, that which is seen from these policies is a reduction in the cost of borrowing for “investment grade” corporations. What is not seen, so clearly, is the incentive corporates have to borrow, not to invest, but to buy back their own stock. Perhaps I am being unfair, but, in a world which is drowning in debt, central bankers seem to think that the over-indebted are not “drowning” but “waving”.

One of the most cherished ideas, promulgated upon an unsuspecting world, is the concept of using fiscal and monetary stimulus to offset cyclical economic downturns. The aim of these “popular” policies is to soften the blow of economic slowdowns – all highly laudable provided the “punch bowl” is withdrawn during the cyclical recovery.

So much for business cycles: but what about the impact these policies may have on structural changes in economic performance relating to supply and demand for factors of production, such as labour, fixed assets or basic materials? I’m thinking here about the impact, especially, of technology and demographics.

Firstly, the cyclical stimulus extended during the downturn is seldom withdrawn during the upturn and secondly, long term structural changes in economies are seldom considered by governments, since these changes evolve over decades or generations, rather than the span of a single parliament. This is an essential weakness in the democratic process which has stifled economic growth for centuries. This excellent paper from Carmen M. Reinhart, Vincent R. Reinhart, and Kenneth S. Rogoff – The Journal of Economic Perspectives – Volume 26 – No 3 – Summer 2012 – Public Debt Overhangs: Advanced Economy Episodes Since 1800 makes this weakness abundantly clear.

The authors expand on their earlier research, this time looking at the impact of excessive public debt overhang on economic growth. They take as their “line in the sand” the point where the government debt to nominal GDP ratio remains above 90% for more than five years. They identify 26 episodes, 20 of which lasted more than a decade – the average was 23 years. It is worth noting that more than one third of these episodes occurred without interest rates rising above normal levels.

In 23 of the 26 episodes, over the 211 year sample, the pace of economic growth was lowered from 3.5% to 2.3% – in other words GDP was reduced by roughly one third. The long term secular impact of high debt and lower growth needs to be weighed against the short-term benefits of Keynesian stimulus. A lowering of the GDP growth rate of 1.2% for 23 years is equivalent to a 24.25% reduction in the potential size of the economy at the end of the debt overhang period – a tall price for any economy to pay.

The authors briefly examine the other types of outstanding debt, in order to arrive at what they dub “the quadruple debt overhang problem”, namely, private debt, external debt (and its associated currency risks) and the “actuarial” debt implicit in “unfunded” pension schemes and medical insurance programmes. This data is hard to untangle but the authors state:-

…the overall magnitude of the debt burdens facing the advanced economies as a group is in many dimensions without precedent. The interaction between the different types of debt overhang is extremely complex and poorly understood, but it is surely of great potential importance.

The 22 developed economies in their sample are now burdened with debt to GDP ratios above the levels seen in the aftermath of WWII. Their 48 emerging market counterparts had their epiphany in the debt crisis of the mid 1980’s, since when they have assumed a certain sobriety of character. This shows up even more glaringly in the divergence since 1986 in the public, plus private, external debt. In developed countries it has risen from around 75% of GDP to more than 250% whilst emerging economies external debt has fallen from a broadly similar 75% to less than 50% today. Governments, often bailout private external debt holders in order to protect the stability of their currencies.

Private domestic credit is another measure of total indebtedness which the authors analyse. For the 48 emerging economies this has remained constant at around 40% of GDP since the mid-1980s whilst in the developed 22 it has risen from 50% in the 1950’s to above 150% today. Since the bursting of the technology stock bubble in 2000 this trend has accelerated but the authors point out that these increases are often caused by cross border capital inflows.

The rise in the debt to GDP ratio may come from a slowing in growth rather than an increase in government debt but the correlation between rising debt and slowing GDP rises dramatically as the ratio exceeds 90%.

The authors draw the following conclusions:-

…First, once a public debt overhang has lasted five years, it is likely to last 10 years or much more (unless the debt was caused by a war that ends).

…it is quite possible to have a “no drama” public debt overhang, which doesn’t involve a rise in real interest rates or a financial crisis. Indeed, in 11 of our 26 public debt overhang episodes, real interest rates were on average comparable, or lower, than at other times.

…Another line of reasoning for dismissing concerns about public debt overhangs is the view that causality mostly runs from growth to debt. However, we discussed a body of evidence which argues runs from growth to debt. However, we discussed a body of evidence which argues that causality does indeed run from the public debt overhang to slower growth. There are counterexamples where a public debt overhang was accompanied by rapid growth, like the immediate period after World War II for the United States and United Kingdom, but these exceptions to the typical pattern do not seem to be the most relevant parallels for the modern world economy.

…The pathway to containing and reducing public debt will require a change that is sustained over the middle and the long term. However, the evidence, as we read it, casts doubt on the view that soaring government debt does not matter when markets (and official players, notably central banks) seem willing to absorb it at low interest rates—as is the case for now.

The Methadone of the Markets

The bull market in fixed income securities began in the early 1980’s. The price of “risk free” assets has always had a significant influence on the valuation of equities but, since the advent of quantitative easing, the principle driver of performance has become the level of interest rates. As the yield on fixed income securities has inexorably declined the spread between the dividend and bond yield has returned to positive territory after many years of inversion.

Companies with growing earnings from their operations can finance more cheaply than at any time in history. Provided they can sustain their growth, their bonds should, theoretically, begin to trade at a discount to government bonds. This would probably have happened before now had the central banks not embarked on quantitative easing revolving around the purchase of government bonds at already artificially inflated prices. The rules on capital weighting which favour “risk free” assets and regulations requiring pension funds and other financial institutions to hold minimum levels of “risk free” assets has further distorted the marketplace.

The unfunded government pension schemes of developed nations are at the mercy of the demographic headwind of a smaller working age population supporting a growing legion of retirees. Added to which, breakthroughs in medical science suggest that actuarial expectations of life expectancy may once again be underestimated.

Ways out of debt

There are a number of solutions other than fiscal austerity. For example, increasing the pensionable age steadily towards the average life expectancy. This may sound extreme but in January 1909, when the pension was first introduced in the UK, the pensionable age was 70 years and life expectancy was 50 years for men and 53.5 for women. The latest ONS data shows male life expectancy at 79 years whilst for females it is 82.8 years. The pensionable age for women has now risen to 63 years and will be brought in line with men (65 years) by 2018. There is still a long way to go, by 2030 the NHS estimate the male average will be 85.7 years, with females living an average of 87.6 years. Meanwhile the pensionable age will reach 68 years by 2028. In other words, the current, deeply unpopular, proposed increase in the pensionable age is barely keeping pace with the projected increase in life expectancy.

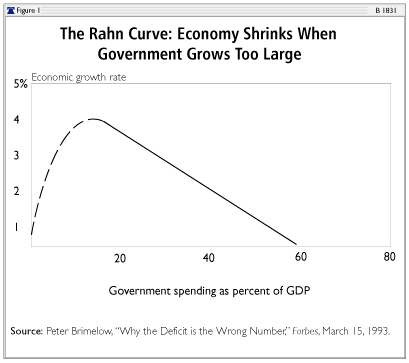

Another solution which would help to reduce the level of public debt is a structural policy of capping government spending at less than 40% of GDP. This could be relaxed to less than 50% during recessions as a temporary counter-cyclical measure. UK GDP averaged 2.47% since 1953 – if government spending only increased slightly less than 1% per annum we could steadily reduce the public sector debt burden towards a manageable 30% level over the next 40 years, after all, as recently as 2005 the ratio of government debt to GDP was at 38%. The chart below of the Rahn Curve shows the optimal ratio of government debt to GDP. Once government spending exceeds 15% it acts as a drag on the potential growth of an economy:-

Source: The Heritage Foundation, Peter Brimelow

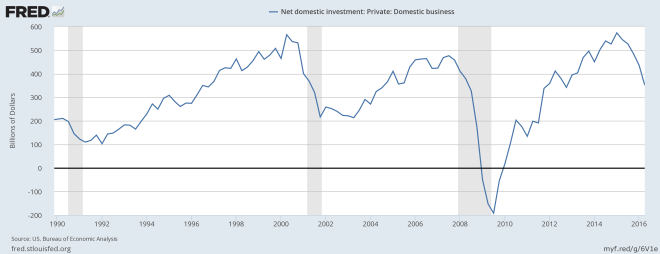

The interest paid on corporate debt and bank loans is tax deductible which creates an incentive to issue debt rather than equity. It is difficult to change this situation but mandating that equity may only be retired from after-tax profits would encourage leverage for investment purposes rather than to artificially enhance the return on equity. The chart below shows the decline in net domestic investment in the US despite historically low interest rates:-

Source: Federal Reserve Bank of St Louis

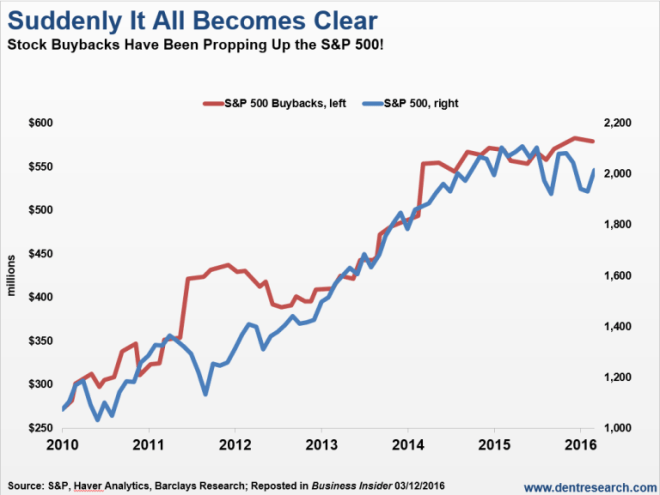

The next chart shows the level of share buybacks and the performance of the S&P500:-

Source: Dent Research, S&P, Haver Analytics, Barclays Research, Business Insider

Household debt is predominantly in the form of mortgages. In most developed countries a shortage of housing stock, due to planning restrictions, has encouraged individuals to speculate in the real estate market. In fact BoE Chief Economist Andy Haldane was quoted in The Sunday Times – Property is a better bet than pensions, says gold-plated Bank guru stating that pensions were complex and housing was a better investment:-

As long as we continue not to build anything like as many houses in this country as we need to … we will see what we’ve had for the better part of a generation, which is house prices relentlessly heading north.

The solution is planning reform. This will reduce house price inflation but it will not reduce the level of mortgage debt, however, once housing ceases to be a “one way bet” the attraction of leveraged speculation in property will diminish.

Conclusions and Investment Opportunities

The underlying problem which caused the great recession of 2009/2010 was excessive debt. The policy response has been to throw petrol on the fire. The first phase of unconventional monetary policy – reducing official interest rates towards zero – has more or less run its course. The next phase – qualitative easing – is now under way. This will start with corporate bonds and proceed to other securities ending up with common stock. Credit spreads will continue to narrow even if government bond yields rise. There will, of course, be episodes of panic when “safe haven” government bonds outperform but this will be temporary and the spread widening will present a buying opportunity.

The UK Investment Grade bond market is relatively small at £285bln and liquidity is therefore less robust than for Euro or US$ denominated issues but there is a £10bln “put” beneath the market. Other initiatives will be forthcoming from the central banks. Their actions will continue to be the dominant factor influencing asset prices in general.