Macro Letter – No 19 – 12-09-2014

German growth prospects – the ECB and Russian gas

- The ECB cut rates and implemented the first phase of OMT

- Russia continues to retaliate against European sanctions

- European Natural Gas prices have risen but shortages seem unlikely

Last week I started researching the risks to German growth of a gas embargo by Russia. This could become a reality if the geo-political situation in the Ukraine should deteriorate further. Before I could put pen to paper, ECB Governor Mario Draghi had implemented a pre-emptive strike; cutting the repo rate to 0.05% and announcing the ECBs intention to embark on outright monetary transactions (OMT) initially in the asset backed securities (ABS) market. The ECB – Statement – provides fuller details. It’s still a little light on content but JP Morgan estimates that the ECB will purchase Eur 47bln of newly issued ABS securities over a three year period.

Whilst these measures stopped short of purchasing Eurozone (EZ) sovereign bonds, European government bond markets reacted favourably. French T-Bill rates turned negative, so too did the yield on 2 year Irish Gilts. The Spanish, not to be outdone, issued 50 year Bonos at a yield of 4%.

Here is a table of some European short term rates from Monday 8th September: –

| Security | Yield | Spread vs Germany | Inflation | Real Yield |

| Austria 1Y | -0.032 | 0.027 | 1.8 | -1.832 |

| Belgium 3M | -0.05 | 0.029 | 0 | -0.05 |

| Belgium 6M | -0.025 | 0.038 | 0 | -0.025 |

| Belgium 1Y | -0.043 | 0.016 | 0 | -0.043 |

| Bulgaria 1Y | 1 | 1.059 | -1 | 2 |

| Croatia 6M | 0.95 | 1.013 | -0.1 | 1.05 |

| Croatia 9M | 1.15 | 1.218 | -0.1 | 1.25 |

| Croatia 1Y | 1.38 | 1.439 | -0.1 | 1.48 |

| Czech Republic 3M | 0.01 | 0.089 | 0.5 | -0.49 |

| Czech Republic 6M | 0.03 | 0.093 | 0.5 | -0.47 |

| Czech Republic 1Y | 0.11 | 0.169 | 0.5 | -0.39 |

| Denmark 3M | -0.06 | 0.019 | 0.8 | -0.86 |

| Denmark 6M | -0.01 | 0.053 | 0.8 | -0.81 |

| Denmark 1Y | 0.15 | 0.209 | 0.8 | -0.65 |

| France 3M | -0.027 | 0.052 | 0.5 | -0.527 |

| France 6M | -0.03 | 0.033 | 0.5 | -0.53 |

| France 9M | -0.011 | 0.057 | 0.5 | -0.511 |

| France 1Y | -0.029 | 0.03 | 0.5 | -0.529 |

| Germany 3M | -0.079 | 0 | 0.8 | -0.879 |

| Germany 6M | -0.063 | 0 | 0.8 | -0.863 |

| Germany 9M | -0.068 | 0 | 0.8 | -0.868 |

| Germany 1Y | -0.059 | 0 | 0.8 | -0.859 |

| Greece 3M | 1.47 | 1.549 | -0.7 | 2.17 |

| Greece 6M | 1.86 | 1.923 | -0.7 | 2.56 |

| Hungary 3M | 1.52 | 1.599 | 0.1 | 1.42 |

| Hungary 6M | 1.55 | 1.613 | 0.1 | 1.45 |

| Hungary 1Y | 1.84 | 1.899 | 0.1 | 1.74 |

| Ireland 1Y | 0.08 | 0.139 | 0.3 | -0.22 |

| Italy 3M | 0.083 | 0.162 | -0.1 | 0.183 |

| Italy 6M | 0.144 | 0.207 | -0.1 | 0.244 |

| Italy 9M | 0.193 | 0.261 | -0.1 | 0.293 |

| Italy 1Y | 0.217 | 0.276 | -0.1 | 0.317 |

| Latvia 3M | 0.2 | 0.279 | 0.8 | -0.6 |

| Latvia 6M | 0.374 | 0.437 | 0.8 | -0.426 |

| Latvia 1Y | 0.258 | 0.317 | 0.8 | -0.542 |

| Lithuania 6M | 0.3 | 0.363 | 0.2 | 0.1 |

| Lithuania 1Y | 0.4 | 0.459 | 0.2 | 0.2 |

| Netherlands 3M | -0.072 | 0.007 | 1 | -1.072 |

| Netherlands 6M | -0.092 | -0.029 | 1 | -1.092 |

| Norway 3M | 1.259 | 1.338 | 2.2 | -0.941 |

| Norway 6M | 1.118 | 1.181 | 2.2 | -1.082 |

| Norway 9M | 1.248 | 1.316 | 2.2 | -0.952 |

| Norway 1Y | 1.276 | 1.335 | 2.2 | -0.924 |

| Poland 3M | 2.65 | 2.729 | -0.2 | 2.85 |

| Poland 1Y | 2.044 | 2.103 | -0.2 | 2.244 |

| Portugal 6M | 0.15 | 0.229 | -0.9 | 1.05 |

| Romania 6M | 2.289 | 2.352 | 1 | 1.289 |

| Romania 1Y | 2.25 | 2.309 | 1 | 1.25 |

| Spain 3M | 0.058 | 0.137 | -0.5 | 0.558 |

| Spain 6M | 0.072 | 0.135 | -0.5 | 0.572 |

| Spain 1Y | 0.153 | 0.212 | -0.5 | 0.653 |

| Sweden 3M | 0.211 | 0.29 | 0 | 0.211 |

| Sweden 6M | 0.202 | 0.265 | 0 | 0.202 |

| Switzerland 3M | -0.11 | -0.031 | 0.1 | -0.21 |

| Switzerland 6M | -0.05 | 0.013 | 0.1 | -0.15 |

| Switzerland 1Y | 0.05 | 0.109 | 0.1 | -0.05 |

| UK 3M Yield | 0.43 | 0.509 | 1.6 | -1.17 |

| UK 6M Yield | 0.546 | 0.609 | 1.6 | -1.054 |

| UK 1Y Yield | 0.509 | 0.568 | 1.6 | -1.091 |

Source: Investing.com and Trading Economics

I have omitted Finland since I was unable to locate prices for shorter maturity than 2 year. Two year Finnish bonds yield -0.026% and inflation is running at +0.8%.

Europe and its periphery are benefitting from low or negative real interest rates. Even this seems insufficient to stimulate robust, sustainable growth.

The Economic Cost of Geo-politics

When I last wrote about the Ukraine earlier this year, I concluded: –

I believe the Ukrainian situation may reduce the likelihood of a rapid increase in tapering by the Fed and increase the prospects for ECB Outright Monetary Transactions. In aggregate that amounts to more QE which should support stocks and higher yielding bonds.

To date, the economic impact on Europe has been limited. The fed have continued to taper in the face of a robust recovery from weak US Q1 GDP data. The EZ, however, has struggled to follow the US lead and the ECB has been forced to act repeatedly to avert further disinflation.

As we head into the winter, it seems an appropriate time to review European Natural Gas, in light of the escalation of tension between Russia and NATO. This is especially pertinent to Germany where, along with its north European neighbours, winter Natural Gas demand is three times greater than during the summer.

This week has seen an escalation of European sanctions against Russia. The European Commission (EC) has curtailed the ability of three of the largest Russian Oil companies to raise capital beyond a one month maturity. Since around half of all longer term gas contracts are priced in relation to the oil price this seems a strange way to avoid disrupting the European gas price. The Russian’s have responded by threatening to ban aircraft access to Russian airspace and, more significantly, to disrupt gas supplies. The Financial Times – Russia aims to choke off gas re-exports to Ukraine picks up on this theme: –

In an effort to offset lost volumes from Russia, Ukraine has sought to secure more gas from the EU, principally through “reverse flows” – re-exports of Russian gas via countries such as Poland, Hungary and Slovakia. But Gazprom, Russia’s state gas company, has long complained about the re-exports, with Alexei Miller, its chief executive, denouncing them as a “semi-fraudulent mechanism”. Senior officials in the European Commission and in eastern European governments say Russia has been raising the prospect of reducing export volumes so their customers have no gas left over for reverse flows to Ukraine. “They say this pretty openly,” said one central European ambassador.

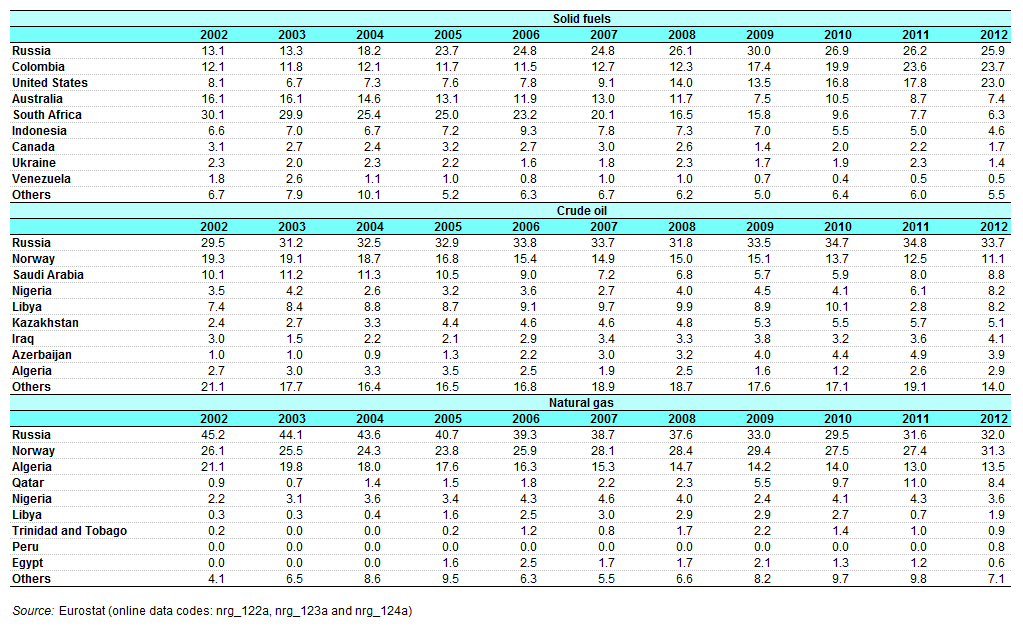

To understand the importance of Russian energy exports to Europe the following table is a useful guide: –

Source: Eurostat

An insight into EU energy policy is provided by the European Commission – Energy Economic Developments in Europe – published in Q1 2014. The section on Natural Gas starts at Page 33:-

In the European Union the majority of natural gas is supplied through bilateral long-term contracts which are negotiated between two parties, importer and exporter, and traditionally indexed to the price of oil. Currently, half of natural gas supply in the EU is still indexed to oil while across the EU a wide variation in import prices of piped gas and LNG has been observed. This is remarkable as at the same time a growing share of gas is traded on spot markets where short-term contracts are concluded on the basis of the market price determined by actual demand and supply. Spot market prices in the EU have been constantly lower than long-term contracts’ prices, at least since 2005.

… In both the US and in the EU, spot-market gas prices have progressed in a similar fashion over the past decade and have followed the movements in the oil price.

In 2005, however, these gas prices have started to clearly fall below the level of the oil price. Between 2008 and 2009 they fell significantly in both regions, likely as a consequence of declining demand due to the economic downturn.

The fall in energy consumption has led to an excess supply of gas on the gas markets around the world and both US and the UK spot markets temporarily converged, trading at around 4/5 USD/MBtu in mid-2009, while the German hub prices fell less evidently, trading still above 8 USD/MBtu in 2009. From 2007 onwards, the US gas spot price has fallen under the price level of the other gas spot markets, which most likely reflects the effect of the surge in domestic shale gas supply. This becomes quite clear after 2009, when energy consumption picked up again following the recovery of the economy. Statistics from more recent years show that while the US spot prices remained low (around 4 USD/Btu in 2011), the EU spot prices (both in the UK and German hub) kept increasing. Wholesale gas prices have continued to rise in the EU while economic activity contracted and consequently natural gas consumption in the EU has been declining: the first half of 2012 represented the EU’s lowest first half year consumption of the last ten years. It was 7% and 14% less than the first half of 2011 and 2010 respectively.

The continued rise in EU wholesale gas prices despite the slump in gas demand and the lower gas spot prices vividly depicts the kind of vulnerability the EU is exposed to due to its high import dependency: as the Asian markets offer higher returns and more robust demand, gas producing countries have increased their trade with Asia lowering supply to Europe. As a consequence wholesale gas prices in Europe have increased while in the US, which now can rely more heavily on domestic production, prices have remained low. US prices were shielded from potential upwards pressure from export demand because of export restrictions (generally expected to be gradually lifted). Furthermore, the impacts on the EU have been further aggravated in this context due to the oil-price indexation of many long-term gas import contracts.

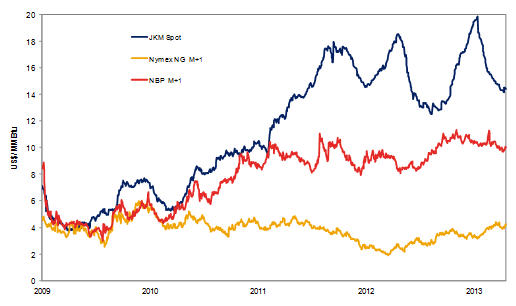

This chart from Schneider Electric shows the divergence in gas prices between US (yellow) EU (red) and Asia (blue): –

Source: Schneider-Electric

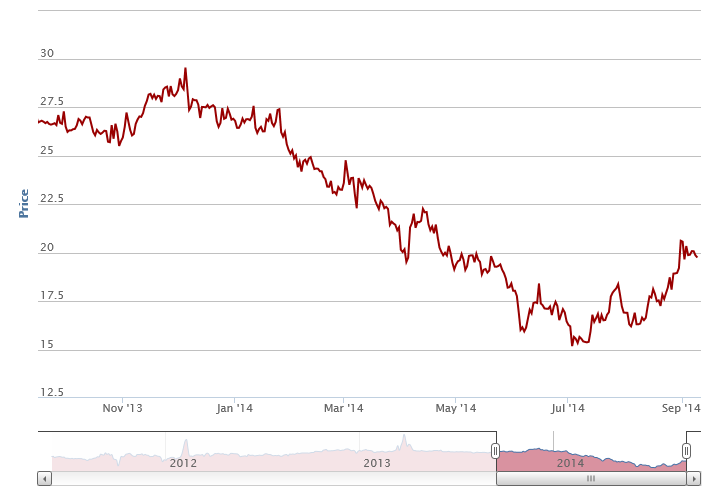

European Natural Gas prices are down from their December 2013 highs but have recently started to recover from the July 2014 lows. The chart below is for Dutch TTF (Title Transfer Facility) Gas: –

Source: EEX

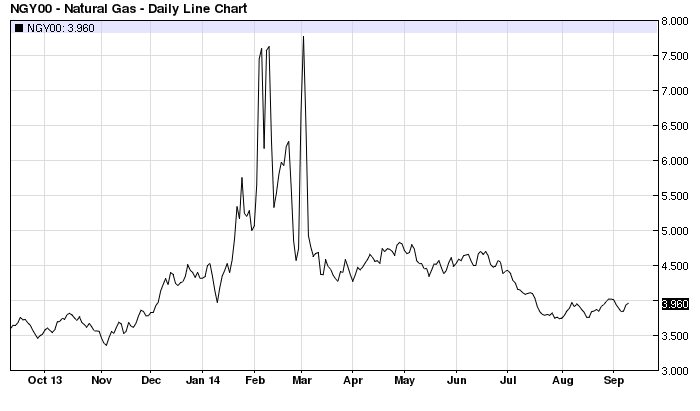

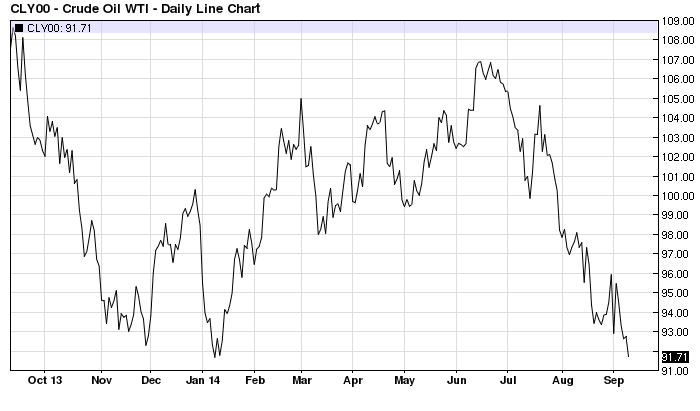

By way of comparison here are the one year charts for US Natural Gas and West Texas Intermediate Crude Oil: –

Source: Barchart.com

Understandably, the US Natural gas market is less concerned about Russian sanctions, and also cognisant of the long lead time between receiving an export license and the US capacity to increase exports of LNG.

Source: Barchart.com

The US Crude Oil market is seemingly unperturbed by the politics of Russia or the Middle East. Or, perhaps, it is the combination of continuous improvements in US supply coupled with rising concern about the slowing of China. A similar pattern is evident in the Brent Crude price.

Returning to Europe: establishing a generic price for European Natural Gas is difficult as this article from Natural Gas Europe – European Natural Gas: So What’s the Real Price? explains. It is also worth noting the seasonality in gas prices. The last major spikes occurred in February/March 2013 and January/February 2012, coinciding with the advent of cold European winter weather.

The EU Commission and national governments are taking no chances this year, as this article from Reuters – Europe drafts emergency energy plan with eye on Russia gas shut-down makes plain:-

A source at the EU Commission said it was considering a ban on the practise of re-selling to bolster reserves.

“In the short-term, we are very worried about winter supplies in southeast Europe,” said the source, who has direct knowledge of the Commission’s energy emergency plans.

“Our best hope in case of a cut is emergency measure 994/2010 which could prevent LNG from leaving Europe as well as limit industrial gas use in order to protect households,” the source said.

European Union Regulation number 994/2010, passed in 2010 to safeguard gas supplies, could include banning gas companies from selling LNG tankers outside of Europe, keeping more gas in reserve, and ordering industry to stop using gas.

The Russian threat to reduce gas supplies to the EU in order to reduce the re-sale of gas to other countries seems rather hollow when the EC would appear to be preparing to take these steps anyway. Nonetheless, if Russia reduces supply what can the EU importing countries do?

Norway is not in a position to make up the shortfall. 96% of Norwegian gas is already exported. At the Flame gas conference in Amsterdam this May, Statoil spokesman Rune Bjornson told delegates, “I think many producers, including us, can adjust on the margins, but most of the production capacity from Norway is typically designed to produce at maximum in winter and that is what we’ll do.”

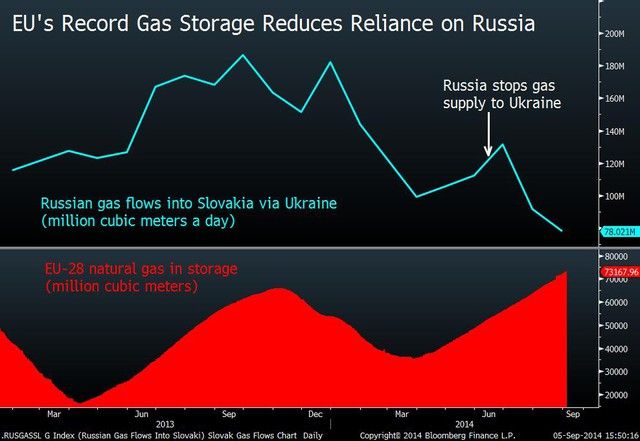

European governments have, however, been actively improving storage capabilities. This process has been on-going since the first Russian/Ukrainian dispute in 2006 – according to recent estimates EU-28 storage is at 90% of capacity which is around 74 bcm. Businessweek – EU Need for Russian Gas Via Ukraine Wanes as Stores Fill – gives a good overview: –

Source: Bloomberg

Europe’s reliance on Russian natural gas shipments via Ukraine is declining after the region pumped a record volume of the fuel into underground inventories, minimizing the risk of shortages during the coming winter.

Given that Geo-politics seems to have had little impact on the performance of world financial markets in the long run should we be worried in the short run and especially with respect to Germany this winter?

The Council for Foreign Relations – The Geopolitical Paradox: Dangerous World, Resilient Markets – opines on this subject this week. The article is concerned mainly about disruption to the oil market: –

It is often noted that the vast majority of postwar recessions have been associated with energy shocks. Rising turbulence in the Middle East has raised the prospect of a long-term disruption in the region, where national borders could be rewritten through violent upheavals. The threat of a Russian cutoff of gas to Europe also hangs over markets. Consequently, it is surprising that energy markets, and oil markets in particular, do not ask for a premium in futures markets for secure energy supplies. At present, current oil contracts are higher than longer-term futures contracts, and though there are technical reasons for this downward trend (“backwardation”), it hardly is suggestive of disrupted or anxious markets.

They go on to discuss Europe describing it as the weak link: –

There are a number of reasons why Europe is the channel through which political risk could reverberate in the global economy. Europe is most vulnerable to disruptions in trade and financial relationships with Russia, though I have argued elsewhere that these costs may be small relative to the costs of inaction. Weak growth in China and elsewhere in the emerging world could significantly affect exports, particularly in Germany. Significantly, though, Europe also faces these challenges at a time of economic stress and limited resilience. Growth in the region has disappointed and leading indicators have tilted downward. Further, concern about deflation is beginning to weigh on sentiment and investment. The persistence of low inflation—well below the ECB’s goal of around 2 percent—is symptomatic of deeper structural problems facing the eurozone, including an incomplete monetary union, deep-seated competitiveness problems in the periphery, and devastatingly high unemployment. Homegrown political risks also threaten to add to the turmoil, as rising discontent within Europe over the costs of austerity is undermining governing parties and fueling populism. The result is a monetary union with little capacity or resilience to defend against shocks. The ECB has responded to these risks with interest-rate cuts and asset purchases, and is expected to move to quantitative easing later this year or early next, but the move comes late, and is unlikely to do more than address the headwinds associated with the ongoing banking reform and continued fiscal austerity. Overall, a return to crisis is an increasing concern and political risks could be the trigger.

The limited impact on financial markets since the beginning of the Ukrainian crisis in February can be seen in the table below: –

| Market/Security | Price 28 Feb | Price 9 Sept | Change | % Change |

| TTF Gas | 22.85 | 19.78 | -3.07 | -13.44 |

| GPL Gas | 23.23 | 20.06 | -3.17 | -13.65 |

| US Nat Gas | 4.74 | 3.96 | -0.78 | -16.46 |

| WTI | 102.58 | 91.71 | -10.87 | -10.60 |

| E.ON | 13.82 | 14.31 | 0.49 | 3.55 |

| RWE | 29.02 | 31.43 | 2.41 | 8.30 |

| DAX | 9692 | 9700 | 8 | 0.08 |

| S&P500 | 1859.45 | 1995.69 | 136.24 | 7.33 |

| 10yr Bund yield | 1.63 | 1 | -0.63 | -38.65 |

| Gold | 1327.6 | 1249.4 | -78.2 | -5.89 |

Source: EEX and Investing.com

Germany – the weakest link?

Since the Hartz reforms of 2002 Germany has emerged from the strain of unification to re-establish its credentials as the powerhouse of European growth. Latterly – and especially since 2008 – its preeminent reputation has become tarnished. The Bundesbank raised its growth forecast in June to 1.9% for 2014 vs its December 2013 forecast of 1.7%. Their optimism has been dented since then by concerns about the politics of Eastern Europe. The Deutsche Bundesbank – August 2014 Monthly Report makes the following observations: –

The global economy appears to have got off to a good start in the second half of the year. As regards the industrial countries, Japan’s economy is expected to rebound in the third quarter. The US economy is likely to remain on a growth path, although it will probably be impossible to maintain the rapid pace of growth attained in the second quarter of the year. Following second- quarter stagnation, the euro area is looking at a resumption of positive economic growth, albeit not at the pace predicted by many analysts in the spring. The underlying cyclical trend in some euro- area countries is turning out to be weaker than expected. At the same time, the geopolitical tensions in Eastern Europe owing to the Ukraine conflict as well as in other parts of the world are now appearing to weigh more heavily on corporate sentiment. Although they will only affect a small percentage of EU exports directly, the recently enacted EU sanctions and the Russian response are likely to dampen sentiment.

The Bundesbank are still predicting an increase in GDP growth for 2015 before moderating once more in 2016. Below is a chart of annual GDP since 2002: –

Source: Trading Economics

The momentum seems to be dissipating. According to the Federal Statistics Office, in 2013, 69% of Germany’s exports were to other EU countries. Asia came second with 16% and the USA third with 12% – a slow down in Asia, specifically China, would be problematic, but the UK, US and peripheral EZ countries might be able to absorb the slack. What is clear, however, is that Germany is vulnerable.

This brings me to the risks to Germany this winter due to rising Natural Gas prices and a curtailment of supply. The IEA – Germany Oil and Gas Security Report 2012 provides a comprehensive overview of the German market: –

Germany has very little domestic oil and natural gas production and relies heavily on imports. It has well diversified and flexible oil and natural gas supply infrastructure, which consists of crude, product and gas pipelines and crude and oil product import terminals. Natural gas is imported into Germany exclusively by cross-border pipeline. The country has no LNG infrastructure, although some German companies have booked capacities in overseas LNG terminals.

Oil continues to be the main source of energy in Germany although it has declined markedly since the early 1970s. It now represents approximately 32% of Germany’s total primary energy supply (TPES).

Natural gas consumption in Germany has declined 10% since 2006. Demand was 90 bcm in 2010, down from 100 bcm in 2005. According to government commissioned analysis, the total consumption of natural gas in Germany is expected to continue to decline over the long term. The share of natural gas in Germany’s TPES is currently around 22%.

The decline in Natural Gas demand is evident across Europe. Earlier this year the Oxford Institute for Energy Studies estimated that, across 35 European countries, demand had fallen from 594 bcm in 2008 to 528 bcm in 2013 – an 11% decline. This is largely due to the high price of Natural Gas relative to Coal and the Europe-wide policies mandating increases in renewable energy production. For those who want to read more about EU renewable energy developments, Bruegal – Elements of Europe’s energy union , published this week, looks at the policy challenges facing Europe between now and 2030.

Germany’s declining demand for Natural Gas and increase in storage capacity will mitigate some of the potential disruption to supply – in 2012 Natural Gas represented 22% of supply vs Oil 32% and Coal 24%. Added to which Germany has adopted some of the most aggressive policies to develop renewable energy, offset, to some extent, by their closure of Nuclear Power plants: –

Under existing government policies the trend towards an increasing share of renewables looks set to continue. The Energy Concept 2010 established a goal for Germany to increase its share of electricity generated from renewable sources to at least 35% of total consumption by 2020. Conversely, the trend towards an increasing share of nuclear in the energy mix looks set to reverse following the government announcement in 2011 of its decision to phase out all German nuclear power plants by the end of 2022.

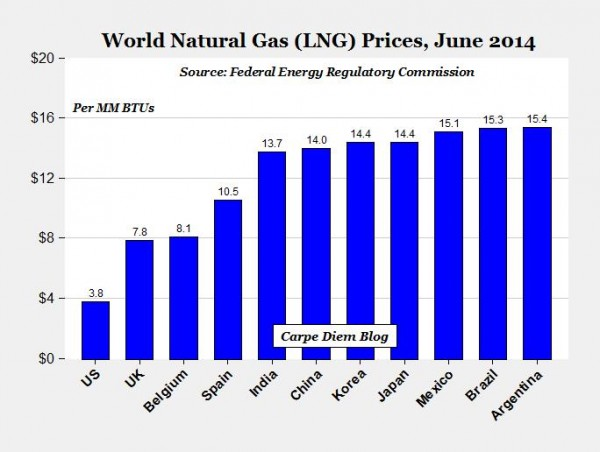

Germany imports Natural Gas primarily from Russia (39%) followed by Norway (35%) and the Netherlands (22%). Germany has no Liquefied Natural Gas (LNG) capacity but the GATE (Gas Access To Europe) terminal in Rotterdam – opened in 2011 – was operating at 10% of capacity in April 2014 and is purported to be capable of supplying 12 bcm (Billion Cubic Metres). This is still a drop in the ocean – Russia supplied Germany with 140 bcm last year. German domestic demand is less than 100 bcm leaving a substantial amount for re-export. Further LNG supply is available from Spain but there are bottlenecks with the trans-Pyrenean pipeline. In any case, Spanish LNG prices are high. The table below shows the divergence in prices for LNG globally, even more than in pipeline supply LNG prices are a function of logistical supply constraints: –

Source: FERC and AEI

Germany’s Natural Gas storage capacity (2012) is 20.8 bcm, making it the highest in Europe, although there are plans to increase this further. In H1 2013 German Natural Gas consumption was 50 bcm – the high levels of storage suggest that Germany is well placed to weather a Russian go-slow this winter.

The complex and diverse nature of Germany’s cross-border pipeline capabilities are shown in the map below, however the largest pipelines by potential capacity are (2012 data): –

| Country | Pipeline | Capacity |

| Ukraine | Bratstvo | 120 bcm |

| Norway | Norpipe, Europipe I and II | 54 bcm |

| Russia | Yamal | 33 bcm |

| Russia | Nord Stream | 27 bcm |

Source : IEA

Source: IEA

Conclusions and financial market implications

After two interruptions to Russian Natural Gas supply in less than a decade, Germany – along with other gas importing countries within the EZ have taken precaution. The most vulnerable countries in the event of a complete cessation of gas supply by Russia are probably the Baltic States, Hungary and Bulgaria. However, Russia is also very dependant on the EU for sales of Gas, Oil and Coal. Nearly 60% of state revenue comes from this trade. This trade is worth $80bln per annum to Gazprom alone. Germany is Russia’s third largest trading partner, whilst Russia ranks 11th on Germany’s list.

If Russian sanctions lead to a cessation of Gas exports then a number of large German utility companies will suffer – most notably E.ON and RWE. However it is most unlikely that German supply will run out. Price increases will either be passed on through higher prices or lead of margin compression due to the disinflationary forces emanating from elsewhere in the economy.

John W Snow – the US Secretary to the Treasury under George W Bush – is quoted as saying, “Higher energy prices act like a tax. They reduce the disposable income people have available for other things after they’ve paid their energy bills.” This is the potential that a reduction in Russian gas supplies and commensurate rise in prices is likely to have on the wider German economy. The ECB has cut rates and started down the road to QE even before the onset of winter. Mario Draghi knows that monetary policy works slowly and many commentators believe the ECB are demonstrably behind the curve due to their attempts to impose austerity on the more profligate member states.

German Bunds may have hit their high for this year, especially since the ECB are now buying ABS, but they remain a “hedge short” at best. The quest for yield hasn’t gone away, EZ high yielding sovereign names will be supported still.

European Equities will be nervous in this environment despite some 52% of Eurostoxx 600 companies beating their earning forecasts for Q2, according to Reuters data. After a summer shakeout, the DAX has regained its composure, but it is already trading on a P/E ratio of nearly 22. Technically it’s a “Hold” until a break of 9,000 on the downside or 10,000 on the upside. But don’t forget that when Mr Draghi uttered, “whatever it takes” the DAX was toying with 5,000

European Natural Gas prices should be supported through the winter but a full-blown “Gas Crisis” is unlikely. A “Winter Squeeze” such as 2012 or 2013 could see spot prices double under normal market conditions. German growth will continue to be hampered by political uncertainty but, all other things equal, it should rebound on any sign of detente and will benefit from the continued recovery of the UK and US economies.