Macro Letter – No 23 – 07-11-2014

An Italian stress-test

Palazzo Salimbeni – Siena

- After the ECB Comprehensive Assessment Italian Banks appear the “weakest link”

- Italian bank ownership of BTPs is a growing concern if the “carry trade” should unravel

- Italian stocks have performed better since March but Real-Estate looks better value

Last week I visited Tuscany for the first time in twenty years. Pictured above is of the head office of Banca Monte dei Paschi di Siena. Monte dei Paschi – founded in 1472 – is generally deemed to be the longest established bank in the world. When I visited the city in 1994 their splendid head office, originally the seat of the Salimbeni family, was not open to the public. In the past month in what looks like a “charm offensive” this situation has changed. It is now possible to peruse the bank’s fine collection of art and ponder on the challenges of operating a modern bank in a medieval building.

The change of attitude towards visitors may have been in response to the Banca D’Italia bail-out in January of last year. Monte dei Paschi suffered Eur 2bln in losses in the aftermath of the 2008 financial crisis. Then ,in 2009, they entered into a series of derivative contracts with Deutsche Bank and Nomura which led to further losses in late 2012. The central bank was forced to act since Monte dei Paschi is the third largest banking institution in Italy – though some distance behind Intesa and Unicredit.

AQR Stress

Last week also saw the release of the ECB Comprehensive Assessment. This included the Asset Quality Review (AQR) of the largest 123 financial institutions in Europe. 25 banks failed the test – eight of them were Italian. The tests were performed early this year and of the 25 banks 12 had addressed their capital shortage issues by the time of the publication of the results, however, Monte dei Paschi had the largest shortfall (Eur 2.11bln) and its share price declined by more than 20% on the news. Here is a list of the Italian banks, before and after their capital raising efforts:-

| Bank | Shortfall | Capital Raised | Net Shortfall |

| Monte dei Paschi di Siena | 4.25 | 2.14 | 2.11 |

| Banca Carige | 1.83 | 1.02 | 0.81 |

| Veneto Banca | 0.71 | 0.74 | 0 |

| Banca Popolare di Milano | 0.68 | 0.52 | 0.17 |

| Banca Popolare di Vicenza | 0.68 | 0.46 | 0.22 |

| Credito Valtellinese | 0.38 | 0.42 | 0 |

| Banca Popolare di Sondrio | 0.32 | 0.34 | 0 |

| Banca Popolare dell’Emilia Romagna | 0.13 | 0.76 | 0 |

| Italian Bank Total | 8.98 | 6.4 | 3.31 |

Source: ECB

The Economist – The ECB’s asset Quality Review : Stressful tests sheds more light on what has changed since the last review of European banks: –

The European Central Bank (ECB) simultaneously to the stress-tests has carried out a comprehensive audit of the value of the stuff on each bank’s balance sheet, the Asset Quality Review (AQR). This was only applied to 123 big banks in the euro zone’s 18 countries, which from next month will be regulated by the ECB instead of national watchdogs.

…The ECB found €136 billion in troubled loans banks had not already confessed to owning, bringing the European total to €879 billion ($1.1 trillion). Italy will have to implement the biggest reclassification of loans (€12 billion), with Greek (€8 billion) and German banks (€7 billion) also challenged. Interpreting the results, even at aggregate level, is complicated by the fact that they are arrived at using data from the end of 2013—and much has happened since then. Notably, many banks that thought they might fail the tests have raised over €45 billion in equity, strengthening them considerably. That explains why only 13 banks will have to unveil plans to raise capital when 25 have apparently failed, including Eurobank in Greece, Monte dei Paschi di Siena in Italy and Portugal’s BCP, the only three with more than €1 billion to raise. They now have to come up with plans to strengthen their balance sheets.

For a different perspective on the ECB Comprehensive Assessment the Peterson Institute – Whither Europe’s Banks after the Stress Test? Makes for interesting reading:-

Beyond the 25 banks that failed the test, other banks face difficulties because the asset quality review forced them to acknowledge their exposure to €135.9 billion in nonperforming loans (NPLs) and write down their assets by €47.5 billion. As mentioned above, only €10.7 billion of this sum was uncovered in banks that failed the comprehensive assessment, leaving around €37 billion of these asset write-downs to be recognized on the books of other euro area banks in the coming quarters. The ECB must now aggressively require banks to recognize these losses.

…International banking authorities have agreed to introduce a new definition of capital for banks to be applicable in 2017. Although this new standard—known as the “fully loaded Common Equity Tier 1 (CET1) ratio” —was not part of the comprehensive assessment, the comprehensive assessment published the data so that financial markets can apply the standard to more fully understand the future state of euro area banks. The CET1 standard is much tougher on banks, as it excludes various lax interim arrangements and accounting standards used by banks before they adopt the new standard. The most notorious of these is the ability of banks to employ what are known as deferred tax assets, which enable the banks to inflate the amount of risk capital they have with what has in many cases been essentially a government fiscal transfer to the banks through the backdoor. The effects of these shenanigans in the comprehensive assessment were to let banks avoid having to add €126.2 billion in new capital to get to the new CET1 standard. Were they to have to add that amount, many more banks would have failed the test. German banks benefitted the most from these issues by €33 billion. Spanish banks get away with not having to add €25 billion in new capital, and Italian banks, €16 billion. The fully loaded CET1 data, which is provided for the adverse scenario for the year 2016, better indicates how banks will fare as the new supervisory rules come into force.

Peterson point out that under the fully-loaded CET1 capital definition a further four Italian banks would have failed the stress tests.

The Brookings Institute – Despite Headlines, it’s Good News on Europe’s Banks, but with Some Risk for the ECB has an altogether more sanguine view: –

European banks are in much better shape than many had feared, if the results announced yesterday for the combined “asset quality review” and “stress tests” are accurate measures of the underlying situation and future prospects for the banks. I know the key people involved and they are highly professional and had a strong incentive not to be too lenient, so I tend to take these results as truly positive. They had political room to produce somewhat more pessimistic results, so I interpret these optimistic findings as their true beliefs. On the downside, the European Central Bank (ECB) now “owns” any major banking problems in Europe and runs real risks if these tests were in fact too optimistic, or even if they were broadly right but new problems develop. Observers generally will not distinguish after the fact between new problems and the playing out of old weaknesses. It is hard to read these results as excessively harsh, which would have been the only protection for the ECB.

What was so good about the results? Only 10 percent or 13 banks out of 130 need to raise any additional capital and the total requirement is a miniscule 10 billion euros compared to 22 trillion euros of assets owned by these banks. This not only says positive things about the current state of the banking system, but also removes the threat of regulatory pressure to deleverage further, which might have inhibited needed lending.

Returning, specifically to the Italian banks Bruegel – Monday blues for Italian banks – suggests that for Italy there is still a long way to go:-

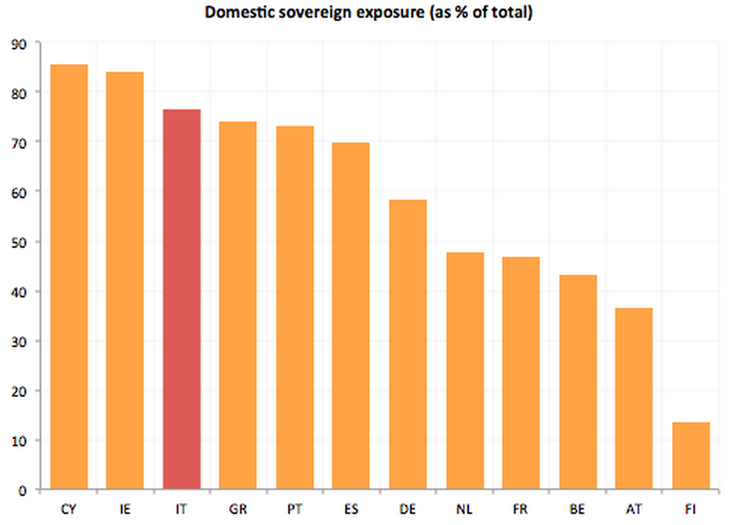

…the Italian banking system is still keeping in place a strong liason dangereuse with the (huge) government debt. This is not at all a special feature of Italian banks (as Figure 1 shows) but with almost 80% of their sovereign long direct gross exposures concentrated on Italy, Italian banks are found in this supervisory exercise to be among the most exposed to the sovereign debt issued by the domestic sovereign. Actually, if one excludes the countries that have been or are under a EU/IMF macroeconomic adjustment programme, Italian banks are the most exposed in the Eurozone.

Source: EBA

More interestingly, the exercise shows that this “home bias”, which is deeply at the root of the sovereign-banking vicious circle that characterised the euro crisis, has even worsened over the last three years.

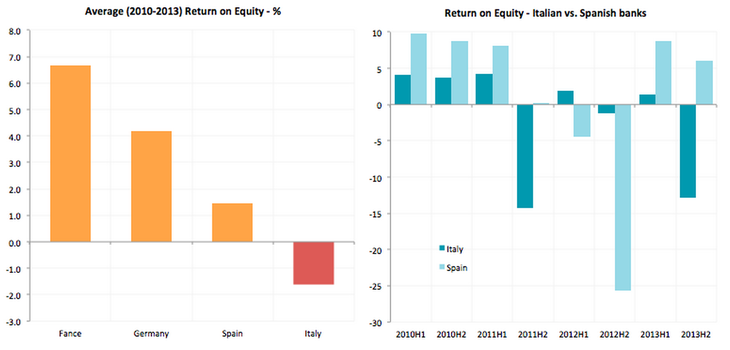

…Sovereign debt accounts by now for around 10% of total assets of Italian banks, on average. The carry trade on these holdings might have kept banks afloat over the last 3 years, but these gains are actually concealing deeper structural issues that Italian banks have – until now – never been forced to face in full.

One such long-known problem of the Italian banking system is profitability, which is (and has been for quite a while now) very low. According to ECB data, average return on equity has been negative over the period 2010-2013 and the comparison with Spanish banks is especially striking. After the huge drop in return on equity during 2012, Spanish banks recovered, whereas Italian banks seemed to have never done it (Figure 2).

Source: EBA

Bruegel goes on to highlight the lack of restructuring of the Italian banking system and suggest that it is ripe for significant consolidation. Being Italy, this will undoubtedly be a more protracted process due to the complex legal structure of many financial institutions and the length of the judicial process. For a detailed review of the Italian judicial system this IMF – Italy Selected Issues paper may be of interest.

Italian Growth

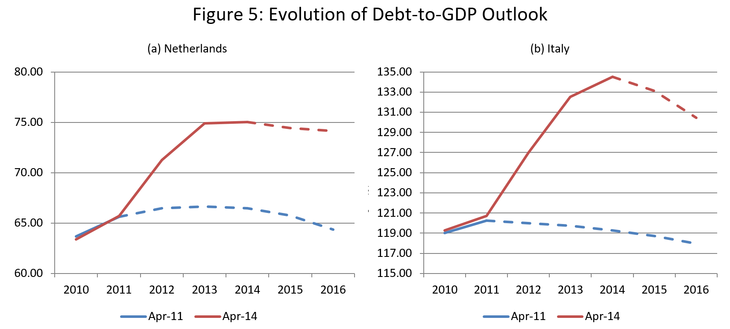

So what are the prospects for Italy now that the banks have almost got their houses in order? The European Commission – Autumn Forecast – released this week – is less than encouraging. Italy is expected to contract -0.4% in 2014 after a decline of -1.9% last year. 2015 is anticipated to see growth returning but only to +0.4%. The Italian government has attempted to reign in public spending but austerity measures have failed to stem the rising ratio of debt relative to GPD. The chart below, also from Bruegel, compares the situation in Italy with that in the Netherlands:-

Source:IMF

The dotted lines show the forecast at each stage. It is some comfort to observe that this is not just an Italian problem but the size of the Italian government debt is, as usual, substantial.

Another important issue to consider when analysing the prospects for Italy is the substantial economic differences between the regions. This Wikipedia map shows the GDP/capita in 2008:-

Source: Wikipedia

My sojourn in Tuscany provided an insight into an “average area” consisting of agriculture and mostly light industry. The agricultural sector is a combination of small holdings, mostly in the north, and larger agro-industry around Maremma. Industry is diversified, although metallurgical firms are still prevalent despite the decline in mining. Service, including banking, and tourism are also significant contributors to the economy of the region.

This is neither the industrial heartland of the Northern League nor the administrative metropolis of Roma but it makes an interesting contrast with other parts of Europe and reveals the slow pace of Italian development over the past two decades. The Italian expression “La Bella Figura” (Nice appearance) as mentioned by Silvia Merler of Bruegal captures the essence of the problem. Italy is a little too comfortable.

In a speech in September by Salvatore Rossi – Senior Deputy Governor of the Banca D’Italia – Finance for Growth he reflected on some “home truths” about the state of the Italian economy:-

Italy has long strayed from the path of economic growth. Common sense tells us this is so and the data confirm it.

In the last six years the recession has doubled the rate of unemployment and eroded 11 percentage points from per capita GDP. But our problems go back much further than that: in 2008, on the eve of the financial crisis, the average amount of goods and services produced by Italian workers was basically unchanged from 1995. In the same period other countries, spurred by the technological paradigm shift of ICT, had seen their productivity rates soar.

The strong growth in employment that was nevertheless recorded in Italy in the pre-crisis years, favoured by the introduction of more flexible work contracts, proved insufficient to offset the effect of the stagnation of productivity on households’ disposable income. At the outbreak of the crisis, for the average household this was at the same level as in the mid-1990s and only the progressive reduction of the saving rate had enabled modest growth in consumption.

The diminishing ability to generate income heralds a decline in living standards, both with respect to this country’s past and to the world’s main players. This is all the more worrying when one considers that in forty years’ time the ratio of people of working age (20-69) to elderly retirees will have halved, from 4 to 2. Even just to maintain per capita living standards at their current levels would require an increase in labour productivity of 25 per cent.

Rossi goes on to discuss the need for finance to help the large number of small companies to grow. He observes that in other countries small firms either succeed and expand rapidly or wither and die whilst in Italy they simply limp on. Rossi discusses the need for economic reform. I believe it requires a serious crisis to achieve these goals.

Bonds

As mentioned earlier in this article, Italian banks are significant holders of BTPs. The European convergence trade has been extremely profitable and hopes that the ECB will begin outright monetary purchases (OMT) should the EZ head into a deep recession means the market prices these bonds with an implicit “put option” attached. I believe this is a far from certain. Only last month we saw a brief panic in the Greek bond market – Italian 10 yr yields followed suit rising by more than 25bp. I see little value remaining long 10yr BTPs at current yields – 2.43% – they have come a long way since their November 2011 lows when they touched 7.50%.

Stocks

The chart below shows the FTSE MIB Index vs EuroStoxx 50 ETF. The Italian stock market has been lagging the broader European market for s significant time as Deputy Governor Rossi’s speech about the lack of economic growth prior to the 2008 crisis observes. However, it is worth noting that the MIB has outperformed EuroStoxx since March of this year, perhaps reflecting concerns about slower growth in France and Germany:-

Source: Yahoo Finance

Sadly the ETF data only stretches back to 2005, nonetheless, this clearly demonstrates the profound underperformance of Italian stocks. The MIB may be outperforming this year but I believe the catalyst is an external slowdown rather than expectation of significant internal growth.

Real-Estate

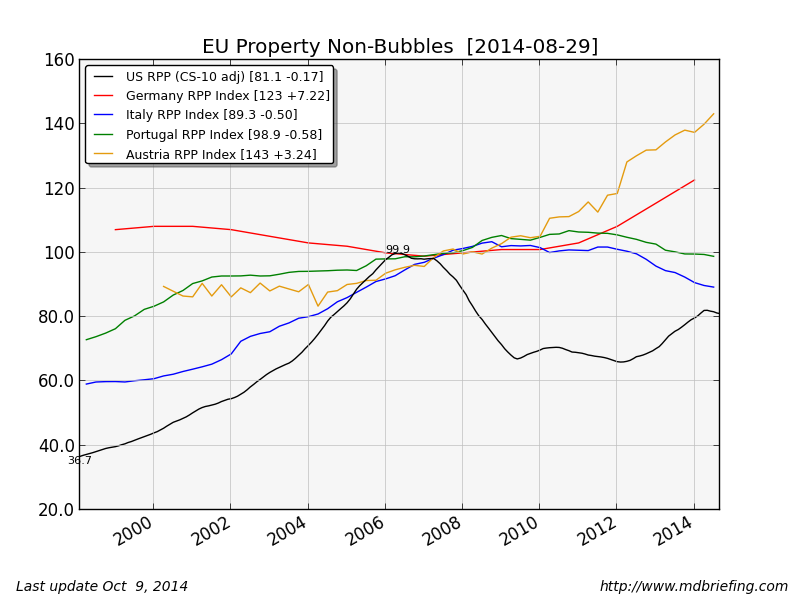

Italian property prices followed the trend seen in many other parts of Europe during the last twenty years but the rise has been muted. This article published in February by Global Property Guide – Italy’s house prices down 6.5% on the year. Will it ever end? Provides some useful background about home ownership and Loan to Value (LTV)rates, it also reflects on the fall in mortgage rate:-

The average interest rate for new housing loans was 2.92% from May 2009 to March 2011, but then rose to a maximum of 4.3% in February 2012. After the ECB rate was reduced from 1% to around 0.75% in July 2012, the average interest rate for house purchases also started declining along with the ECB rate. In November 2013, the interest rate for new housing loans was at 3.54%.

Across the country, Italian house prices have been declining since 2009, however, unlike some other European countries the Italian mortgage market is relatively under developed and LTV rates remain subdued. Whilst debt is a major issue for Italy, mortgage debt acts as less of a fiscal drag on the economy than in the UK or Ireland.

Source: MD Briefing

Recent price trends suggest that a recovery is under way. Milanese housing is now forecast to rise by around 4% in 2014 – earlier this year expectations were for continued price declines. The initial resurgence in demand is likely to emanate from the commercial sector. International demand for tourist property will be subdued by the supply overhang in Spain and Portugal but, once the new TASI property tax has worked its way through the system, the broader market will start to clear.

Conclusion and investment opportunities

The correction in Real-Estate prices in Italy has been relatively subdued in comparison with Spain, Portugal or Ireland but, despite additional taxation, the market is showing nascent signs of recovery. This is partly due to the significant reduction in mortgage rates since 2012. Italian property did rise substantially between 2000 and 2008 (around 85%) but this is moderate in comparison with some other EZ countries.

As an investment opportunity Real-Estate is preferable to BTPs or the Italian stock market. Italian REITs have been available since 2006 but recent changes to rules introduced in August may make the market more vibrant; this article from RE Europe -Italy makes REIT regime more competitive internationally, to grow sector by attracting foreign investment provides more detail. Before diving into, what is clearly, a limited market, this article from Bloomberg – Italy seeks to ease REIT rules is also worth reading.

Italy has weaker growth and demographic prospects than some other Europen countries and therefore Real-Estate investment opportunities will be better elsewhere in the EZ, but within Italy I prefer this sector to Bonds or Stocks. After all, at 74.1% Italy is 24th in the world ranking by property ownership (2012 data). After five years of declining prices housing is now more affordable. As the economy recovers from the weakness of 2013 latent demand should emerge. As the picture at the start of this article shows an Italian’s home is his castle.