Macro Letter – No 43 – 09-10-2015

Brazil – Good buy or Goodbye?

- The Bovespa is down 35% in US$ terms this year

- Government bond yields are back to levels last seen during the crisis of 2009

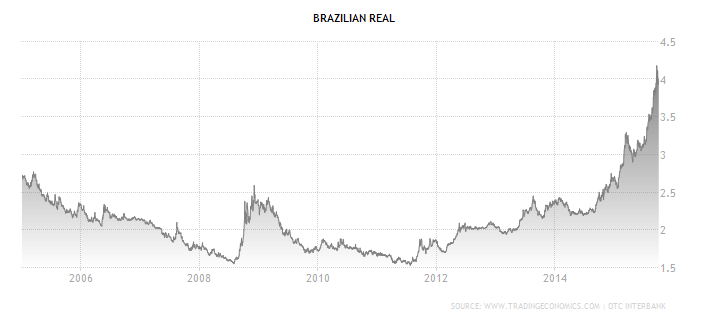

- The BRL has declined by 45% against the US$ during 2015

- Bond agency downgrades and government inaction exacerbate the sense of crisis

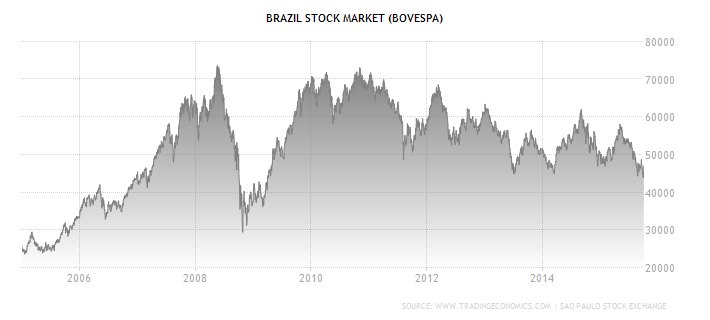

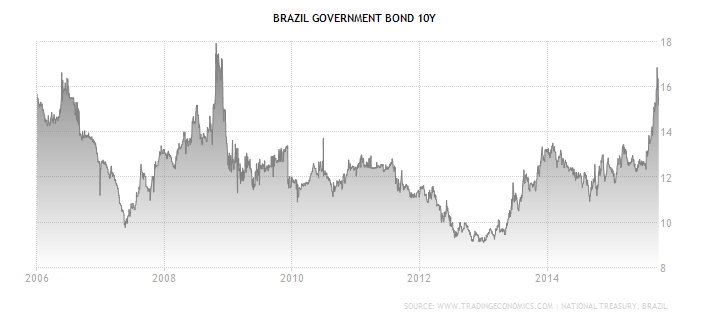

When I last gave a speech about the Brazilian economy and stock market prospects, back in March 2014, I was optimistic. During the summer of that year the Bovespa rallied, USDBRL improved and Brazilian government bond yields declined, but by early September these nascent trends had lost momentum. The table lower shows the evolution:-

| Market | 28-Mar | 29-Aug | 28-Dec | 05-Oct |

| Bovespa | 50415 | 61288 | 48512 | 47033 |

| 10yr Bond | 12.8 | 11.21 | 12.33 | 15.23 |

| USDBRL | 2.27 | 2.23 | 2.69 | 3.92 |

Source: Investing.com

The charts below show these markets over the last 10 years:-

Source: Trading Economics

Source: Trading Economics

Source: Trading Economics

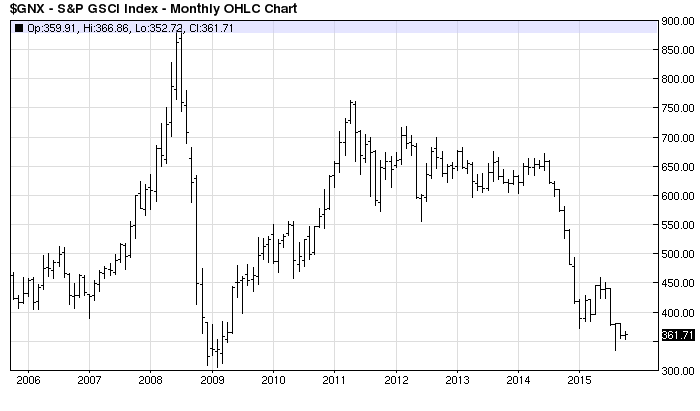

For good measure, and since Brazil’s economy is sensitive to the price of commodities here is the Goldman Sachs Commodity Index over the same period:-

Source:Barchart.com

It is worth remembering that, despite the importance of commodities – and Coffee made fresh lows for the year in September – the largest contributor to Brazilian GDP is services (67%).

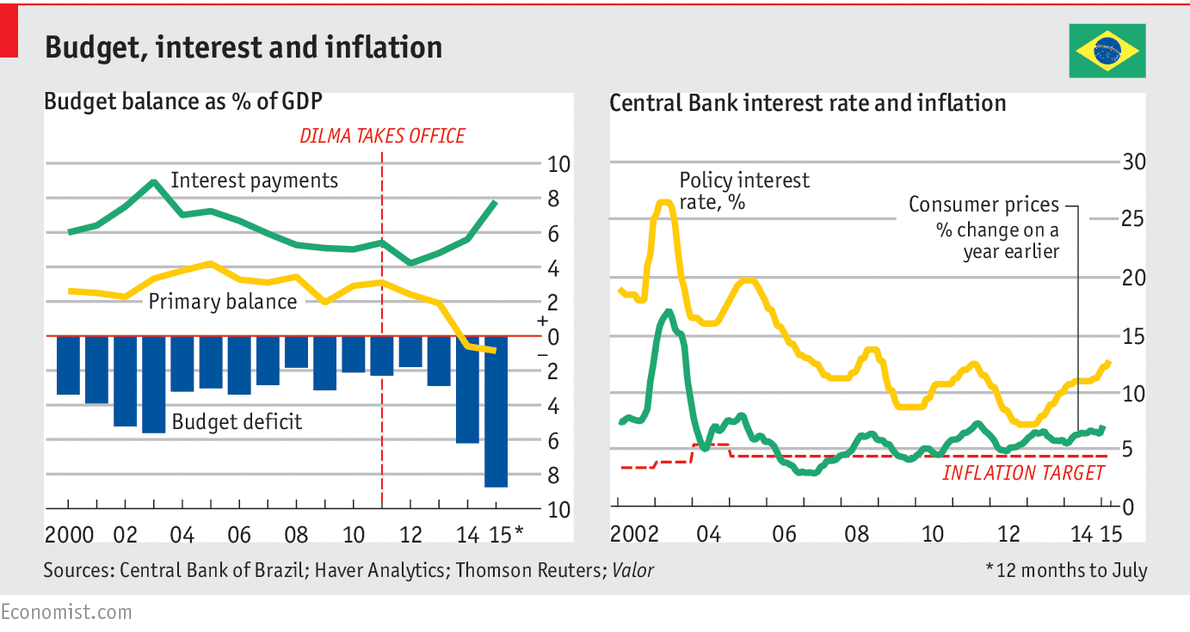

During the second half of 2014, inflation remained broadly stable at around 6.75%, but, as the BRL weakened, inflation picked up sharply forcing the Bank of Brazil to raise interest rates, meanwhile the government primary budget surplus evaporated:-

Source: Economist

This 2nd September Economist article – Brazilian waxing and waning – sums up the range of negative forces besetting the Brazilian economy:-

In the past few years Brazil’s economy has disappointed. It grew by 2.2% a year, on average, during President Dilma Rousseff’s first term in office in 2011-14, a slower rate of growth than in most of its neighbours, let alone in places like China or India. Last year GDP barely grew at all. It contracted by 1.6% in the first quarter, compared to the same period last year, and is expected to shrink by as much as 2% in 2015. Household consumption registered the first drop, year-on-year, since Ms Rousseff’s left-wing Workers’ Party (PT) came to power in 2003. At the same time, public spending has surged. In 2014, as Ms Rousseff sought re-election, the budget deficit doubled to 6.75% of GDP. For the first time since 1997 the government failed to set aside any money to pay back creditors. Its planned primary surplus, which excludes interest owed on debt, of 1.8% of GDP ended up being a 0.6% deficit. Brazil’s gross government debt of 62% may look piffling compared to Greece’s 175% or Japan’s 227%. But Brazil’s high interest rates of around 13% make borrowing costlier to service.

…As the government loosened fiscal policy, the Central Bank prematurely slashed its benchmark interest rate in 2011-12. This pushed up inflation, which is now above the bank’s self-imposed upper limit of 6.5%, and way above its 4.5% target. The interest-rate cut has since been reversed. On June 3rd the Bank’s monetary policy-makers raised the rate once more, boosting it to 13.75%, more than a percentage point higher than before the decision to cut.

…In the past ten years wages in the private sector have grown faster than GDP (public-sector workers have done even better). That allowed consumers to borrow more, which encouraged still more spending. Now the virtuous circle is turning vicious. Real wages have been falling since March, compared to a year earlier, mainly because Brazilian workers’ productivity never justified the earlier rises.

…unemployment, which has long been falling and dipped below 5% for most of 2014, increased to 6.4% in April. Economists expect it to reach 8% this year.

…the government is cutting spending on unemployment insurance (which had risen even when the jobless rate was falling) and on other benefits. Taxes, including fuel duty, are going up. So, too, are bills for water and electricity.

…Consumer confidence has fallen to its lowest level since Fundação Getulio Vargas, a business school, began tracking it in 2005. The government has no money to boost investment. Petrobras, the state-controlled oil giant and Brazil’s biggest investor, is in the midst of a corruption scandal that has paralysed spending: the forgone investment may reduce GDP growth this year by one percentage point. It is hard to see where growth will come from.

Worst of all, Ms Rousseff’s policy levers are jammed. She cannot loosen fiscal policy without precipitating a downgrade of Brazil’s credit rating. In fact, her hawkish finance minister, Joaquim Levy, has slashed 70 billion reais off the discretionary spending planned for this year (on top of the modest welfare reforms). Nor can the Central Bank ease monetary policy. That would once again undermine its credibility—and weaken the currency. A depreciating real, which is oscillating around a 10-year low, pushes up inflation; it also makes Brazil’s $230 billion dollar-denominated debt dearer by the day.

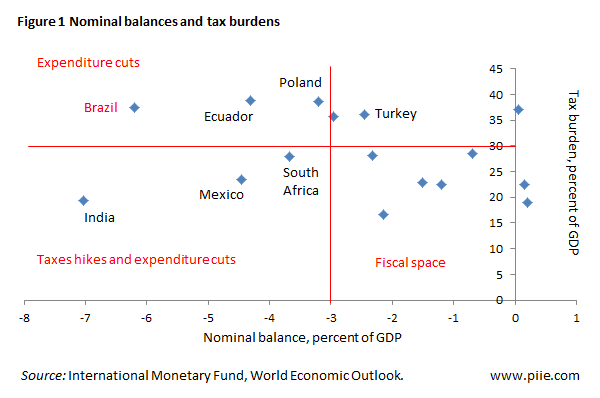

This chart, courtesy of the Peterson Institute, highlights the relative predicament facing Brazil’s government:-

Source: IMF

On September 9th – one week after the Economist article was published – S&P cut Brazil’s bond rating to BB+ – this is “Junk Bond” status. It followed Moody’s downgrade to Baa3 on August 11th. There seems little reason to “Buy Brazil”, but it is when markets look most dire that one should pay the most attention.

In May 2015 I wrote about the prospects for Brazil and Russia here – once again, I was anticipating the rebound in commodity prices coming to the aid of these commodity exporters – yet again, I was premature. The economic slowdown in China continues, commodity exporting countries remain under pressure and, from a technical perspective, the GSCI appears to be heading back to test the 2009 lows.

My conclusions about Brazilian Real-Estate have become slightly more negative since May. The recent increase in domestic inflation, combined with a rise in unemployment, makes rental yields – ranging from 4 to 6% – less attractive. Real yields have grown more negative whilst rental arrears and defaults rise.

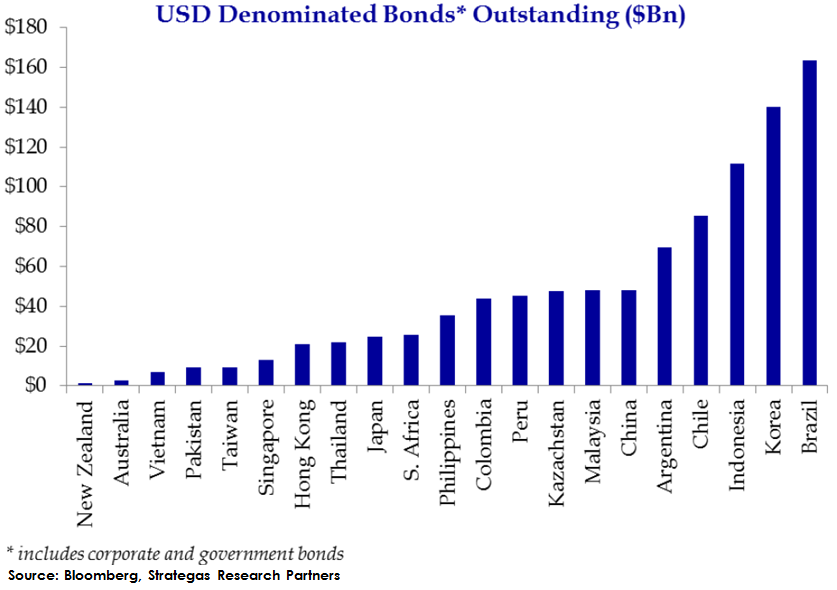

Government bonds also lack their previous allure; short term rates rose again from 13.75% to 14.25% at the end of July. Back in March 2014 the SELIC rate was 10.75% whilst 10yr government bonds yielded 12.80% – 205bp of positive carry. Today the yield pick-up is worth a mere 48bp. My analysis of value, back in May, was based on the expectation that the currency had weakened sufficiently and commodity markets were forming a bottom – both these expectations proved erroneous. Since the currency has weakened further, corporate bonds are likely to come under additional pressure due to the large outstanding US$ issuance:-

Source: Bloomberg and Strategas Research Partners

The IMF – May 2015 Brazil – selected report 15/122 – suggests that the situation is not quite so dire as the table above suggests, nonetheless, I would expect to see a rise in the number of high-profile defaults over the coming months:-

Petrobras accounts for some 13.5 percent of total NFC FX debt. It hedged 70 percent of its FX exposure through both domestic and global derivative markets despite ample FX income.9

Other exporting companies account for 36 percent of FX debt.

Non-exporting companies with at least 80 percent of their FX debt hedged in domestic derivatives markets account for 17 percent of FX debt.

Non-exporting companies (both foreign-owned and domestic firms) with hedge for less than 80 percent of their exposures account for 33.5 percent of NFC FX debt,10 or about 10 percent of total debt (Financial Stability Report, September 2014).

The solitary ray of hope has been the Bovespa, it is substantially lower than in May though not far from where it ended 2014. The table below looks at the CAPE – Cyclically Adjusted Price Earnings Ratio, PE, PC – Price to Cashflow, PB – Price to Book, PS – Price to Sales and DY – Dividend Yield:-

| Country | CAPE | PE | PC | PB | PS | DY |

| Russia | 4.8 | 8.8 | 3.7 | 0.8 | 0.7 | 4.30% |

| Hungary | 7.9 | 23.4 | 4.1 | 1 | 0.5 | 2.50% |

| Brazil | 8.2 | 19.4 | 5.8 | 1.3 | 1.1 | 3.70% |

| Poland | 10.3 | 14.1 | 9.5 | 1.3 | 0.8 | 3.40% |

| Turkey | 10.3 | 11 | 8 | 1.4 | 1 | 3.40% |

| Czech | 10.7 | 14.3 | 6.2 | 1.4 | 1.1 | 6.10% |

| Korea (South) | 12.2 | 12.9 | 6.3 | 1 | 0.6 | 1.40% |

| China | 13.8 | 6.2 | 4.1 | 0.9 | 0.6 | 4.90% |

| Malaysia | 15.6 | 16.1 | 10.8 | 1.7 | 1.9 | 3.40% |

| Thailand | 15.7 | 17 | 10 | 2 | 0.9 | 3.20% |

| Indonesia | 17 | 17.9 | 12.3 | 3.1 | 2.2 | 2.60% |

| Israel | 17.4 | 16.5 | 11.1 | 1.8 | 1.4 | 2.80% |

| Taiwan | 17.8 | 11.5 | 7.3 | 1.7 | 0.9 | 4.10% |

| India | 18.5 | 21.5 | 13.7 | 2.6 | 1.5 | 1.50% |

| South Africa | 19.2 | 14.6 | 8.5 | 2.2 | 1.3 | 3.60% |

| Mexico | 21.2 | 26.9 | 11.9 | 2.6 | 1.5 | 1.90% |

| Philippines | 22.3 | 19.5 | 12.7 | 2.4 | 2 | 1.90% |

Source: Starcapital.de

I’ve ranked these markets by CAPE to look at valuation from a longer-term perspective. Remember, however, the Bovespa index has only a 14% exposure to Energy and 14% to Commodities; domestic consumption will drive growth for many Brazilian companies – the consumer is likely to be in cyclical retreat as wages and benefits fall. Exporters should thrive due to the currency devaluation but for the broader index these effects will take time to manifest themselves in higher stock prices. My longer-term enthusiasm from May remains undimmed, but I was clearly too early calling the bottom. With China still slowing, the headwinds facing Brazil have yet to fully abate.

Emerging markets in general, are under pressure. Back in January 2014 the World Bank Global Economic Prospects stated:-

…if markets react sharply to the continued tapering, then capital flows to developing countries could decrease by as much as 80 percent, destabilizing current account balances, leading to disorderly depreciations of regional currencies, and quite possibly, increasing imported inflation.

They estimated that 60% of all capital flows to emerging markets, since the financial crisis, have been a by-product of QE.

The IMF – WEO – Financial Stability Report – October 2015 – reviews the situation:-

Corporate debt in emerging market economies has risen significantly during the past decade. The corporate debt of nonfinancial firms across major emerging market economies increased from about $4 trillion in 2004 to well over $18 trillion in 2014. The average emerging market corporate debt-to-GDP ratio has also grown by 26 percentage points in the same period, but with notable heterogeneity across countries.

EM Debt to GDP now stands at roughly 70%.

The Institute of International Finance estimate that investors sold $40bln of EM assets during Q3 2015. Brazil topped their list for asset outflows in Q3 – a 27% decline – closely followed by Indonesia and China:-

The marked decline in EM bond and equity in fund allocations amounted to some 80% of the drop seen during the worst of the taper tantrum in Q2 2013. This has left fund allocations to EM bonds and equities nearly 1.5 percentage points below end-June levels–at just 11%, EM allocations are at their lowest since early 2009. The decline in global investors’ appetite for emerging market stocks has been particularly striking, with EM equity funds suffering more than EM bond funds. Large fund outflows, falling asset prices and marked losses in EM currencies against the U.S. dollar have all contributed to lower allocations.

The IIF go on to state that this year EM countries will witness a capital outflow of $541bln for 2015 vs a net inflow of $32bln for 2014. These are the first EM outflows since 1988.

No way out?

In a recent Bloomberg Op-Ed – The Anatomy of Brazil’s Financial Meltdown – Mohamed El-Erian proposes official “Circuit-Breakers” to stop the vicious cycle. Peterson Institute – A Non-Circuit Breaker Agenda for Brazil – disagree:-

What are the options for Brazil? With interest rates at 14.25 percent, there is unfortunately little room for further rate hikes. With short-term domestic rates at these levels and global interest rates at close to zero, one would be hard pressed to argue that remedies used in the 1990s—specifically abrupt interest rate hikes of a high order of magnitude—would make a big impact on reversing capital outflows. If market pressures continue unabated and exchange interventions are ineffective, Brazil might well need to resort to capital controls. A further credit downgrade might follow, and the stage would be set for the type of inevitable crash that many economists imagined they would no longer see. While a crisis cannot be fully avoided—arguably, it is already happening—the government could still take some action to instill confidence. A strong commitment to prudent fiscal management over the medium term might help attenuate market turbulence even if the government’s hands are tied in the short run by political dysfunction. Instituting debt limits as discussed above would be a good start; Poland’s experience is testament to how fiscal credibility can be enhanced through their adoption. In Brazil’s case, debt limits have an additional advantage: They would send the right medium-term signals without being as overtly unpopular as the other measures and reforms the country desperately needs.

“Circuit-Breaker” policy proposals and the spectre of capital controls are unlikely to stem capital flight in the near-term, but with EM exposures already back to 2009 levels, I believe we’re nearer the end than the beginning of the repatriation process.

Conclusions and Investment Opportunities

For investment to return to Brazil, repatriation of existing investment needs to run its course, corporate bond defaults need to peak and begin to improve, unemployment needs to rise and then begin to decline and the government needs to prove it has the resolve to adhere to a policy of real austerity.

Currency

The BRL is the weakest it has been in more than 20 years, it last approached these levels back in October 2002. Foreign Exchange reserves remain high, I would expect the markets to test the central bank’s resolve. Further currency weakness certainly cannot be ruled out.

Bonds

The full impact of recent currency weakness on Brazilian US$ denominated bonds has yet to run its course. Default rates should rise, the Serasa Experian Corporate Default Index rose 13.3% in the period January to August 2015, meanwhile, corporate delinquencies for the month were 16.1% higher than in August 2014.

Stocks

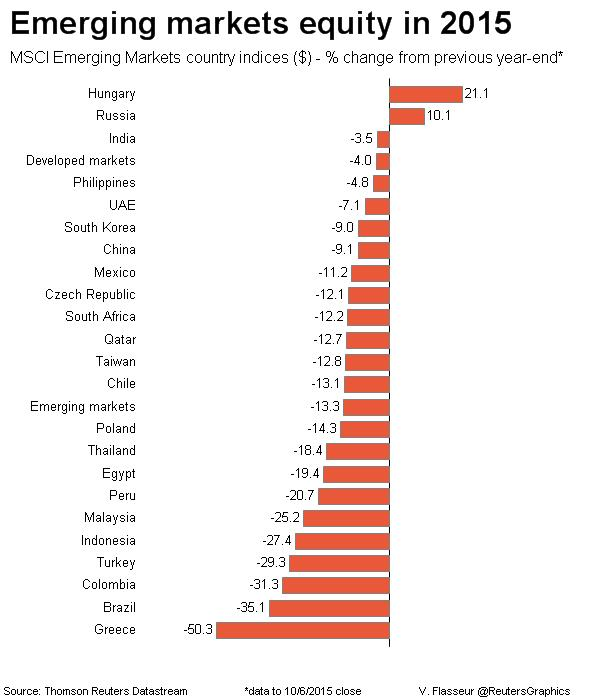

According to Blackrock investors outflows from EM ETFs in September exceeded $3.2bln, albeit, sentiment has improved over the past week. The chart below shows EM stock market performance for the year to 6th October, Brazil has suffered more than every country except Greece:-

Source: Reuters

For the contrarian investor this may present an opportunity to buy – personally, I would prefer to see some indication of government resolve to tackle the countries difficult domestic economic issues first. Next year Brazil will host the Olympic Games – this is an opportunity to push through unpopular policies and showcase all the reasons to invest in Brazil. It is always darkest before the light – I shall be watching closely.