![]()

Macro Letter – No 121 – 04-10-2019

Value, Momentum and Carry – Is it time for equity investors to switch?

- Index tracking and growth funds have outperformed value managers for several years

- Last month value was resurgent, but will it last?

- In the long run, value has offered a better risk adjusted return

- The long-term expected return from growth stocks remains hard to assess

Value, momentum and carry are the three principal means of extracting return from any investment. They may be described in other ways but these are really the only games in town. I was reminded of this during the last month as value based equity managers witnessed a resurgence of performance whilst index tracking products generally suffered. Is this a sea-change or merely a case of what goes up must come back down?

My premise over the last few years has been that the influence of central banks, in reducing interest rates to zero or below, has been the overwhelming driver of return for all asset classes. The stellar performance of government bonds has percolated through the credit markets and into stocks. Lower interest rates has also made financing easier, buoying the price of real-estate.

Traditionally, in the equity markets, investment has been allocated to stocks which offer growth or income, yet with interest rates falling everywhere, dividend yields offer as much or more than bonds, making them attractive, however, growth stocks, often entirely bereft of earnings, become more attractive as financing costs approach zero. In this environment, with asset management fees under increasing pressure, it is not surprising to observe fund investors accessing the stock market by the cheapest possible means, namely ETFs and index tracking funds.

During the last month, there was a change in mood within the stock market. Volatility within individual stocks remains relatively high, amid the geo-political and economic uncertainty, but value based active managers saw a relative resurgence, after several years in the wilderness. This may be merely a short-term correction driven more by a rotation out of the top performing stocks, but it could herald a sea-change. The rising tide of ever lower interest rates, which has floated all ships, may not have turned, but it is at the stand, value, rather than momentum, may be the best means of extracting return in the run up to the US presidential elections.

A review of recent market commentary helps to put this idea in perspective. Firstly, there is the case for growth stocks, eloquently argued by Jack Neele at Robeco – Buying cheap is an expensive business: –

One of the most frequent questions I have been asked in recent years concerns valuation. My focus on long-term growth trends in consumer spending and the companies that can benefit from these often leads me to stocks with high absolute and relative valuations. Stocks of companies with sustainability practices that give them a competitive edge, global brand strength and superior growth prospects are rewarded with an above-average price-earnings ratio.

It is only logical that clients ask questions about high valuations. To start with, you have the well-known value effect. This is the principle that, in the long term, value stocks – adjusted for risk – generate better returns that their growth counterparts. Empirical research has been carried out on this, over long periods, and the effect has been observed in both developed and emerging markets. So if investors want to swim against the tide, they need to have good reasons for doing so.

Source: Robeco, MSCI

In addition, there are – understandably – few investors who tell their clients they have the market’s most expensive stocks in their portfolio. Buying cheap stocks is seen as prudent: a sign of due care. However, if we zoom in on the last ten years, there seems to have been a structural change since the financial crisis. Cheap stocks have done much less well and significantly lagged growth stocks.

Source: Robeco, MSCI

Nevertheless, holding expensive stocks is often deemed speculative or reckless. This is partly because in the financial industry the words ‘expensive’ and ‘overvalued’ are often confused, despite their significant differences. There are many investors who have simply discarded Amazon shares as ‘much too expensive’ in the last ten years. But in that same period, Amazon is up more than 2000%. While the stock might have been expensive ten years ago, with hindsight it certainly wasn’t overvalued.

The same applies for ‘cheap’ and ‘undervalued’. Stocks with a low price-earnings ratio, price-to-book ratio or high dividend yield are classified as cheap, but that doesn’t mean they are undervalued. Companies in the oil and gas, telecommunications, automotive, banking or commodities sectors have belonged to this category for decades. But often it is the stocks of these companies that structurally lag the broader market. Cheap, yes. Undervalued, no.

The author goes on to admit that he is a trend follower – although he actually says trend investor – aside from momentum, he makes two other arguments for growth stocks, firstly low interest rates and secondly the continued march of technology, suggesting that investors have become much better at evaluating intangible assets. The trend away from older industries has been in train for many decades but Neele points out that since 1990 the total Industry sector weighting in the S&P Index has fallen from 34.9% to 17.3% whilst Technology has risen from 5.9% to 15.6%.

If the developed world is going to continue ageing and interest rates remain low, technology is, more than ever, the answer to greatest challenges facing mankind. Why, therefore, should one contemplate switching from momentum to value?

A more quantitative approach to the current environment looks at the volatility of individual stocks relative to the main indices. I am indebted to my good friend Allan Rogers for his analysis of the S&P 100 constituents over the past year: –

OEF, the ETF tracking the S&P 100, increased very modestly during the period from 9/21/2018 to 9/20/2019. It rose from 130.47 to 132.60, a gain of 1.63%. During the 52 weeks, it ranged between 104.23 and 134.33, a range of 28.9% during a period where the VIX rarely exceeded 20%. Despite the inclusion of an additional 400 companies, SPY, the ETF tracking the S&P 500, experienced a comparable range of 29.5%, calculated by dividing the 52 week high of 302.63 by the 52 week low of 233.76. SPY rose by 2.2% during that 52 week period. Why is this significant? Before reading on, pause and make your own estimate of the average 52 week range for the individual stocks in the S&P 100. 15%? 25%? The average 52 week price range for the components was 49%. The smallest range was 18%. The largest range was 134%. For a portfolio manager tasked with attempting to generate a return of 7% per annum, the 100 largest company stocks offer potential profit of seven times the target return if one engages in active trading. Credit risk would appear to be de minimus for this group of companies. This phenomenon highlights remarkable inefficiency in stock market liquidity.

This analysis is not in the public domain, however, please contact me if you would like to engage with the author.

This quantitative approach when approaching the broader topic of factor investing – for a primer Robeco – The Essentials of Factor Investing – is an excellent guide. Many commentators discuss value in relation to investment factors. Last month an article by Olivier d’Assier of Axioma – Has the Factor World Gone Mad and Are We on the Brink of Another Quant Crisis? caught my eye, he begins thus: –

To say that fundamental style factor returns have been unusual this past week would be the understatement of the year—the decade, in fact. As reported in yesterday’s blog post “Momentum Nosedives”, Momentum had a greater-than two standard deviation month-to-date negative return in seven of the eleven markets we track. Conversely, Value, which has been underperforming year-to-date everywhere except Australia and emerging markets, has seen a stronger-than two standard deviation month-to-date positive return in four of those markets. The growth factor also saw a sharp reversal of fortune last week in the US, while leverage had a stronger-than two standard deviation positive return in that market on the hopes for more monetary easing by the Fed.

The author goes on to draw parallels with July 2007, reminding us that after a few weeks of chaotic reversals, the factor relationships returned to trend. This time there is a difference, equities in 2007 were not a yield substitute for bonds, today, they are. Put into the context of geopolitical and economic growth concerns, the author expects lower rates and sees the recent correction in bond yields as corrective rather than structural. As for the recent price action, d’Assier believes this is due to unwinding of exposures, combined with short-term traders buying this year’s losing factors, Value and Dividend Yield, and selling winners such as Momentum and Growth. Incidentally, despite the headline, Axioma does not envisage a quant crisis.

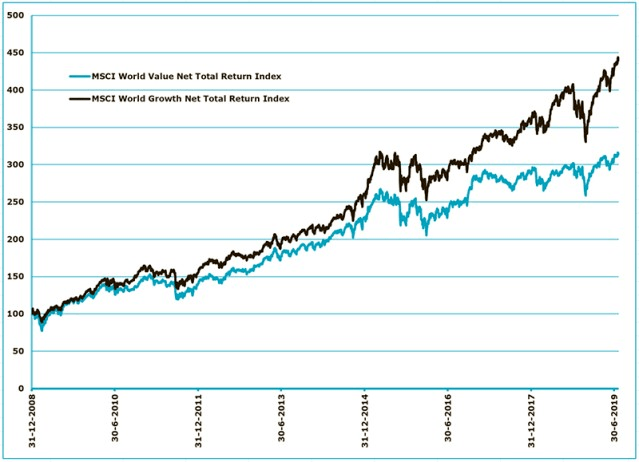

Returning to the broader topic of momentum versus value, a recent article from MSCI – Growth’s recent outperformance was and wasn’t an anomaly – considers whether the last decade represents a structural shift, here is their summary: –

Growth strategies have performed well over the past few years. For investors, an important question is whether the recent performance is an anomaly.

For a growth strategy that simply picks stocks with high growth characteristics, the recent outperformance is out of line with that type of growth strategy’s historical performance.

For a strategy that targets the growth factor while controlling for other factors, the recent outperformance has been in line with its longer historical performance.

The chart below attempts to show the performance of the pure growth factor adjusted for non-growth factors: –

Source: MSCI

If anything, this chart shows a slightly reduced return from pure growth over the last three years. The authors conclude: –

…to answer whether growth’s recent performance is an anomaly really depends on what we mean by growth. If we mean a simple strategy that selects high-growth stocks, then the recent performance is not representative of that strategy’s long-term historical performance. In this case, we can attribute the recent outperformance relative to the long term to non-growth factors and particular sectors — exposure to which has not been as detrimental recently as it has been over the long run. But for a factor- and sector-controlled growth strategy, the performance is mainly driven by exposure to the growth factor. In this case, the recent outperformance has been in line with the longer-term outperformance.

As I read this I am reminded of a quant hedge fund manager with whom I used to do business back in the early part of the century. He had taken a tried a tested fundamental short-selling strategy and built a market neutral, industry neutral, sector neutral portfolio around it, unfortunately, by the time he had hedged away all these risks, the strategy no longer made any return. What we can probably agree upon is that growth stocks have outperformed income and value not simply because they are growth stocks.

The Case for Value

They say that history is written by the winners, nowhere is this truer than in investment management. Investors move in herds, they want what is hot and not what is not. In a paper published last month by PGIM – Value vs. Growth: The New Bubble – the authors’ made several points, below are edited highlights (the emphasis is mine): –

-

We have been through an extraordinary period of value factor underperformance over the last 18 months. The only comparable periods over the last 30 years are the Tech Bubble and the GFC.

-

Historically, we would expect a very sharp reversal of value performance to follow. This was the case in each of the two previous extreme periods.

-

We tested the drivers of recent value underperformance to see if we are in a “value trap.” Historically, fundamentals have somewhat deteriorated, but prices expected a bigger deterioration, so the bounce-back more than offset the fundamental deterioration. In a value trap environment, we would expect a greater deterioration in fundamentals. In the last 18 months, we have actually seen an improvement in fundamental earnings for value stocks, but a deterioration in pricing. This combination is unprecedented, and signals the opposite of a value trap environment.

-

…we examined the behavior of corporate insiders… The relative conviction of insiders regarding cheaper stocks is higher than ever, which reinforces our conviction about the magnitude of the performance opportunity from here.

-

It is never easy to predict what it will take to pop a bubble, but there are multiple scenarios that we envisage as potential catalysts, including both growth and recessionary conditions.

These views echo an August 2019 article by John Pease at GMO – Risk and Premium – A Tale of Value – the author concludes (once again the emphasis is mine): –

Value has underperformed the market in 10 of the last 12 months, including the last 7. Its most recent drawdown began in 2014 and the factor is quite far from its high watermark. The relative return of traditional value has been flat since late 2004. All in all, it has been a harrowing decade for those who have sought cheap stocks, and we have tried to understand why.

We approached this problem by decomposing the factor’s relative returns. The relative growth profile of value has not changed with time; the cheapest half (ex-financials) in the U.S. has continued to undergrow the market, but by no more than what we have come to expect. These companies have also not compromised their quality to keep growth stable, suggesting that any shifts that have occurred in the market have not disproportionately hurt value’s fundamentals.

The offsets to value’s undergrowth, however, have come under pressure. Value’s yield advantage has fallen as the market has become more expensive. The group’s rebalancing – the tendency of cheap companies to see their multiples expand and rotate out of the group while expensive companies see their multiples contract and come into value – is also slower, with behavioral and structural aspects both at play. Though these drivers of relative outperformance have diminished, they still exceed value’s undergrowth by more than 1%, indicating that going forward, cheap stocks (at least as we define them) are likely to reap a decent, albeit smaller, premium.

This premium has not materialized over the last decade for a simple reason: relative valuations. Value has seen its multiples expand a lot less than the market. This makes sense – because value tends to have significantly lower duration than other equities, a broad risk rally shouldn’t be as favorable to cheap stocks as it should be to their expensive counterparts. And we have had quite a rally.

It isn’t possible to guarantee that the next decade will be kinder to value than the previous one was. The odds would seem to favor it, however. Cheap stocks still provide investors with a premium, allowing them to outperform even if their relative valuations remain low. If relative valuations rise – not an inconceivable event given a long history of mean-reverting discount rates – the ensuing relative returns will be exceptional. And value, after quite the pause, might look valuable again.

A key point in this analysis is that the low interest rate environment has favoured growth over value. Unless the next decade sees a significant normalisation of interest rates, unlikely given the demographic headwinds, growth will continue to benefit, even as momentum strategies falter due to the inability of interest rates to fall significantly below zero (and that is by no means certain either).

These Macro Letters would not be In the Long Run without taking a broader perspective and this July 2019 paper by Antti Ilmanen, Ronen Israel, Tobias J. Moskowitz, Ashwin Thapar, and Franklin Wan of AQR – Do Factor Premia Vary Over Time? A Century of Evidence – fits the bill. The author examine four factors – value, momentum, carry, and defensive (which is essentially a beta neutral or hedged portfolio). Here are their conclusions (the emphasis is mine): –

A century of data across six diverse asset classes provides a rich laboratory to investigate whether canonical asset pricing factor premia vary over time. We examine this question from three perspectives: statistical identification, economic theory, and conditioning information. We find that return premia for value, momentum, carry, and defensive are robust and significant in every asset class over the last century. We show that these premia vary significantly over time. We consider a number of economic mechanisms that may drive this variation and find that part of the variation is driven by overfitting of the original sample periods, but find no evidence that informed trading has altered these premia. Appealing to a variety of macroeconomic asset pricing theories, and armed with a century of global economic shocks, we test a number of potential sources for this variation and find very little. We fail to find reliable or consistent evidence of macroeconomic, business cycle, tail risks, or sentiment driving variation in factor premia, challenging many proposed dynamic asset pricing theories. Finally, we analyze conditioning information to forecast future returns and construct timing models that show evidence of predictability from valuation spreads and inverse volatility. The predictability is even stronger when we impose theoretical restrictions on the timing model and combine information from multiple predictors. The evidence identifies significant conditional return premia from these asset pricing factors. However, trading profits to an implementable factor timing strategy are disappointing once we account for real-world implementation issues and costs.

Our results have important implications for asset pricing theory, shedding light on the existence of conditional premia associated with prominent asset pricing factors across many asset classes. The same asset pricing factors that capture unconditional expected returns also seem to explain conditional expected returns, suggesting that the unconditional and conditional stochastic discount factors may not be that different. The lack of explanatory power for macroeconomic models of asset pricing challenges their usefulness in describing the key empirical factors that describe asset price dynamics. However, imposing economic restrictions on multiple pieces of conditioning information better extracts conditional premia from the data. These results offer new features for future asset pricing models to accommodate.

This paper suggests that, in the long run, broad asset risk premia drive returns in a consistent manner. Macroeconomic and business cycle models, which attempt to forecast asset values based on expectations for economic growth, have a lower predictive value.

Conclusions and investment opportunities

I have often read market commentators railing against the market, complaining that asset prices ignored the economic fundamentals, the research from AQR offers a new insight into what drives asset returns over an extended time horizon. Whilst this does not make macroeconomic analysis obsolete it helps to highlight the paramount importance of factor premia in forecasting asset returns.

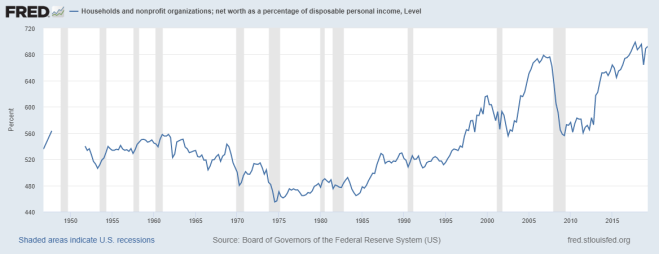

Returning to the main thrust of this latter, is this the time to switch from momentum to value? I think the jury is still out, although, as the chart below illustrates, we are near an all-time high for the ratio between net worth and disposable income per person in the US: –

Source: Federal Reserve

This is a cause for concern, it points to severe imbalances within households: it is also a measure of rising income inequality. That stated, many indicators are at unusual levels due to the historically low interest rate environment. Investment flows have been the principal driver of asset returns since the great recession, however, now that central bank interest rates in the majority of developed economies are near zero, it is difficult for investors to envisage a dramatic move into negative territory. Fear about an economic slowdown will see risk free government bond yields become more negative, but the longer-term driver of equity market return is no longer solely based on interest rate expectations. A more defensive approach to equities is likely to be seen if a global recession is immanent. Whether growth stocks prove resurgent or falter in the near-term, technology stocks will continue to gain relative to old economy companies, human ingenuity will continue to benefit mankind. Creative destruction, where inefficient enterprises are replaced by new efficient ones, is occurring despite attempts by central banks to slow its progress.

For the present I remain long the index, I continue to favour momentum over value, but, as was the case when I published – Macro Letter – No 93 back in March 2018, I am tempted to reduce exposure or switch to a value based approach, even at the risk of losing out, but then I remember the words of Ryan Shea in his article Artificial Stupidity: –

…investment success depends upon behaving like the rest of the crowd almost all of the time. Acting rational when everyone else is irrational is a losing trading strategy because market prices are determined by the collective interaction of all participants.

For the active portfolio manager, value factors may offer a better risk reward profile, but, given the individual stock volatility dispersion, a market neutral defensive factor model, along the lines proposed by AQR, may deliver the best risk adjusted return of all.