Macro Letter – No 28 – 23-01-2015

The prospects for the UK in 2015 – Stocks, Gilts and Sterling

- Unlike major Eurozone bond markets, UK 10 year Gilts have yet to make new highs

- The FTSE has lagged both the S&P500 and the DAX

- Sterling continues to appreciate against the Euro, but decline versus the UD$

- UK election uncertainty will dominate and constrain markets until May

Last year the UK stock market trod water while other markets, often with weaker fundamentals, trended higher. Meanwhile UK Gilts headed back towards the multi-year low yields last seen during the Euro crisis in July 2012. UK growth still appears robust when compared to other EU countries; it has broadly kept pace with the US over the course of the last 18 months.

| Annualised GDP | ||

| Country | UK | USA |

| Q1 2013 | 0.9 | 1.7 |

| Q2 2013 | 1.7 | 1.8 |

| Q3 2013 | 1.6 | 2.3 |

| Q4 2013 | 2.4 | 3.1 |

| Q1 2014 | 2.4 | 1.9 |

| Q2 2014 | 2.6 | 2.6 |

| Q3 2014 | 2.6 | 2.7 |

Source: Trading Economics

Earlier this month saw the publication of the Deloitte – Q4 CFO Survey. This influential report is based on a survey of 119 CFO, of which 32 represent FTSE 100 companies. They see a growing divide between good UK fundamentals and UK politics in the run up to the general election in May. The positive domestic environment is also at odds with a number of external risks including the collapse in commodity prices, slowing emerging market growth – especially in China – and the continued weakness and political uncertainty surrounding the Eurozone (EZ).

56% of CFO’s believe now is a good time to invest in their businesses – down from a record high of 71% in Q3. This is still well above the long-term average and the general expectation is that Capital Expenditure will increase 9% in 2015.

The Deloitte report underpins hopes for the return of real wage growth for the first time in six years. The UK employment report, released on Wednesday, may indicate the beginning of a trend: it reveals average weekly earnings rising 1.7% in November – down from 1.9% in October but the third consecutive month of above inflation wage growth. Headline unemployment was 5.8%, down from a previous 6%, but employment growth was muted and the activity rate has declined by 0.5% over the last six months. In other words, less people are participating in the labour market. The rate of private sector pay inflation actually slowed in November from 2.4% to 2.1% – real-wage growth may be distorted by temporary disinflationary factors such as falling energy prices. I think it is safe to suggest that UK living standards are stabilising after a painful period of adjustment.

Last week also saw the publication of UK inflation data. Following a trend seen in a number of other developed markets, it came in at 14 year low of +0.5% – well below the Bank of England (BoE) target of 2%. It is likely that Governor Carney will blame this divergence on external factors when he writes his first letter of explanation to the UK Chancellor. The excuses have already begun; this speech, given yesterday by external MPC member David Miles, opens:-

What can monetary policy be expected to do? My short answer comes in three parts: First, rather a lot less than many people who view inflation targets as too narrow seem to think; those who want to broaden the aims of monetary policy well beyond inflation to include targets for growth, financial stability and even income inequality may seriously over-estimate what policy can realistically achieve. Second, rather a lot more than is implied by many economic models which take a narrow view of the channels through which monetary policy affects behaviour and as a result make the ability of monetary policy to stabilise the economy precarious. Third, the success of monetary policy in achieving stable inflation (or prices) depends crucially on that being consistent with fiscal policy. Monetary policy cannot be expected to achieve price stability in isolation from things fiscal; monetary policy does not hold all the cards – it cannot trump everything.

The fall in inflation has been widespread, as the chart below shows, but this may not be an indication of economic malaise since external factors, such as the fall in oil prices and the continued decline in the Euro, are a significant influence. Nonetheless, as the Economic Research Council observe in their recent commentary, this is the first time on record that all four sub-sectors have experienced an inflation rate of 1% or less in a single month:-

Source: ONS and Economic Research Council

A more important gauge of corporate domestic conditions can be gleaned from the BoE – Q4 2014 Credit Conditions Survey – published on 6th January. Here are some of the highlights:-

…The overall availability of credit to the corporate sector was unchanged in Q4 according to lenders, and was expected to remain unchanged in Q1.

…While demand for credit from small businesses was reported to have decreased in Q4, demand from medium-sized companies increased significantly. Demand for credit from large corporates increased slightly in 2014 Q4.

…Spreads on lending to small businesses were unchanged in Q4, while spreads for medium-sized companies and large corporates narrowed significantly. These trends were expected to continue over the next three months.

…Default rates on corporate lending fell in Q4, particularly on lending to small businesses. Losses given default were unchanged in Q4 for small businesses, but fell for medium-sized companies and large corporates.

The minutes of the December MPC meeting showed a unanimous vote in favour of maintaining the stock of assets purchased during the period of QE from September 2009 to July 2012 – £375 bln – despite two members continuing to vote in favour of a 25bp rate increase. On Wednesday the January MPC minutes showed a unanimous accord to leave rates unchanged. Alert to the possibly temporary nature of the positive price shocks of lower oil and a declining Eur, Weale and McCafferty, the two MPC hawks, said their decision was “finely balanced”. The minutes went on to say:-

…the risks to CPI inflation in the medium term might have, if anything, shifted to the upside, but all members were also alert to the downside risk of current low inflation becoming entrenched.

At first sight the Deloitte CFO survey and the BoE Credit Conditions survey appear to be at odds, until one remembers the degree to which corporate sector demand for credit has been stifled by the unconventional monetary policy of the BoE and other central banks over the last few years. Negative real-interest rates distort the credit price discovery mechanism.

Corporates have chosen to issue special dividends or buy back stock rather than borrow at ostensibly attractive rates because of the uncertainty which surrounds the economic consequences of interest rate normalisation.

Nonetheless, in several respects, the UK economy looks robust, especially in comparison to most of the EZ. Six years of falling real wages – down 11% over the period – has allowed average working hours and private sector GDP to push well above the pre-crisis highs of 2007. Productivity, however, remains a problem, real GDP per hour barely moved, suggesting that “low wage – low skill” employment has taken up the slack. This has stimulated an influx of 1.5mln immigrant workers, and stoked divisive political debate, in the process. The economy may have grown but the standard of living of the average voter has not.

UK Public sector finances remain a concern as this chart from the Economic Research Council demonstrates:-

Source: Economic Research Council and ONS

Net government borrowing has improved, retreating from its zenith of 10% of GDP in 2009/2010 to less than 6% in 2013/2014, however the total Net Debt to GDP ratio continues to rise – the ERC are forecasting 83% during the 2014/2015 tax year. Ian Stewart – Chief Economist at Deloitte’s – put it succinctly in a weekly note back in November – Recession Over, Deficit Reduction Grinds On:-

The IMF reckons that the UK’s budget deficit will come in at 5.3% of GDP this year. In Europe, only Spain has a bigger deficit. Markets have worried a lot about public sector indebtedness in the euro area in recent years, but the ratio of borrowing to GDP in France, Italy and Greece this year is likely to be around half UK levels.

…Public sector deficits have been falling as a share of GDP in most countries since 2009.

Small nations which endured deep financial crises have been most aggressive in cutting public borrowing. Greece, Iceland, Ireland, Portugal and Latvia top the league table of deficit reduction since 2009. The US and UK also cut borrowing aggressively. But both, ironically, now have deficits which exceed those of Greece, Ireland and Iceland.

The best way of shrinking public deficits is to grow the economy. Yet while the UK has easily outpaced its peers this year progress in reducing the deficit has gone into reverse. In the first seven months of the 2014/15 financial year the deficit was 6% higher than in the same period a year earlier. The official forecast for a 12% reduction in the deficit in 2014/15 looks unattainable.

The long squeeze on public expenditure is actually on track. The problem is that tax revenues have lagged well behind expectations. Several factors are at work.

Much of the growth in UK employment in the last year has been in low wage work, dampening earnings growth and tax revenues. (The positive side of this is that the young and the unskilled are getting back into work. The proportion of young people not in work education or training is at the lowest level in ten years).

Stronger than expected growth in self-employment, where average earnings are below those in the rest of the economy, have also hit government revenues. The Office of National Statistics calculates that the median incomes for the self-employed fell by a whopping 22% between 2008-09 and 2012-13.

The Coalition’s decision to raise the tax free threshold to £10,000 has eaten further into revenues. Meanwhile, a lower oil price has hit North Sea revenues and a cooling housing market means less money for the Treasury from Stamp Duty.

The Coalition’s strategy has been to shrink the deficit mainly through cutting public expenditure. According to the Institute for Fiscal Studies spending cuts account for 71% of the planned fiscal consolidation, reduced interest payments 15% and tax rises just 12%.

Most planned tax rises have taken effect, but two-thirds of the planned cuts to spending on public services still have to take effect.

The UK is over five years through a ten-year programme of deficit reduction. Roughly half of the total planned tightening still lies ahead. The speed and composition of deficit reduction seem likely to remain a central issue in the next Parliament.

But that’s not how voters see things. A recent poll for the Financial Times by Populus found that 60% of voters do not believe that any further cuts in public spending will be necessary in the next Parliament.

Paradoxically, cutting budget deficits may be politically easier in a time of crisis than when the economy is growing. Voters’ concerns are already shifting away from the economy. Five more years of austerity is not a slogan that is likely to appeal to an electorate that has been through the deepest recession in generations.

The hope for whichever party or coalition wins the next election is that tax revenues pick up. Without such a recovery the next government would have to choose between pushing back the timetable for eliminating the deficit or piling on more austerity. The recession may be over, but much of the pain of deficit-reduction still lies ahead.

The continued deterioration in government finances is one factor which is holding back UK growth, another is the rapid increase in private sector borrowing; primarily mortgages, helped by an extension of the Funding for Lending scheme, and credit cards. According to the Money Charity – January 2015 report:-

People in the UK owed £1.463 trillion at the end of November 2014.

This is up from £1.433 trillion at the end of November 2013 – an extra £591 per UK adult.

The average total debt per household – including mortgages – was £55,384 in November. The revised figure for October was £55,297.

Per adult in the UK that’s an average debt of £28,968 in November – around 115.0% of average earnings. This is up from a revised £28,922 in October.

…Outstanding consumer credit lending was £168.8 billion at the end of November 2014.

This is up from £158.8 billion at the end of November 2013, and is an increase of £199 for every adult in the UK.

These combined public and private sector trends helped to push the current account deficit to a 60 year high of £27bln – 6% of GDP – in Q3 2014, notwithstanding a record service sector surplus of 5.1%:-

Source: economicshelp.org and OBR

The latest Ernst and Young’s ITEM Club forecast was released this week. This revised UK growth since their last estimate in October, from 2.4% to 2.9% for 2015. The revision is mainly due to lower oil prices. This also leads them to predict that inflation will average zero over the course of 2015. The clouds on this decidedly bright horizon are external factors, such as the dismal prospects for EZ growth, the continued slowing of a debt encumbered Chinese economy and the geo-political downside risks for Russia and its acolytes. All these factors would reduce growth but also, barring a dramatic increase in the price of energy, herald lower inflation.

Below is a chart showing annualised UK GDP data over the period 2007-2014:-

Source: Trading Economics and ONS

The recovery looks robust until one realises that over the period 1993 to 2007 UK GDP averaged 3.3%. In the last three years it has only managed 0.9%.

I concur with the ITEM Club; BoE rates are unlikely to rise for some while yet – the money markets are not pricing in a rate rise until Q1 2016. As in many other developed countries, the economic recovery has been muted and protracted due to the overhang of debt and the “monetary engineering” of consumption.

Politics

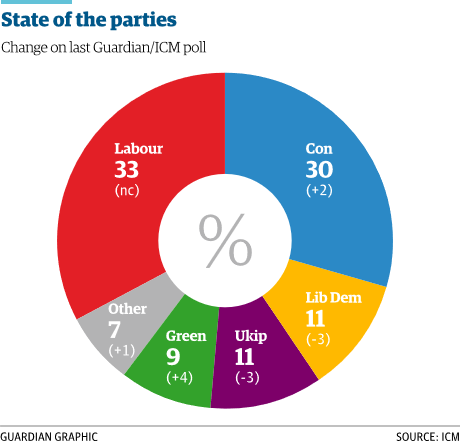

May 7th is the date set for the general election; this event will dominate the political agenda for H1 2015. The latest ICM opinion poll published by The Guardian on Tuesday looks like this:-

Source: Guardian and ICM

An article published last Sunday by British Future – 2015 A Year of Uncertainty – suggest that the election will be the most open in 40 years:-

We don’t even know how many parties will end up forming a government, let alone which ones. New ICM polling for this year’s State of the Nation 2015 report from British Future sheds some light on key issues surrounding the General Election campaign and beyond.

How people predict the outcome of the May 7 election depends very much on who they are, with most party supporters feeling that their team have a good chance: 88% of Conservatives think their party will be in government, while 78% of Labour supporters think theirs will. They can’t both be right. That two-thirds of UKIP supporters think Nigel Farage and co. will be part of the government and 49% of Lib Dems think they will, shows how open a contest it could be.

In an election that may well be dominated by questions about immigration and identity, not everyone is confident that we can emerge from the debate unscathed, with social and community cohesion intact. Our poll finds that only a quarter of Britons believe we can come through the 2015 election campaign with good community relations across our multi-faith and multi-ethnic society. A similar number worry that the tone of the election campaign will damage relations between different communities, while another group of voters wish the gloves would come off more.

…It is the job of politicians to articulate different views, but also to aggregate them. This has become more difficult as our fragmented politics show. But in a fractious society there will also be a greater appetite for politicians who can tell a broader story about what brings us together – one which can engage people in the cities and in coastal towns, across the generations, and build common cause across class, faith and ethnic lines in the Britain we all share.

Asset Market Direction

Uncertainty surrounding the general election will limit price moves for the UK stocks and Gilts until mid-year at the earliest; if anything, there may be capital outflows.

Gilts

Gilts offer higher yields than Bunds or Oats and yet, to a Euro based investor, the currency risk of Gilts, as opposed to the country risk of BTPs or Bonos, makes the carry-trade less than obvious in a UK election year. Here are a selection of 10 year Government bond yields from, post ECB QE announcement at 17:00 GMT on Thursday 22nd:-

| Country | 10 yr Yield | Spread over Bunds |

| Switzerland | -0.19 | -0.64 |

| Germany | 0.45 | 0 |

| Finland | 0.46 | 0.01 |

| Netherlands | 0.48 | 0.03 |

| France | 0.62 | 0.17 |

| Ireland | 1.18 | 0.73 |

| Spain | 1.42 | 0.97 |

| UK | 1.51 | 1.06 |

| Italy | 1.62 | 1.17 |

| Portugal | 2.36 | 1.91 |

| Greece | 8.89 | 8.44 |

Source: Investing.com

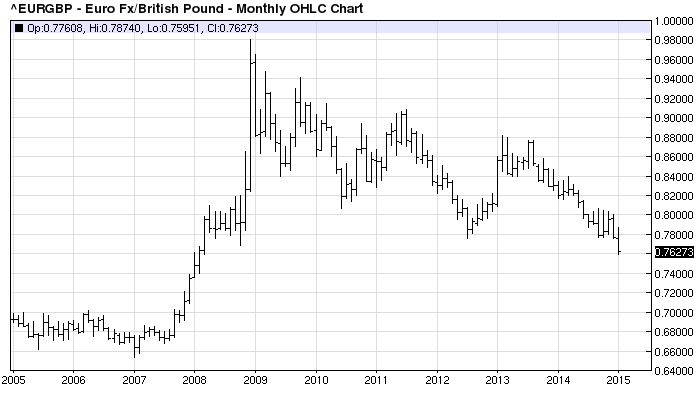

The recent actions of the Swiss National Bank (SNB) whilst extreme, are an indication of the potential impact of currency risk both on the value of a bond and its yield. Meanwhile Gilts, like other government bonds continue their inexorable rise. Here is the monthly yield for 10 year Gilts since January 2007:-

Source: Trading Economics

The absolute low in yield was seen in July 2012 at 1.40% during the depths of the last Euro crisis – at that juncture German Bunds were yielding around1.25% – a spread of around 15bp. I believe we will see fresh all-time highs in Gilts over the coming months, although I am not yet ready to short German Bunds against them, even for more than 100bp of positive carry. In absolute terms Gilt yields have halved in the last 13 months. For long-term investors a yield of 1.5% is hardly exciting, but that is what I said this time last year, only to watch fixed income markets have their best period of capital appreciation in many years.

Currency

The BoE decision to embrace aggressive QE early in the aftermath of the Great Recession – mainly during September and October 2009 – meant that the UK economy was the first to recover, however, as the chart below makes clear, the 40% depreciation of the GBP exchange rate versus its main trading partner created the conditions for a rapid export led recovery in economic fortunes:-

Source: Barchart.com

This month, prompted by the continued strengthening of the US$ and the unpegging of the CHF, has seen EUR/GBP break through the 61.8% retracement level (0.78). It is not inconceivable that the entire move will now be retraced. The 0.70 highs of 2005/2006 look like the next obvious level of support. This will hasten a further deterioration in the current account deficit and allow the EZ to export some of its deflation to the UK.

Against the US$, Sterling has been weakening, as international capital has flowed into the US markets. I expect continued weakness of Cable – it is likely to retest 1.42, a level last reached in May 2010 – together with further Sterling strength versus the Euro.

Stocks

Covering the period since 2010, here is a chart of showing the relative performance of FTSE versus DAX and EuroStoxx 50:-

Source: Yahoo Finance

What is clear is that German stocks have benefitted, from the receding of the Euro crisis, significantly more than either the UK or the broader European market. The DAX outperformance of FTSE, however, dates back to the early 2000’s Hartz reforms which have been key to German growth for more than a decade. As often happens, the UK stock market had already anticipated the resurgence in economic growth prior to 2012. In 2014 the FTSE marked-time as mining and commodity stock weakness was offset by stronger performance in other sectors – especially technology.

The continued weakness in GBP/USD may encourage inward capital flows into UK stocks. The upward momentum of the US economy – barring a major correction on the back of an energy sector related debt default – will also benefit UK stocks; the US is still “the Consumer of Last Resort”. The IMF – World Economic Outlook update cut its global growth forecast earlier this week from 3.8% to 3.5% but increased its US forecast from 3.1% to 3.6%. This is their introduction: –

Global growth will receive a boost from lower oil prices, which reflect to an important extent higher supply. But this boost is projected to be more than offset by negative factors, including investment weakness as adjustment to diminished expectations about medium-term growth continues in many advanced and emerging market economies.

Global growth in 2015–16 is projected at 3.5 and 3.7 percent, downward revisions of 0.3 percent relative to the October 2014 World Economic Outlook (WEO). The revisions reflect a reassessment of prospects in China, Russia, the euro area, and Japan as well as weaker activity in some major oil exporters because of the sharp drop in oil prices. The United States is the only major economy for which growth projections have been raised.

The distribution of risks to global growth is more balanced than in October. The main upside risk is a greater boost from lower oil prices, although there is uncertainty about the persistence of the oil supply shock. Downside risks relate to shifts in sentiment and volatility in global financial markets, especially in emerging market economies, where lower oil prices have introduced external and balance sheet vulnerabilities in oil exporters. Stagnation and low inflation are still concerns in the euro area and in Japan.

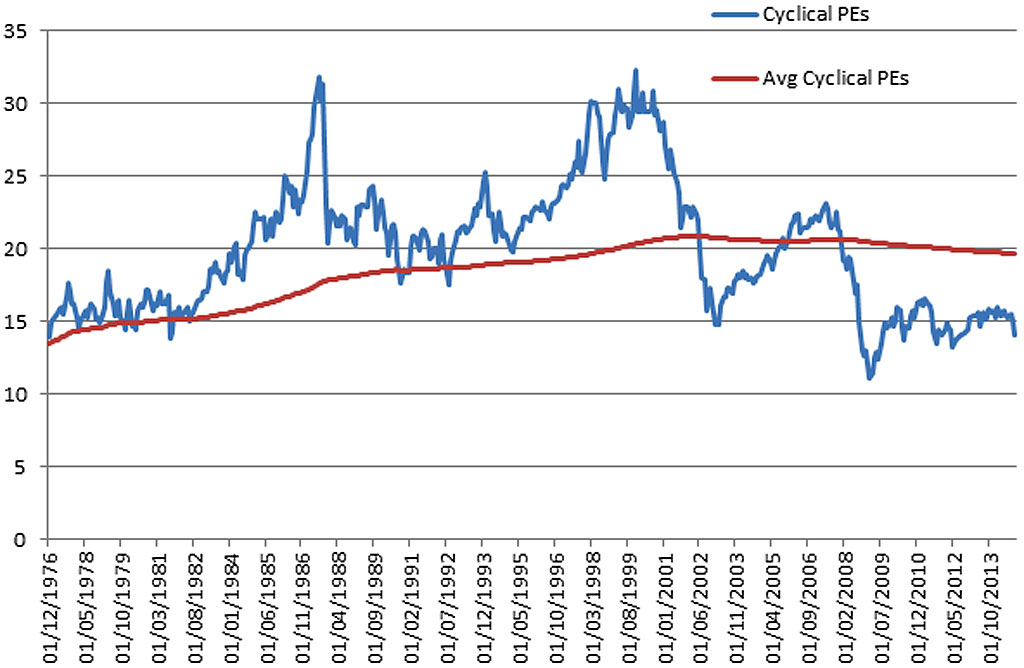

The FTSE is trading on a P/E of around 16 times earnings: this is not far above its long run average. The Shiller/Case CAPE – a measure of the price versus the last 10 years earnings – suggests the market is relatively cheap. Trading at around 15 times it compares favourably with the 27 times multiple of the US. The chart below shows the evolution over the last 40 years – it is from mid-October 2014 and the FTSE is around 300 points higher since then:-

Source: Hargreaves Lansdown

This metric is underpinned by the following chart, again courtesy of the Economic Research Council, which shows the comparative profitability of the UK services and manufacturing sectors:-

Source: Economic Research Council and ONS

UK manufacturing sector profitability is hitting a 16 year high – lower energy prices can only help them improve margins further. This may be one of the factors influencing the investment intensions expressed in the Deloitte CFO survey. Perhaps demand for corporate credit might return in earnest after the election.

With politics overshadowing the market until May, I expect an out-performance by UK stocks to be delayed until H2 2015. Of the many external factors, the performance of the US stock market is probably the most important. The US market has outperformed the UK substantially since the mid-2012 Euro crisis:-

Source: Yahoo Finance

I envisage latent demand driving the UK stock market in the second half of the year. For those who are concerned that the US equity bull-market may be nearing the end its current cycle, long FTSE short S&P500 could be an interesting relative value play. Technically, however, the S&P500 is still trending higher whilst the FTSE should be bought on a convincing breakout above 6875.