![]()

Macro Letter – No 120 – 13-09-2019

Uncertainty and the countdown to the US presidential elections

- JP Morgan analyse the impact of 14,000 presidential Tweets

- Gold breaks out to the upside despite US$ strength

- China backs down slightly over Hong Kong

- Trump berates Fed Chair and China

These are just a few of the news stories which drove financial markets during the summer: –

VOX – The Volfefe Index, Wall Street’s new way to measure the effects of Trump tweets, explained

DailyFX – Gold Prices Continue to Exhibit Strength Despite the US Dollar Breakout

BBC – Carrie Lam: Hong Kong extradition bill withdrawal backed by China

FT – Trump lashes out at China and US Federal Reserve — as it happened.

For financial markets it is a time of heightened uncertainty. The first two articles are provide a commentary on the way markets are evolving. The impact of social media is rising, with Trump in the vanguard. Geopolitical uncertainty and the prospect of fiscal debasement are, meanwhile, upsetting the normally inverse relationship between the price of gold and the US$.

The next two items are more market specific. The stand-off between the Chinese administration and the people of the semi-autonomous enclave of Hong Kong, prompts concern about the political stability of China, meanwhile the US Commander in Chief persists in undermining the credibility of the notionally independent Federal Reserve and seems unable to resist antagonising the Chinese administration as he raises the stakes in the Sino-US trade war. Financial markets have been understandably unsettled.

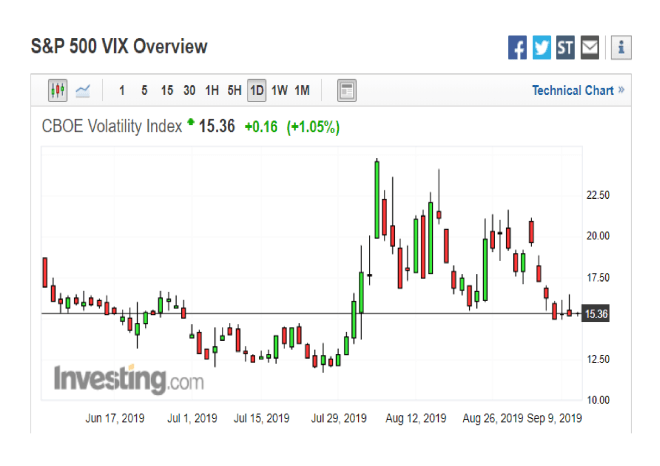

Ironically, despite the developments high-lighted above, during August, US bonds witnessed sharp reversals lower, suggesting that geopolitical tensions might have moderated. Since the beginning of September prices have rebounded, perhaps there were simply more sellers than buyers last month. In Europe, by contrast, German bunds reached new all-time highs, only to suffer sharp reversal in the past week. Equity markets responded to the political uncertainty in a more consistent manner, plunging and then recovering during the past month. As the chart below illustrates, there has been increasing debate about the challenge of increased volatility since the end of July: –

Source: Investing.com

Yet, as always, it is not the volatility or even risk which presents a challenge to financial market operators, it is uncertainty. Volatility is a measure derived from the mean and variance of a price. It is a cornerstone of the measurement of financial risk: the key point is that it is measurable. Risk is something we can measure, uncertainty is that which we cannot. This is not a new observation, it was first made in 1921 by Frank Knight – Risk, Uncertainty and Profit.

Returning to the current state of the financial markets, we are witnessing a gradual erosion of belief in the omnipotence of central banks. See Macro Letter’s 48, 79 and 94 for some of my previous views. What has changed? As Keynes might have put it, ‘The facts.’ Central Banks, most notably the Bank of Japan, Swiss National Bank and European Central Bank, have been using zero or negative interest rate policy, in conjunction with balance sheet expansion, in a valiant attempt to stimulate aggregate demand. The experiment has been moderately successful, but the economy, rather like a chronic drug addict, requires an ever increasing fix to reach the same high.

In Macro Letter – No 114 – 10-05-2019 – Debasing the Baseless – Modern Monetary Theory – I discussed the latest scientific justification for debasement. My conclusion: –

The radical ideas contained in MMT are unlikely to be adopted in full, but the idea that fiscal expansion is non-inflationary provides succour to profligate politicians of all stripes. Come the next hint of recession, central banks will embark on even more pronounced quantitative and qualitative easing, safe in the knowledge that, should they fail to reignite their economies, government mandated fiscal expansion will come to their aid. Long-term bond yields will head towards the zero-bound – some are there already. Debt to GDP ratios will no longer trouble finance ministers. If stocks decline, central banks will acquire them: and, in the process, the means of production. This will be justified as the provision of permanent capital. Bonds will rise, stocks will rise, real estate will rise. There will be no inflation, except in the price of assets.

As this recent article from the Federal Reserve Bank of San Francisco – Negative Interest Rates and Inflation Expectations in Japan – indicates, even central bankers are beginning to doubt the efficacy of zero or negative interest rates, albeit, these comments emanate from the FRBSF research department rather than the president’s office. If the official narrative, about the efficacy of zero/negative interest rate policy, is beginning to change, state sponsored fiscal stimulus will have to increase dramatically to fill the vacuum. The methadone of zero rates and almost infinite credit will be difficult to quickly replace, I anticipate widespread financial market dislocation on the road to fiscal nirvana.

In the short run, we are entering a period of transition. Trump may continue to berate the chairman of the Federal Reserve and China, but his room for manoeuvre is limited. He needs Mr Market on his side to win the next election. For Europe and Japan the options are even more constrained. Come the next crisis, I anticipate widespread central bank buying of stocks (in addition to government and corporate bonds) in order to provide liquidity and insure economic stability. The rest of the task will fall to the governments. Non-inflationary fiscal profligacy will be de rigueur – I can see the politicians smiling all the way to the hustings, safe in the knowledge that deflationary forces have awarded them a free-lunch. Someone, someday, will have to pay, of course, but they will be long since retired from public office.

Conclusions and Investment Opportunities

During the next year, markets will continue to gyrate erratically, driven by the politics of European budgets, Brexit and the Sino-US trade war. These issues will be eclipsed by the twittering of Donald Trump as he seeks to win a second term in office. Looked at cynically, one might argue that Trump’s foreign policy has been deliberately engineered to slow the US economy and hold back the stock market. During the next 14 months, a new nuclear weapons agreement could be forged with Iran, relations with North Korea improved and a trade deal negotiated with China. Whether this geopolitical largesse is truly in the President’s gift remains unclear, but for a maker of deals such as Mr Trump, the prospect must be tantalising.

For the US$, the countdown to the US election remains positive, for stocks, likewise. For the bond market, the next year may be broadly neutral, but given the signs of faltering growth across the globe, it seems unlikely that yields will rise significantly. Economies will see growth slow, leading to an accelerated pace of debt issuance. Bouts of volatility, similar to August or Q4 2018, will become more commonplace. I remain bullish for asset markets, nonetheless.