Macro Letter – No 46 – 20-11-2015

Should we buy Turkey for Thanksgiving?

- Erdogan’s AKP won an unexpected majority in this month’s election

- The Turkish Lira (TRY) has fallen by 60% against the USD since 2008

- Turkish stocks look inexpensive by several measures

- Economic reform appears unlikely

Back in June the AKP failed to achieve a majority in this year’s first general election. Second time around they achieved a resounding victory – though not the “supermajority” required for constitutional reform. The main reason for the loss of confidence earlier in the year was the state of the Turkish economy. Now the AKP has an opportunity to embark on economic reform – this may be easier said than done.

They need to deal with rising unemployment which, having dipped to 9.3% in May, is on the rise again – August 10.1%. Labour participation has been steadily rising – from 43.6 in 2006 to 51.2 today, however it is still low by international standards and female participation is a rather dismal 29%. Youth unemployment has fallen from 28% in 2009 to 18.3% in August, but this does not bode well for their relatively young nation. Of the 77mln population, 67% are notionally working age – 15 to 64. Only 6% are over 64 years. Turks make up 75% of the population whilst Kurds already account for 18%; as this 2012 article from the IB Times – A Kurdish Majority In Turkey Within One Generation? makes clear, substantial cultural challenges lie ahead.

High unemployment has impacted consumer confidence which plunged to 58.52 in September – its lowest level since the global recession of 2009. October saw a rebound to 62.78.

Core inflation remains stubbornly high despite the fall in oil prices. During the summer it dipped below 8% but by October it was 9.3%. The chart below shows the core inflation rate over the last decade:-

Source: Tradingeconomics and Eurostat

High inflation is primarily due to the weakness of the TRY; the next chart shows USDTRY, but the BIS Effective exchange rate also declined from 100 in 2010 to 70.6 at the end of 2014. The last big TRY devaluation occurred between February and October 2001, the move since 2008 has been of a similar magnitude, albeit with less precipitous haste:-

Source: Tradingeconomics

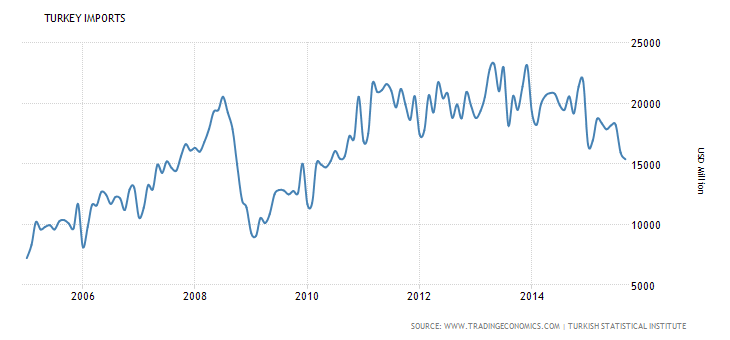

Inflation might have been even higher had imports not fallen:-

Source: Tradingeconomics and Turk Stat

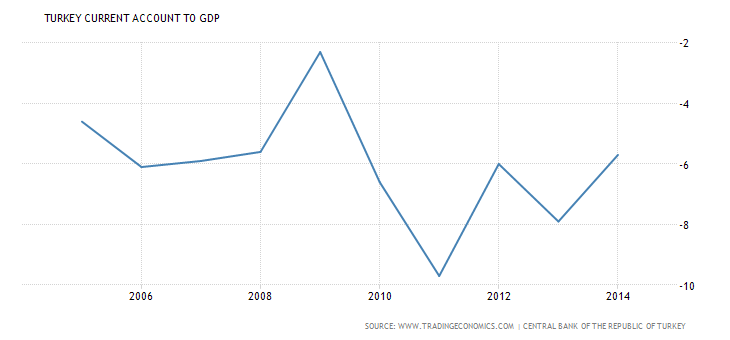

The decline in imports, principally from Russia (10.4%) China (10.3%) and Germany (9.2%) helped reduce the current account deficit to some extent but at -6% of GDP it remains, unhealthy:-

Source: Tradingeconomics and Central Bank of Turkey

Turkey is a big energy importer – for a more detailed discussion on energy security for Turkey (and the EU) this working paper from Bruegel – Designing a new Eu-Turkey Gas Partnership is worth perusal.

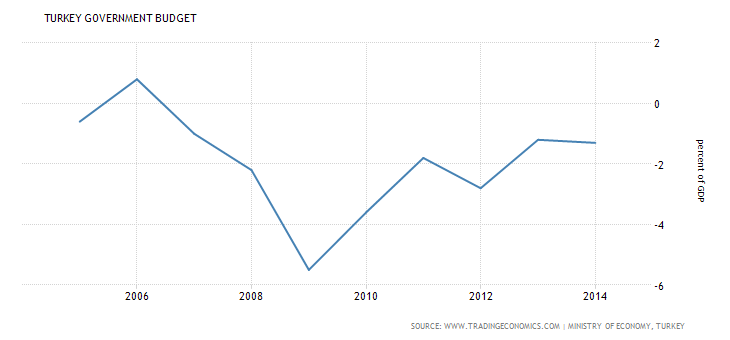

The current account deficit is matched by the government budget balance, this has remained negative for most of the decade, although the debt to GDP ratio is an undemanding 33%:-

Source: Tradingeconomics and Turkish Ministry of Economics

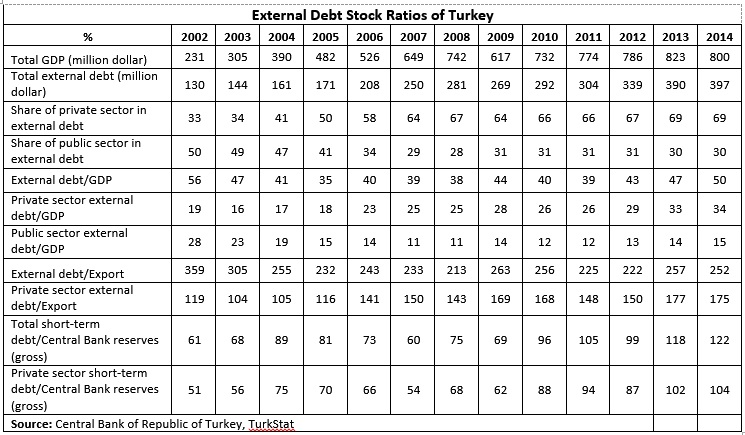

Meanwhile Turkey’s external debt continues to grow, it now equates to more than half of GDP:-

Source: Tradingeconomics and Turkish Treasury

Much of the external borrowing has been short-term and the private sector accounts for more than two thirds of the total. Since 2002 GDP has increased from $233bln to $800bln – during the same period external debt has tripled. Short-term debt to central bank reserves have doubled. The table below investigates this and other aspects of Turkey’s external debt:-

Source: Central Bank of Turkey and Turk Stat

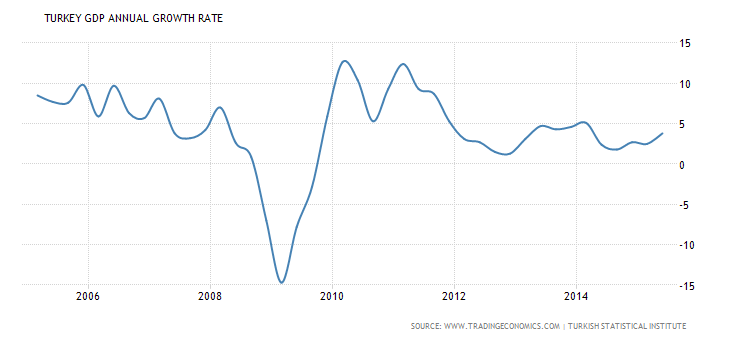

In 2013 Morgan Stanley dubbed Turkey one of the “fragile five”, the others being Brazil, India, Indonesia and South Africa. These countries had high external debt, twin deficits, structurally high inflation and slowing growth. Turkish GDP has been recovering somewhat this year – 3.8% in Q2 2015 – but it remains below its 2002-2011 average of 5.2%:-

Source: Tradingeconomics and Turk Stat

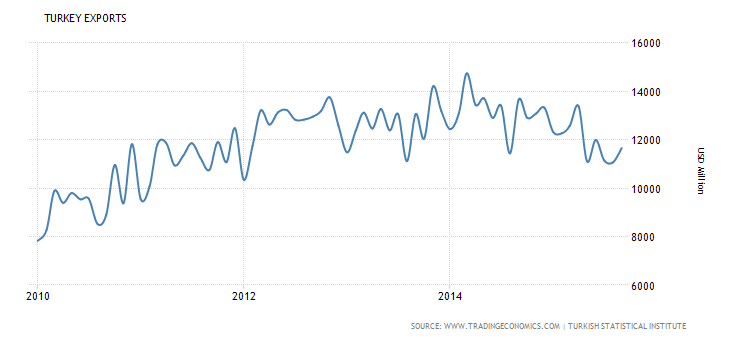

Given the weakness of the currency it is surprising that economic recovery has not been more pronounced. This may be due to the parlous state in Turkey’s principal export markets, Germany (9.6%) has seen slow growth and Iraq (6.9%) has been in recession:-

Source: Tradingeconomics and Turk Stat

In March Morgan Stanley announced that India and Indonesia had made sufficient reforms to be removed from the “Fragile” category. Turkey remains, unreformed, especially in terms of its labour laws – a focal point if they are to reduce structural unemployment.

Turkey has demographic trends on its side but its productivity has been stagnant since the financial crisis. The OECD estimated GDP per hour for 2014 at 29.3 hours – in 2007 it was 28.9 hours.

Financial Markets

Short-term interest rates, which touched 10% last year, have fallen to 7.5%, despite inflation and TRY weakness, but the independence of the central bank has been questioned since Erdogan openly criticised their interest rate policy in March – with the AKP majority restored the problem of inflation may be deferred:-

Source: Tradingeconomics and Central Bank of Turkey

Reflecting market sentiment better, 10yr Turkish Government bonds, reached 10.78% in October, although they have recovered, in the wake of the election, to yield 9.72% today (Wednesday 18th) here is a five year chart:-

Source: Tradingeconomics and Turkish Treasury

From a technical perspective bond yields appear to have backed away from the 2014 highs, but considered in conjunction with the continued trend of the TRY, I lack the confidence to buy ahead of real economic reform package. Meanwhile, the US Federal Reserve look set to raise interest rates next month, putting further downward pressure on the TRY and driving short-term US$ financing costs higher.

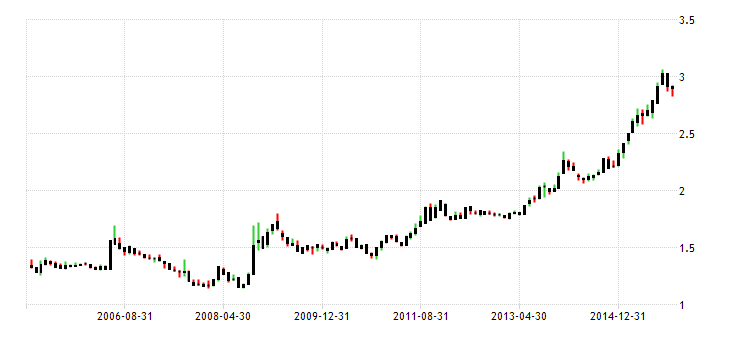

The Turkish XU100 stock index rallied from 77,776 to 83,692 after the election – today (Wednesday 18th) it stands at 81,274. It has been buoyed by currency weakness:-

Source: Tradingeconomics and Istanbul Stock Exchange

The market valuation is relatively undemanding. A CAPE of 10.3 is higher than its emerging European neighbours, but on a straight PE basis (11 times) and dividend yield (3.4%) it is comparable. On a price to cost, price to book or price to sales basis, however, it is more expensive than Emerging Europe.

The largest stocks in the index are:-

| Company | Ticker | Sector |

| Garanti Bankası | GARAN | Banking |

| Akbank | AKBNK | Banking |

| Turkcell | TCELL | Telecommunications |

| Koç Holding | KCHOL | Conglomerate |

| Türkiye İş Bankası | ISATR | Banking |

| Türk Telekom | TTKOM | Telecommunications |

| Enka İnşaat | ENKAI | Construction |

| Sabancı Holding | SAHOL | Conglomerate |

| Halk Bankası | HALKB | Banking |

| Efes Beverage Group | AEFES | Beverage |

| Vakıfbank | VAKBN | Banking |

| Turkish Airlines | THYAO | Transportation |

Source: Istanbul Stock Exchange

Whilst the economy is 25% Agriculture, 26% Industry and 49% Services, the stock market is dominated by banks. At the end of 2013 the weights for the XU100 were 36% Banks, 17% Beverages and 8% Conglomerates – although the fragmented (30 companies) cement industry should be mentioned. It is the largest in Europe and fifth largest globally. Rising bond yields, even though they have fallen since the election, and the weakness of the TRY increase the risk of bank losses. Technically, one should remain long, but I’m not inclined to add aggressively at this stage.

An additional concern is Turkey’s political relations with the EU. According to a 3rd September article from Brookings – Why 100,000s of Syrian refugees are fleeing to Europe:-

Turkey’s is being deeply affected too, in spite of having the largest economy in the region and a strong state tradition. Its resources and public patience are wearing thin. The Syrian refugee issue certainly plays a role in the current political instability in the country. According to UNHCR, Turkey became the world’s largest recipient of refugees (total, including those from Iraq) in 2014.

The EU’s inability to act on concert to address the migrant crisis, along with the imminent collapse of the Schengen Agreement, is likely to further strain relations. It may not stop existing trade but it is likely to slow new business developments.

Security remains a major issue for the new Turkish government as CFR – What Turkey’s Election Surprise Says About the Troubled Country explains:-

…Turkey now confronts simultaneous conflicts with the PKK and the Islamic State. After a year of intensive American diplomacy, Ankara’s decision last July to provide the United States and coalition forces access to air bases close to the Islamic State’s territory has made Turkey a target.

On a more positive note. The new government is likely to make good on its election promises by increasing fiscal stimulus. That 33% debt to GDP ratio must be burning a hole in Erdogan’s pocket. Stimulus is expected to be directed at infrastructure – the “three R’s”, roads, railways and real-estate. “Grand projects” include a third Airport and a mountaintop mosque for Istanbul, a third bridge and a tunnel across the Bosporus, a canal linking the Black Sea to the Sea of Marmara and a gigantic presidential palace in Ankara.

Conclusion – the currency is key

On balance I think it is too soon to buy Turkish bonds or stocks. The new government seems reluctant to embrace the economic reforms needed to drive productivity growth. External debt will have to be repaid, inflation, subdued and jobs created. Turkish stocks look relatively inexpensive and her bonds may be tempting to the carry trader, but an appreciating TRY is key – should the currency recover, stocks and bonds will follow.