Macro Letter – No 67 – 9-12-2016

Russia – Will the Bear come in from the cold?

- In 2015/16 the Russian economy suffered in the sharpest recession since 2008/09

- The RTSI Stock Index, anticipating a recovery, is up 78% from its January lows

- Russian government bonds traded at 8% in August down from 16% in December 2014

- The Ruble has stabilised after the devaluation of 2014/2015 and inflation is still falling

Since January many emerging equity and bond markets have staged a spectacular recovery. Russia has been among the winners, buoyed by hopes of an end to international sanctions and a, relative, rapprochement with the new US administration. A near-virtuous circle is achieved when combined with the country’s strengthening trade relationship with China and the rising oil price, stemming from the first OPEC production agreement in eight years.

Looking at the RTSI Index, a lot of this favourable news is already in the price:-

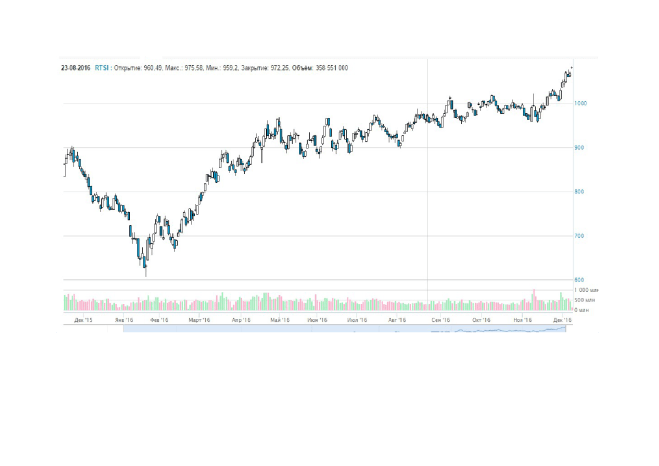

Source: Moscow Exchange

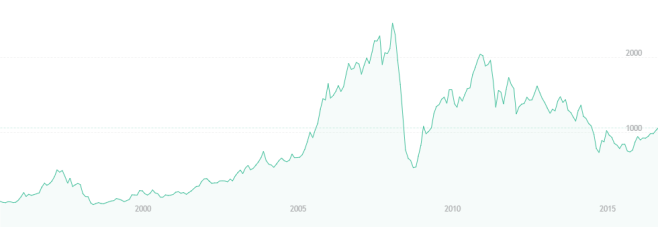

Since January the RTSI has rallied by 78% and, at 1082 is close to the highs of May 2015 (1092) from whence it broke down to the lows of January (607). Is it too late to join the party? A longer-term chart lends perspective:-

Source: Tradingview

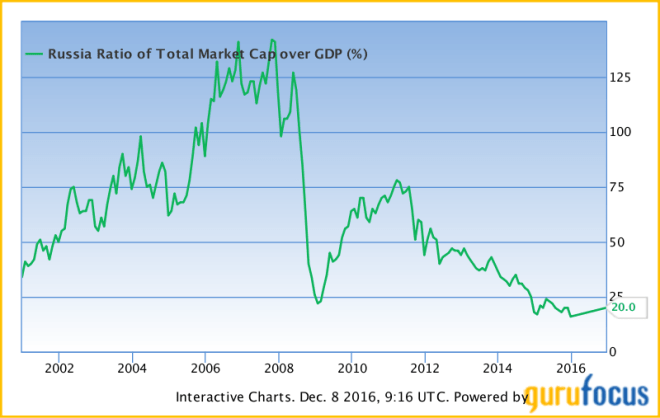

By a number of other metrics Russian stocks still look inexpensive. The chart below compares stock market capitalisation to GDP:-

Source: Guru Focus

The current ratio is 20%, the average over the period since 2000 is 65% – return to mean would imply a 19.25% annual return for Russian stocks over the next eight years. That would equate to a compound return of 409%.

The table below shows the P/E Ratios of four Russian ETFs as of 8th December:-

| Symbol | Name | P/E Ratio |

| RSXJ | VanEck Vectors Russia Small-Cap ETF | 6.07 |

| ERUS | iShares MSCI Russia Capped ETF | 7.33 |

| RBL | SPDR S&P Russia ETF | 7.72 |

| RSX | VanEck Vectors Russia ETF | 8.73 |

Source: EFTdb.com

For comparison, the iShares MSCI BRIC ETF (BKF) currently trades on a PE of 10 times.

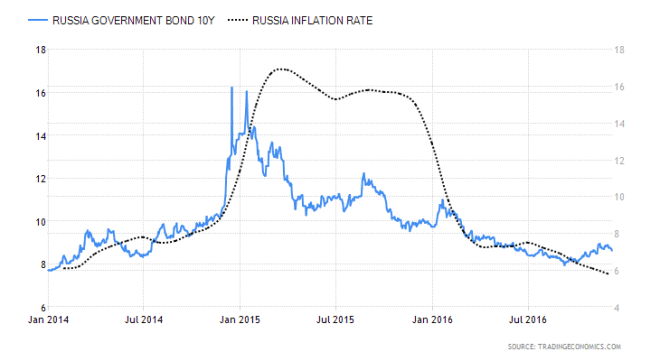

Bonds, Inflation and the Ruble

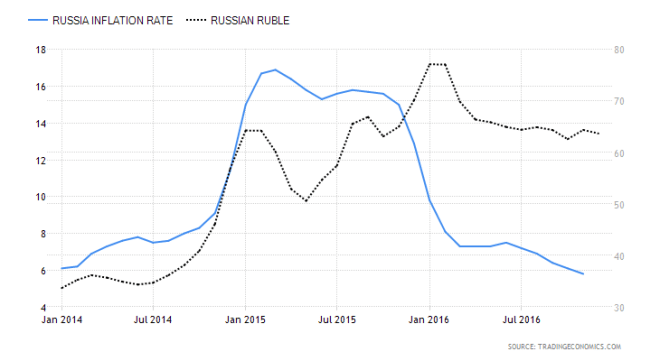

Russian inflation has been declining rapidly this year as the sharp devaluation of 2014/2015 feeds through. The two charts below shows the USDRUB (black – RHS) and Russian CPI (blue – LHS) and Russian 10 year Government bonds (blue – LHS) versus CPI (black – RHS):-

Source: Trading Economics

Source: Trading Economics

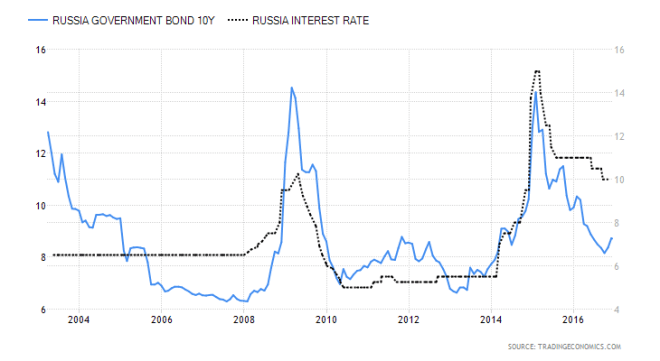

Whilst the Ruble has stabilised at a structurally higher level than prior to the annexation of the Crimea, the inflation rate has been brought back under control by the hawkish endeavours of the Central Bank of Russia. The benchmark one-week repo rate remains at 10%, down from 17% in December 2014 but still well above the rate of inflation – which the Central Bank of Russia forecast to fall to 4% by the end of next year. The yield curve remains inverted but that has not always been a structural feature of the Russian market. The chart below compares the one week repo rate (black – RHS) versus 10yr Government bonds (blue – LHS):-

Source: Trading Economics

Economics and Politics

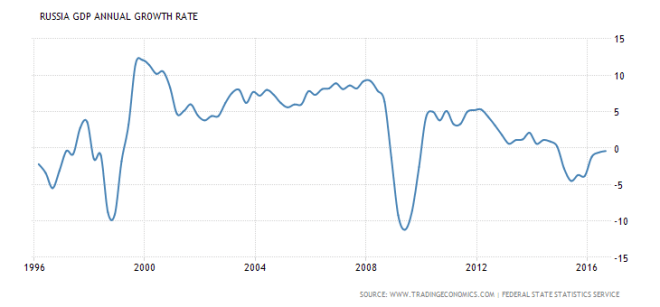

The IMF WEO – October 2016 revised its GDP forecast for Russia in 2017 to +1.1% (versus +0.1% in July) although they revised their 2016 estimate to -0.8% from +0.4%. Focus Economics poll of analysts, forecast 1.2%, whilst Fathom Consulting’s Global Economic Strategic asset Allocation Model (GESAM) is predicting +0.8. Between 1996 and 2016 the average rate of GDP growth was 3.08%. As the chart below shows, the growth rate has been volatile and, like many countries globally, the post 2008/2009 period has been more subdued:-

Source: Trading Economics, Federal Statistics Service

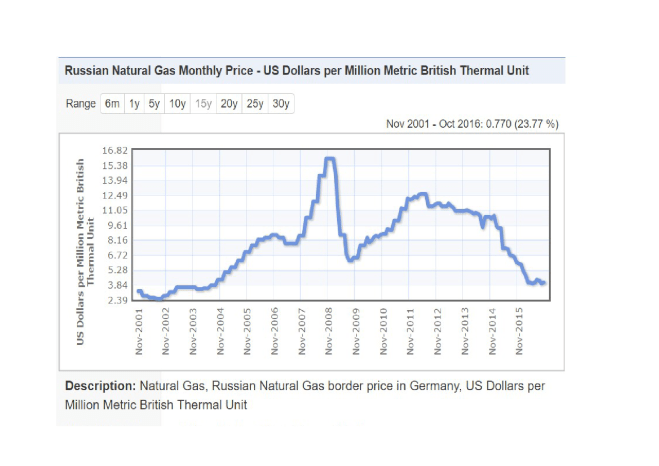

Oil and Gas

Russia’s largest export markets are Netherlands 11.9%, China 8.3% and Germany 7.4%. Their main exports are oil and gas. The chart below shows the price of Russian gas at the German border over the last 15 years:-

Source: Indexmundi

Whilst this may be good news for European consumers it has led to considerable political tension. Russia is developing a new gas pipeline – Nord Stream 2 – which will double Russia’s gas export capacity and avoid the geographic obstacle of the Ukraine. It is scheduled to be operational in 2019.

However the EU is developing another gas pipeline – the Southern Gas Corridor, avoiding Russian territory, which is scheduled to be operational in 2020 – to diversify their sources of supply. The Carnegie Moscow Centre – Gazprom’s EU Strategy Is a Dead End – December 6th 2016 takes up the story:-

The EU points out that Ukraine has never violated its gas transit obligations, while Russia shut off the tap during some of the coldest days in 2006 and 2009, and then sharply cut the volume of exports to Europe in late 2014, each time for political reasons. Brussels believes that the real threat to European energy security is not Ukraine but rather the unpredictability of Russian authorities.

US LNG exports are slowly increasing but producers are expected to focus on meeting demand from Japan and other parts of Asia, where prices are higher, first. The Colombia SIPA Center on Global Energy Policy – American Gas to the Rescue – September 2014 – made the following observations which still hold true:-

Although US LNG exports increase Europe’s bargaining position, they will not free Europe from Russian gas. Russia will remain Europe’s dominant gas supplier for the foreseeable future, due both to its ability to remain cost-competitive in the region and the fact that US LNG will displace other high-cost sources of natural gas supply. In our modeling we find that 9 billion cubic feet per day (93 billion cubic meters per year) of gross US LNG exports results in only a 1.5 bcf/d (15 bcm) net addition in global natural gas production.

By forcing state-run Gazprom to reduce prices to remain competitive in the European market, US LNG exports could have a meaningful impact on total Russian gas export revenue. While painful for Russian gas companies, the total economic impact on state coffers is unlikely to be significant enough to prompt a change in Moscow’s foreign policy, particularly in the next few years.

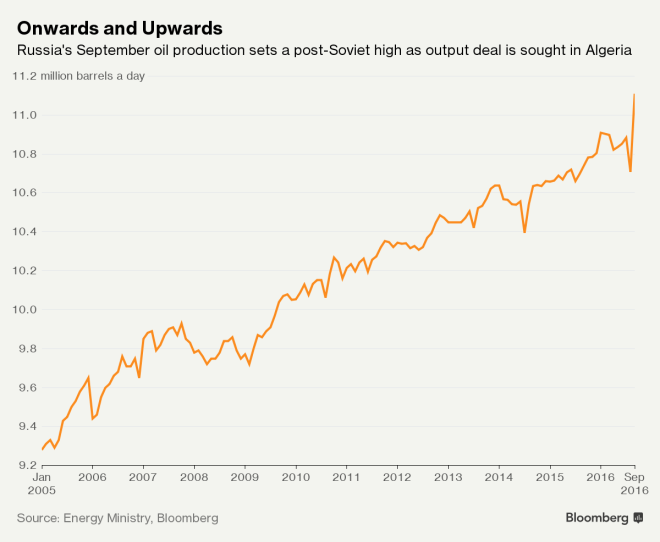

Oil is a more global market and the 29th November OPEC production agreement, the first that OPEC members have signed in eight years, should help to stabilise global prices – that is assuming that OPEC members do not cheat. Russia, although not a member of OPEC, agreed to reduce production by 300,000 bpd. Russia had just achieved record post-soviet production of 11.1mln bpd in September, they have room to moderate their output:-

Source: Bloomberg, Russian Energy Ministry

Prospects for 2017

In 2015 tax from oil and gas amounted to 52% of Russian receipts – a stabilisation of the oil price will be a significant fiscal boost next year. Russia has been far from profligate since 2008, it runs a trade and current account surplus and, although the government is in deficit to the tune of 2.6% of GDP this year, the government debt to GDP ratio is a very manageable 17.17%.

Looking ahead to 2017 Brookings – The Russian economy inches forward – highlights a number of features which support optimism for the future:-

…the country seems to have turned the corner and growth is expected to be positive in 2017-2018. One key reason is that over the last two years, the government’s policy response package of a flexible exchange rate policy, expenditure cuts in real terms, and bank recapitalization—along with tapping the Reserve Fund—has helped buffer the economy against multiple shocks.

…The banking sector has also now largely stabilized. The consolidated budget of regional governments even registered a surplus in the first eight months of 2016. Indeed, on the back of projected rising oil prices, we expect the economy to enter positive territory in 2017 and 2018, reaching 1.5-1.7 percent.

…With a growing federal fiscal deficit (3.7 percent of GDP by end 2016), one proactive step the government has taken is to reintroduce a three-year, medium-term fiscal framework, which proposes to cut the deficit by about 1 percent each year ultimately leading to a balanced budget by 2020. The budget is conservatively costed at a $40 per barrel oil price, and cuts are driven mostly by a reduction in expenditures in mostly defense/military and social policy. If adhered to, this medium-term framework will be an important step toward reducing overall policy uncertainty.

China (and India)

In the longer term a major focus of Russian economic policy has, and continues to be, the development of trade with China. The first Russo-Chinese partnership agreements were signed in 1994 and 1996, followed by the Treaty of Friendship and Cooperation in 2001 and the Strategic Partnership in 2012 which was superseded by a further agreement in 2014 – signed by President Xi. Ratified shortly after the annexation of the Crimea and imposition of sanctions by the US and EU, the latest agreement has substance. Here are some of the more prominent deals which have emerged from the closer cooperation:-

- Gazprom and China National Petroleum Corporation (CNPC) announced a 40 year gas supply deal, including plans to build the “Power of Siberia” gas pipeline.

- Rosneft agreed to supply CNPC with $500bln of oil, potentially making Russia, China’s largest supplier of oil, surpassing Saudi Arabia. The Eastern Siberia-Pacific Ocean oil pipeline will be connected to Northeast China next year and a pipeline linking Siberia’s Chayandinskoye oil and gas field to China comes online in 2018.

- The Central Bank of Russia signed a RUB 815bln swap agreement with the PBoC to boost bilateral trade. They had previously contracted business in US$.

The Diplomat – Behind China and Russia’s ‘Special Relationship’ – investigates the impact this new cooperation is beginning to have:-

…Russia has become one of the five largest recipients of Chinese outbound direct investment in relation to the Chinese government’s Belt and Road Initiative (BRI) connecting Asia with Europe. Meanwhile, China was Russia’s largest bilateral trade partner, in 2015; in spite of declining overall bilateral trade in U.S. dollar terms (mainly due to sharp declines in the ruble as well as the yuan), relative to 2014, trade flows continued to expand in terms of volume.

In this context, it was significant that Russia’s exports of mechanical and technical products to China rose by about 45 percent over the course of 2015 possibly signifying an important trend in the diversification and competitiveness of Russia’s non-energy sector in terms of bilateral trade prospects with China.

The Diplomat goes on to highlight the improved and increasing importance of Russian trade with India:-

The Russia-India-China (RIC) trilateral grouping is considered by its participants as an important arrangement in securing political stability, both globally and in the region. India and Russia’s relations have remained strong for several decades, with Russia being India’s largest defense and nuclear energy partner. However, while China’s and Russia’s relations have clearly improved in the last few years, the China-India relationship has somewhat lagged the development of the other two legs of the triangle. Consequently, Russia has played a role in bringing both sides closer together through its interactions in the RIC grouping.

The Trump Card?

US pre-election rhetoric from the Trump campaign suggested a less combative approach to Russia. Trump said he would “look into” recognising Crimea and removing sanctions, however, Republican hawks in Congress will want to have their say. Syria may be the key to a real improvement in relations – don’t hold your breath.

Conclusion and Investment Opportunities

The Ruble has stabilised and whilst Russia has some external debt the amount is not excessive. The effect of the devaluation of 2014/2015 has run its course and inflation is forecast to decline further next year. It may weaken against the US$ in line with other countries but is likely to be range-bound, with a potential upward bias, against its major trading partners.

The Central Bank of Russia has maintained tight grip short term interest rates, leaving it room to reduce rates, perhaps, as soon as Q1 2017. Russian government bond yields halved since their highs of 16% in late 2014, but have risen by around 60bp since August following the trend in other global bond markets. With short term interest rates set to decline, the inversion of the yield curve is likely to unwind, but this favours shorter dated, lower duration bonds – there is also a risk of forced liquidation by international investors, if US and other bond markets should decline in tandem.

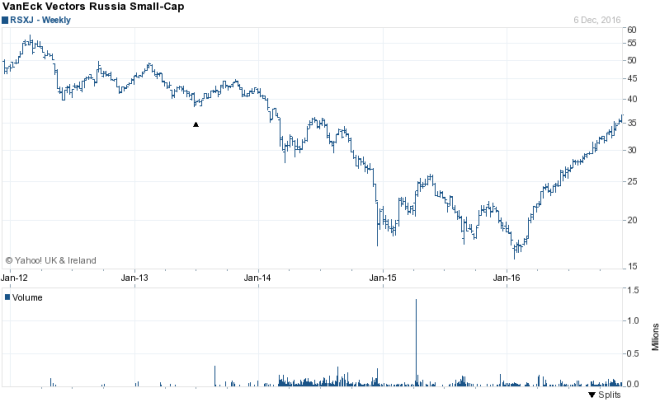

The Russian stock market has already factored in much of the positive economic and political news. The OPEC deal took shape in a series of well publicised stages. The “Trump Effect” is unlikely to be as significant as some commentators hope. The ending of sanctions is the one factor which could act as a positive price shock, however, the Russian economy has suffered a severe recession and now appears to be recovering of its own accord. The VanEck Vectors Russia Small-Cap ETF (RSXJ) has very little exposure to oil and gas and therefore reflects a less commodity-centric aspect of the Russian economy. The chart below covers the five years since 2011. It has risen further than the major indices since January yet still trades at a lower PE ratio:-

Source: Yahoo Finance

Like the RTSI Index the small-cap ETF looks over-bought, however, the economic recovery in Russia appears to be broad-based, Chinese growth, in response to further fiscal stimulus, has increased and the oil price has (at least for the present) stabilised around $50/bbl. If you do not have exposure to Russia, you should consider an allocation. There may be better opportunities to buy, but waiting for trends to retrace can leave you feeling like Tantalus. The last two bull-markets – January 2009 to March 2011, and July 2004 to May 2008 – saw the RTSI Index rally 315% and 382% respectively. In the aftermath of the Russian crisis of 1998 the index rose from 61 to 755 in less than six years (1,138%). Don’t be shy but also keep some power dry.