Macro Letter – No 47 – 04-12-2015

What are the prospects for UK financial markets in 2016?

- The EU referendum may take place as early at as June next year

- Financial markets appear to be ignoring the vote at present

- The tightening of bank capital requirements is almost over

- Higher tax receipts have tempered the pace of fiscal tightening

In assessing the prospects for UK financial markets next year I will focus on three areas, the EU referendum, the stability of the financial system and the state of government finances.

The EU Referedum

As we head into 2016 political and economic commentators are beginning to focus on the potential impact of a UK exit from the EU would have on the British economy. Given the size and importance of the financial services sector to the economy, I want to investigate claims that a UK exit would be damaging to growth and lead to a rise in unemployment. For a more general overview of the referendum please see my July 3rd post – Which way now – FTSE, Gilts, Sterling and the EU referendum?

In February a report by the UK Parliament – Financial Services: contribution to the UK economy opened with the following statement:-

In 2014, financial and insurance services contributed £126.9 billion in gross value added (GVA) to the UK economy, 8.0% of the UK’s total GVA. London accounted for 50.5% of the total financial and insurance sector GVA in the UK in 2012. The sector’s contribution to UK jobs is around 3.4%. Trade in financial services makes up a substantial proportion of the UK’s trade surplus in services. In 2013/14, the banking sector alone contributed £21.4 billion to UK tax receipts in corporation tax, income tax, national insurance and through the bank levy.

The GVA was down from a 2009 high of 9.3%. For London the GVA was 18.6%. In international terms the UK ranks fourth, behind Luxembourg, Australia and the Netherlands in terms of the size of its financial services sector. As at September 2014, 1.1mln people were employed in the sector. According to research by PWC financial services accounted for £65.6bln or 11.5% of total government tax receipts in 2013-14.

Last week the Evening Standard – ‘Brexit’ would lead to loss of 100,000 bank jobs, says City – cited senior banking figures warning of the potential impact of the UK leaving the EU:-

Mark Boleat, policy chairman at the City of London Corporation, said: “If as a country we were to vote to leave, then London’s position as a leading financial centre would remain but without doubt there would be an impact on our relative size and the jobs we support.”

Confidential client research from analysts at US investment bank Morgan Stanley, seen by the Standard, warned that “firms for whom the EU market is important” would need to “adjust their footprint” in London if the Eurosceptic cause was victorious.

Sir Mike Rake, deputy chair of Barclays and chairman of BT, said: “It is extremely difficult to quantify the number of jobs that would be lost and the time frame over which that might happen but leaving the EU would severely damage London’s competitiveness and our financial services sector.”

There have been growing hints from financial institutions that they are starting to plan for Britain quitting the 28 member club.

Both HSBC, which announced a review of the location of its global headquarters in April, and JP Morgan are reportedly in talks about moving sections of their businesses to Luxembourg in part because of the threat of Brexit.

Deutsche Bank, which employs 9,000 people in Britain, has set up a working group to review whether to move parts of its business from Britain in the event of a UK withdrawal.

US asset management group Vanguard, which has a City office, has admitted that Brexit would have a “significant impact” on its operation across Europe and has already started planning for it.

Many senior bankers are concerned that they would lose the financial services “passporting” rights enjoyed by fellow EU members.

A fascinating historic assessment of the opinion of the UK electorate towards the EU is contained in this week’s Deloitte – Monday Briefing, they anticipate a referendum date of either June or September 2016, in order to avoid coinciding with a French (March/April) or German (September) election in 2017:-

Since Ipsos MORI started polling on this issue in 1977 on average 53% of voters in a simple yes/no poll have supported membership and 47% have opposed it. The yes vote reached a low of 26% in 1980 rising, over the following decade, to a peak of 63% in 1991, shortly before the pound’s ejection from the European Exchange Rate Mechanism.

In June of this year Ipsos MORI showed UK public support for the EU, again on a straight yes/no poll, at an all-time peak of 75%. Since then it has fallen away in parallel with heightened UK public concerns about immigration. The most recent Ipsos MORI poll, from mid-October, showed the yes vote at 59%.

More recent polls suggest a further narrowing of the yes lead. Across eight polls carried out in November the yes vote averaged 52% and the no vote 48%.

The yes vote is, by and large, younger and more affluent than the no. Opposition to the EU rises sharply among the over 40s, an important consideration given that voter turnout is higher among older voters. Conservative voters tend to be more eurosceptic than Labour voters; white voters tend to be more sceptical than non-white voters.

… “don’t knows” averaged around 15% of all voters, more than enough to tip the vote decisively.

The last referendum on UK membership of what was then the European Economic Community (EEC) was held in 1975, just two years after the UK joined the EEC. The vote was an overwhelming victory for EEC membership, with the electorate voting by 67.2% to 32.8% to stay in.

… In an intriguing paper economists David Bowers and Richard Mylles of Absolute Strategies Research (ASR) outline how the political landscape has shifted in the last 40 years.

… in 1975 the debate was about membership of a trading bloc, the Common Market. For sure, the commitment to “ever closer union” was in the Treaty of Rome, but in 1975 few in the UK, especially in the yes campaign, paid much attention to it. Since then the EU has grown from 9 to 28 members, expanded into Central and Eastern Europe, created the Single Currency and acquired more characteristics of a federal union.

…In 1975 the UK economy was in a shambles, slipping into the role of sick man of Europe. In the previous three years the UK had endured a recession, double digit inflation, endemic industrial unrest and the imposition of a three-day working week to save scarce energy supplies. British voters in 1975 looked enviously to the prosperity and stability of Germany. Today the UK is seeing decent growth, while the euro area grapples with the migration crisis, sluggish activity and the difficulties of building a durable monetary union. On a relative basis the performance of the UK economy looks, for now at least, pretty good.

…The Maastricht Treaty of 1992 established the right of people to live and work anywhere in the EU, but… it was EU enlargement into Central and Eastern Europe in 2004 that caused immigration into the UK to rise markedly, pushing migration up the list of UK voter concerns. More recent migration from North Africa and the Middle East, and the growing problems facing the Schengen nations, have added new concerns.

The final factor…was the enthusiasm of the majority of the press for the Common Market in 1975. The press gave the then Prime Minister, Harold Wilson, largely uncritical coverage of his negotiations for a “better deal” in Britain’s relationship with the Community. (Historians tend to the view that Wilson actually achieved little in his negotiations with the Community; but he deftly turned meagre result into a public relations triumph). The lone dissenting voice in a general mood of press enthusiasm for the EEC was the Communist Morning Star. This time round it seems likely that a number of major papers will take a euro sceptic line.

The most recent poll, published by ORB last week in the wake of the Paris attacks, found 52% in favour of exit.

Financial Stability

This week saw the release of the Bank of England – Financial Stability Report – December 2015 – it suggests that the UK economy has moved beyond the post-crisis phase, the risks are, once again, external in nature:-

The global macroeconomic environment remains challenging. Risks in relation to Greece and its financing needs have fallen from their acute level at the time of the publication of the July 2015 Report. But, as set out in July, risks arising from the global environment have rotated in origin from advanced economies to emerging market economies. Since July, there have been further downward revisions to emerging market economy growth forecasts. In global financial markets, asset prices remain vulnerable to a crystallisation of risks in emerging market economies. More broadly, asset prices are currently underpinned by the continued low level of long-term real interest rates, which may in part reflect unusually compressed term premia. As a consequence, they remain vulnerable to a sharp increase in market interest rates. The impact of such an increase could be magnified, at least temporarily, by fragile market liquidity.

Domestically, the FPC judges that the financial system has moved out of the post-crisis period. Some domestic risks remain elevated. Buy-to-let and commercial real estate activity are strengthening. The United Kingdom’s current account deficit remains high by historical and international standards, and household indebtedness is still high.

Against these elevated risks some others remain subdued, albeit less so than in the post-crisis period to date. Comparing credit indicators to the past alone cannot provide a full risk assessment of the level of risk today, but can be informative. Aggregate credit growth, though modest compared to pre-crisis growth, is rising and is close to nominal GDP growth. Spreads between mortgage lending rates and risk-free rates have fallen back from elevated levels.

They go on to note that the Tier 1 capital position of major UK banks was 13% of risk-weighted assets in September 2015, below the levels advocated by the Vicker’s Commission but above Basel requirements. The Financial Policy Committee (FPC) are expected to impose a 1% counter-cyclical capital buffer in the near future, but otherwise the fiscal tightening, which has been in train since the aftermath of the financial crisis has finally run its course.

The other risks which concern the Bank are cyber-risks of varying types and, of course, the uncertainty surrounding the EU referendum.

Autumn Statement and Spending Review

Last week saw the publication of the UK Chancellor’s Autumn Statement and Spending Review. Mr Osborne was fortunate; the OBR found an additional £27bln in tax receipts which allowed him to reverse some of the more unpopular spending cuts previously announced. He still hopes to balance the government budget by 2020/2021. Public spending will rise from £757bln this year to £857bln in 2020/21. Assuming the economy grows as forecast, public spending to GDP ratio should fall from 39.7% to 36.5%.

Writing in the Telegraph Mark Littlewood of the IEA said:-

George Osborne has today made a one-way bet. His announcements are based on two predictions: continually low interest rates and sustained strong economic growth, making our debt repayments lower than anticipated and tax revenues higher than expected. These are not unrealistic assumptions, but if either go off course, the savings announced today will not go nearly far enough.

Market Performance

Stocks

Financial markets abhor uncertainty. Concern about collapsing FDI and Scottish devolution due to Brexit, will hang over the markets until the outcome of the vote is known: meanwhile rising rhetoric will discourage investment. Regardless of economic performance UK stocks are likely to underperform.

Back in July I believed the uncertainty about the UK position on the EU would have minimal effect:-

Unless the UK joins the EZ, currency fluctuations will continue whether they stay or go. Gilt yields will continue to reflect inflation expectations and estimates of credit worthiness; being outside the EU might impose greater fiscal discipline on subsequent UK governments – in this respect the benefits of EU membership seem minimal. The UK stock market will remain diverse and the success of UK stocks will be dependent on their individual businesses and the degree to which the regulatory environment is benign.

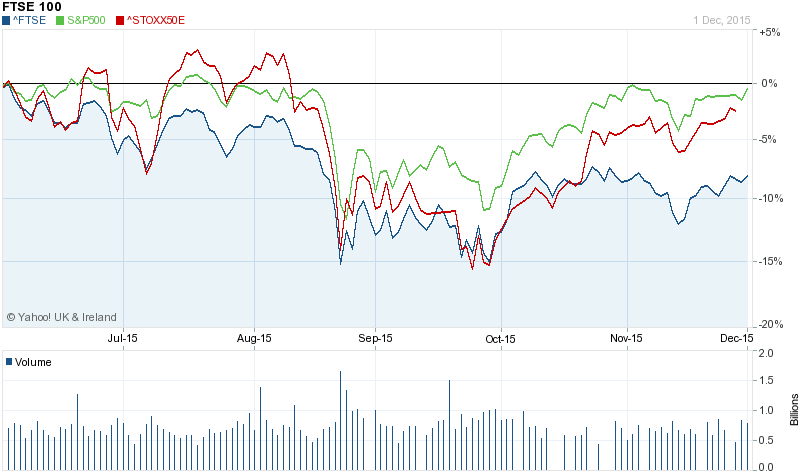

Here’s how the markets have evolved since the summer. Firstly the FTSE100 vs EuroStox50 and S&P500 – six month chart, at first blush, I was wrong, the FTSE has underperformed EutoStoxx and the S&P:-

Source: Yahoo Finance

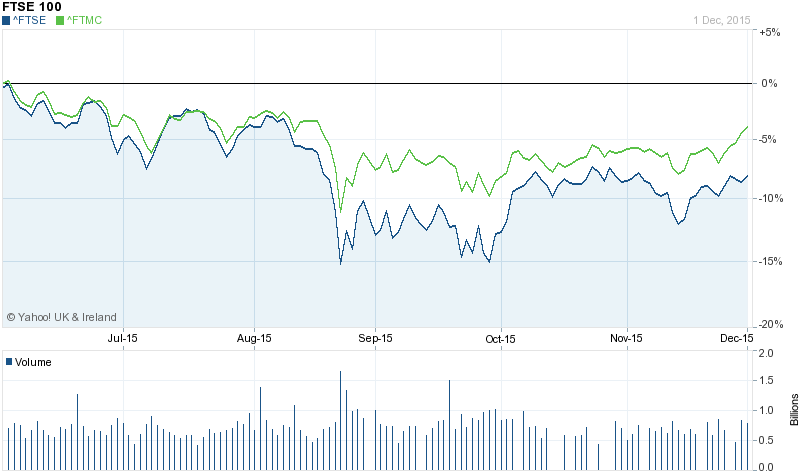

However, the FTSE250 tells a different story:-

Source: Yahoo Finance

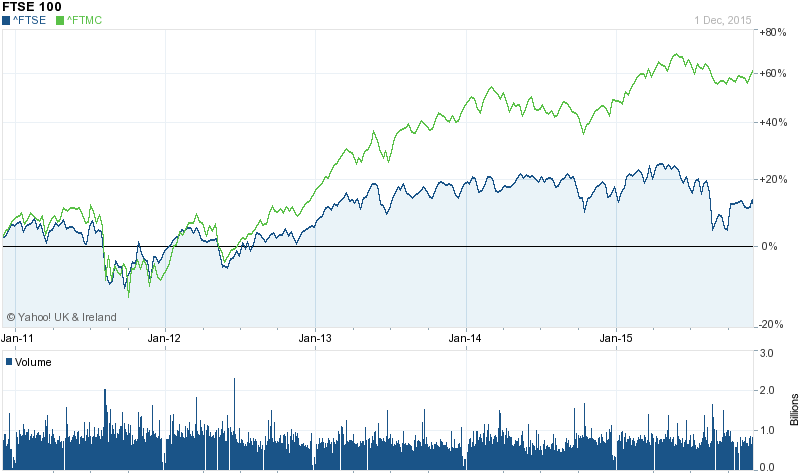

This divergence has been in place for several years as the five year chart below shows:-

Source: Yahoo Finance

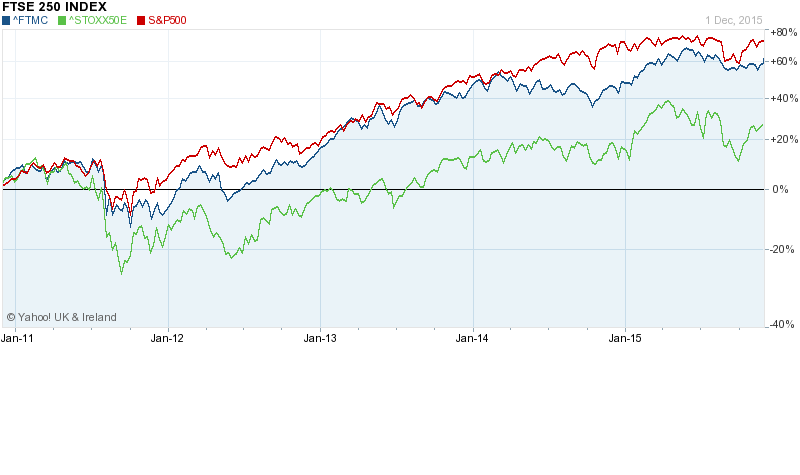

Here is the FTSE250 compared to EuroStox50 and the S&P500 – over the same five year period. The mid cap Index has followed the S&P, although in US$ terms its performance has been less impressive:-

Source: Yahoo Finance

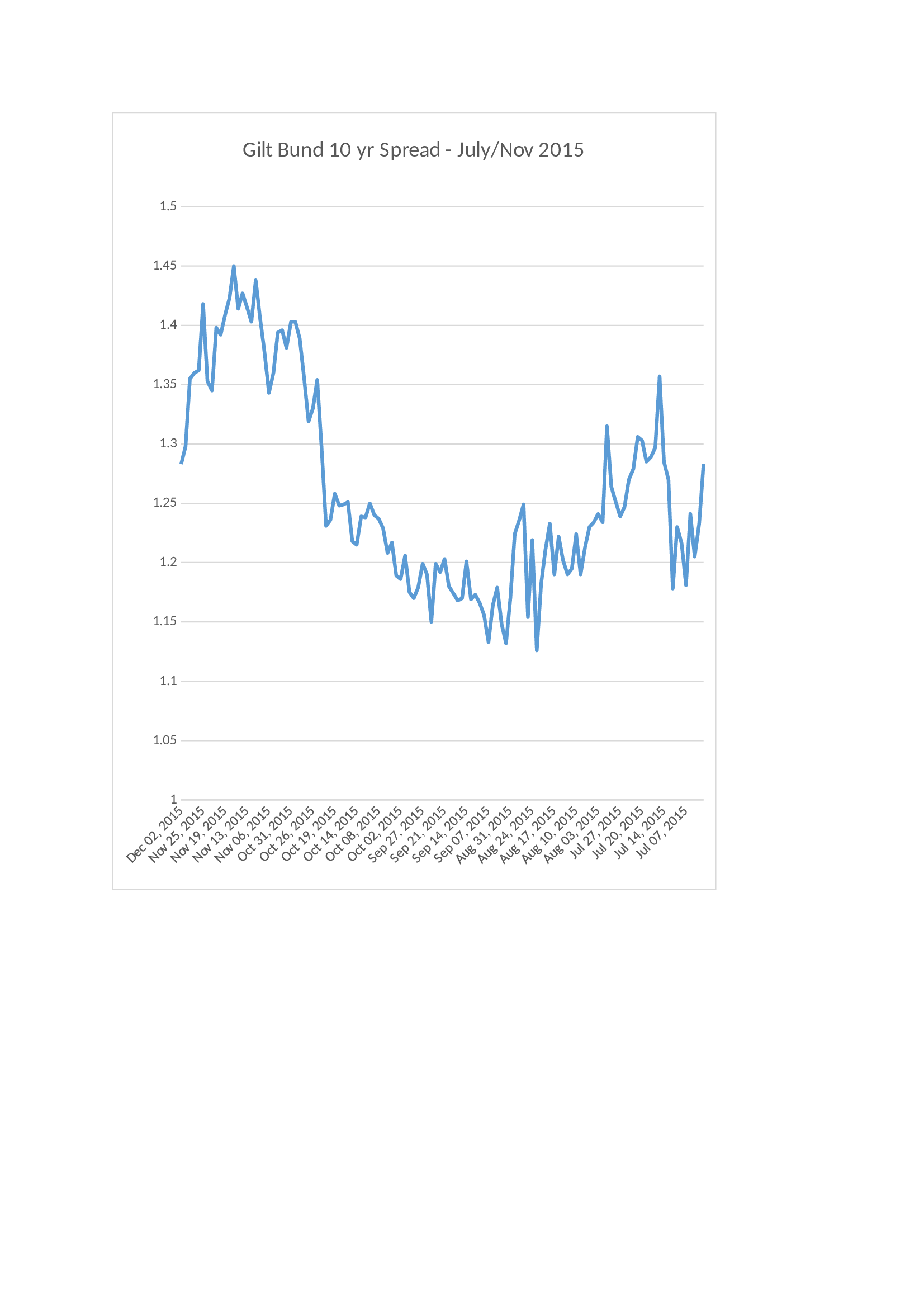

Gilts and Bunds

During the period since the beginning of July the spread between 10yr Gilts and Bunds has ranged between 112bp and 145bp reaching its narrowest during the fall in equity markets in August and widening amid concerns about European growth last month. UK Inflation expectations remain subdued; this is how the MPC – November Inflation Report described it:-

All members agree that, given the likely persistence of the headwinds weighing on the economy, when Bank Rate does begin to rise, it is expected to do so more gradually and to a lower level than in recent cycles.

Sterling

The Sterling Effective Exchange Rate has traded in a relatively narrow range (please excuse the date axis, vagaries of the Bank of England’s data format – this is a one year chart):-

Source: Bank of England

During stock market weakness in the summer Sterling strengthened. After weakening in October it rebounded, following the US$, in November.

Back in July I anticipated a weakening of Sterling:-

Ahead of the referendum, uncertainty will lead to weakness in Sterling, higher Gilt yields and relative underperformance of UK stocks. If the UK electorate decide to remain in the EU, there will be a relief rally before long-term trends resume. If the UK leaves the EU, Sterling will fall, inflation will rise, Gilt yields will rise in response and the FTSE will decline. GDP growth will slow somewhat, until an export led recovery kicks in as a result of the lower value of Sterling. The real cost to the UK is in policy uncertainty.

It may be that capital outflows are about to begin in earnest but I start to question my assumptions – the market seems to be caught between the uncertainty surrounding UK membership of the EU and doubts about the longevity of the “European Experiment” as a whole.

Conclusion

Gilts remain below their long run average spread over Bunds but the interest rate environment is exceptionally benign, making any pick up in yield attractive. The FTSE250 index appears to be ignoring concerns about collapsing commodities, slowing emerging markets – especially China – and the prospect of Brexit, but it may struggle to remain detached for much longer. Sterling also appears to have ignored the referendum debate so far. Or perhaps, the UK market is a relative “safe haven” offering exposure to European markets without the angst of Euro membership – either way I remain cautious until the political uncertainties dissipate.