.

.

.

.

Macro Letter – No 2 – 16-12-2013

Commodity super-cycles in a fiat currency world

Notwithstanding weakness in the last six weeks, stock markets have witnessed significant gains during 2013, but commodities – with a few exceptions – have failed to follow suit.

For global investors the advent of investible commodity indices has simplified the commodity allocation process but I have always encouraged my readers to view each commodity on its own merits.

The Goldman Sachs – GSCI Index is constructed on a production weighted basis; the table below is courtesy of Reuters: –

|

2013 2012 Change Vs 2012 WTI Crude 30.96% 24.71% 6.25% Kansas Wheat 0.88% 0.68% 0.20% Live Cattle 2.71% 2.62% 0.09% Sugar 1.90% 1.85% 0.05% Cotton 1.12% 1.07% 0.05% Gold 3.05% 3.00% 0.05% Soybeans 2.63% 2.62% 0.01% Coffee 0.83% 0.82% 0.01% Natural Gas 2.03% 2.02% 0.01% Zinc 0.52% 0.51% 0.01% Cocoa 0.23% 0.23% 0.00% Nickel 0.58% 0.58% 0.00% Silver 0.49% 0.49% 0.00% Aluminum 2.12% 2.13% -0.01% Lead 0.38% 0.40% -0.02% Corn 4.66% 4.69% -0.03% Feeder Cattle 0.49% 0.52% -0.03% LME Copper 3.24% 3.28% -0.04% Lean Hogs 1.52% 1.58% -0.06% Chicago Wheat 3.04% 3.22% -0.18% Gas Oil 8.11% 8.56% -0.45% RBOB Gasoline 5.02% 5.90% -0.88% Heating Oil 5.13% 6.17% -1.04% Brent Crude 18.35% 22.34% -3.99% |

This highlights the increasing production of WTI Crude (West Texas Intermediate) relative to Brent Crude. It also highlights the substantial index weighting to Energy followed by Metals and then Grains. In this letter I will keep these weightings in mind.

The table below, from barchart.com, shows the year to date performance of the major US futures markets. The price divergence is not atypical.

.

.

.

.

Source: barchart.com

As an “asset class” commodities offer among the most uncorrelated returns, but, unlike more traditional assets, they generally have a negative real expected long-term return. In other words, due to human ingenuity, the cost of production falls over time.

Back in 2006 I used the chart below from the Economist as part of a presentation about the dangers of “long-only” investment in commodities. The Economist first published its Industrial Commodity-price index in 1864 due to demand for information on commodity markets resulting from the strong price appreciation during the preceding two decades. The commodity price appreciation was driven primarily by US demand as the country industrialised and then entered into a bloody civil war. Historic data was collected to create a starting level of 100 in 1845. When the raw data is deflated using the US GDP deflator you will observe that the current index is rebounding from a cyclical low of 20.

The Economist industrial commodity-price index

.

.

.

.

.

Source: Economist

Today, in a world of fiat currencies, it is more difficult to examine the cause and effect of changes in supply and demand for commodities because their measurement – generally in US$ – is itself a “moving target” rather than a “store of value”. However, given the vagaries of Gold leasing and the plethora of conspiracy theories surrounding the price of Gold, the “gently declining” US$ seems like the most familiar measure of value. This “Dollar Value” is practical in the short-term but in the Long Run the entire commodity cycle may be as much a reflection of monetary policy as supply and demand for the underlying commodities.

The collapse of Bretton Woods in 1971 heralded in a period of inflation, the appointment of Paul Volcker as governor of the Federal Reserve finally reversed this process as he attempted to control the supply of money. The bursting of the “Tech Bubble” and a policy of low interest rates created the conditions for the next “Super-cycle”.

One of the vexing issues with commodity super-cycles is their variability of duration. This paper from the United Nations Department of Economic and Social Affairs – Super-cycles of commodity prices since the mid-nineteenth century – is a useful guide to the difficulties of prediction: –

http://www.un.org/esa/desa/papers/2012/wp110_2012.pdf

Here is the abstract:-

Decomposition of real commodity prices suggests four super-cycles during 1865-2009 ranging between 30-40 years with amplitudes 20-40 percent higher or lower than the long-run trend. Non-oil price super-cycles follow world GDP, indicating they are essentially demand-determined; causality runs in the opposite direction for oil prices. The mean of each super-cycle of non-oil commodities is generally lower than for the previous cycle, supporting the Prebisch-Singer hypothesis. Tropical agriculture experienced the strongest and steepest long-term downward trend through the twentieth century, followed by non-tropical agriculture and metals, while real oil prices experienced a long-term upward trend, interrupted temporarily during the twentieth century.

The paper goes on to point out that these cycles can last between 20 and 70 years. The UN, however, focus on developing country demand, seeing it as the main driver of the cycles; they don’t consider the “money” side of this phenomenon.

The origin of modern economic studies of cycles is thought to have commenced with Nicolai Kondratiev, it was then taken up by economists of the Austrian School, most notably Joseph Schumpter. At this time – 1930’s – other price cycle theories were being developed independently by Ralph Elliott, among others. Elliott’s ideas were published in his book – The Wave Principle – in 1938. Among his influences were the Italian 10th Century mathematician Leonardo of Pisa – otherwise known as Fibonacci.

I believe there is another long-term factor which drives these cycles, beyond economic growth and currency debasement, and that is geopolitical tension. In developing my thoughts on this subject I am indebted to two authors; Marc Widdowson – The Coming Dark Age – The Phoenix Principle – which I must admit I am still reading, you may download it here: –

http://www.scribd.com/doc/63914376/The-Coming-Dark-Age

The other author is David Murrin – Breaking the Code of History – David looks at the history of empires using a wave principle derived from Elliott and the Polish-American mathematician Benoit Mandelbrot’s theories of fractal geometry, here is his website:-

In simple terms, David’s observation is that the majority of wars, throughout history, have been driven by resource scarcity. Looking back at the Economist Commodity Price Index you can identify the great conflicts of recent history. However, during the tumults, more often than not, payment in specie was suspended and inflation ensued. Any countries return to the “Gold Standard”, or its equivalent, was likely to precipitate an inevitable period of deflation; as happened to the UK and US after the first world war.

Returning to the factor of debasement, during the “Great Deformation”, as David Stockman describes the post Bretton Woods era (1971 onwards) governments have been operating in an elastic “quasi-war finance” environment. When ever a crisis arrives, governments lean on their respective central banks to backstop the markets with abundant liquidity. As the worlds’ “reserve currency” is the US$, the US government has an advantage – what De Gaulle referred to as the “exorbitant privilege” during the period of the gold exchange standard, remains a boon today – but other countries have succeeded to a lesser degree by allowing their currencies to decline relative to the UD$.

The prospects for commodities

Looking ahead to 2014 there are a plethora of factors to consider. I will focus on just a few: –

Commodity – Demand

On the demand side of the equation are China followed by other emerging market countries where strong economic growth is expected. Below is the OECD GDP forecast from 20th November 2013: –

| Real gross domestic product – forecasts | ||||||||||

| | |

2008 |

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

|

| | Australia |

2.4

|

1.5

|

2.6

|

2.4

|

3.7

|

2.5

|

2.6

|

3.1

|

|

| | Austria |

0.9

|

-3.5

|

1.9

|

2.9

|

0.6

|

0.4

|

1.7

|

2.2

|

|

| | Belgium |

1.0

|

-2.8

|

2.4

|

1.9

|

-0.3

|

0.1

|

1.1

|

1.5

|

|

| | Canada |

1.2

|

-2.7

|

3.4

|

2.5

|

1.7

|

1.7

|

2.3

|

2.6

|

|

| | Chile |

3.2

|

-0.9

|

5.7

|

5.8

|

5.6

|

4.2

|

4.5

|

4.9

|

|

| | Czech Republic |

3.1

|

-4.5

|

2.5

|

1.8

|

-1.0

|

-1.5

|

1.1

|

2.3

|

|

| | Denmark |

-0.8

|

-5.7

|

1.4

|

1.1

|

-0.4

|

0.3

|

1.6

|

1.9

|

|

| | Estonia |

-4.2

|

-14.1

|

2.6

|

9.6

|

3.9

|

1.0

|

2.4

|

4.0

|

|

| | Finland |

0.3

|

-8.5

|

3.4

|

2.7

|

-0.8

|

-1.0

|

1.3

|

1.9

|

|

| | France |

-0.2

|

-3.1

|

1.6

|

2.0

|

0.0

|

0.2

|

1.0

|

1.6

|

|

| | Germany |

0.8

|

-5.1

|

3.9

|

3.4

|

0.9

|

0.5

|

1.7

|

2.0

|

|

| | Greece |

-0.2

|

-3.1

|

-4.9

|

-7.1

|

-6.4

|

-3.5

|

-0.4

|

1.8

|

|

| | |

2008 |

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

|

| | Hungary |

0.9

|

-6.8

|

1.1

|

1.6

|

-1.7

|

1.2

|

2.0

|

1.7

|

|

| | Iceland |

1.2

|

-6.6

|

-4.1

|

2.7

|

1.4

|

1.8

|

2.7

|

2.8

|

|

| | Ireland |

-2.2

|

-6.4

|

-1.1

|

2.2

|

0.1

|

0.1

|

1.9

|

2.2

|

|

| | Israel 1 |

4.5

|

1.2

|

5.7

|

4.6

|

3.4

|

3.7

|

3.4

|

3.5

|

|

| | Italy |

-1.2

|

-5.5

|

1.7

|

0.6

|

-2.6

|

-1.9

|

0.6

|

1.4

|

|

| | Japan |

-1.0

|

-5.5

|

4.7

|

-0.6

|

1.9

|

1.8

|

1.5

|

1.0

|

|

| | Korea |

2.3

|

0.3

|

6.3

|

3.7

|

2.0

|

2.7

|

3.8

|

4.0

|

|

| | Luxembourg |

-0.7

|

-5.6

|

3.1

|

1.9

|

-0.2

|

1.8

|

2.3

|

2.3

|

|

| | Mexico |

1.2

|

-4.5

|

5.1

|

4.0

|

3.6

|

1.2

|

3.8

|

4.2

|

|

| | Netherlands |

1.8

|

-3.7

|

1.5

|

0.9

|

-1.2

|

-1.1

|

-0.1

|

0.9

|

|

| | New Zealand |

-0.6

|

0.3

|

0.9

|

1.3

|

3.2

|

2.3

|

3.3

|

2.9

|

|

| | Norway |

0.1

|

-1.6

|

0.5

|

1.2

|

3.1

|

1.2

|

2.8

|

3.1

|

|

| | Poland |

5.0

|

1.6

|

3.9

|

4.5

|

2.1

|

1.4

|

2.7

|

3.3

|

|

| | Portugal |

0.0

|

-2.9

|

1.9

|

-1.3

|

-3.2

|

-1.7

|

0.4

|

1.1

|

|

| | Slovak Republic |

5.8

|

-4.9

|

4.4

|

3.0

|

1.8

|

0.8

|

1.9

|

2.9

|

|

| | Slovenia |

3.4

|

-7.9

|

1.3

|

0.7

|

-2.5

|

-2.3

|

-0.9

|

0.6

|

|

| | Spain |

0.9 |

-3.8

|

-0.2

|

0.1

|

-1.6

|

-1.3

|

0.5

|

1.0

|

|

| | |

2008 |

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

|

| | Sweden |

-0.8

|

-5.0

|

6.3

|

3.0

|

1.3

|

0.7

|

2.3

|

3.0

|

|

| | Switzerland |

2.2

|

-1.9

|

3.0

|

1.8

|

1.0

|

1.9

|

2.2

|

2.7

|

|

| | Turkey |

0.7

|

-4.8

|

9.2

|

8.8

|

2.2

|

3.6

|

3.8

|

4.1

|

|

| | United Kingdom |

-0.8

|

-5.2

|

1.7

|

1.1

|

0.1

|

1.4

|

2.4

|

2.5

|

|

| | United States |

-0.3

|

-2.8

|

2.5

|

1.8

|

2.8

|

1.7

|

2.9

|

3.4

|

|

| | Euro area (15 countries) |

0.2

|

-4.4

|

1.9

|

1.6

|

-0.6

|

-0.4

|

1.0

|

1.6

|

|

| | OECD-Total |

0.2

|

-3.5

|

3.0

|

1.9

|

1.6

|

1.2

|

2.3

|

2.7

|

|

| | Brazil |

5.2

|

-0.3

|

7.5

|

2.7

|

0.9

|

2.5

|

2.2

|

2.5

|

|

| | China |

9.6

|

9.2

|

10.4

|

9.3

|

7.7

|

7.7

|

8.2

|

7.5

|

|

| | India |

6.2

|

5.0

|

11.2

|

7.7

|

3.8

|

3.0

|

4.7

|

5.7

|

|

| | Indonesia |

6.0

|

4.6

|

6.2

|

6.5

|

6.2

|

5.2

|

5.6

|

5.7

|

|

| | Russian Federation |

5.2

|

-7.8

|

4.5

|

4.3

|

3.4

|

1.5

|

2.3

|

2.9

|

|

| | South Africa |

3.6

|

-1.5

|

3.1

|

3.5

|

2.5

|

2.1

|

3.0

|

3.7

|

|

Source: OECD

Resource security has influenced China’s foreign policy for several years. Their increasing presence in Africa is but one example of this approach. Chinese trade negotiations at a bilateral and multilateral level continue apace. China’s latest economic policies are discussed by Jamestown Foundation – Economic Reform in the Third Plenum: Balancing State and Market –

The new “market-centric” policy suggests more, rather than less, uncertainty for commodity prices: –

The plenum report calls for the market to play a “decisive role” (juedingxing zuoyong) in the allocation of resources in the economy. This represents an elevation from previous party documents, which assigned the market a “fundamental role” (jichuxing zuoyong) in resource allocation. This change in language reflects a step forward in the continued reduction in the number of official price controls. Areas that are specifically targeted in the report include the prices of water, oil, natural gas, electricity, transportation and information technology.

As the private sector gains traction and State Owned Enterprises (SOEs) diminish, better inventory controls are bound to be implemented. Chinese stockpiles of commodities have been a function of SOEs ability to purchase well into the future. The more cash-flow constrained private sector will need to operate more efficiently and with lower stock levels. During the transition I anticipate some reduction in demand. In the past year a moderate slow-down in Chinese growth, combined with a backing-up of US Treasury yields in anticipation of the tapering of QE has put significant downward pressure on a broad array of industrial commodities. With stronger growth forecast for next year demand may lead to an increase in prices but the structural rebalancing towards the private sector is a strong counter-factor.

Energy – supply

On the supply side, starting with Oil, Gas and Coal are the OPEC members, Russia and USA – though it is worth noting that China is the fifth largest Oil producer. Recent price action in Crude Oil has been puzzling in that the price rallied following the recent Iranian peace deal. The European Council for Foreign Relations – The Gulf and sectarianism – give some insight into the increased risk that the recent agreement has created, however, it goes on to look at Shiite/Sunni tensions throughout the whole middle eastern region: –

No single country is considered to do more to propagate sectarianism than Saudi Arabia. As Andrew Hammond writes in his essay in this issue of Gulf Analysis, the Saudi royal family sees itself as the rightful inheritor and guardian of Islamic orthodoxy. Saudi Arabia’s formal interpretation of Islam is ideologically sectarian, condemning all other traditional schools of Islamic thought and religious communities as heresy. The state and private citizens put millions every year into evangelism (known in Arabic as da’wa), the establishment of schools and mosques worldwide and financial support to print and broadcast media that promote its interpretation of Islam.

As Shiite communities inside Saudi Arabia and around it constitute the largest and most organised group of such “heretics”, it deliberately subjects them to particularly stringent criticism and discrimination. Even before the Arab Awakening, the rise of an Islamist, Shiite Iran, and then a Shiite Iraq had already posed a serious threat to a Saudi and Wahhabi influence over the region.

The full article can be found here: –

http://ecfr.eu/page/-/ECFR91_GULF_ANALYSIS_AW.pdf

The oil price appears to be trapped in a virtuous/vicious circle: a collapse in the oil price will exacerbate sectarian tensions prompting a rise in the price of oil. Only a significant slowdown in global demand is likely to change this dynamic.

Of course, there are other geopolitical flashpoints; Russia – as they approach the winter Olympics – the South China Sea (as discussed last week) but the disruption to energy supplies created by a new Middle Eastern conflict would probably cause the largest immediate damage to global growth. Returning to the UN paper, the “Oil Cycle” tends to be “contra” to other commodities; rising oil prices are often referred to as a tax on consumption. It may also go some way to explaining the relatively strong performance of oil in 2013 despite significant increases in fracking production and continuous improvement in drilling techniques. The chart below shows the relative strength of oil since the Great Recession began.

.

.

.

Source: infomine.com

Natural Gas in the US is a “local” market due to US restrictions on the issue of export licenses and the significant cost of gas liquefaction. In Europe, Russia is the dominant player. Russian gas prices have been relatively stable this year, although they have rebounded more strongly than US Natural Gas since 2008.

The recent surge in US gas prices is a response to regional weather conditions. It’s worth noting that US Natural Gas prices tend to be either non or negatively correlated to the price of WTI. Overall supply is increasing and as the government issues more LNG licenses – longer-term I expect prices to remain subdued.

.

.

.

Source: infomine.com

Coal has remained subdued in the US and elsewhere during 2013. China is the largest producer followed by the US, India, Australia and Russia. Thermal Coal has rallied recently in response to the spike in Natural Gas but, barring a significant increase in global demand, I don’t envisage a marked increase in prices in 2014.

.

.

.

Source: infomine.com

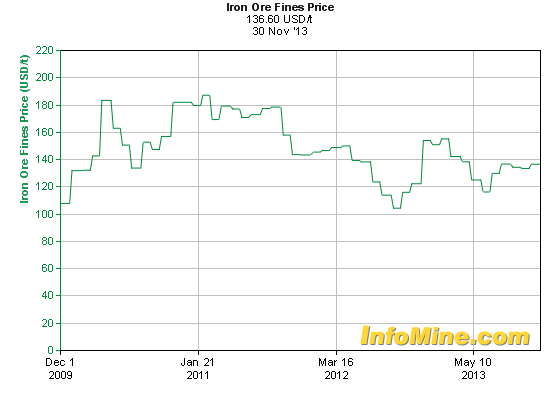

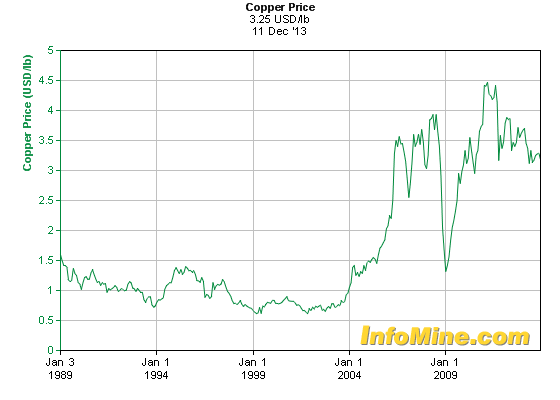

Industrial metals – Supply

Among the industrial metals I will focus on Iron Ore/Steel and Copper. These form the basis for a large swathe of industrial activity. The largest producers of Iron Ore are China, Australia, Brazil, India and Russia. By contrast global copper production is dominated by Chile which produces around 5 mln tons (USA is next with just over 1 mln tons).

.

.

.

Source: infomine.com

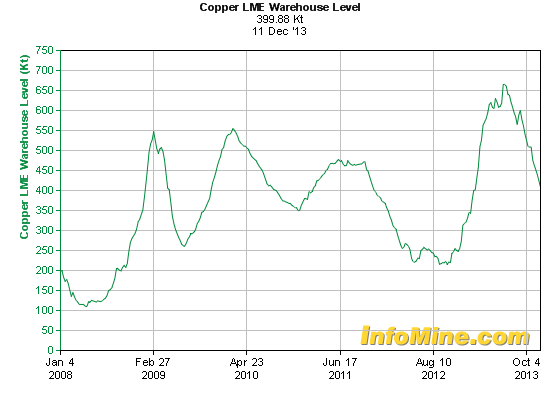

Iron Ore has reflected the moribund state of global demand since the start of the great recession. Copper has recovered from its 2009 lows but further upside impetus is lacking. This may have been due to the high levels of stock, however, during the last six months these stock levels have started to decline. A small increase in demand could lead to a significant re-rating.

.

.

.

Source: infomine.com

Precious Metals – supply

The precious metals complex is dominated by Gold and 2013 has been a difficult year for the “Gold-bugs” as central banks continue adding liquidity but gold prices fail to respond. So much has been written about this subject that I feel I can add little to the debate except to note that the disparity between paper gold (ETFs and Certificate) appear to be at an unusually large discount to physical gold – especially in India and China. For more insights into the arcana of the gold leasing market, I refer you to an excellent article by Gold Money’s Alasdair Macleod – There’s too little gold in the West – published by the Cobden Centre: –

http://www.cobdencentre.org/?s=There+is+too+little+gold+in+the+West+

Here is his typically bullish dénouement: –

Bearing in mind Veneroso’s conclusion in 2002 that there must be 10,000-15,000 tonnes out on lease and loan from the central banks at that time, one could imagine that this figure has increased significantly. Officially, the signatories of the Central Bank Gold Agreement, plus the U.S. and U.K. own 20,393 tonnes. A number of other central banks are likely to have been persuaded to “invest” their gold, but this is bound to exclude Russia, China, the Central Asian states, Iran, and Venezuela. Taking these holders out (amounting to about 3,000 tonnes) leaves a balance of 8,401 tonnes for all the rest. If we further assume that half of that has been deposited in London, New York, or Zurich and leased out, that means the total gold leased and available for leasing since 2002 is about 12,000 tonnes. And once that has gone, there is no monetary gold left for the purpose of price suppression.

Could this have disappeared since 2002 at an average rate of 1,000 tonnes per annum? Quite possibly, in which case, the central banks are very close to losing all control over the gold price.

Meanwhile the trend continues lower.

Gold

.

.

.

.

Source: Tradingcharts.com

Agricultural commodities – supply

With the agricultural sector demand is broadly constant although secular trends such as China’s increasing consumption of meat are structurally important. Within the agricultural sector I will review Wheat, Corn and Soybeans. No pork bellies, frozen concentrated orange juice and none of the softs – not because these markets don’t matter but in the interests of brevity.

In June 2013 the Food and Agriculture Organisation (FAO) published their long-term forecast for agricultural production. Here is their press release: –

Global agricultural production is expected to grow 1.5% a year on average over the coming decade, compared with annual growth of 2.1% between 2003 and 2012, according to a new report published by the OECD and FAO today.

Limited expansion of agricultural land, rising production costs, growing resource constraints and increasing environmental pressures are the main factors behind the trend. But the report argues that farm commodity supply should keep pace with global demand.

The OECD-FAO Agricultural Outlook 2013-2022 expects prices to remain above historical averages over the medium term for both crop and livestock products due to a combination of slower production growth and stronger demand, including for biofuels,

The report says agriculture has been turned into an increasingly market-driven sector, as opposed to policy-driven as it was in the past, thus offering developing countries important investment opportunities and economic benefits, given their growing food demand, potential for production expansion and comparative advantages in many global markets.

However, production shortfalls, price volatility and trade disruption remain a threat to global food security. The OECD/FAO Outlook warns: “As long as food stocks in major producing and consuming countries remain low, the risk of price volatility is amplified. A wide-spread drought such as the one experienced in 2012, on top of low food stocks, could raise world prices by 15-40 percent.”

China, with one-fifth of the world’s population, high income growth and a rapidly expanding agri-food sector, will have a major influence on world markets, and is the special focus of the report. China is projected to remain self-sufficient in the main food crops, although output is anticipated to slow in the next decade due to land, water and rural labour constraints.

Presenting the joint report in Beijing, OECD Secretary-General Angel Gurría said: “The outlook for global agriculture is relatively bright with strong demand, expanding trade and high prices. But this picture assumes continuing economic recovery. If we fail to turn the global economy around, investment and growth in agriculture will suffer and food security may be compromised. (Read Mr. Gurría’s speech)”

“Governments need to create the right enabling environment for growth and trade,” he added. “Agricultural reforms have played a key role in China’s remarkable progress in expanding production and improving domestic food security.”

FAO Director-General Jose Graziano da Silva said: “High food prices are an incentive to increase production and we need to do our best to ensure that poor farmers benefit from them. Let’s not forget that 70 percent of the world’s food insecure population lives in rural areas of developing countries and that many of them are small-scale and subsistence farmers themselves.”

He added: “China’s agricultural production has been tremendously successful. Since 1978, the volume of agricultural production has grown almost five fold and the country has made significant progress towards food security. China is on track to achieving the first millennium development goal of hunger reduction.

While China’s production has expanded and food security has improved, resource and environmental issues need more attention. Growth in livestock production could also face a number of challenges. We are happy to work with China to find viable and lasting solutions.”

Developing countries to gain

Driven by growing populations, higher incomes, urbanization and changing diets, consumption of the main agricultural commodities will increase most rapidly in Eastern Europe and Central Asia, followed by Latin America and other Asian economies.

The share of global production from developing countries will continue to increase as investment in their agricultural sectors narrows the productivity gap with advanced economies. Developing countries, for example, are expected to account for 80 percent of the growth in global meat production and capture much of the trade growth over the next 10 years. They will account for the majority of world exports of coarse grains, rice, oilseeds, vegetable oil, sugar, beef, poultry and fish by 2022.

To capture a share of these economic benefits, governments will need to invest in their agricultural sectors to encourage innovation, increase productivity and improve integration in global value chains, FAO and OECD stressed.

Agricultural policies need to address the inherent volatility of commodity markets with improved tools for risk management while ensuring the sustainable use of land and water resources and reducing food loss and waste.

Specifically in the US, droughts and extreme weather conditions have been the principal factors influencing supply. Water remains a scare and undervalued resource but improvements in technology and farming methods are ongoing. Nonetheless, prices for irrigated farm land have been making new highs during the year. Below are a series of Ten Year monthly charts of Wheat, Corn and Soybeans. The price spike of 2008 is evident in each case and the subsequent rally of Corn and Soybeans to make new highs in 2012. However, during 2013, despite another year of droughts, prices have remained subdued. Nonetheless, prices appear to be near to the base of their long-term up-trends.

Wheat

.

.

.

Source:Tradingcharts.com

Corn

.

.

.

Source: Tradingcharts.com

Soybeans

.

.

.

Source: tradingcharts.com

The latest USDA reports (December 2013) can be found here: –

Wheat

http://www.ers.usda.gov/publications/whs-wheat-outlook/whs-13l.aspx

Projected 2013/14 supplies are raised 10 million bushels this month to 3,008 million bushels. Production and carryin stocks are unchanged, but imports are raised to 10 million bushels to 160 million bushels with expected higher hard red spring (HRS) and soft red winter (SRW) imports from Canada, up 5 million bushels each.

Corn

http://www.ers.usda.gov/publications/fds-feed-outlook/fds-13l.aspx

Projected 2013/14 corn use is increased 100 million bushels this month, split evenly between fuel ethanol and exports. Margins have been very favorable for ethanol mills, with higher ethanol and distillers’ dried grains (DDG) prices on the revenue side combined with lower corn prices on the input side. Exports have benefitted from lower corn prices and increased global consumption. Increases in use are offset slightly by a 5-million-bushel increase in projected imports. Production and feed and residual are unchanged. Projected carryout is tighter by 95 million bushels, at 1.8 billion bushels, but still double last season’s estimate of 824 million. The 2013/14 season-average farm price for corn is projected 10 cents lower at the midpoint of $4.40 per bushel, with the range narrowed to $4.05 to $4.75 based on prices reported to date.

World coarse grain production for 2013/14 is projected higher this month led by increases for Canadian corn and barley, Australian barley, and Ukrainian corn. Global coarse grain use prospects increase slightly more than production increases, trimming expected global ending stocks.

Soybeans

http://www.ers.usda.gov/publications/ocs-oil-crops-outlook/ocs-13l.aspx

USDA raised its 2013/14 forecast of U.S. soybean exports this month by 25 million bushels to 1.475 billion. Similarly, 2013/14 exports of soybean meal were forecast 250,000 tons higher to 10.5 million short tons, which prompted an expected increase in the domestic soybean crush by 5 million bushels to 1.69 billion. An improved demand outlook lowered the forecast of season-ending soybean stocks by 20 million bushels this month to 150 million. USDA raised its forecast range for the season-average farm price by 35 cents this month to $11.50-$13.50 per bushel.

For Argentina, area reductions for corn and sunflowerseed led USDA to raise its 2013/14 soybean area estimate by 300,000 hectares this month to 20 million. As a result, Argentine soybean production is forecast 1 million tons higher to 54.5 million metric tons. Additional output of Argentine soybean meal may push exports of the commodity in 2013/14 to a record 29.4 million tons. Yet, Argentine soybean stocks could be higher by next September to 28.5 million tons.

None of these forecasts looks excessively constrained and the proximity to trend-line support makes me cautious in the near-term, a breakdown through the ten year up trend could see a retracement of the entire cycle.

A longer term factor which may yet change this dynamic dramatically is the effect of the “Eddy Minimum”.

For some general background on sunspots and climate, this Princeton University website is a useful resource: –

http://www.princeton.edu/~achaney/tmve/wiki100k/docs/Maunder_Minimum.html

The argument in favour of a cooling of global temperature is not new but for the latest comments on this subject the following website is informative: –

Conclusion

Throughout 2013 I waited for a resumption of the commodity bull-trend, expecting that the pick-up in economic activity, combined with the provision of central bank liquidity, would fuel the next leg of the super-cycle. It never materialised. Global growth remained subdued, China switched to a policy of “quality not quantity” and “taper terror” in the US, increased deflation expectations: and revealed weaknesses in a number of emerging markets. Even in the agricultural sector, weather related stress failed to materially reverse the downward pressure on prices.

Looking ahead to 2014 I can see little reason, thus far, to be broadly long commodities – as mentioned at the beginning I encourage all investors to view each market on its own particular merits. However, just like 2013, I am waiting for bearish sentiment to turn. To misquote St Augustine’s teenage prayer “Give me commodities Lord, but not yet!”

I’ll be back in mid January. With best wishes for the festive season and New Year. Col

Pingback: Emerging Markets and disinflation in developed economies | In the Long Run

Exceptional post but I wwas wondering iff yoou could write a litte more oon this

subject? I’d bee veery thankful iif yyou could elablrate a littlee bit further.

Cheers!

Hi Desiree,

A little more commodity related content today.

Cheers,

Col

Pingback: How do we square the decline in trade with the rebound in industrial commodities? – In the Long Run