Macro Letter – No 7 – 14-03-2014

El Nino – Commodities and the export of Emerging Market inflation

Emerging markets currencies have been under pressure since the middle of 2013. Many of these markets have above target inflation but have been helped during the past three years by falling commodity prices. Whilst industrial metals continue to decline and energy products mark time, some key perishable commodities have seen sharp price increases since the beginning of 2014. In part this is due to increased expectation of an El Nino weather pattern developing in the second half of 2014.

For emerging economies food prices are a more significant proportion of consumer prices than for developed economies; as food prices rise, wages will need to follow. The one-off impact of currency weakness will help EM exporters in the near-term, but, once this process has run its course, emerging markets will attempt to export their higher inflation.

Commodity indices

Since the spring of 2011 commodity prices have fallen significantly as the CRB Index chart below shows.

Source: Barchart.com

With the start of 2014 resurgence has begun. It is still nascent, but this may mark the beginning of a new trend. What is driving this process, which commodities are leading, which are lagging and where will the inflationary impact of higher prices show up first?

The CRB Index is one of many commodity indices but it is reasonably diversified and has a heavier weighting to perishable commodities than some other indices. Here is the current list of constituents: –

Raw Industrials: Hides, tallow, copper scrap, lead scrap, steel scrap, zinc, tin, burlap, cotton, print cloth, wool tops, rosin, and rubber (59.1%).

CRB BLS Foodstuffs: Hogs, steers, lard, butter, soybean oil, cocoa, corn, Kansas City wheat, Minneapolis wheat, and sugar (40.9%).

For comparison here is the GSCI, a trade-weighted index of commodities by value. This index is energy heavy (70%) with Crude representing nearly 50% of the index. The weighting for industrial metals is just over 6% and grains around 12%:-

Source: Barchart.com

The table below gives a brief snapshot of a narrower range of commodity futures over the past year, these prices were taken this morning (14th March) UK time:-

|

Commodity |

Daily |

1 Week |

1 Month |

YTD |

| Copper |

0.09% |

-5.12% |

-10.33% |

-16.82% |

| Brent Crude |

0.07% |

-1.67% |

-1.84% |

-2.60% |

| WTI |

-0.04% |

-4.36% |

-2.19% |

5.05% |

| Nat Gas |

-0.66% |

-5.71% |

-16.15% |

12.50% |

| US Corn |

-0.41% |

-0.92% |

8.30% |

-32.77% |

| US Wheat |

0.06% |

2.91% |

12.55% |

-7.00% |

Source: Investing.com

I will review these key markets, adding some commentary on Iron Ore, Coal, Soybeans and Rice since these are critical constituents of industrial metals, energy and agriculture globally.

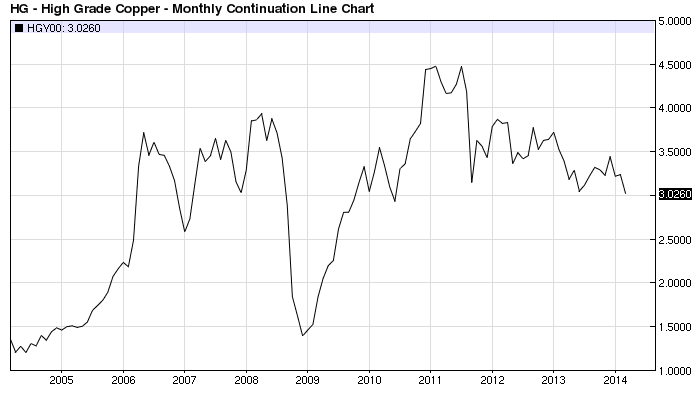

Copper and Iron Ore

Copper prices remain depressed due to a lack of industrial demand, especially from China. Shanghai Copper dropped to a four year low last week after the publication of weak trade data (-18% vs a forecast of +5%).

This chart shows US High Grade Copper. Further weakness may cause a rout: –

Source: Barchart.com

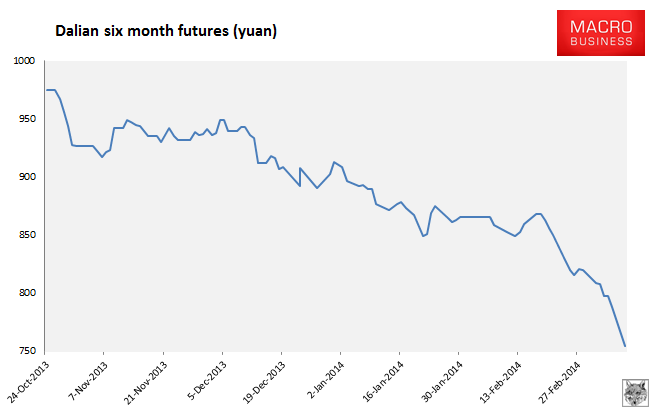

The lack of Chinese industrial demand is also seen in this chart of Dalian Iron Ore Futures: –

Source: Macrobusiness.com.au

Crude Oil

The disparity between the performance of Brent Crude and WTI is not a topic I want to discuss on this occasion; however, using WTI as a proxy, the chart below indicates that prices have remained stable with a small upward bias over the last couple of years. During this same period the US economy has slowly begun to recover:-

Source: Barchart.com

Part of the subdued nature of the price action is due to increases in US domestic production. The US has been fortunate in its ability to harness new technology to increase energy productivity but, as this article from the Manhattan Institute – New Technology for Old Fuel – points out, this is a process which has evolved over many decades; here’s an extract from the executive summary:-

…The key findings of this paper include:

• Between 1949 and 2010, thanks to improved technology, oil and gas drillers reduced the number of dry holes drilled from 34 percent to 11 percent.

• Global spending on oil and gas exploration dwarfs what is spent on “clean” energy. In 2012 alone, drilling expenditures were about $1.2 trillion, nearly 4.5 times the amount spent on alternative energy projects.

• Despite more than a century of claims that the world is running out of oil and gas, estimates of available resources continue rising because of innovation. In 2009, the International Energy Agency more than doubled its prior-year estimate of global gas resources, to some 30,000 trillion cubic feet—enough gas to last for nearly three centuries at current rates of consumption.

• In 1980, the world had about 683 billion barrels of proved reserves. Between 1980 and 2011, residents of the planet consumed about 800 billion barrels of oil. Yet in 2011, global proved oil reserves stood at 1.6 trillion barrels, an increase of 130 percent over the level recorded in 1980.

• The dramatic increase in oil and gas resources is the result of a century of improvements to older technologies such as drill rigs and drill bits, along with better seismic tools, advances in materials science, better robots, more capable submarines, and, of course, cheaper computing power.

In a number of less developed countries the geopolitics of oil are more relevant. On the United States doorstep is Venezuela – ranked 9th by Crude production (3mln bpd). The political and economic situation within the country is getting worse in the post-Chavez environment. This short article from The Peterson Institute – Can Venezuela Learn from Ukraine? Sums up the current situation: –

…For Venezuela’s sake, President Maduro should be watching events unfold in Ukraine and act to avoid the sort of bloodshed that finally led to the ouster of Yanukovych. If he does, he may buy himself some more time to devise a strategy to unwind some of the most egregious economic distortions.

Last April, at the Peterson Institute’s spring Global Economic Prospects meeting, we predicted [pdf] that Venezuelan President Maduro would be unable to continue Hugo Chavez’s legacy of 21st century socialism because of serious economic and political pressures. Those pressures have only increased. With his own party far from united, question marks regarding the role of the military, and a strengthening protest movement, it is only a matter of time before Venezuela also reaches a breaking point. Perhaps helped by a coordinated effort by the Mercosur countries and the United States, Venezuela should step up to the challenge.

Another political hot-spot is Russia. Producing 10.9 mln bpd, Russia is the largest Oil producer globally. She is unlikely to reduce production but may divert supply away from Europe should the Ukrainian impasse deteriorate further. On balance this may not be catastrophic for the global economy since China may be an obvious beneficiary.

Shia, Saudi Arabia (ranked 2nd – producing 9.9 mln bpd) has a veneer of stability, but the increasing dialogue between the developed nations and Sunni, Iran (ranked 4th – producing 4.2 mln bpd) concerning their nuclear development programme, is inherently destabilising.

Barring a collapse in world economic growth, I believe Crude Oil prices will be robustly supported. Excepting the benign influence of US domestic productivity gains, the risks are skewed to the up-side.

Natural Gas

Unlike Crude Oil, Natural Gas is geographically constrained by distribution bottlenecks. At a global level Natural Gas can be divided into three price groups as the chart below illustrates: –

Source: World Bank and Knoema

Please note: this chart doesn’t incorporate the price increase in Europe since the Ukrainian revolution began. These price differentials are a source of opportunity and will encourage technological development, especially in the area of natural gas liquification.

The steady increase in US Nat Gas since early 2012 is seen more clearly in the next chart: –

Source: Barchart.com

The latest up-surge has been driven by the extreme cold weather which affected much of the US. This is a reminder of the natural cyclicality of Nat Gas prices in response to extremes of cold or hot. The current price is towards the upper end of its post 2009 range. Improvements in fracking technology make any price increases attractive for producers to increase supply. Production improvements are evident even in areas where conventional extraction techniques are employed. The Potential Gas Committee – April 2013 press release paints a rosy picture for production in general: –

The Potential Gas Committee (PGC) today released the results of its latest biennial assessment of the nation’s natural gas resources, which indicates that the United States possesses a total technically recoverable resource base of 2,384 trillion cubic feet (Tcf) as of year-end 2012. This is the highest resource evaluation in the Committee’s 48-year history, exceeding the previous high assessment (from 2010) by 486 Tcf. Most of the increase arose from new evaluations of shale gas resources in the Atlantic, Rocky Mountain and Gulf Coast areas.

These changes have been assessed in addition to 49 Tcf of domestic marketed-gas production estimated for the two-year period since the Committee’s previous assessment.

“The PGC’s year-end 2012 assessment reaffirms the Committee’s conviction that abundant, recoverable natural gas resources exist within our borders, both onshore and offshore, and in all types of reservoirs—from conventional, ‘tight’ and shales, to coals,” said Dr. John B. Curtis, Professor of Geology and Geological Engineering at the Colorado School of Mines and Director of the Potential Gas Agency there, which provides guidance and technical assistance to the Potential Gas Committee.

The inherent volatility of Nat Gas prices makes prediction about longer term trends difficult, but, I believe the main factor which will influence US Nat Gas prices longer term will be the development of LNG capacity: and this must be preceded by the issuance of further Nat Gas export licenses by the US DOE.

Coal

Coal doesn’t appear in the commodity futures table above, but, like Iron Ore and Natural Gas, it is globally important. This chart from Uppsala University – Coal future of China and the World shows how Coal production is still increasing:-

Source: Uppsala University

According to the World Coal Association, China is currently the world’s largest producer but also the largest importer, 81% of its electricity is generated from Coal. By comparison the second largest producer, USA, is the forth largest exporter and uses Coal for only 43% of its electricity generation. The third largest producer, India, is the third largest importer and uses Coal for 68% of its electricity generation.

The World Bank compiles monthly commodity prices including Coal from three of the top six export countries; this shows a similarly subdued pattern to industrial metals. Prices are not far above their 2008-2009 lows :-

Source: Knoema and World Bank

Of the BRIC economies, China, India and Russia are among the top five Coal producers (whilst Brazil is 12th largest producer of Crude Oil). From an energy-security perspective, Coal is a geopolitical palliative since “known reserves” are globally distributed. Prices are far from over-stretched and predictions for “Peak-Coal” are still some decades away. If Coal prices rebound from their current levels it will most likely be due to demand-pull factors.

Grains and El Nino

Last year Wheat, Corn and Soybeans all declined substantially, but, when viewed over the past decade prices appear to have consolidated and are now beginning to push higher.

Source: Barchart.com

Source: Barchart.com

Source: Barchart.com

US Rice, by contrast, remained broadly stable.

Source: Barchart.com

To understand the impact on emerging market inflation, however, we need to look beyond the US domestic market. The table below shows Wheat and Rice production for 2013 by country.

| WHEAT | ||

| Rank | Country | Production 2013 (mln tons) |

|

1 |

China |

125.6 |

|

2 |

India |

94.9 |

|

3 |

United States |

61.8 |

|

4 |

France |

40.3 |

|

5 |

Russia |

37.7 |

| RICE | ||

| Rank | Country | Production 2013 (mln tons) |

|

1 |

China |

143 |

|

2 |

India |

99 |

|

3 |

Indonesia |

36.9 |

|

4 |

Bangladesh |

33.8 |

|

5 |

Vietnam |

27.1 |

|

6 |

Thailand |

20.5 |

|

7 |

Philippines |

11 |

|

8 |

Myanmar |

10.75 |

|

9 |

Brazil |

7.82 |

|

10 |

Japan |

7.5 |

The disruption to grain production in the Ukraine provides significant price support for Wheat (and also Corn) but a more global factor may be brewing in the central Pacific: El Nino. Whilst Wheat and Rice are not substitutes El Nino weather patterns may disrupt production of both commodities. Risks are on the upside.

Last week the NOAA – ENSO (National Oceanic and Atmospheric Administration – El Nino Southern Oscillation) report maintained its forecast of a 50% chance of El Nino developing by summer or fall 2014. For the US El Nino has a number of effects on agriculture as this article from The Southeast Climate Consortium illustrates: –

During El Niño Years

Corn yields are usually lower than historic averages.

Harvests of summer crops such as corn, peanuts, and cotton may be delayed because of increased rains in the fall.

Frequent rains may reduce tilling and yield of winter wheat.

Wheat yields in southern AL and GA are generally higher than average during El Niño.

Frequent rains at the end of August and in early September may increase Hessian fly populations on winter wheat.

For a more global view of the El Nino effect the following map simplifies an otherwise complex picture, droughts in Brazil, India, Indonesia and Australia stand out: –

Source: PhysicalGeography.net

Last month Reuters – El Nino threatens to return described some of the risks, you will notice they predict heavy rain in Brazil – the El nino effect is a distinctly complex: –

A strong El Nino can wither crops in Australia, Southeast Asia, India and Africa when other parts of the globe such as the U.S. Midwest and Brazil are drenched in rains.

While scientists are still debating the intensity of a potential El Nino, Australia’s Bureau of Meteorology and the U.S. Climate Prediction Center have warned of increased chances one will strike this year.

…Last month, the United Nations’ World Meteorological Organization said there was an “enhanced possibility” of a weak El Nino by the middle of 2014.

The specter of El Nino has driven global cocoa prices to 2-1/2 year peaks this month on fears that dry weather in the key growing regions of Africa and Asia would stoke a global deficit. Other agricultural commodities could follow that lead higher if El Nino conditions are confirmed.

… In India, the world’s No.2 producer of sugar, rice and wheat, a strong El Nino could reduce the monsoon rains that are key to its agriculture, curbing production.

“If a strong El Nino occurs during the second half of the monsoon season, then it could adversely impact the production size of summer crops,” said Sudhir Panwar, president of farmers’ lobby group Kishan Jagriti Manch.

El Nino in 2009 turned India’s monsoon patchy, leading to the worst drought in nearly four decades and helping push global sugar prices to their highest in nearly 30 years.

Elsewhere in Asia, which grows more than 90 percent of the world’s rice and is its main producer of coffee and corn, a drought-inducing El Nino could hit crops in Thailand, Indonesia, Vietnam, the Philippines and China.

And it could deal another blow to wheat production in Australia, the world’s second-largest exporter of the grain, which has already been grappling with drought in the last few months.

Between 2006 and 2008 average world prices for Rice rose by 217%, Wheat by 136%, Corn by 125% and Soybeans by 107%. This prompted food riots in India and other emerging market countries. Many commentators blamed developed countries whose institutions had been investing in commodities to diversify their portfolios away from traditional asset classes, but El Nino also had a significant hand in this process.

In December 2013 CFTC proposed amended limits on positions size for 28 US commodity futures markets – not solely to aid the emerging world. This may restrict some investment activity but is unlikely to reduce volatility. Here is the Harvard Law School Forum review of the proposal.

For emerging economies food prices are more important to CPI. This essay from the St Louis Federal Reserve – Food Prices and Inflation in Emerging Markets sheds more light on the topic: –

Rising food prices contribute more to inflation in developing countries because food is a much higher share of the consumption basket in emerging markets than in wealthier countries. For example, food accounts for 15 percent of the U.S. consumer price index (CPI) basket, but 50 percent of the Philippines’ CPI basket. Compounding the differences, research shows that there is a much more significant pass-through from food prices to non-food prices in developing countries compared with advanced countries, where there is almost none.

Emerging Market Currencies and inflation

The weakening of emerging market currencies since mid-2013 has been widely covered in the financial press. The “Fragile Five” – Brazil, India, Indonesia, South Africa and Turkey – have, among other attributes, above target inflation. How much higher will this become in response to their declining currencies and when will this inflation start to be exported? Assuming there is a lag between changes in commodity prices and CPI, last year’s commodity price declines will still be feeding through in 2014. Lower exchange rates allow these economies to become more export competitive in the near-term, but, once this adjustment has run its course, cost push factors will begin to emerge unless world economic growth suddenly stalls.

In Q4 2013 Societe Generale produced the following chart, this is their forecast for EM currencies after the fall: –

Source: Societe Generale

This would be an export led recovery at the expense of developed markets. Adding commodity inflation into the mix together with higher domestic wage costs, in order to meet higher food prices, could begin a global reflation process. Near-term the impact of the EM currency group will, however, be disinflationary for developed economies. This EM Currency ETF chart high-lights the depreciation since Q1 2013: –

Source: Yahoo Finance

Conclusion

Industrial metal prices remain under pressure due to weakness of demand especially from China. Energy prices continue to tread water but are supported by forecasts of better world GDP growth during 2014 and geopolitical concerns. Grains and other perishable commodity prices are vulnerable to upside pressure should a strong El Nino phase develop in H2 2014.

Stronger world growth combined with higher commodity prices will eventually lead to reflation in developed markets as price increases are exported from emerging markets. These effects may be muted by adverse demographics in some countries but those countries with youth on their side will witness an end to the great moderation and the beginning of a new longer-term inflation cycle.

For equity markets inflation is not a universal good as this article from Detlev Schlichter recounts but many emerging markets already have high interest rates. Whilst these rates may go higher still the fear of higher rates is far less severe in these emerging markets than in developed markets where zero-bound asymmetry predominates. I believe emerging market equities – especially agricultural exporters – are well placed to benefit from the next inflation cycle.

Just to let you know Saudi Arabia is Sunni and Iran is Shia

Thanks Holly, it was a long article and I misread my map of Islam. Cheers, Col