Macro Letter – No 84 – 29-09-2017

Japan – Politics, Central Banking and the Nikkei 225

- PM Abe called a snap general election for October, amid rising geopolitical tensions

- The BoJ maintain QQE despite Federal Reserve plans to reduce its balance sheet

- Japanese stocks will benefit if the ‘Three Arrows’ of Abenomics continue

- Japanese wages are rising whilst inflation is stuck at zero

On Monday Japanese Prime Minister, Shinzo Abe, called a snap general election. During the press conference in which he made the announcement he said:-

It is my mission as prime minister to exert strong leadership abilities at a time when Japan faces national crises stemming from the shrinking demographic and North Korea’s escalating tensions…

He went on to outline a JPY 2trln stimulus package, to be implemented before year end. This will be financed by raising the consumption tax rate from 8% to 10% in October 2019. The tax increase is expected to generate JPY 5trln/annum and, if any revenue remains after the stimulus, it will be used to reduce government debt. With a further JPY 2trln earmarked for education and social programmes it seems unlikely the maths will add up.

Meanwhile, despite the Federal Reserve’s announcement, last week, that they will begin balance sheet reduction, the Bank of Japan (BoJ) continue their policy of quantitative and qualitative easing (QQE) involving the unorthodox ‘yield curve control’ measures. From more on this please see Macro Letter – No 65 – Yield Curve Control – the road to infinite QE which I published in November 2016. I stand by my conclusion, although my prediction about the JPY (I thought it would continue to weaken) has yet to come to pass:-

If zero 10 year JGB yields are unlikely to encourage banks to lend and demand from corporate borrowers remains negligible, what is the purpose of the BoJ policy shift? I believe they are creating the conditions for the Japanese government to dramatically increase spending, safe in the knowledge that the JGB yield curve will only steepen beyond 10 year maturity.

I do not believe yield curve control will improve the economics of bank lending at all. According to World Bank data the average maturity of Japanese corporate syndicated loans in 2015 was 4.5 years whilst for corporate bonds it was 6.9 years. Corporate bond issuance accounted for only 5% of total bond issuance in Japan last year – in the US it was 24%. Even with unprecedented low interest rates, demand to borrow for 15 years and longer will remain de minimis.

Financial markets will begin to realise that, whilst the BoJ has not quite embraced the nom de guerre of “The bank that launched Helicopter Money”, they have, assuming they don’t lose their nerve, embarked on “The road to infinite QE”. Under these conditions the JPY will decline and the Japanese stock market will rise.

In the long run demographic forces may halt Abenomic attempts to debase the Yen. This 2015 paper from the Federal Reserve Bank of St Louis – Aging and the Economy: The Japanese Experience – makes fascinating reading. Here is a snippet, but I urge you to read the whole article for an overview of the impact of an ageing population on economies in general, Japan exhibits some unique characteristics in this respect:-

In a third study, economists Derek Anderson, Dennis Botman and Ben Hunt found that the increased number of pensioners in Japan led to a sell-off of financial assets by retirees, who needed the money to cover expenses. The assets were mostly invested in foreign bonds and stocks. The sell-off, in turn, fueled appreciation of the yen, lowering costs of imports and leading to deflation.

Returning to the current environment, on Monday, in a speech to business leaders in Osaka entitled – Japan’s Economy and Monetary Policy – BoJ Governor Haruhiko Kuroda made several observations about the economy, labour market and inflation:-

The economy is expanding moderately, and the real GDP growth rate for the April-June quarter registered a firm increase of 2.5 percent on an annualized basis. It is the first time in eleven years, since 2006, that it has continued to mark positive growth for six consecutive quarters…

The year-on-year rate of increase in hourly wages of part-time employees, which are particularly sensitive to the tightening of the labor market, has registered about 2.5 percent. This is higher than that of full-time employees, implying that the difference in wage levels between part-time and full-time employees has become smaller…

In the labor market as a whole, the unemployment rate has declined to around 3 percent, which is equivalent to virtually full employment, and the active job openings-to-applicants ratio stands at 1.52, exceeding the highest figure during the bubble period and reaching a level last seen as far back as in 1974…

The year-on-year rate of change in the consumer price index (CPI) excluding fresh food has increased to around 0.5 percent recently, but that which also excludes the effects of a rise in energy prices has been relatively weak, remaining at around 0 percent…

Kuroda-san went on to defend the BoJ 2% inflation target and explain the logic behind their ‘QQE with Yield Curve Control’ mechanism. I am struck by the improving affluence of the average worker in Japan. Inflation is zero whilst wage growth, except for the dip in July to -0.3%, has been positive for most of this decade. Real Japanese wages have been rising which is in stark contrast to many of its G7 peers. See Pew Research – For most workers, real wages have barely budged for decades for more on this subject.

The minutes of the July 19th/20th BoJ – Monetary Policy Meeting – were released on Tuesday. They left policy unchanged. The short-term interest rate target at -0.10% and the long-term rate (10yr JGB yield) at around zero. Commenting on the economy they noted continued solid investment, especially by larger firms and the sustained improvement in private consumption. The consumption activity index (CAI) for Q1 2017 showed a fourth consecutive quarterly increase. I was interested in the statement highlighted below (the emphasis is mine):-

…members shared the view that, with corporate profits improving, which mainly reflected the growth in overseas economies, business fixed investment plans were becoming solid on the whole. They also shared the recognition that the employment and income situation had improved steadily and private consumption had increased its resilience. Members then concurred that a positive output gap had taken hold, given the recent tightening of labor market conditions and the increase in capacity utilization rates, with the latter reflecting a rise in production. Based on this discussion, they agreed to revise the Bank’s economic assessment upward to one stating that Japan’s economy “is expanding moderately, with a virtuous cycle from income to spending operating” from the previous one stating that the economy “has been turning toward a moderate expansion.” One member pointed out that Japan’s economy was shifting from a recovery dependent on external demand to a more self-sustaining expansion brought about by an improvement in domestic demand. This member continued that it was also becoming evident that improvements in economic activity had been spreading across a wider range of areas, urban to regional.

The current QQE policies were reconfirmed (emphasis mine):-

With regard to the amount of JGBs to be purchased, it would conduct purchases at more or less the current pace — an annual pace of increase in the amount outstanding of its JGB holdings of about 80 trillion yen — aiming to achieve the target level of the long-term interest rate specified by the guideline.

With regard to asset purchases other than JGB purchases, many members shared the recognition that it was appropriate for the Bank to implement the following guideline for the intermeeting period. First, it would purchase exchange-traded funds (ETFs) and Japan real estate investment trusts (J-REITs) so that their amounts outstanding would increase at annual paces of about 6 trillion yen and about 90 billion yen, respectively. Second, as for CP and corporate bonds, it would maintain their amounts outstanding at about 2.2 trillion yen and about 3.2 trillion yen, respectively.

An independent summation of the current environment and the prospects for the Japanese economy comes from an article by Kazumasa Iwata – President of the Japan Center for Economic Research – AJISS – The Future of the Japanese Economy: The Great Convergence and Two Great Unwindings:-

Since bottoming out in November 2012, the Japanese economy has been in an expansionary phase that reached its 58th month in September of this year. Although not yet as long as the economic expansion achieved during the Koizumi reforms (73 months), the current phase exceeded the mark set by the Izanagi boom of the late 1960s (57 months). While this phase is technically termed expansionary, it lacks strength. In contrast to the average growth rate of 1.8% seen during the Koizumi reforms, the average rate in the ongoing expansion has only been about 1%.

The economic strategy underlying Abenomics is to put the Japanese economy on the road to 2% growth. The experiences of the Koizumi reforms demonstrate that it is quite possible to realize 2% growth by implementing an effective growth strategy. This is evidenced by the theory of convergence through technology diffusion. The catch-up attained by China, India and other emerging countries since the 1990s through offshoring and the construction of global value chains has been astounding. Professor Richard Baldwin argues that the start of the Industrial Revolution ushered in an era of Great Divergence for the global economy via technological innovation and capital accumulation in the developed countries and elsewhere, and that from the 1990s we have been in an age of Great Convergence due to rapid drops in information and telecommunications costs.

In contrast to the brisk development enjoyed by emerging countries, Japan has found itself in a two-decade-long period of stagnation, its economy falling far below the convergence line predicted by Convergence Theory…

Japan already failed to boost its productivity during the 1st IT Revolution of the mid-1990s, and it is now in the 2nd IT Revolution, otherwise known as the 4th Industrial Revolution, centered on IoT, AI, and Big Data. OECD research shows that the top 5% frontier companies have not seen a decline in productivity growth since the financial crisis. Other companies lag behind these frontier companies in globalizing and using digital technology (digitalization), which has only widened the productivity gap between them. Were all companies in Japan able to boost their performance on par with the top ten companies utilizing AI and IoT, Japan’s growth rate could be accelerated by 4% (JCER 2017).

It is interesting to note that Iwata-san sees the greatest risk coming from the unwinding of QE by the Federal Reserve and the ECB, combined with the increasingly protectionist stance of US trade policy. He does not appear to expect the BoJ to reverse QQE, nor Abenomics to falter.

Market Impact

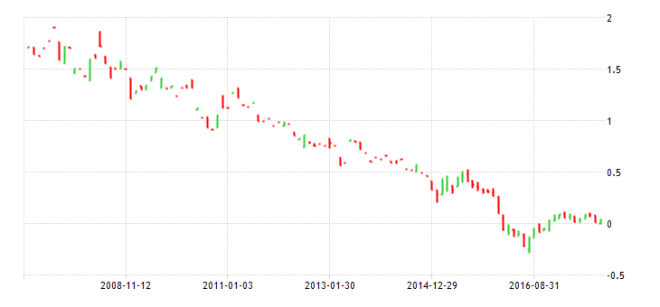

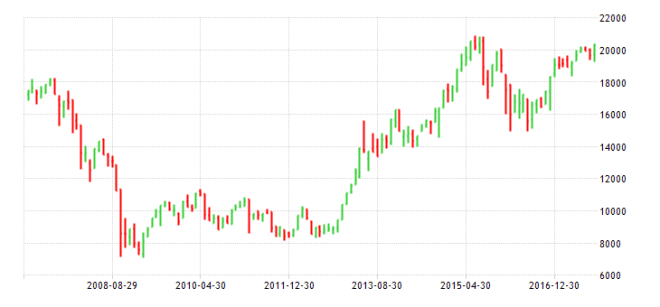

What does the forthcoming election and continuation of infinite QQE mean for Japanese financial markets? Firstly here are three 10 year charts, of the USDJPY, 10yr JGBs and the Nikkei 225:-

Source: Trading Economics

Source: Trading Economics

Source: Trading Economics

The Yen has been trading a range this year; it has strengthened against a generally weakening US$, whilst weakening against a resurgent Euro. 10yr JGBs have been held in an effective straightjacket by ‘Yield curve control’. Meanwhile the Nikkei 225 has followed the lead of other equity markets, both in Asia and the US, and marched steadily higher. A break above the highs of August 2015 would see the index trading at its highest since 1997. A dividend yield of 2% (source: Star Capital – as at 30/6/2017) looks attractive compared to JGBs or inflation, although a P/E ratio of more than 17 times and a CAPE ratio above 26 may be cause for caution.

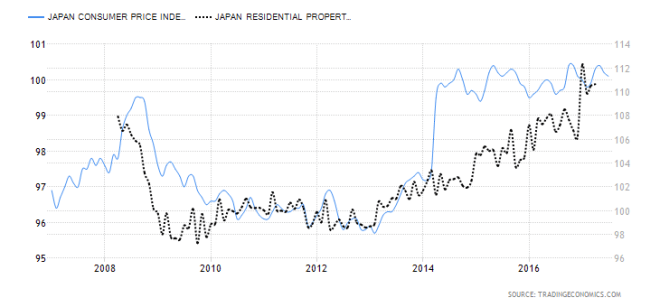

An assessment of financial markets would not be complete without a review of real estate. The BoJ mentioned that house prices have been fairly flat this year. Below is a r chart of the Japan Housing Index and the CPI Index since the financial crisis of 2008:-

Source: Trading Economics, Japan Ministry of Internal Affairs

Real Estate rental yields are currently around 2.5% making property an alternative to stocks for the long term investor. Personally, with dividend yields around 2%, I would want more than 50 basis points to invest in such an illiquid asset: chacun a son gout.

The Geopolitics of North Korea makes Japan vulnerable: Japan’s currency will bear the brunt of this. Given that much of the recent economic growth has been export led, this Yen weakness is unlikely to damage the prospects for the stock market, except perhaps in the short-term.

If Abe wins a convincing mandate on 22nd October, military spending may be added to the mix of public sector stimulus. Pervious consumption tax increases have proved damaging to the nascent economic recovery, this time, dare I say it, might be different. With wages increasing and domestic demand finally beginning to rise, a moderate tax hike maybe achievable, although I still think it more likely that implementation will be deferred.

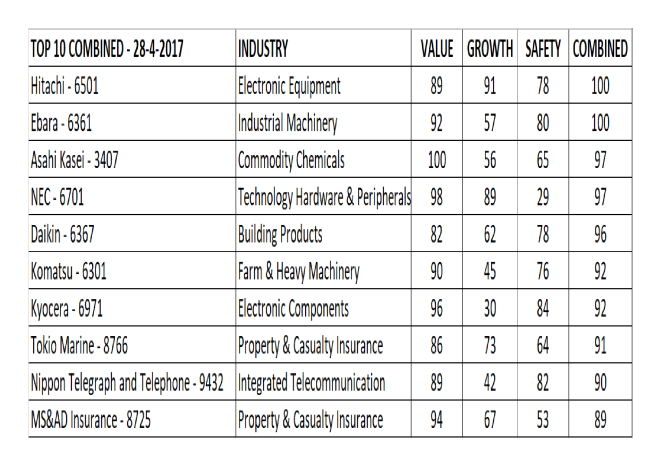

The table below, which shows the top 10 best value stocks in the Nikkei, was calculated on 28th April. It is produced by Obermatt – click on the name to find out more about Obermatt’s excellent range of services and their valuation methodologies:-

Source: Obermatt

To be clear, being a top-down macro investor, I have not personally delved into the relative merits of the stocks above, but I am comforted to note that most of them are household names, even outside Japan. A testament to the quality of many Japanese corporations.

From a technical perspective one should have bought the chart breakout back in November 2016. The market is close to resistance at 21,000 and I would like to see a monthly close above this level before risking additional capital, however, after nearly three decades of deflationary adjustment, the Japanese economy may be beginning to find sustainable growth. I believe this is despite, rather than as a result of, government and central bank policy: but that’s a topic for another time.