Macro Letter – No 44 – 23-10-2015

What’s right with the Trans-Pacific Partnership?

- The TPP may boost real-incomes by $285bln by 2025

- US Congress should approve the TPP to avoid international political embarrassment

- The TPP may be expanded to include South Korea, Taiwan and maybe even China

- Many companies involved in auto, pharma, IT and agricultural should benefit

For Asia-Pacific, the Trans-Pacific Partnership (TPP) is the most substantial trade agreement in history. In this video Cato Institute – Putting the TPP in Perspective: 150 Years of U.S. Trade Policy in Less than 4 Minutes – remind us that this is a “Managed Trade Agreement” rather than a “Free Trade Agreement” (FTA).

The 12 TPP participating countries – Australia, Brunei, Canada, Chile, Japan, Malaysia, Mexico, New Zealand, Peru, Singapore, USA and Vietnam – represent almost 40% of output and 25% of exports of goods and services globally. This makes it the largest regional trade agreement in history.

After five years of “horse-trading” and “turf-wars” the agreement was finally signed on 5th October, yet, with US Congressional enactment still awaited in December, much media commentary has focussed on the weaknesses of the agreement. These include:-

- Agriculture – Japanese resistance to the elimination of tariffs on agricultural imports, including rice, beef, pork, dairy, wheat, barley, and sugar. Japan’s average most-favoured nation (MFN) tariff for agricultural products is 16.6% – although some tariffs are as high as 700%. The US accounts for 25% of agricultural imports to Japan.

- Intellectual property rights – Whilst all TPP members agree on high IP standards, the devil is in the detail. The period of data exclusivity for drug tests, protection of trade secrets, and liability of ISPs for transmitting illegal/pirated material all remain contentious.

- State-owned enterprises – TPP members are committed to levelling the playing field in respect of preferential access to finance or new markets. Problems arise over the length of the transition period before the new rules must be adopted, standardisation of accounting practices, board governance and unbiased procurement processes.

- Labour – Issues remain around the adoption of ILO Fundamental Principles, prohibiting workplace discrimination and upholding consistent child labour practices.

- Investor-State Dispute Settlement – Investor-State Dispute Settlement provisions allow international investors to use dispute settlement proceedings against host governments if they believe their property has been expropriated without compensation or regulated in a discriminatory manner. TPP members disagree about the extent of carve-outs from Investor-State Dispute Settlements for health, safety, and environmental regulations.

According to the Independent – TPP trade agreement text won’t be made public for four years – so in the interim here is the USTR Summary.

The Guardian – Wikileaks release of TPP deal text stokes ‘freedom of expression’ fears – provides more details about Chapter 12, covering IP, yet it is not clear whether this is the final version of the document or not.

In attempting to assess the initial deal The Economist – Every silver lining has a cloud – said:-

First, there is the fact that the agreement has been so hard to sell in America. It took months, and several legislative setbacks, before Barack Obama won the authority to fast-track a congressional vote on TPP. The deal may still be voted down, in America or elsewhere. Those who would succeed Mr Obama as president know that TPP holds few votes. This week Hillary Clinton, the Democratic front-runner and once a promoter of TPP, came out against it. The beneficiaries of TPP—consumers, as well as exporters—are numerous, but their potential gains diffuse. By contrast, inefficient firms and farms, about to be exposed to greater foreign competition, are obvious and vocal. Canada, for example, limited the threat to its dairy farmers and doled out a big new subsidy. The saga is a reminder of how hard free trade is to champion.

Second, the TPP deal underscores the shift away from global agreements. The World Trade Organisation, which is responsible for global deals, has been trying, and largely failing, to negotiate one since 2001. Reaching agreement among its 161 members, especially now that average tariffs around the world are relatively low and talks are focused on more contentious obstacles to trade, has proved almost impossible. Regional deals are the next best thing, but, by definition, they exclude some countries, and so may steer custom away from the most efficient producer. In the case of TPP, the glaring outcast is China, the linchpin of most global supply chains.

Third, good news on TPP stands in contrast to bad news elsewhere. Cross-border trade today is as much about the exchange of data as it is the flow of goods and services: this week saw the annulment by a European court of a deal that had enabled American firms to transfer customer data across the Atlantic. Conventional trade faces even stronger headwinds. The volume of goods shipped in the first half of this year was just 1.9% higher than in the same period of 2014, far below its long-term average growth of 5%. This reflects not only China’s soggy demand for imports—a threat to the developing economies that supply it—but also the accumulation of minor measures that silt up global trade.

Deals like TPP are the most effective way to reverse this sorry trend, by reducing tariffs and other obstacles to trade. Optimists hope it can now be expanded, to include China and others. Sadly, experience suggests that will be hard.

Looked at from a more positive perspective, the TPP tops the US trade policy agenda, incorporating President Obama’s “Asia Pivot”. Signatory countries account for 36% of US trade in goods and services. US ratification of this agreement will upgrade a range of existing FTAs stretching back to NAFTA (1994).

With some exceptions – mostly in agriculture – the TPP aims to remove tariff barriers for goods and services. It will also address some “access” issues in areas such as competition policy, direct investment, labour and environmental standards.

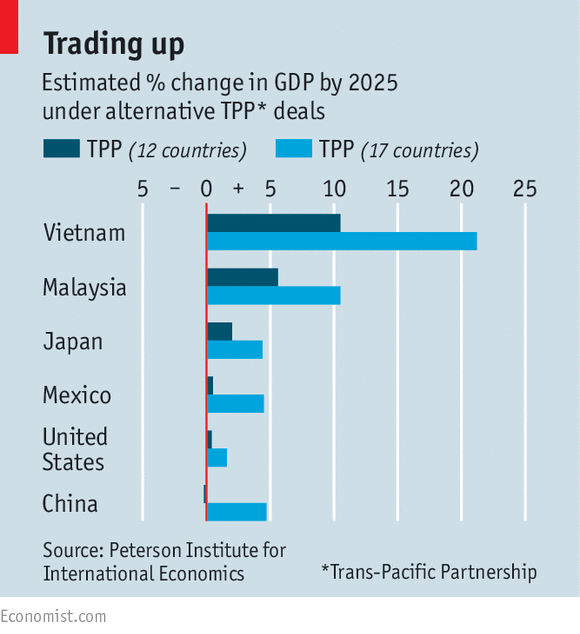

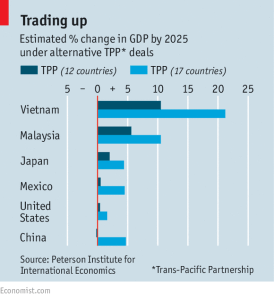

Japan and the US will be the principal beneficiaries of the TPP (64% of GDP gains) but it has been estimated that the agreement could boost real incomes of member countries by $285bln by 2025, with exports increasing by $440 billion (+7%) assuming full-adoption.

The TPP could achieve even more since is allows for the future accession of new members. South Korea, possibly regretting its decision not to take part in the initial negotiations, has announced its interest, while Indonesia, the Philippines, Thailand, and Taiwan are evaluating the benefits. It might even form the framework for a bilateral FTA between the US and China. The chart below shows the potential benefit in GDP terms:-

Source: Economist and Peterson Institute

A brief history of free-trade

Source: Mises.org

The liberal idea of free trade sprang from the earliest discoveries in the field of economics. It is the embodiment of the spirit of “comparative advantage” – David Riccardo’s observation that specialisation makes economic sense and that those agents with a natural economic advantage should specialise and trade, rather than attempting to produce all goods to meet their own needs.

There are difficulties in achieving genuine free trade. Consumer organisations are relatively weak in comparison with trade organisations: this iniquity is the flaw at the heart of so many FTAs. Consumers, if consulted, would vote unanimously in favour of cheaper goods. Inflation targeting might prove difficult for central banks but people’s standard of living would improve, all other things equal. This is the benign face of deflation; it is also the reason why productivity growth is critical to economic progress.

Since the time of Sumer, empire building has involved conquest, assimilation and trade. Artefacts of North African and Middle-Eastern origin uncovered at Roman archaeological sites in Britain, bears testament to the wide-spread distribution of goods throughout the Roman Empire.

The Spanish theologian, philosopher and jurist Francisco de Vitoria (1483 – 1546) developed the first ideas about freedom of commerce and freedom of the seas. A forerunner to FTAs, were the “most favoured nation” (MFN) clauses attached to international treaties during the European colonial era – many of these MFN clauses are still in use today – but it was the philosopher Adam Smith, along with Ricardo, who articulated what we would recognise as free-trade theory today.

William Huskisson (1770 – 1830) was appointed President of the Board of Trade and Treasurer of the Navy in 1823. He was part of the Canningite faction of the Tory party, led by George Canning, which formed a brief coalition government in 1827. Perhaps Huskisson’s greatest contribution to free-trade was his reform the Navigation Acts. This allowed other nations full equality and reciprocity of shipping duties, it repealed the labour laws, introduced a new sinking fund, reduced duties on manufactures and foreign imports, and repealed quarantine duties.

Huskisson had also been a member of the committee appointed to inquire into the causes of the agricultural distress of 1821 – this committee proposed a relaxation of the Corn Laws chiefly due to his strenuous advocacy. Sadly it was the potato famine in Ireland that eventually saw their repeal in 1846. It was the campaign to repeal the Corn Laws which eventually led to the next great clarion for free trade, the Cobden-Chevalier Treaty of 1860. The treaty reduced French duties on most British manufactured goods to around 30% and reduced British duties on French wines and brandy. During the next decade the value of British exports to France more than doubled whilst French wine imports increased by 100%.

Richard Cobden (1804 – 1865) had founded the Anti-Corn Law league in 1838. That the current TPP has taken just five years is therefore encouraging. Cobden is a giant in the annals of free-trade, to find out more about this extraordinary man and the relevance of his ideas today please visit The Cobden Centre. A recent post – No more “Free-Trade” treaties: it’s time for genuine free trade – is an excellent example of their important work:-

Murray Rothbard opposed NAFTA and showed that what the Orwellians were calling a “free trade” agreement was in reality a means to cartelize and increase government control over the economy. Several clues lead us to the conclusion that protectionist policies often hide behind free trade agreements, for as Rothbard said, “genuine free trade doesn’t require a treaty.”

The Cobden-Chevalier Treaty spawned a cascade of bilateral FTAs across Europe. By some estimates these agreements reduced tariffs in Europe by 50%. Sadly as the world economy entered a recession in 1873 the enthusiasm for free trade began to wane. The First World War saw the situation deteriorate further, whilst the great depression of the 1930’s heralded an increase in nationalism which went hand in hand with protectionism.

According to the World Trade Organisation (WTO) – established in 1995 in the wake of the NAFTA agreement of 1994 – the General Agreement on Tariffs and Trade (GATT) of 1947 was the starting point for multilateral FTAs, although it was originally agreed between just 23 countries. This followed in the wake of the 1944 Bretton Woods Agreement which had established the IMF, World Bank and Bank for Reconstruction and Development. By 1951 the European Coal and Steel Community had been founded – later to become the EEC (1957).

Many other bilateral and multilateral agreements followed. For a more detailed investigation of the history of free trade, this WTO – Historical background and current trends 2011 – article is worth investigating. One point the WTO make in conclusion is:-

…despite the explosion of PTAs in recent years, 84 per cent of world merchandise trade still takes place on an MFN (Most Favoured Nation) basis (70 per cent if intra-EU trade is included).

Viewed from this perspective, the ideal of “Free Trade” still has far to go.

Other perspectives on the TPP

In this recent article Bruegal – Trans-Pacific Partnership: Should the key losers – China and Europe – join forces? the authors anticipate a Chinese response which could benefit the EU-

The winners are obvious: Obama and Shinzo Abe, arguably also the US and Japanese economies. Obama can leave office with a strong demonstration of the US pivot to Asia, and Abe can finally argue that the third arrow of his Abenomics program is not empty.

The losers are also obvious: China and Europe. China not only has been left out of the deal, but it has been left out on purpose. If anybody had any doubt (at some point China was invited into the negotiations and some still expect China to continue discussing membership in the future), Obama’s official statement on TPP yesterday makes it very clear: “when more than 95 percent of our potential customers live outside our borders, we can’t let countries like China write the rules of the global economy”. For China the issue is not only losing access to the US market but also the fact that its most important trading partners are in the deal, with the notable exception of Europe.

The fact that TPP has not yet being ratified by national parliaments still offers room for doubt as to TPP’s actual economic significance (exemptions from its coverage could spring out in every jurisdiction) but there is no doubt that it will be economically relevant. TPP covers 40 per cent of global trade and spans 800 million people. Not only will trade barriers be reduced to the minimum in virtually every sector (including generally protected ones such as agriculture) but also common standards will need to be used by all participants, be it for investment, environment or labour. In this regard, the primacy of the protection of brand names over the protection of geographical indications of agricultural products, or the priority of the protection of trade secrets over press freedom are cornerstones of the US success in its negotiations with TPP partners, which also shows the price that a country like Japan are willing to pay for US-led security. In the same vein, the high price to pay (in terms of US supremacy on the negotiation table) makes it all the more unlikely for China to seriously consider joining the bloc in the near future: the treatment of state-owned enterprises and data protection are two stumbling blocks. The latter is also a key deterrent for Europe’s TTIP negotiations.

They see a window of opportunity to the EU to negotiate a deal with China.

From a geo-political standpoint Chatham House – For the West, the Trans-Pacific Partnership Must Not Falter – see the TPP providing benefits which go well beyond economics:-

But the economic benefits are only one upside of the deal. While it is by no means assured, there could also be a significant geostrategic impact. The TPP was not the only Asian trade agreement of choice. China, for example, had been supporting an alternative Regional Comprehensive Economic Partnership. But the 12 TPP participants – the US, Australia, Brunei, Canada, Chile, Japan, Malaysia, Mexico, New Zealand, Peru, Singapore and Vietnam – sent a clear message regarding the kind of standards and rules they believe are best placed to provide the greatest benefit to their populations – from greater transparency and anticorruption to more free and open markets.

Western leadership

The TPP now sets the bar. If successful, in time other states will hopefully join including, most significantly, India, China and South Korea. But this will take time and the TPP has to prove itself first. Prospective member states will have to make extremely tough political choices in order to join and they and their populations will need to see meaningful tangible benefits first. But the door has been left open and if the TPP turns out to realize some of its potential, others could come knocking on the door.

This podcast from CFR – Trans-Pacific Partnership Trade Deal – gives a good global overview from both an economic and political perspective:-

…If you look at the U.S. negotiations with Europe—the Transatlantic Trade and Investment Partnership—if those come to fruition—and they’re on a somewhat slower track—you’re going to reach a position for the United States where two-thirds of its trade is covered under free trade arrangements of some sort of another.

…you’ve had a stalemate in the Doha Round for more than a decade now between the advanced economies—primarily the United States, Europe, Japan to some extent—and the big emerging economies—China, India, and Brazil. And they’re just at loggerheads over a whole series of issues, from, you know, farm subsidies in the U.S. and Europe to the pace of opening up manufacturing markets in the developing countries.

…The Europeans are always very conscious about not losing their relative trade advantages, and the possibility of Japan, and then if Korea docks on to the TPP as well—the possibility of those countries having better access to the U.S. market than European companies would enjoy, I think that will be a spur to action at the—at the U.N.

…Peterson Institute, for example, thinks that Japan is going to gain upwards of $119 billion in absolute gains from TPP.

…TPP is an instrument of Abenomics, the broader structural reorganization inside Japan, and it leverages for Abe all kinds of transformations that would be difficult to accomplish by a Japanese government on its own.

…There’s some loud minority voices of criticism. But overall, the opinion polling in Japan has really embraced this notion of TPP participation.

…The LDP has long been the protector and party that has advocated on behalf of Japan’s farmers. It is now leading this agricultural reform, largely because Japan’s farmers are aging. They’re getting older. And there’s a demand from within the agricultural sector for these reforms and a more competitive-oriented agricultural policy.

Nonetheless, in some parts of Japan Abe’s party still is seen as betraying some of the core interests of its postwar conservative protections, and so he’ll have to tread a little bit carefully to make sure that he can pay off or make sure that the farmers will not be mistreated.

…Initially the rhetoric out of the Chinese government was reasonably hostile to TPP. That has softened in recent months. But clearly, to make the sorts of reforms that would be necessary to join the TPP would be a very big lift for China.

…if Congress rejects the TPP, that’s a slap in the face to 11 other countries, including close allies like Mexico, Canada, Japan, Australia, and New Zealand that have made difficult decisions domestically in order to be able to conclude the deal. So the thinking has always been, at the end of the day, Congress is going to be very reluctant to do that.

Countering the enthusiasm of Chatham House, The Diplomat – Could the TPP Actually Divide Asia? – cautions that there are geopolitical risks that the TPP will increase tensions in the region.

Firstly, South Korea:-

U.S.-Korea free trade agreement (KORUS) came into effect in March 2012. South Korea is undoubtedly a strong candidate to join the group, given that KORUS is seen as a gold standard for free trade deals. Nevertheless, the U.S.-Korea free trade pact largely exempted the politically sensitive Korean rice market. That alone will undoubtedly be a major political issue for all member countries should Korea negotiate entry into the pact, and it will certainly be a source of contention with Japan, a founding member of the TPP that was forced to make concessions on its equally politically sensitive rice market.

Then, Taiwan:-

The Taiwanese government has made clear that it hopes to be one of the first entrants to the TPP, not only to further its position as a global exporter, but also to encourage domestic reform that is critical if Taiwan is to remain competitive. Given its experience in joining the World Trade Organization, whereby it had to wait until China was ready for accession in 2001 so that it could join at the same time, there is growing concern that Taipei would have to wait again for Beijing to be ready. The frustration of being unable to join a group that is seen as key to Taiwan’s growth will undoubtedly strain cross-Strait relations.

And finally, the undermining of existing agreements:-

The Regional Comprehensive Economic Partnership (RCEP) includes not only all 10 ASEAN countries, but also China, Japan, South Korea, India, Australia, and New Zealand. Critics of the RCEP have been quick to dismiss the pact as aiming at lower standards compared to the TPP, and as focused too heavily on relatively unambitious tariff barrier reductions. Moreover, it is seen as a Chinese-led initiative that does not include the United States. Yet the fact that RCEP brings hitherto unlikely partners such as Burma and Cambodia into the fold of regional trade agreements in itself should be heralded as a significant development that has already achieved what is one of the major longer-term goals of TPP, namely to encourage nations to adopt internationally developed rules and standards.

To round off the arguments for and against here is Mish Shedlock – Hillary Clinton, Dead Rats, Toilet Paper Politics – he’s definitively unimpressed:-

Every country is a firm believer in free trade for exports, but no country wants free trade for imports. Obviously, that cannot work mathematically, which is precisely why the deal had to be negotiated in secret and has taken five years to produce questionable results. …The New York Times reports “Trans-Pacific Partnership Seen as Door for Foreign Suits Against U.S.“. WikiLeaks analysis explains that this lets firms “sue” governments to obtain taxpayer compensation for loss of “expected future profits.” This agreement is a lawyer’s fantasyland dream come true. Corporations will be suing governments left and right over “expected future profits.” For example, Australia would not sign the deal unless it obtained a waiver for health warnings on cigarette packages that are more stringent than elsewhere. Apparently, all other lawsuits are fair game. And it will be taxpayers who pay the bill. Imagine the lawsuits over GMOs (genetically modified organisms). Monsanto will be suing every country that blocks its GMO products.

…I propose TPP will create a nightmare of worldwide lawsuits at taxpayer expense, while doing nothing that will genuinely advance free trade. Mish Free Trade Proposal As I have stated numerous times, I am in favor of free trade. An excellent free trade agreement would consist of precisely one line of text: “All tariffs and all government subsidies on all goods and services will be eliminated effective immediately”. I maintain that the first country that does that will be the beneficiary, regardless of what any other country does!

Conclusions and investment opportunities

The TPP has 30 chapters to be analysed. It will probably under-deliver as Shedlock indicates, however, perception that large scale, multilateral free-trade negotiation is back on the agenda, after such a long absence – NAFTA was back in 1994 – is likely to be supportive for markets

Country level benefit to financial markets

- Japan will benefit from the external assistance it lends to the policies of Abenomics. Japanese agriculture will be negatively affected but internal subsidies will mitigate its impact. The TPP should have a strong positive influence on the Nikkei. This will help support JGB yields but is unlikely to cause a significant increase in the JPY if the BoJ continues with its QQE policy..

- Singapore should benefit, providing goods and services to its Asian neighbours. The Straits Times Index should be supported and the SGD is likely to appreciate.

Sectoral stock market effects

- US, Canadian, Australian and New Zealand agricultural businesses should reap significant benefits over time – especially Australian sugar refineries – whilst agro-business in Japan will be impaired.

- Vietnam’s apparel manufactures should have improved terms of trade, as will Malaysian Palm Oil producers.

- Companies in the Japanese and US auto-industry will benefit.

- US pharmaceutical companies will benefit.

- IT companies, especially from the US but also Japan, will benefit.

In the long run, other countries, including South Korea, Taiwan and perhaps even China, may join the TPP. Uncertainty still revolves around final approval of the treaty by the US, but, as more information begins to emerge, investment flows will start to influence equity prices across certain sectors and, more broadly, on a country specific basis.