Macro Letter – No 24 – 21-11-2014

Oil and Growth

- The oil price has fallen by 30% since the summer

- Global inflation expectations are starting to be revised downwards accordingly

- Global growth, led by energy importers will be revised higher

The Oil Price

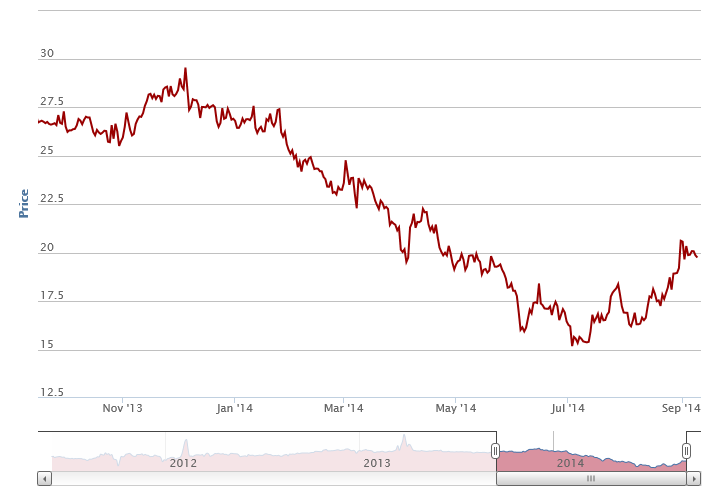

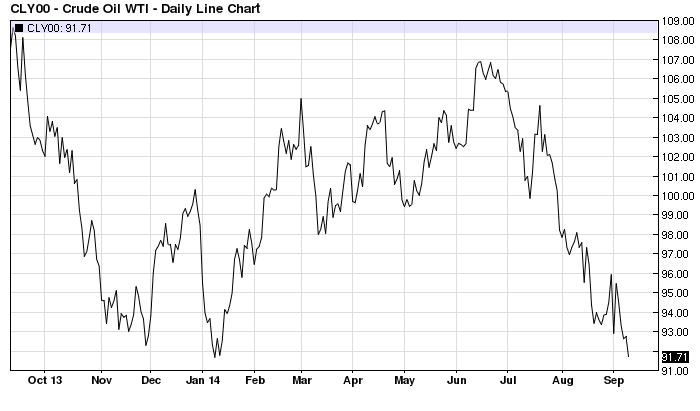

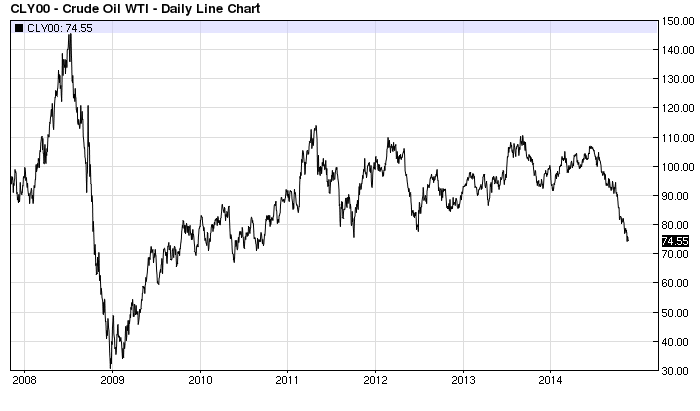

Since the summer crude oil prices have fallen sharply from above US$105 to below US$75/barrel. This price move has led to discussion of lower demand stemming from a slow-down in global economic activity. Whilst I expect a benign influence on inflation I am not convinced that the price decline is due to a reduction in global demand. Here is a daily chart for Spot West Texas Intermediate crude oil (WTI) since November 2007:-

Source: Barchart.com

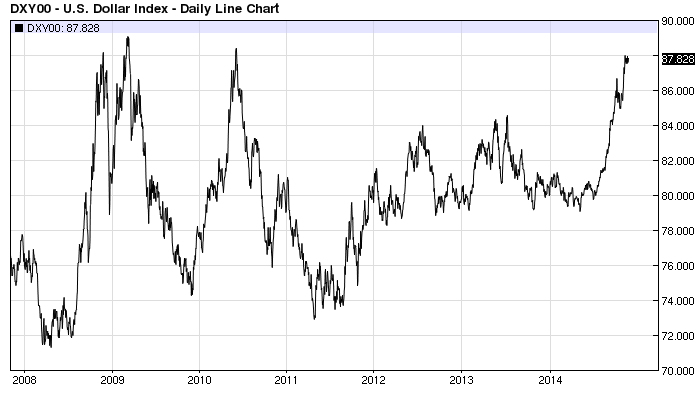

The precipitous decline in 2008 was driven by the global recession following the US sub-prime crisis. The liquidity fuelled recovery in the oil price and the world economy was engineered by the largest central banks. During the same period the US$ Index rose and then declined in a broadly inverse manner to Oil though the motivation for the vacillations in the value of the US currency is broader:-

Source: Barchart.com

Aside from the steady strengthening of the US$ there are a number of factors which have conspired to drive oil prices lower. Firstly there has, and will continue to be, additional supply emanating from the US where improved energy technology has produced significant increase in production over the last five years –from 1.8bln barrels in 2008 to 2.3bln barrels in 2013. In May 2014 it hit a 25 year high of 8.4mln barrels and the Energy Information Administration (EIA) forecast 2015 production will hit the highest level since 1972. The economic impact of cheaper US energy underpins a manufacturing renaissance which is slowly gathering momentum across America.

The next factor is Saudi Arabian production which has not yet been reduced in response to lower prices. Perhaps this, in turn, is a reaction to the secular decline in oil demand from developed countries; though the announcement, last week, of an emissions reduction agreement by China and the USA may add to the downward pressure. Brookings – The U.S. and China’s Great Leap Forward opined thus: –

The world’s two largest emitters of carbon dioxide together pledged deep reductions – well in advance of the pressure they will face in the upcoming UN Climate Change negotiations that begin in Lima later this month, and which are scheduled to conclude a year from now in Paris. They also did so at a level deeper than many had expected. While both countries have already begun efforts to cut emissions, the timing of the announcement and the depth of the reductions went beyond what many diplomats, businesses and environmental groups anticipated.

… Internationally, both countries have a range of other issues to address – including working with the poorest nations which lack the resources to make similarly dramatic cuts, but who are deeply affected by a warmer, wetter world. Still, even with all those obstacles ahead, today’s agreement is the beginning of a great leap forward for climate protection.

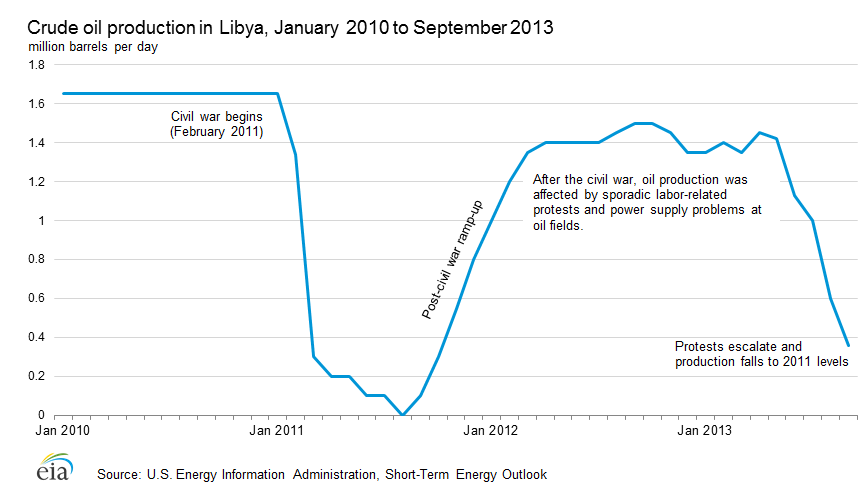

Additional supply could swiftly come on stream from Libya. Further talks are scheduled between the rival Libyan factions in Khartoum, Sudan, on December 1st. The chart below shows how swiftly Libyan production has declined:-

Source: EIA

Also hanging over the market is the prospect of Iranian production increases as international sanctions are reduced. Between 2011 and 2013 Iranian oil exports declined from 3mln bpd to less than 1mln bpd. This year they have rebounded strongly, averaging more than 1mbpd. Iranian production has been running at around 3 mbpd but the National Iranian Oil Company expects an increase to 4.3 mbpd next year – though several commentators are doubtful of Iran’s ability to achieve this increase in output. For more detail on the Iranian situation this article – Al Monitor – Iran takes steps to reduce economic risk of falling oil prices may be of interest.

There are some demand factors which may also undermine prices. Chinese growth has been slowing but, more importantly, the Chinese administration has adopted a policy of re-balancing away from production towards domestic consumption. In theory this process should reduce China’s energy demand; off-set, to some degree, by increased export demand from other emerging market countries as they seek to supply China’s consumption needs. I believe lower energy prices will help Chinese exporters to increase margins or export volumes – or both.

The latest IEA Oil Market Report made these observations: –

Oil’s rout gained momentum in October and extended into November, with Brent at a four-year low below $80/bbl. A strong US dollar and rising US light tight oil output outweighed the impact of a Libyan supply disruption. ICE Brent was last trading at $78.50/bbl – down 30% from a June peak. NYMEX WTI was at $75.40/bbl.

Global oil supply inched up by 35 kb/d in October to 94.2 mb/d. Compared with one year ago, total supply was 2.7 mb/d higher as higher OPEC production added to non-OPEC supply growth of 1.8 mb/d. Non-OPEC production growth is forecast to ease to 1.3 mb/d for 2015 from this year’s 1.8 mb/d high.

OPEC output eased by 150 kb/d in October to 30.60 mb/d, remaining well above the group’s official 30 mb/d supply target for a sixth month running. The group’s oil ministers meet on 27 November against the backdrop of a 30% price decline since they last gathered in June.

Global oil demand estimates for 2014 and 2015 are unchanged since last month’sReport, at 92.4 mb/d and 93.6 mb/d, respectively. Projected growth will increase from a five-year annual low of 680 kb/d in 2014 to an estimated 1.1 mb/d next year as the macroeconomic backdrop is expected to improve.

OECD industry oil stocks built counter-seasonally by 12.6 mb in September. Their deficit versus average levels, after ballooning earlier this year, fell to its narrowest since April 2013. Preliminary data show that despite a 4.2 mb draw, stocks swung into a surplus to average levels in October for the first time since March 2013.

Global refinery crude demand hit a seasonal low in October amid peak plant maintenance and seasonally weak product demand. The 4Q14 throughput estimate is largely unchanged since last month’s Report, at 77.5 mb/d, as robust Russian and Chinese throughputs offset a steeper-than-expected drop in US runs in October.

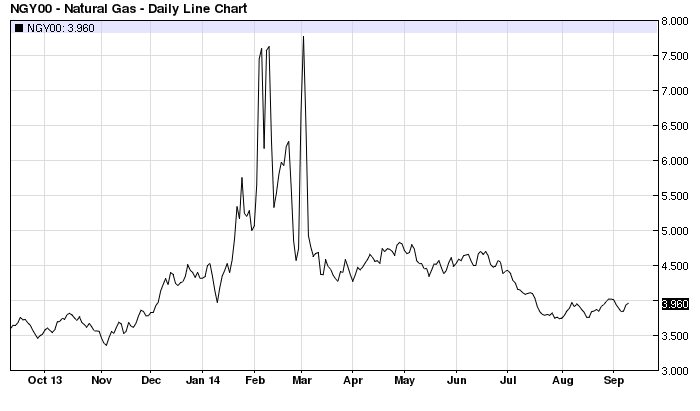

Set against these forces, driving the price of oil lower, is the geo-political tension between Russia and NATO, the ISIS insurgency in Iraq and the continued instability of the Middle East emanating from the civil war in Syria. It is difficult to estimate how far the oil price would decline if the civil unrest in Ukraine and Syria ended tomorrow, I suspect, another 20% to 25%% -during the Kuwait War in the month of October 1990 the price of WTI declined from $40 to $27/barrel even before the war was over:-

Source: Barchart.com

From a technical perspective the breakout from the 2011 range to the downside suggests support around $66, $62, $58, with a final capitulation target of $46. There are, however, reasons to be more optimistic about the prospects for oil, even near-term.

A factor, mentioned by the IEA, which may lead to a reduction in supply, is the outcome of the forthcoming OPEC meeting due to take place on 27th November. Qatar has already begun, reducing production from 800,000 bpd to 650,000bpd last month. At the end of November they will reduce production further to 500,000 bpd – in total a 40% cut. They are not the only countries to be reducing production. The tables below are taken from the OPEC Monthly Report November 2014 which included Secondary Sources: –

Source: OPEC

Whilst oil prices may trend somewhat lower the term structure of the TWI futures market has recently returned from several years of backwardation to contango – Brent Crude has been in contango for some while. This suggests that lower prices are beginning to reduce US domestic over-supply as smaller US operators cease to be able to produce oil profitably. Below $65 the EIA forecast for 2015 will probably need to be revised lower. Prices are likely to be better underpinned at their current levels.

Another encouraging factor is US domestic demand from refiners. US Crack spreads – the price spread between crude oil and its products – has started to widen in recent weeks. Oil demand should increase in response to higher product margins. The cracking margins have risen most dramatically for Gasoline but Heating Oil margins have also improved and may catch up if predictions of an exceptionally cold winter in the Northern hemisphere prove to be correct. NOAA – Winter Outlook from last month is reasonably sanguine – warm in the West and Alaska, cold in South and Rockies – but substantial snowfall in Siberia (the largest in October since 1967) is cause for caution.

Global Growth

This brings me on to the impact of lower oil prices on global growth. Obviously the large crude oil exporting countries will suffer from reduced revenue but the importers of oil – and gas, since many gas contracts are referenced to the price of oil – should be beneficiaries. This recent article from Brookings – Oil – A Question of Economics – reminds readers of some of the ubiquitous benefits to the global economy of lower energy prices: –

Virtually all businesses will benefit from lower transportation costs by expanding their profit margins or passing the benefit to consumers at lower prices. The lower income groups, who spend a higher proportion of their incomes on transport, will see their disposable incomes rise, benefiting retailers who serve their needs and thereby increasing demand in the economy. Food prices are also likely to fall, as food production, processing and sales distribution are energy intensive activities, thereby benefiting lower income groups further. Increased consumption will stimulate aggregate demand, creating investment opportunities and economic growth. Governments in the west may also have the opportunity to increase fuel taxes to cover the real cost of the negative externalities of carbon emissions, or raise revenue to improve public transportation systems. Furthermore, governments in the Middle East and Asia will reduce spending on their fuel subsidies and may take the opportunity to improve the workings of market forces, which the IMF and Western powers have been seeking for them to do.

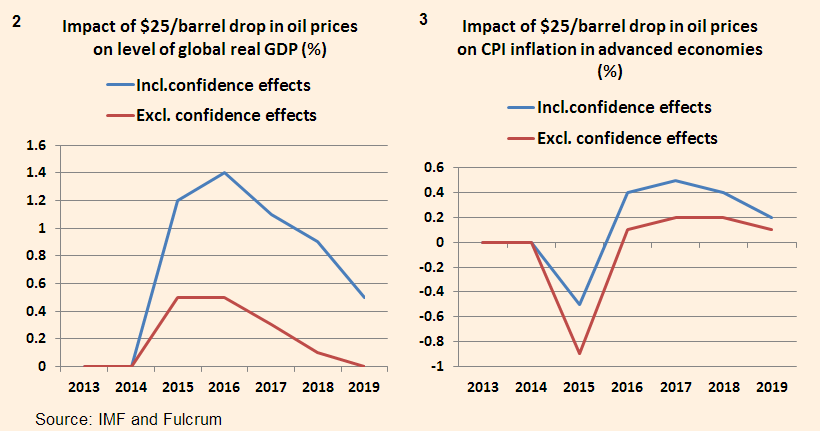

The effect of lower oil prices is felt quite rapidly by consumers globally. Oil consumers, at the household level, receive an immediate boost to their real income. This “wind-fall” is then either spent or saved. An explanation of these effects can be found in this Gavyn Davies article in the Financial Times – Large global benefits from the 2014 oil shock (Some of you may need to subscribe to this “limited free service”). He uses IMF data to produce two very interesting charts: –

Source: IMF and Fulcrum

The fall in inflation will be of greater concern to the ECB than the other major central banks. The BoJ has already acted aggressively in response to the economic slowdown in Japan, the Abe government has deferred a scheduled tax increase and announced an early election. The Federal Reserve, having completed its tapering of QE, will be focussed on wage growth. As central bank to the world’s second largest and rising oil producer, the Fed will be concerned about the drag on growth from a slowdown in the energy and utility sectors; market expectations of interest rate increases will be deferred once again. If the ECB act aggressively to head off the chimera of deflation this may be enough to improve global confidence – I believe this makes the blue line prediction more likely. If WTI should plummet towards $60, the improvement in economic growth should be even greater.

As recently as last month the IMF – World Economic Outlook – forecast for Oil prices was $102.76 for 2014 and $99.36 for 2015. They continue to cling to their forecasts based on expectation of increased geo-political tensions. Given that their 2015 forecast is around 30% above current levels if they are mistaken and the oil price remains subdued their global growth forecast could be around 0.6% too low.

Last month The Economist – Cheaper Oil: Winners and Losers – took up the theme of lower oil prices:-

A 10% change in the oil price is associated with around a 0.2% change in global GDP, says Tom Helbling of the IMF. A price fall normally boosts GDP by shifting resources from producers to consumers, who are more likely to spend their gains than wealthy sheikhdoms. If increased supply is the driving force, the effect is likely to be bigger—as in America, where shale gas drove prices down relative to Europe and, says the IMF, boosted manufactured exports by 6% compared with the rest of the world. But if it reflects weak demand, consumers may save the windfall.

The authors go on to discuss farmers as the main direct beneficiaries of cheaper oil. India especially but other economies with a large agricultural sector as well: –

Energy is the main input into fertilisers, and in many countries farmers use huge amounts of electricity to pump water from aquifers far below, or depleted rivers far away. A dollar of farm output takes four or five times as much energy to produce as a dollar of manufactured goods, says John Baffes of the World Bank. Farmers benefit from cheaper oil. And since most of the world’s farmers are poor, cheaper oil is, on balance, good for poor countries.

Take India, home to about a third of the world’s population living on under $1.25 a day. Cheaper oil is a threefold boon. First, as in China, imports become cheaper relative to exports. Oil accounts for about a third of India’s imports, but its exports are diverse (everything from food to computing services), so they are not seeing across-the-board price declines. Second, cheaper energy moderates inflation, which has already fallen from over 10% in early 2013 to 6.5%, bringing it within the central bank’s informal target range. This should lead to lower interest rates, boosting investment.

Third, cheaper oil cuts India’s budget deficit, now 4.5% of GDP, by reducing fuel and fertiliser subsidies. These are huge: along with food subsidies, the total is 2.5 trillion rupees ($41 billion) in the year ending March 2015—14% of public spending and 2.5% of GDP. The government controls the price of diesel and compensates sellers for their losses. But, for the first time in years, sellers are making a profit. As in China, cheaper oil should reduce the pain of cutting subsidies—and on October 19th Narendra Modi, India’s prime minister, said he would finally end diesel subsidies, free diesel prices and raise natural-gas prices.

The price move has also prompted a response from the researchers at the Dallas Fed – Oil Prices Fall Despite Global Uncertainty – whilst their concern is broadly domestic they note that it is Non-OECD demand which is driving the increase in oil demand. The largest beneficiaries of lower oil prices will be oil importing emerging market countries: China, India and, to the extent that they are still considered an emerging economy, South Korea. Other candidates include Singapore, Taiwan, Poland, Greece, Indonesia, South Africa, Brazil and Turkey.

Conclusion and Investment Opportunities

Foreign Exchange

The fall in oil prices has been mirrored, inversely, by the rise of the US$. This trend is already well established but I expect it to continue. This is not so much a reflection of the strength of the US economy as the moribund nature of growth expectations in the EU and Japan.

Government Bonds

Lower inflation expectations, combined with central bank inflation targets, should ensure a delay to interest rate tightening even in response to a resurgence of wage growth. Bond prices will continue to be underpinned. At any sign of a slowing of economic growth, yield curves will flatten further. Convergence of EZ bond yields will continue.

Equities

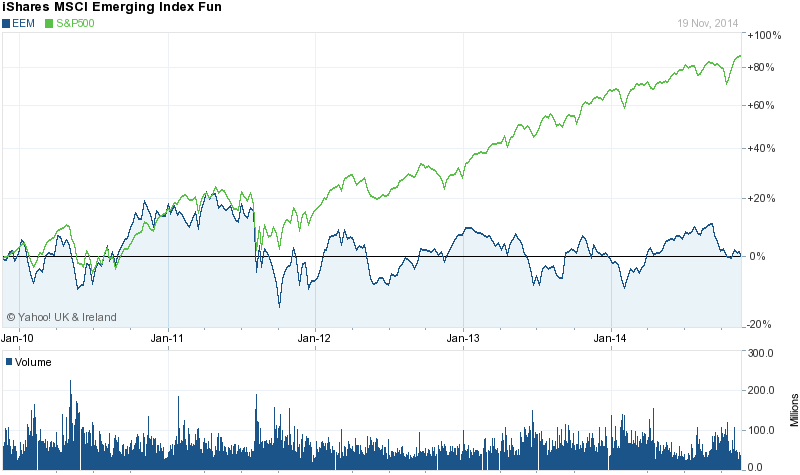

The chart below shows the relative performance of the S&P500 Index vs MSCI Emerging Market ETF (EEM) over the last five years, after an initial rebound from the Great Recession the US stock market began to outperform other stock markets, driven by the economic boon of oil and gas technology, the implementation of TARP and the highly accommodative policies of the Fed. With the current round of QE at an end, US investors may need to look further afield in search of value :-

Source: Yahoo Finance

Expectation of “Lower for Longer” interest rates and cheaper oil is supportive for stock markets in general although there will be sector specific winners and losers. Geographically, lower oil prices will favour those economies most reliant on oil imports, especially if their exchange rate is pegged to the US$. Given the under-performance of many emerging market equities over the last few years I believe this offers the best investment opportunity going forward into 2015. Those countries with floating exchange rates such as India have already benefitted from currency devaluation of 2013; however, there is still potential upside for equities, even after the strong performance of 2014. The SENSEX Index (BSE) started the year around 21,000 and is currently making new highs at 28,000, but during the last three months it has tended to track the performance of the S&P 500 Index – despite the fall in oil prices. I anticipate a general re-rating of emerging market equities next year.